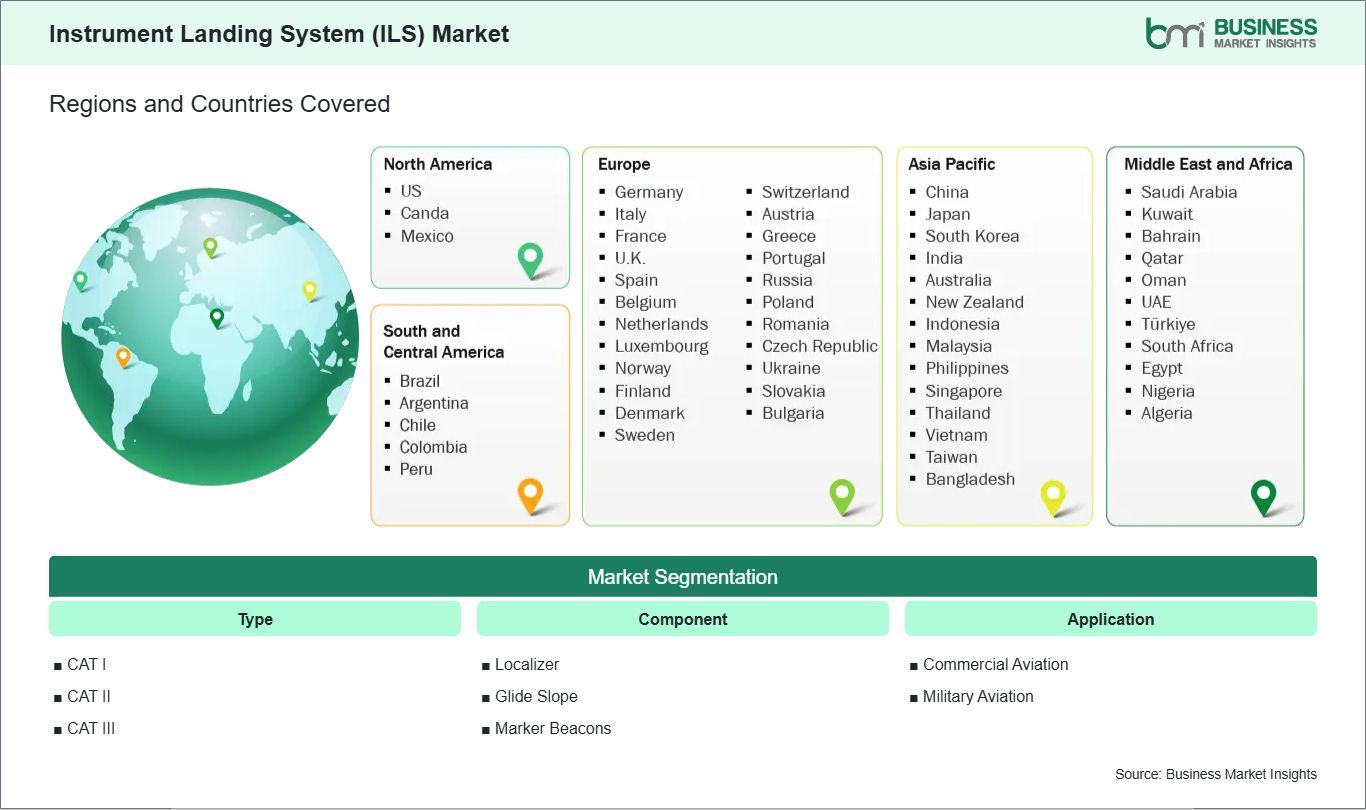

The Instrument Landing System (ILS) market shows diverse regional adoption patterns influenced by airport modernization priorities, regulatory operating standards, runway traffic density, and the need for dependable low-visibility landing support. Across the global market, replacement of aging navigation infrastructure remains a central theme, particularly where operators are aligning airfield systems with broader safety, continuity, and lifecycle management objectives. Procurement patterns also reflect differences in runway complexity, weather exposure, and institutional funding structures.

North America maintains a mature operating environment shaped by established airport networks, demanding compliance regimes, and sustained attention to navigation resilience. Investment emphasis in this region often centers on renewal of legacy installations, calibration quality, and integration with wider air traffic modernization programs. Commercial hubs value ILS for operational continuity during weather disruption, while military airfields prioritize deployability, equipment integrity, and dependable landing assurance across fixed and expeditionary settings.

Asia Pacific reflects a more expansion-oriented landscape, supported by airport capacity development, runway additions, and infrastructure upgrades across both established and emerging aviation markets. Regional demand is reinforced by the operational importance of precision approach capability at high-throughput airports exposed to seasonal visibility constraints. The market also benefits from long-term investment in civil aviation networks, creating room for both new installations and selective upgrades that strengthen runway performance and service reliability.

Europe continues to emphasize certified performance, maintenance discipline, and modernization of precision approach systems within complex regulatory environments. Emerging markets across the Middle East, Africa, and South and Central America present a different growth profile, where airport development programs, runway rehabilitation, and air connectivity objectives shape procurement decisions. In these regions, ILS investment is often linked to broader capability expansion, making system reliability, technical support, and long-term maintainability especially relevant.