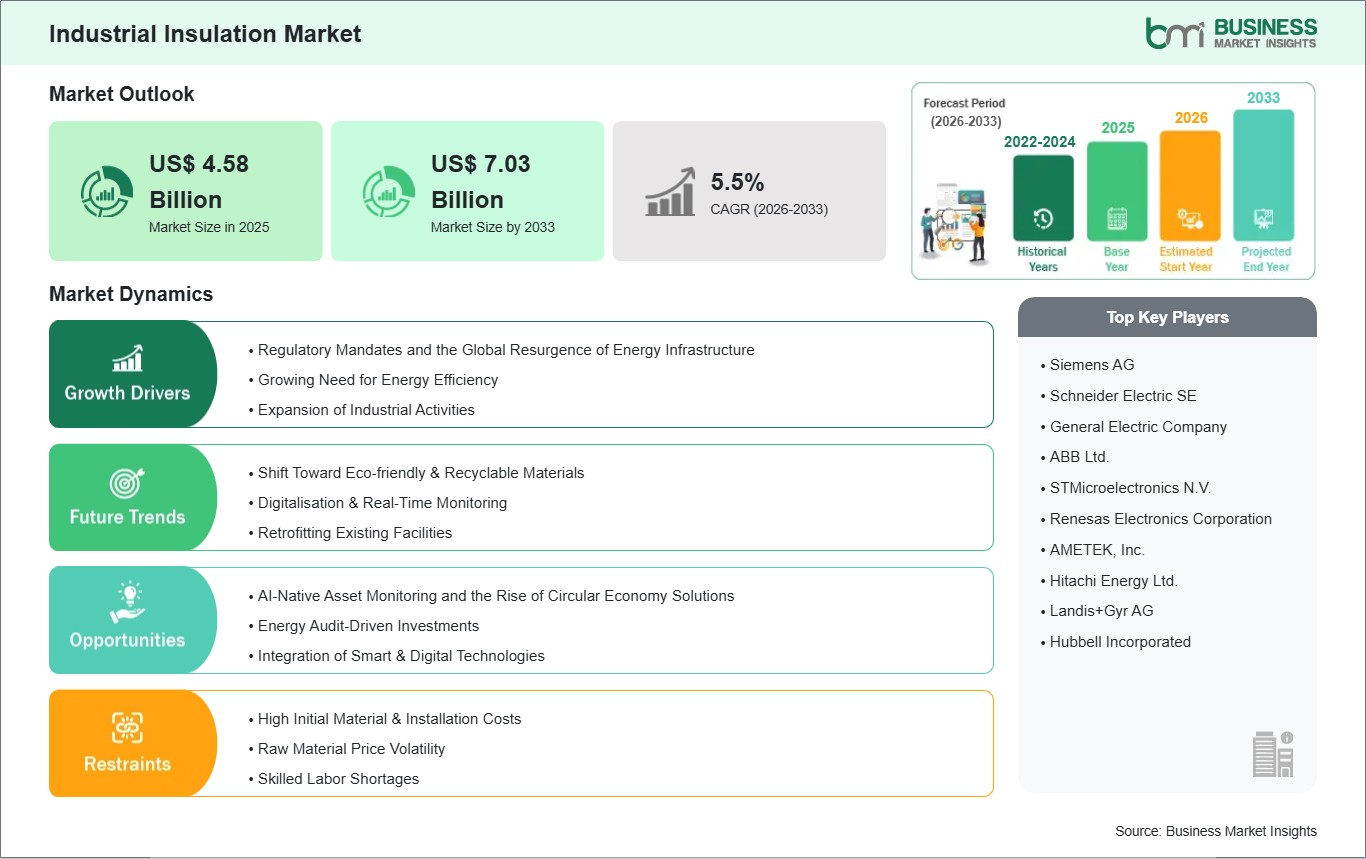

The Industrial Insulation market size is expected to reach US$ 7.03 billion by 2033 from US$ 4.58 billion in 2025. The market is estimated to record a CAGR of 5.5% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Industrial insulation refers to the specialized application of materials, such as mineral wool, fiberglass, calcium silicate, and foamed plastics, to industrial equipment, piping, and structures to regulate thermal energy. These systems serve as a critical barrier against heat transfer, condensation, and noise, ensuring the safe and efficient operation of high-heat and cryogenic processes. Market progression is fundamentally propelled by stringent global energy efficiency regulations, which mandate the insulation of industrial infrastructure to reduce carbon emissions. Furthermore, significant capital investments in oil and gas infrastructure, particularly LNG terminal development, and the expansion of industrial capacity in emerging economies serve as primary catalysts for sustained demand.

However, several factors may restrain market development. The substantial initial capital expenditure required for large-scale insulation projects, including procurement and skilled labor, can be prohibitive for manufacturers operating on narrow margins. Technical challenges related to Corrosion Under Insulation (CUI), a hidden threat where moisture trapped beneath the material leads to rapid equipment degradation, require costly monitoring and maintenance. Additionally, the industry faces challenges related to supply chain volatility for specialized raw materials and a persistent skills gap, as the installation of complex insulation systems requires specialized expertise that is currently in high demand.

Despite these hurdles, the market holds significant opportunities in the expansion of sustainable and bio-based insulation materials, which align with corporate net-zero targets. The rise of aerogel blankets and vacuum insulation panels, offering superior thermal resistance with minimal thickness, and the integration of digital twins and drone-based thermal imaging for predictive maintenance are expected to support long-term development. Manufacturers are also finding growth potential in the retrofitting of existing facilities, as older plants seek to comply with modern environmental standards through improved thermal management.

Key segments that contributed to the derivation of the Industrial Insulation market analysis are form, material, and end-use industry.

By Form, the market is segmented into Pipe, Blanket, and Board.

By Material, the market is divided into Mineral wool, Calcium silicate, and Plastic foams.

By End-use Industry, the market is categorized into Power, Oil & petrochemical, Gas, Chemical, Cement, and Food & beverage.

Industrial Insulation Market Drivers and Opportunities:

Regulatory Mandates and the Global Resurgence of Energy Infrastructure

The primary driver for the Industrial Insulation Market is the systemic global implementation of stringent energy efficiency standards and the extensive expansion of critical energy corridors. The Escalating Stringency of Energy Performance Mandates acts as a foundational catalyst, as regulatory frameworks, such as the European Union`s Energy Performance of Buildings Directive and national energy conservation codes, require industrial operators to minimize heat loss to meet binding carbon-reduction targets. This momentum is further propelled by Significant Capital Investments in LNG and Petrochemical Infrastructure; the global surge in LNG terminal construction and subsea oil and gas exploration necessitates specialized cryogenic and corrosive-resistant insulation solutions to ensure safe transportation and storage. In the technological sphere, the Rapid Adoption of High-Performance Aerogels and Vacuum Insulation Panels serves as a vital driver, as these materials offer superior thermal resistance in ultra-thin profiles, enabling efficiency gains in space-constrained industrial environments. Furthermore, the Urgent Requirement to Mitigate Corrosion Under Insulation (CUI) is driving the demand for advanced, moisture-resistant materials and coatings that can extend the lifespan of metallic assets while maintaining thermal integrity. Together, these factors, regulatory compliance, infrastructure growth, and asset protection, ensure a robust and essential growth path for the global Industrial Insulation Market.

AI-Native Asset Monitoring and the Rise of Circular Economy Solutions

A significant high-value opportunity lies in the convergence of Industrial Insulation with IoT Sensing and Sustainable Material Science. Next-generation Smart Insulation Systems with Integrated Sensor Networks are being developed to utilize real-time data to detect moisture ingress and temperature fluctuations, allowing for predictive maintenance that can prevent catastrophic asset failure. There is also a major growth frontier in the development of Closed-Loop Recycling and Low-Embodied Carbon Materials; as industries align with circular economy principles, the demand for recyclable mineral wool and bio-based foamed plastics is expanding, offering a unique opportunity for manufacturers to differentiate through sustainability credentials. Furthermore, the expansion of Modular and Prefabricated Insulation Solutions presents a lucrative opportunity, as offsite-engineered sections can be rapidly installed with minimal on-site labor, addressing the global shortage of skilled insulation contractors. Beyond traditional sectors, the rise of Thermal Management for Hydrogen Production and Storage offers a unique frontier, where specialized insulation is required to handle the extreme temperatures associated with emerging green energy technologies. Manufacturers who focus on Custom-Engineered Cryogenic Specialty Solutions and those pioneering Automated Robotic Installation Systems are positioned to lead the global Industrial Insulation Market.

Industrial Insulation Market Size and Share Analysis:

Based on material, the Mineral Wool subsegment holds the primary market presence, serving as the standard for high-temperature and fire-safe applications due to its excellent thermal stability and acoustic damping properties. While Calcium Silicate remains a critical choice for heavy-duty industrial environments requiring high compressive strength, it holds a specialized secondary position. A notable trend is the surge in the Plastic Foams (Polyurethane and Polystyrene) subsegment, which is registering significant expansion. In these materials, insulation is becoming essential for Cold Chain and Cryogenic Logistics, as the strategic expansion of LNG transportation and temperature-sensitive chemical processing necessitates materials with exceptionally low thermal conductivity and moisture resistance.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Siemens AG

Schneider Electric SE

General Electric Company

ABB Ltd.

STMicroelectronics N.V.

Renesas Electronics Corporation

AMETEK, Inc.

Hitachi Energy Ltd.

Landis+Gyr AG

Hubbell Incorporated

Get more information on this report

Industrial Insulation Market Report Coverage and Deliverables:

The "Industrial Insulation Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, global and regional framework, major players, and recent developments

Market concentration, heat map analysis, prominent players, and recent developments

Detailed company profiles, including SWOT analysis

Industrial Insulation Market Geographic Insights:

The geographical scope of the Industrial Insulation market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

The Asia-Pacific Industrial Insulation Market serves as the primary engine for global volume, driven by the expansion of petrochemical refineries and power plants. China and India are leading contributors to regional growth, characterized by significant governmental initiatives to modernize industrial facilities and reduce operational energy consumption. Japan and South Korea continue to lead in the development of high-performance materials such as aerogels and vacuum insulation panels, prioritizing thermal efficiency for advanced electronics and precision manufacturing. The region benefits from a maturing supply chain and an increasing transition toward localized production of mineral wool and fiberglass.

Market progression is further supported by a transition toward Smart Insulation Monitoring Systems and fire-resistant high-performance materials, which provide real-time data on thermal integrity and ensure the safety of industrial personnel. The increasing adoption of removable and reusable insulation blankets for maintenance efficiency and low-emission foamed plastics, alongside strategic growth in LNG terminal development and renewable energy infrastructure, solidifies the global landscape as a vital arena for the evolution and future scaling of the Industrial Insulation Market.

Get more information on this report

Industrial Insulation Market Research Report Guidance:

The report includes qualitative and quantitative data in the Industrial Insulation market across form, material, end-use industry, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Industrial Insulation market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by form, material, end-use industry, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Industrial Insulation Market News and Key Development:

The Industrial Insulation market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Industrial Insulation market are:

In October 2025, TopBuild acquired Specialty Products and Insulation (SPI), expanding its mechanical insulation distribution and fabrication capabilities across North America. The acquisition strengthens TopBuild`s commercial and industrial insulation offerings and extends its geographic footprint. This development is positive for the industrial insulation market, supporting innovation, operational efficiency, and market growth.

In December 2025, Etex acquired Dutch fire protection panel specialist Drumarkon, expanding its Promat platform with integrated fire, thermal, and acoustic insulation solutions for the marine and industrial sectors. The acquisition strengthens Etex`s technology expertise and global presence, enabling fully integrated insulation offerings. This development is positive for the industrial insulation market, supporting innovation and market growth.

Key Sources Referred:

World Bank & Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Industrial Insulation Market

Siemens AG

Schneider Electric SE

General Electric Company

ABB Ltd.

STMicroelectronics N.V.

Renesas Electronics Corporation

AMETEK, Inc.

Hitachi Energy Ltd.

Landis+Gyr AG

Hubbell Incorporated

About Author— Electronics and Semiconductor Research Team

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the Industrial Insulation Market?

The Industrial Insulation Market is valued at US$ 4.58 Billion in 2025, it is projected to reach US$ 7.03 Billion by 2033.

What is the CAGR for Industrial Insulation Market by (2026 - 2033)?

As per our report Industrial Insulation Market, the market size is valued at US$ 4.58 Billion in 2025, projecting it to reach US$ 7.03 Billion by 2033. This translates to a CAGR of approximately 5.5% during the forecast period.

What segments are covered in this report?

The Industrial Insulation Market report typically cover these key segments-

Form (Pipe, Blanket, and Board)

Material (Mineral wool, Calcium silicate, and Plastic foams)

End-use Industry (Power, Oil & petrochemical, Gas, Chemical, Cement, and Food & beverage)

What is the historic period, base year, and forecast period taken for Industrial Insulation Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Industrial Insulation Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Industrial Insulation Market?

The Industrial Insulation Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Siemens AG

Schneider Electric SE

General Electric Company

ABB Ltd.

STMicroelectronics N.V.

Renesas Electronics Corporation

AMETEK, Inc.

Hitachi Energy Ltd.

Landis+Gyr AG

Hubbell Incorporated

Who should buy this report?

The Industrial Insulation Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Industrial Insulation Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Industrial Insulation Market

Get Free Sample For Industrial Insulation Market