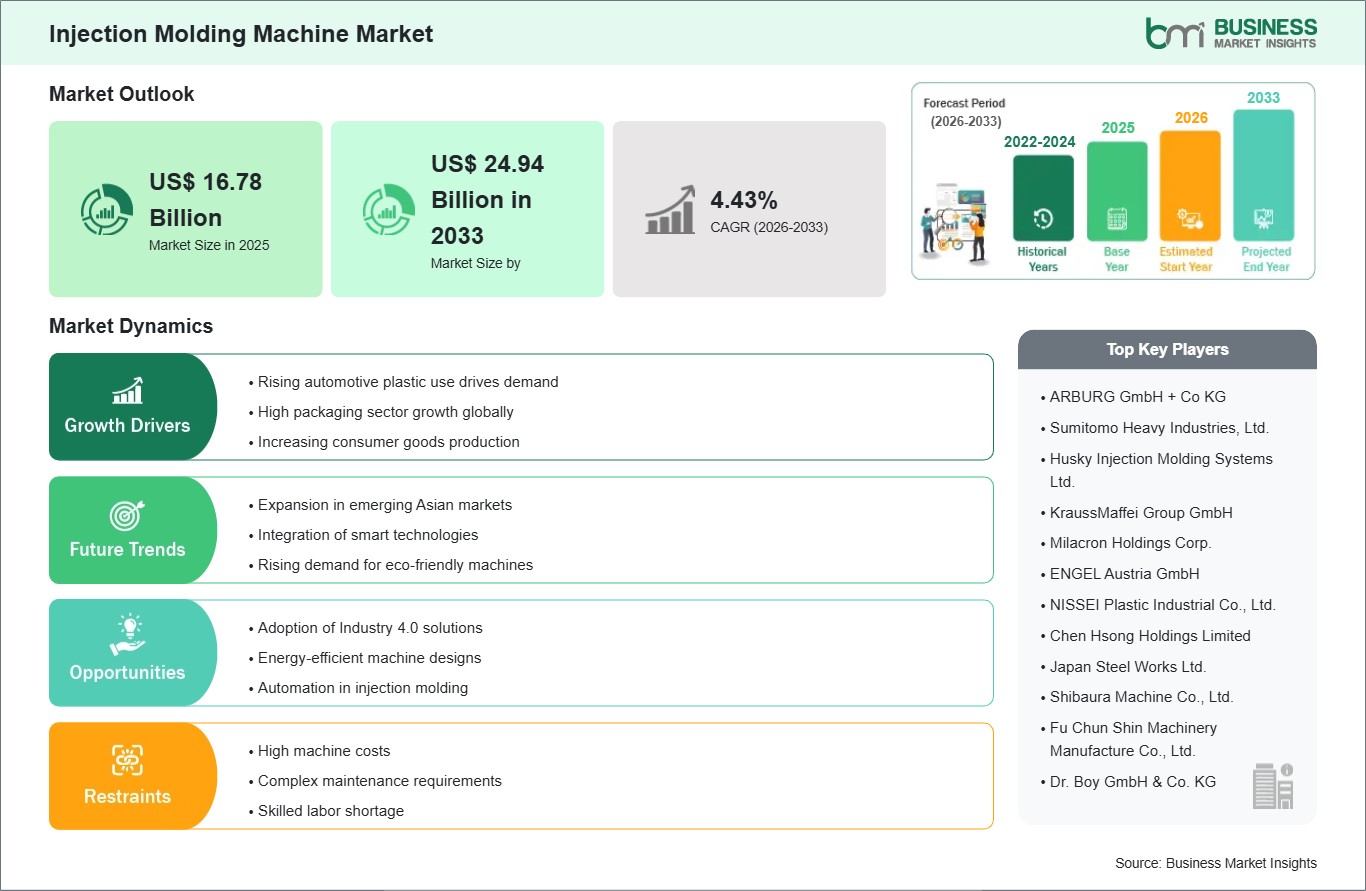

The injection molding machine market size is expected to reach US$ 24.94 Billion by 2033 from US$ 16.78 Billion in 2025. The market is estimated to record a CAGR of 4.43% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Injection molding machines are industrial systems that melt material, inject it into a mold cavity, and form repeatable components with controlled geometry. Their role spans high-volume manufacturing where dimensional consistency, cycle efficiency, and process stability determine production economics. These machines support a broad set of molded products used across transport, medical, packaging, electronics, and household applications. As manufacturing priorities shift toward precision and throughput, the category remains central to modern polymer processing operations.

Market momentum is shaped by the need for efficient part production, lower scrap rates, and improved machine control across demanding output environments. Automotive manufacturers require repeatable molding for structural and interior components, while packaging converters prioritize speed and cavity performance for continuous runs. Medical and electronics producers emphasize process accuracy and cleanliness, which supports machine upgrades that improve monitoring, clamping response, and injection consistency. These requirements collectively sustain equipment replacement and capacity expansion decisions.

Within segmentation, hydraulic systems retain relevance where robust force delivery and established plant familiarity matter, while electric systems gain preference in precision-oriented and energy-conscious settings. Hybrid platforms bridge performance requirements by combining control advantages with practical operating flexibility. On the demand side, automotive and packaging remain prominent application areas because both require dependable volume output and consistent molding quality. End-user adoption also reflects broader manufacturing priorities tied to healthcare, consumer electronics, and electrical equipment production.

Technology evolution is steadily redefining machine value beyond basic molding capability. Greater use of servo systems, digital interfaces, process analytics, and integrated automation is improving repeatability while simplifying production oversight. Manufacturers are refining machine architectures to support tighter tolerances, faster setup adjustment, and better compatibility with application-specific tooling needs. This progression is particularly relevant in sectors that require shorter validation cycles, more stable quality output, and greater visibility into shop-floor performance.

Competition in this sector is shaped by engineering depth, machine reliability, service responsiveness, and the ability to address distinct production environments. Suppliers differentiate through platform breadth, automation compatibility, and specialization across packaging, medical, and industrial molding requirements. Market positioning also depends on how effectively manufacturers align machine design with customer priorities such as precision, uptime, and lifecycle efficiency. As procurement standards become more technical, competitive advantage increasingly rests on application fit rather than broad equipment availability alone.

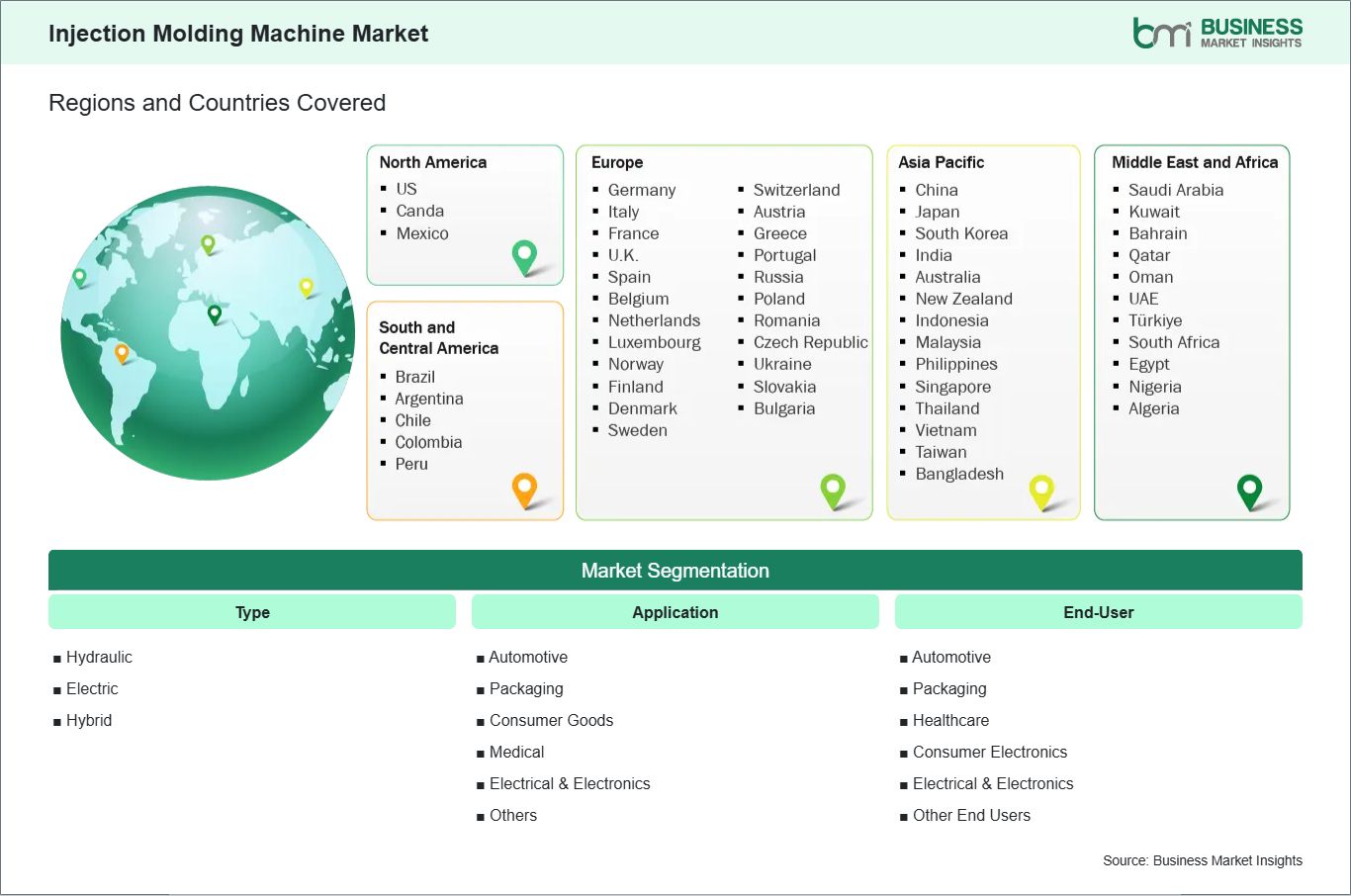

The injection molding machine market is segmented by type, and application. Each category reflects different operating priorities, production settings, and purchasing considerations.

By Type

Hydraulic: Suits heavy-duty molding with strong clamping requirements.

Electric: Enables precise control and cleaner operating conditions.

Hybrid: Balances force capability with improved process responsiveness.

By Application

Automotive: Requires dimensional stability for interior and structural components.

Packaging: Favors fast cycles and consistent multi-cavity output.

Consumer Goods: Supports cost-efficient production across diverse molded formats.

Medical: Demands process accuracy and dependable repeatability.

Electrical & Electronics: Prioritizes fine-feature molding and controlled precision.

Injection Molding Machine Market Drivers and Opportunities:

Need for Precision Manufacturing Across High-Volume End Uses

Manufacturers across automotive, packaging, medical, and electronics are under pressure to produce complex parts with tighter tolerances and stable cycle output. That requirement increases reliance on injection molding machines capable of controlled clamping, repeatable injection, and consistent thermal performance. As product designs become more detailed and production schedules more demanding, buyers move toward machine platforms that can maintain quality across extended runs without compromising operating discipline.

The effect of this requirement is visible in equipment selection criteria across both mature factories and newly commissioned molding lines. Precision capability now influences procurement decisions because scrap reduction, dimensional control, and repeatability directly affect downstream assembly and product acceptance. In this context, injection molding machines are not only production assets but also quality assurance instruments, which reinforces their strategic relevance within high-output manufacturing environments.

Integration of Automation and Digital Process Optimization

A clear opportunity is emerging from the shift toward automated molding cells and digitally supervised production systems. Machine suppliers are embedding smarter controls, data visibility tools, and automation interfaces that simplify repeat setup and operational tracking. These capabilities strengthen use cases in packaging, healthcare, and consumer electronics, where production teams value faster changeovers, cleaner execution, and machine behavior that can be monitored with greater consistency.

Looking ahead, this opportunity extends beyond premium installations and into broader manufacturing modernization programs. Facilities seeking tighter control over uptime, maintenance planning, and process transparency are likely to expand deployment of digitally enabled machines. That progression supports wider market penetration across sectors that prioritized only output volume. Over time, automation-linked machine differentiation can reshape purchasing patterns and create stronger demand for higher-value molding platforms.

Injection Molding Machine Market Size and Share Analysis:

The injection molding machine market size is expected to reach US$ 24.94 Billion by 2033 from US$ 16.78 Billion in 2025. The market is estimated to record a CAGR of 4.43% from 2026 to 2033.

This trajectory indicates measured expansion supported by continuing equipment relevance across manufacturing sectors that require precision molding, repeatable output, and process efficiency. The market is advancing through technology refinement rather than abrupt structural change, which gives growth a stable and equipment-led character.

By type, hydraulic machines maintain a strong position because they remain familiar across established production settings and support demanding force requirements. Electric machines hold notable relevance in precision-centered environments, especially where cleaner operation and control responsiveness matter. Hybrid systems continue to attract attention by combining operational flexibility with improved performance balance, making them suitable for manufacturers that need both productivity and tighter process handling.

Among applications, automotive remains a leading area due to the sustained need for molded interiors, exterior, and under-the-hood components with reliable dimensional performance. Packaging also commands a substantial share because machine uptime, speed, and multicavity consistency are critical in that segment. Medical and electrical applications reinforce market depth by requiring dependable process control, while consumer goods sustain broader equipment utilization across diverse product formats.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

ARBURG GmbH + Co KG

Sumitomo Heavy Industries, Ltd.

Husky Injection Molding Systems Ltd.

KraussMaffei Group GmbH

Milacron Holdings Corp.

ENGEL Austria GmbH

NISSEI Plastic Industrial Co., Ltd.

Chen Hsong Holdings Limited

Japan Steel Works Ltd.

Shibaura Machine Co., Ltd.

Fu Chun Shin Machinery Manufacture Co., Ltd.

Dr. Boy GmbH & Co. KG

WITTMANN BATTENFELD GmbH

Get more information on this report

Injection Molding Machine Market Report Coverage and Deliverables:

The " Injection Molding Machine Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

The injection molding machine market shows diverse regional adoption patterns influenced by industrial maturity, end-use specialization, production economics, and equipment modernization priorities. Across the global landscape, purchasing behavior reflects the balance between replacement demand in established manufacturing hubs and new capacity requirements in expanding processing centers. The market also responds to differences in automation readiness, machine preference, and sector mix, which together create distinct regional trajectories for equipment selection and deployment.

North America maintains a strong market position because manufacturers place considerable emphasis on process reliability, plant productivity, and equipment capability aligned with technical applications. Demand is supported by packaging, medical manufacturing, and automotive supply chains that require repeatable output and responsive machine control. Buyers in this region also show interest in automation compatibility and lifecycle efficiency, which sustains attention toward advanced machine platforms rather than purely cost-led procurement decisions.

Asia Pacific presents the broadest manufacturing intensity for this sector, supported by extensive plastics processing activity and large downstream consumption across packaging, electronics, automotive, and household goods. The region benefits from established machine production ecosystems as well as continued industrial build-out in several economies. Purchasing patterns range from volume-focused installations to technologically upgraded systems, giving the market a layered structure where both capacity expansion and machine advancement remain commercially relevant.

Europe retains importance through its concentration of engineering-driven manufacturing and preference for high-performance equipment in precision applications. Efficiency, process control, and machine sophistication remain central considerations across regional buyers. Beyond Europe, emerging markets in the Middle East, Africa, and South and Central America are developing their role through industrial diversification, packaging demand, and localized production initiatives. These markets may differ in scale, yet they collectively widen the long-term addressable base for injection molding machine suppliers.

Get more information on this report

Injection Molding Machine Market Research Report Guidance:

The report includes qualitative and quantitative data in the market across type, application, and end-user and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by type, application, and end-user and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Injection Molding Machine Market News and Key Development:

Recent developments in the injection molding machine market reflect portfolio expansion, consolidation, and technology-focused positioning across equipment suppliers.

These updates indicate continued focus on capability enhancement and strategic transactions within the sector.

In August 2025, KraussMaffei is setting a milestone in the processing of fiber-reinforced thermoplastics. This innovative process enables the direct, fiber-friendly compounding of polypropylene (PP) and chopped glass fibers in the injection molding process for the first time. Visitors to K can experience the CFP technology live at the exhibition stand: A GX 650-4300 with the new LRXplus 350 linear robot is producing a complex tailgate component for the automotive industry.

In April 2026, ENGEL is expanding its direct presence in the Spanish market by rebranding of its former sales partner Roegele as ENGEL Spain. Since 1 April, the company has been represented in Spain by its own subsidiary. For local plastics processors, this combines the continuity of a team established on the ground for decades with direct access to the technology, service and solutions portfolio of the global ENGEL Group from injection moulding machines and automation to digital assistance systems.

Key Sources Referred:

World Bank -Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Injection Molding Machine Market

ARBURG GmbH + Co KG

Sumitomo Heavy Industries, Ltd.

Husky Injection Molding Systems Ltd.

KraussMaffei Group GmbH

Milacron Holdings Corp.

ENGEL Austria GmbH

NISSEI Plastic Industrial Co., Ltd.

Chen Hsong Holdings Limited

Japan Steel Works Ltd.

Shibaura Machine Co., Ltd.

Fu Chun Shin Machinery Manufacture Co., Ltd.

Dr. Boy GmbH & Co. KG

WITTMANN BATTENFELD GmbH

Frequently Asked Questions

How big is the Injection Molding Machine Market?

The Injection Molding Machine Market is valued at US$ 16.78 Billion in 2025, it is projected to reach US$ 24.94 Billion in 2033 by .

What is the CAGR for Injection Molding Machine Market by (2026 - 2033)?

As per our report Injection Molding Machine Market, the market size is valued at US$ 16.78 Billion in 2025, projecting it to reach US$ 24.94 Billion in 2033 by . This translates to a CAGR of approximately 4.43% during the forecast period.

What segments are covered in this report?

The Injection Molding Machine Market report typically cover these key segments-

End-User (Automotive, Packaging, Healthcare, Consumer Electronics, Electrical & Electronics, Other End Users)

What is the historic period, base year, and forecast period taken for Injection Molding Machine Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Injection Molding Machine Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Injection Molding Machine Market?

The Injection Molding Machine Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

ARBURG GmbH + Co KG

Sumitomo Heavy Industries, Ltd.

Husky Injection Molding Systems Ltd.

KraussMaffei Group GmbH

Milacron Holdings Corp.

ENGEL Austria GmbH

NISSEI Plastic Industrial Co., Ltd.

Chen Hsong Holdings Limited

Japan Steel Works Ltd.

Shibaura Machine Co., Ltd.

Fu Chun Shin Machinery Manufacture Co., Ltd.

Dr. Boy GmbH & Co. KG

WITTMANN BATTENFELD GmbH

Who should buy this report?

The Injection Molding Machine Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Injection Molding Machine Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Injection Molding Machine Market

Get Free Sample For Injection Molding Machine Market