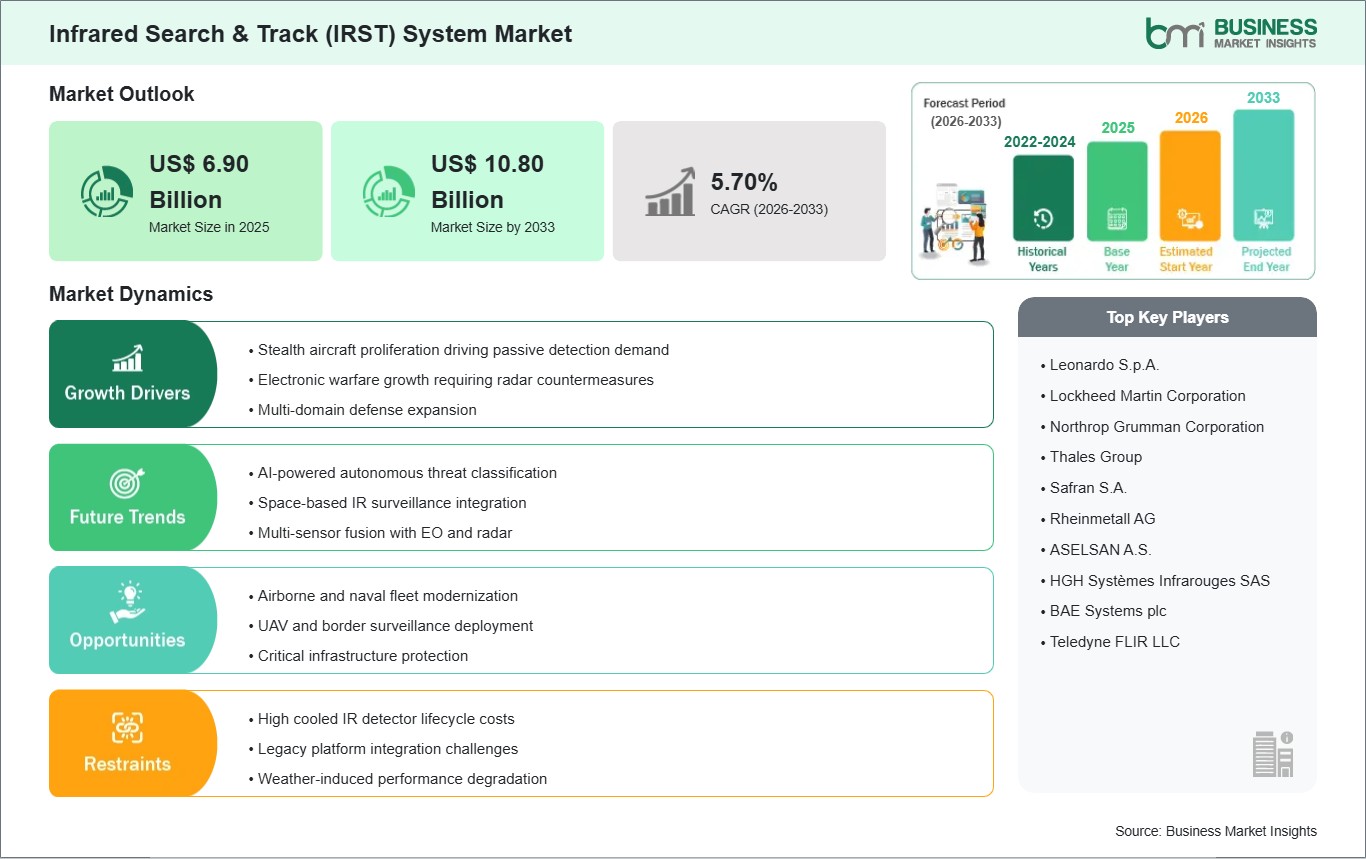

The Infrared Search & Track (IRST) System market size is expected to reach US$ 10.80 Billion by 2033 from US$ 6.90 Billion in 2025. The market is estimated to record a CAGR of 5.70% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Infrared search and track systems are passive electro-optical sensing platforms designed to detect, localize, and follow heat signatures from aircraft, missiles, vessels, and ground threats without emitting radio frequency energy. Their operating value lies in covert surveillance, resistance to electronic jamming, and compatibility with layered targeting architectures used across contested environments.

Procurement momentum reflects the defense sector’s preference for passive sensing tools that complement radar in dense electronic warfare settings. Programs focused on stealth detection, long-range air defense, maritime domain awareness, and border monitoring are widening deployment scope across airborne, naval, and land platforms. This expansion is further supported by modernization cycles that prioritize sensor fusion and survivability.

Platform segmentation shows airborne systems retaining the broadest operational relevance because fighter aircraft and special mission platforms require persistent passive target tracking. Naval installations remain important for horizon surveillance and threat cueing, while land-based deployments support perimeter security and mobile battlefield observation. On the technology side, cooled IR detectors maintain preference where range, sensitivity, and target discrimination are mission-critical.

Engineering progress is improving signal processing, multispectral imaging, stabilization, and integration with mission computers. These refinements strengthen target recognition quality while reducing false alarms in cluttered backgrounds. As architectures become more modular, the industry is moving toward adaptable configurations that fit both new-build defense platforms and upgrade pathways for legacy fleets.

Competitive conditions are shaped by platform qualification requirements, defense procurement timelines, and the ability to align sensor performance with operational doctrines. Suppliers that can deliver compact designs, robust tracking algorithms, and integration readiness for broader combat systems are positioned to secure program continuity as procurement agencies emphasize mission resilience over stand-alone sensor performance.

Infrared Search & Track (IRST) System Market - Strategic Insights:

Get more information on this report

Infrared Search & Track (IRST) System Market Segmentation Analysis:

The market is segmented by platform, technology, and end-user based on deployment architecture and mission requirements.

By Platform

Airborne: Dominates procurement through fighter integration and long-range passive target tracking.

Naval: Supports discreet horizon scanning and maritime threat cueing.

Land: Extends battlefield observation for mobile and fixed surveillance roles.

By Technology

Cooled IR Detectors: Preferred for superior sensitivity in extended-range defense missions.

Uncooled IR Detectors: Favored where compact design and lower maintenance are priorities.

By End-User

Military & Defense: Accounts for the core installed base across combat and surveillance platforms.

Civil & Commercial: Emerging in specialized monitoring and security-oriented applications.

Infrared Search & Track (IRST) System Market Drivers and Opportunities:

Rising Emphasis on Passive Threat Detection in Contested Environments

Modern defense planning increasingly prioritizes sensors that operate without disclosing platform position. That requirement has strengthened demand for IRST systems because they detect thermal signatures without active emissions. As radar denial, electronic attack, and low-observable aircraft become more relevant to mission planning, procurement teams are aligning surveillance investments with passive sensing architectures that preserve tactical discretion.

This transition influences acquisition priorities across air, sea, and land domains. Defense operators view IRST integration as a practical method to strengthen target tracking continuity when conventional detection channels are degraded. Its relevance rises in scenarios requiring early cueing, layered situational awareness, and interoperability with fire-control and mission management systems, making the technology strategically important for force modernization programs.

Expansion of Multi-Platform Sensor Fusion and Upgrade Programs

A notable opportunity is emerging through sensor fusion programs that combine infrared tracking with radar, electronic support measures, and mission software. This trend is encouraging modular IRST configurations that can be installed on new platforms or retrofitted onto existing fleets. Such flexibility improves operational value while enabling defense agencies to extend capability without fully redesigning platform architectures.

Future scope is broadening as upgrade cycles extend beyond fighter aircraft into naval combatants, ground surveillance units, and specialized security applications. Expanding deployment pathways support broader supplier participation in mission computing, optics, and software subsystems. Over time, this convergence can strengthen market depth by linking passive detection capability with wider command, control, and targeting ecosystems.

Infrared Search & Track (IRST) System Market Size and Share Analysis:

The Infrared Search & Track (IRST) System market size is expected to reach US$ 10.80 Billion by 2033 from US$ 6.90 Billion in 2025. The market is estimated to record a CAGR of 5.70% from 2026 to 2033. This trajectory reflects steady procurement activity tied to defense modernization, passive sensing requirements, and broader integration of infrared surveillance within multi-layered combat systems.

By platform, airborne systems hold the leading position because combat aircraft and mission platforms depend on passive detection during complex operational scenarios. By technology, cooled IR detectors maintain the stronger position due to their higher sensitivity, longer detection reach, and suitability for advanced defense applications that require precise thermal discrimination.

By application, military and defense remains the dominant end-user environment, supported by sustained investment in surveillance, targeting, and battlespace awareness. Civil and commercial participation remains comparatively limited, though specialized security, monitoring, and infrastructure protection uses create a gradual pathway for selective expansion beyond traditional defense procurement.

Infrared Search & Track (IRST) System Market Report Highlights:

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Leonardo S.p.A.

Lockheed Martin Corporation

Northrop Grumman Corporation

Thales Group

Safran S.A.

Rheinmetall AG

ASELSAN A.S.

HGH Systèmes Infrarouges SAS

BAE Systems plc

Teledyne FLIR LLC

Get more information on this report

Infrared Search & Track (IRST) System Market Report Coverage and Deliverables:

The "Infrared Search & Track (IRST) System Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering the areas below:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Infrared Search & Track (IRST) System Market Geographic Insights:

The Infrared Search & Track (IRST) System market shows diverse regional adoption patterns influenced by defense modernization priorities, threat perception, platform readiness, and procurement frameworks. Across the global landscape, adoption is shaped by how armed forces balance passive surveillance requirements with broader command, control, and targeting integration objectives.

North America maintains a strong position due to established aerospace manufacturing capabilities, advanced combat aviation programs, and sustained spending on sensor resilience in electronically contested environments. Procurement emphasis in this region centers on integrating passive detection alongside radar and mission systems, supporting operational flexibility across air and naval defense architectures.

Asia Pacific presents a dynamic growth environment as regional security concerns encourage investment in airborne surveillance, coastal defense, and integrated battlefield awareness. Countries across the region are strengthening indigenous defense manufacturing while also expanding procurement partnerships, creating favorable conditions for IRST deployment on aircraft, maritime assets, and selective land-based systems.

Europe continues to advance through combat aircraft upgrade programs, cross-border defense collaboration, and emphasis on passive sensing against low-observable threats. Emerging markets in the Middle East, Africa, and South and Central America show more selective uptake, typically aligned with perimeter security, air defense enhancement, and modernization of strategic surveillance assets where operational discretion is a priority.

Get more information on this report

Infrared Search & Track (IRST) System Market Research Report Guidance:

The report encompasses both qualitative and quantitative data pertaining to the market, categorized by platform, technology, and end-user, and geographical regions.

Beginning with Chapter 2, the report presents key takeaways that underscore the primary trends and market outlook.

Chapter 3 is dedicated to outlining the research methodology employed in this study.

In Chapter 4, an ecosystem analysis is provided.

Chapter 5 delves into the significant industry dynamics affecting the market, including driving factors, existing challenges, potential opportunities, and emerging trends. This section also includes an impact analysis of these drivers and constraints.

Chapter 6 reviews the market scenario, detailing historical revenue figures and forecasts extending to the year 2033.

Chapters 7 through 10 analyze market segments based on platform, technology, and end-user, and geography, covering regions such as North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. These chapters include market revenue data, forecasts, and driving factors.

Chapter 11 presents a competitive analysis, featuring a heat map of key players within the market.

Chapter 12 offers an industry landscape analysis, detailing business activities such as market initiatives, recent developments, mergers, and joint ventures on a global scale, alongside a competitive overview.

In Chapter 13, comprehensive profiles of major companies operating in the market are provided. These profiles include key facts, business descriptions, product and service offerings, financial overviews, SWOT analyses, and significant developments.

Finally, Chapter 14, the appendix, includes a brief company overview, a list of abbreviations, and a disclaimer.

Infrared Search & Track (IRST) System Market News and Key Development:

The Infrared Search & Track (IRST) System Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In February 2025, The U.S. Navy has declared Initial Operating Capability (IOC) status for a new infrared search-and-track (IRST) sensor system developed by Lockheed Martin(NYSE:LMT) for F/A-18 Super Hornet strike fighters. At the core of this innovative system is IRST21, Lockheed Martin’s long-wave infrared search-and-track sensor that passively detects airborne targets well beyond visual range. For Naval Aviators,this new capability is expected to enhance the F/A-18 platform's effectiveness and improve mission survivability.

In October 2025, Lockheed Martin (NYSE: LMT) has been awarded a $233 million firm-fixed-price contract to deliver IRST21 Block II systems and initial spares to the U.S. Navy and Air National Guard (ANG).

Key Sources Referred:

World Bank: Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Infrared Search & Track (IRST) System Market

Leonardo S.p.A.

Lockheed Martin Corporation

Northrop Grumman Corporation

Thales Group

Safran S.A.

Rheinmetall AG

ASELSAN A.S.

HGH Systèmes Infrarouges SAS

BAE Systems plc

Teledyne FLIR LLC

Frequently Asked Questions

How big is the Infrared Search & Track (IRST) System Market?

The Infrared Search & Track (IRST) System Market is valued at US$ 6.90 Billion in 2025, it is projected to reach US$ 10.80 Billion by 2033.

What is the CAGR for Infrared Search & Track (IRST) System Market by (2026 - 2033)?

As per our report Infrared Search & Track (IRST) System Market, the market size is valued at US$ 6.90 Billion in 2025, projecting it to reach US$ 10.80 Billion by 2033. This translates to a CAGR of approximately 5.70% during the forecast period.

What segments are covered in this report?

The Infrared Search & Track (IRST) System Market report typically cover these key segments-

Platform (Airborne, Naval, Land)

Technology (Cooled IR Detectors, Uncooled IR Detectors)

End-User (Military & Defense, Civil & Commercial)

What is the historic period, base year, and forecast period taken for Infrared Search & Track (IRST) System Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Infrared Search & Track (IRST) System Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Infrared Search & Track (IRST) System Market?

The Infrared Search & Track (IRST) System Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Leonardo S.p.A.

Lockheed Martin Corporation

Northrop Grumman Corporation

Thales Group

Safran S.A.

Rheinmetall AG

ASELSAN A.S.

HGH Systèmes Infrarouges SAS

BAE Systems plc

Teledyne FLIR LLC

Who should buy this report?

The Infrared Search & Track (IRST) System Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Infrared Search & Track (IRST) System Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Infrared Search & Track (IRST) System Market

Get Free Sample For Infrared Search & Track (IRST) System Market