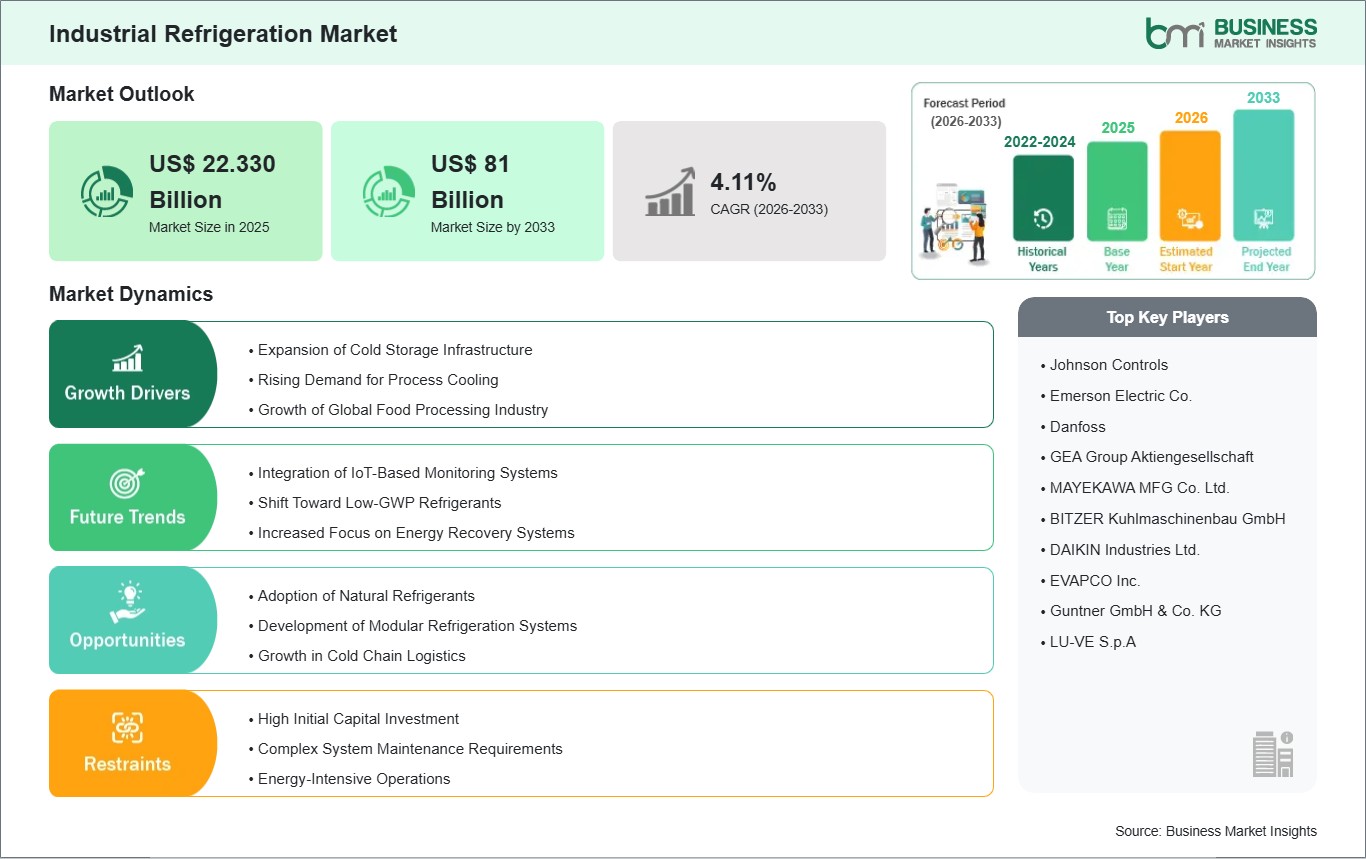

The Industrial Refrigeration Market size is expected to reach US$ 81 Billion by 2033 from US$ 22.330 Billion in 2025. The market is estimated to record a CAGR of 17.48% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global industrial refrigeration market is experiencing consistent growth, propelled by the expansion of the cold chain logistics sector, stringent food safety regulations, and increasing demand from processing industries. Industrial refrigeration systems are critical for preserving perishable goods, maintaining precise temperatures in chemical processes, and supporting large-scale storage and distribution networks.

Key drivers include the rapid growth of the organized food retail and processing sector, which demands reliable and efficient cold storage, and the global pharmaceutical industry's need for temperature-controlled supply chains. Furthermore, the enforcement of international environmental regulations, such as the Kigali Amendment, is accelerating the transition to low-GWP (Global Warming Potential) refrigerants. The market faces challenges such as high initial capital investment, complex system maintenance, and the ongoing phasedown of hydrofluorocarbon (HFC) refrigerants. However, significant opportunities are emerging from technological advancements in energy-efficient compressors and heat exchangers, the integration of IoT for predictive maintenance, and the rising demand for natural refrigerant-based systems in sustainable cold chain infrastructure.

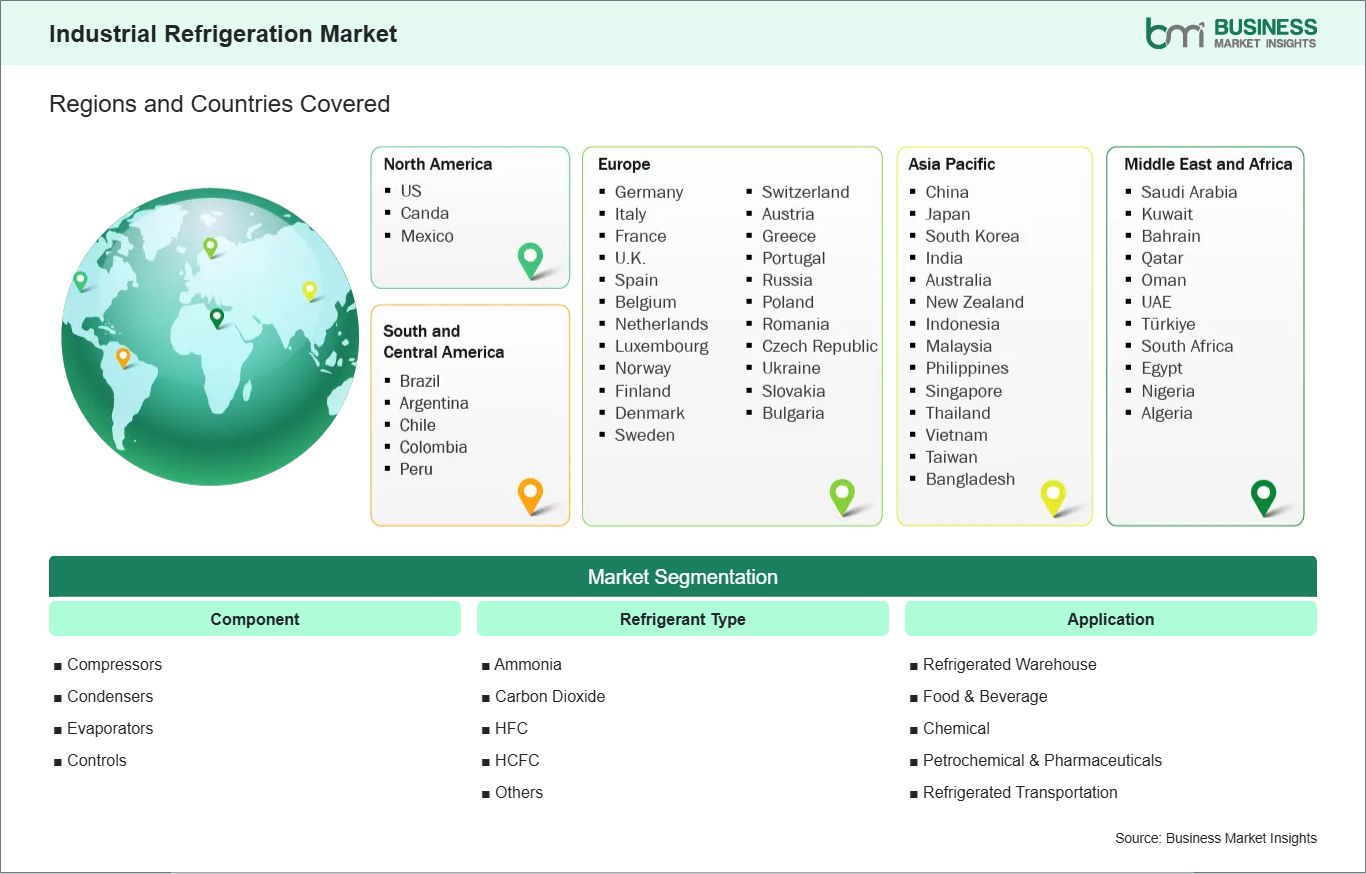

Key segments that contributed to the derivation of the industrial refrigeration market analysis are component, refrigerant type, and application.

By component, the industrial refrigeration market is segmented into compressors, condensers, evaporators, and controls. The compressors segment dominated the market in 2024.

By refrigerant type, the market is classified into ammonia, carbon dioxide, HFC, HCFC, and others. The ammonia segment held the largest share in the industrial refrigeration market in 2024.

By application, the market includes refrigerated warehouse, food & beverage, chemical, petrochemical & pharmaceuticals, and refrigerated transportation. The food & beverage segment held the largest share in the industrial refrigeration market in 2024.

Industrial Refrigeration Market Drivers and Opportunities:

Expansion of Cold Chain Logistics and Food Safety Standards

The relentless global expansion of cold chain logistics, driven by rising consumer demand for perishable foods, pharmaceuticals, and vaccines, represents a primary growth engine for the industrial refrigeration market. Stringent international food safety standards and regulations mandate consistent temperature control from production to point-of-sale, necessitating robust refrigeration systems in processing plants, distribution centers, and refrigerated transportation. The growth of e-commerce grocery delivery and the globalization of food supply chains further amplify this demand. This trend is not only increasing the volume of new system installations but also driving the modernization and expansion of existing refrigerated warehouse and transport fleets, creating sustained, long-term demand for efficient and reliable industrial refrigeration solutions across the entire value chain.

Transition to Natural and Low-GWP Refrigerants

The global push for environmental sustainability and regulatory compliance is creating a substantial opportunity centered on the transition away from synthetic, high-GWP refrigerants. International agreements like the Kigali Amendment to the Montreal Protocol are mandating the phasedown of HFCs, compelling industries to adopt eco-friendly alternatives. This regulatory shift is accelerating investment in systems designed for natural refrigerants such as ammonia (R717) and carbon dioxide (R744), which have minimal ozone depletion and global warming impact. This transition drives demand for new, specially engineered components, system retrofits, and entirely new installations. It fosters innovation in system design for safety and efficiency, opens new service and maintenance revenue streams, and allows technology leaders to capture market share by offering future-proof, compliant, and sustainable refrigeration solutions.

Industrial Refrigeration Market Size and Share Analysis:

Based on component, the industrial refrigeration market is segmented into compressors, condensers, evaporators, and controls. Compressors lead the segment as they are the core energy-consuming component of any refrigeration cycle, with continuous innovation focused on improving their efficiency, variable-speed operation, and reliability across diverse industrial applications.

Based on refrigerant type, the market is classified into ammonia, carbon dioxide, HFC, HCFC, and others. Ammonia remains the dominant refrigerant for large-scale industrial applications due to its superior thermodynamic properties, zero ODP (Ozone Depletion Potential), and low cost, though carbon dioxide systems are experiencing faster growth driven by sustainability mandates in commercial and sub-industrial applications.

By application, the market includes refrigerated warehouse, food & beverage, chemical, petrochemical & pharmaceuticals, and refrigerated transportation. The food & beverage sector continues to be the largest segment, fueled by global population growth and changing consumption patterns. The chemical & pharmaceutical segment is also significant, requiring highly precise and reliable temperature control for production and storage processes.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Johnson Controls

Emerson Electric Co.

Danfoss

GEA Group Aktiengesellschaft

MAYEKAWA MFG Co. Ltd.

BITZER Kuhlmaschinenbau GmbH

DAIKIN Industries Ltd.

EVAPCO Inc.

Guntner GmbH & Co. KG

LU-VE S.p.A

Get more information on this report

Industrial Refrigeration Market Report Coverage and Deliverables:

The Industrial Refrigeration Market Size and Forecast (2022–2033) report provides a detailed analysis of the market covering below areas:

Industrial Refrigeration Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Industrial Refrigeration Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Industrial Refrigeration Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the industrial refrigeration market

Detailed company profiles, including SWOT analysis

The Asia-Pacific region is the largest and fastest-growing market for industrial refrigeration, driven by its rapidly expanding food processing sector, massive investments in cold storage infrastructure, and growing pharmaceutical manufacturing. Countries such as China, India, Japan, and Southeast Asian nations are witnessing booming demand for refrigerated warehouses and transportation to support domestic consumption and agricultural exports, supported by government initiatives to reduce food waste and improve food security.

North America remains a mature yet technologically advanced market, characterized by stringent FDA and USDA regulations that mandate high standards for food safety and cold chain integrity. The United States and Canada have well-established, large-scale cold storage networks. They are early adopters of energy-efficient and natural refrigerant technologies, driven by sustainability goals and the need to modernize aging infrastructure.

Europe represents a highly regulated and innovation-focused market, where strict environmental directives like the F-Gas Regulation are accelerating the shift to low-GWP refrigerants. Germany, France, the United Kingdom, and Italy lead the region with advanced food & beverage and pharmaceutical industries that demand precise, reliable, and eco-friendly refrigeration solutions, fostering a strong market for system upgrades and new sustainable installations.

Get more information on this report

Industrial Refrigeration Market Research Report Guidance:

The report includes qualitative and quantitative data in the industrial refrigeration market across component, refrigerant type, application, and geography.

The report starts with the key takeaways (Chapter 2), highlighting the key trends and outlook of the Industrial Refrigeration Market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the industrial refrigeration market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Industrial Refrigeration Market scenario in terms of historical market revenues and forecast till the year 2031.

Chapters 7 to 10 cover the Industrial Refrigeration Market segments by component, refrigerant type, application, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the industrial refrigeration market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Industrial Refrigeration Market News and Key Development:

The Industrial Refrigeration Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the industrial refrigeration market are:

In July 2025, Robertshaw, a global leader in the design and manufacture of industrial control products and systems, and a recognized technology leader in thermal and flow control solutions, announced the launch of its 2025 Ranco® commercial refrigeration line. This upgraded line—featuring important new products and enhancements to existing ones—continues the legacy of innovation from the Ranco business, which was founded in 1913.

In September 2024, Carrier Transicold announced the commercial launch of a new version of its Vector® HE 19 unit at IAA Transportation 2024 in Hanover, Germany. Featuring a new refrigerant with low global warming potential (GWP) and compatible with hydrogenated vegetable oil (HVO) biofuel or B100 biofuel, this refrigeration solution for semi-trailers has been designed to significantly reduce carbon dioxide (CO2) emissions while maintaining exceptional performance. Carrier Transicold is part of Carrier Global Corporation (NYSE: CARR), a global leader in intelligent climate and energy solutions.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Industrial Refrigeration Market

Johnson Controls

Emerson Electric Co.

Danfoss

GEA Group Aktiengesellschaft

MAYEKAWA MFG Co. Ltd.

BITZER Kuhlmaschinenbau GmbH

DAIKIN Industries Ltd.

EVAPCO Inc.

Guntner GmbH & Co. KG

LU-VE S.p.A

About Author— Electronics and Semiconductor Research Team

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the Industrial Refrigeration Market?

The Industrial Refrigeration Market is valued at US$ 22.330 Billion in 2025, it is projected to reach US$ 81 Billion by 2033.

What is the CAGR for Industrial Refrigeration Market by (2026 - 2033)?

As per our report Industrial Refrigeration Market, the market size is valued at US$ 22.330 Billion in 2025, projecting it to reach US$ 81 Billion by 2033. This translates to a CAGR of approximately 17.48% during the forecast period.

What segments are covered in this report?

The Industrial Refrigeration Market report typically cover these key segments-

What is the historic period, base year, and forecast period taken for Industrial Refrigeration Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Industrial Refrigeration Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Industrial Refrigeration Market?

The Industrial Refrigeration Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Johnson Controls

Emerson Electric Co.

Danfoss

GEA Group Aktiengesellschaft

MAYEKAWA MFG Co. Ltd.

BITZER Kuhlmaschinenbau GmbH

DAIKIN Industries Ltd.

EVAPCO Inc.

Guntner GmbH & Co. KG

LU-VE S.p.A

Who should buy this report?

The Industrial Refrigeration Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Industrial Refrigeration Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Industrial Refrigeration Market

Get Free Sample For Industrial Refrigeration Market