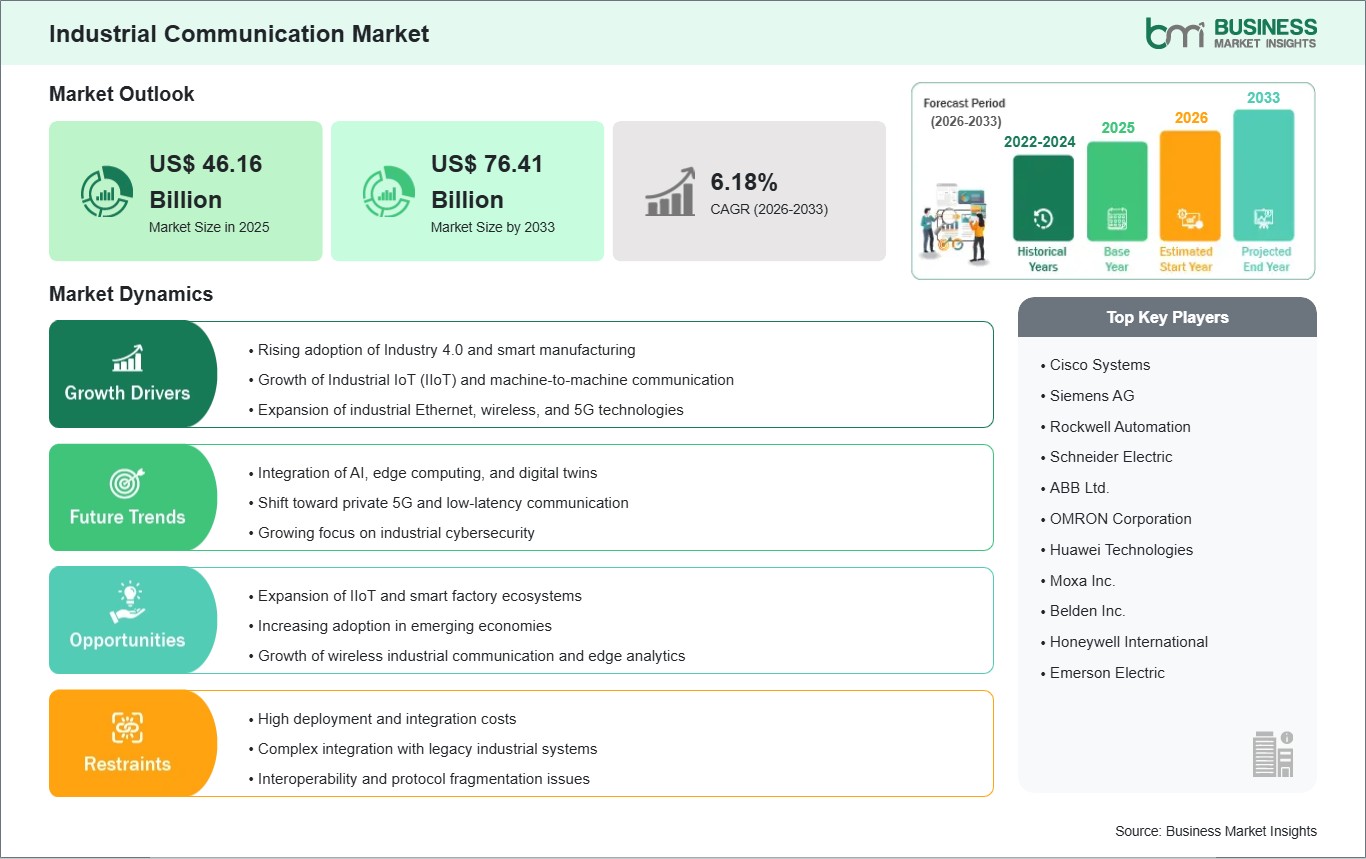

Rising Demand for Automation, Connectivity, and Efficiency

The industrial communication market is being driven by the growing need for automation, seamless connectivity, and operational efficiency across manufacturing, energy, automotive, and process industries. Industrial communication systems, including fieldbus, industrial Ethernet, and wireless protocols, enable real‑time data exchange between machines, sensors, and control systems, forming the backbone of Industry 4.0. The rapid expansion of smart factories and digital transformation initiatives is amplifying adoption, as companies seek to optimize production, reduce downtime, and enhance resource utilization. Automotive and electronics industries are reinforcing demand, with industrial communication supporting robotics, assembly lines, and quality inspection. Energy and utilities are also fueling growth, as communication networks enable predictive maintenance, smart grid management, and remote monitoring. Additionally, stricter regulatory standards for safety, cybersecurity, and interoperability are propelling investment in advanced communication solutions. Collectively, automation priorities, connectivity requirements, and efficiency goals are sustaining momentum in the global industrial communication market.

Rising Integration of IoT, 5G, and Emerging Applications

Opportunities in the industrial communication market are expanding through the integration of IoT ecosystems, 5G networks, and emerging cross‑industry applications. IoT‑enabled communication platforms are opening lucrative opportunities by offering real‑time monitoring, predictive analytics, and adaptive control across industrial environments. The rollout of 5G is gaining traction, enabling ultra‑low latency and high‑bandwidth communication for mission‑critical applications such as autonomous vehicles, robotics, and remote operations. The growing emphasis on digital transformation is fueling demand for interoperable communication systems that integrate seamlessly with cloud platforms, ERP systems, and industrial IoT frameworks. Emerging applications in healthcare and logistics are driving innovation, as industrial communication supports connected medical devices, automated warehouses, and supply chain visibility. Aerospace and defense sectors are reinforcing opportunities, where secure, high‑performance communication systems are essential for mission‑critical operations. Additionally, sustainability trends are encouraging deployment of energy‑efficient communication solutions that align with global environmental goals. The expansion of smart cities, renewable energy projects, and advanced manufacturing ecosystems is creating new pathways for adoption. Vendors who focus on IoT‑ready, 5G‑enabled, and industry‑specific communication solutions are well‑positioned to capture growth. The convergence of IoT, 5G, and smart automation underscores a transformative trajectory for the global industrial communication market.