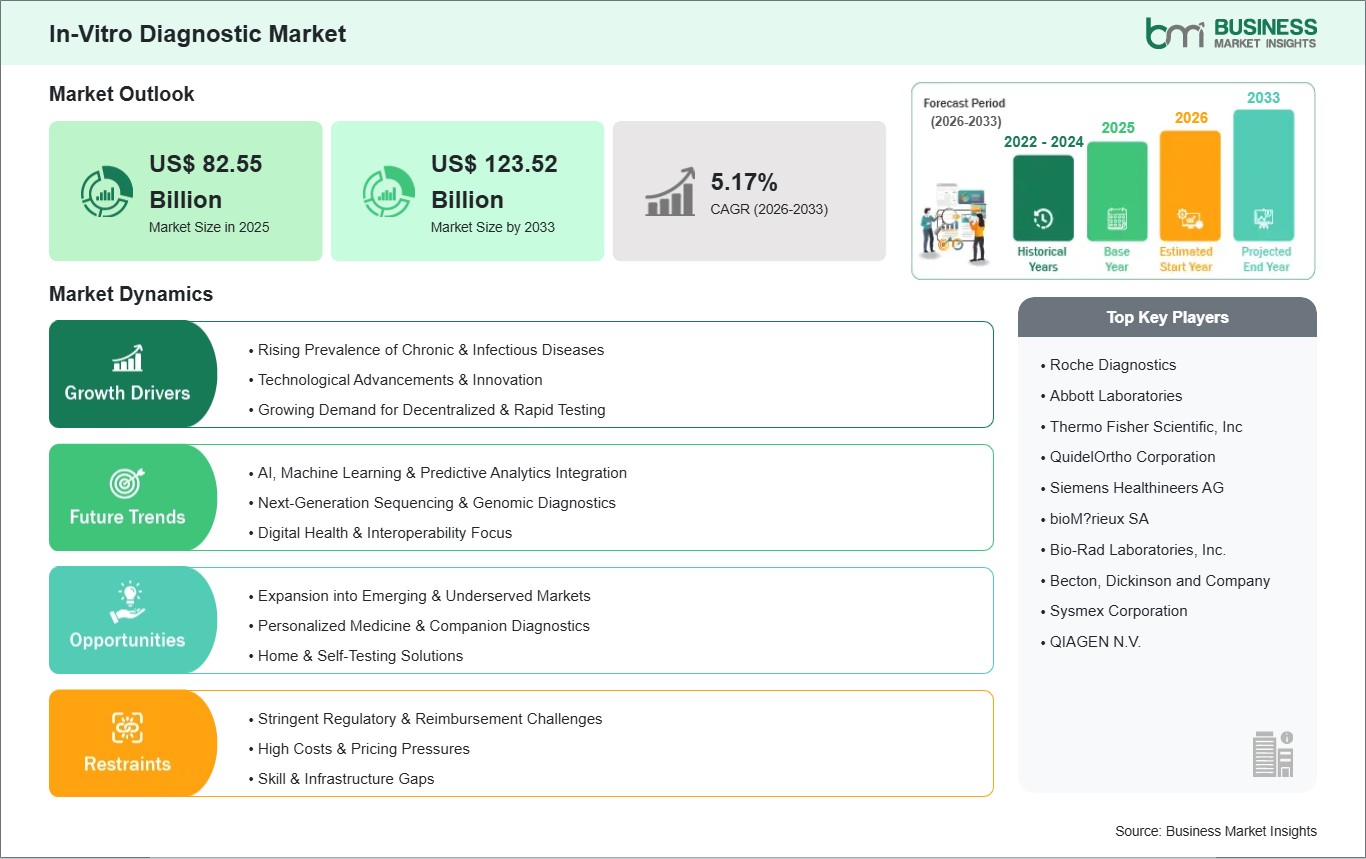

The In-Vitro Diagnostic Market size is expected to reach US$ 123.52 Billion by 2033 from US$ 82.55 Billion in 2025. The market is estimated to record a CAGR of 5.17% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The in-vitro diagnostics (IVD) market includes products, instruments, and services used for the analysis of samples such as blood, urine, and tissues to detect diseases, conditions, and infections outside the living body. The market is primarily influenced by the increasing prevalence of chronic diseases such as diabetes, cancer, and cardiovascular disorders; growing number of infectious disease outbreaks; aging population; as well as a rising global focus on the early detection, personalized medicine, and preventive healthcare.

It basically segments into reagents & kits which hold the largest share due to the recurring consumption; infectious diseases and oncology as the major applications; immunoassays and molecular diagnostics as the main sources of technologies; clinical laboratories/hospitals as the major end, users with the point, of, care (POC) testing rapidly expanding for decentralized access. The technological improvements in next, generation sequencing, digital pathology, AI, driven analytics, multiplex assays, and rapid POC devices are some of the factors that are helping to improve the accuracy, speed, and usability. At the same time, companion diagnostics are helping to guide targeted therapies.

Geographically, the North America is leading the market due to the existence of the advanced healthcare infrastructure, the favorable regulatory environment, and the high rate of adoption of innovative technologies, hence Europe is in the second position. Asia, Pacific is showing the highest speed of movement and this is a result of factors such as more people having access to healthcare, the growing middle class which is increasing the household disposable income, and the governments preventive healthcare programs in countries such as China and India. On the other hand, the markets in Latin America and Africa are struggling to keep up; however, they have enormous opportunities as a result of their gradually improving diagnostics infrastructure.

Major companies such as Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, Danaher Corporation, Thermo Fisher Scientific, and bioMrieux are striving for the major market share by investing heavily into R&D, making insightful acquisitions, and integrating digital technologies. The market for IVD is, in essence, moving in the direction of precision, portability, and connectivity while still maintaining a balance between the solid core of lab testing and the breakthrough possibilities of molecular and home, based diagnostics.

In-Vitro Diagnostic Market - Strategic Insights:

Get more information on this report

In-Vitro Diagnostic Market Segmentation Analysis:

Key segments that contributed to the derivation of the In-Vitro Diagnostic market analysis are product, test type, application, and end user.

By product, the in-vitro diagnostic market is segmented into reagents & consumables, instruments & systems, services. The reagents & consumables segment dominated the market in 2025.

By test type, the market is segmented into immunodiagnostics, molecular diagnostics, hematology, microbiology & cytology, and others. The immunodiagnostics segment held the largest share of the market in 2025.

By application, the market is segmented into infectious diseases, oncology, diabetes testing, cardiology, autoimmune diseases, and others. The infectious diseases segment held the largest share of the market in 2025.

By end user, the market is segmented into hospital laboratories, diagnostic laboratories, point-of-care settings, others. The hospital laboratories segment held the largest share of the market in 2025.

In-Vitro Diagnostic Market Drivers and Opportunities:

Rising Prevalence of Chronic and Infectious Diseases

The substantial increase in lifestyle diseases such as diabetes, cancer, cardiovascular disorders, and infectious diseases is the leading factor driving the global in, vitro diagnostics market growth. These diseases have a massive impact on the health of people worldwide, and diabetes affects more than 500 million adults. The number of patients is expected to increase with aging populations, obesity, urbanization, and lifestyle changes. Therefore, the demand for the monitoring and early detection of such diseases has also grown significantly. These diseases require frequent and regular testing of glycemic control, tumor markers, cardiac biomarkers, and pathogen identification, which are the techniques used in IVD that are now the most preferred in the prevention of complications, treatment guidance, and outcome improvement.

Moreover, the problem of infectious diseases, which includes the return of pandemics and antimicrobial resistance, is a cause of the increased demand for rapid immunoassays, molecular diagnostics, and POC tests. The aging population in the developed regions is causing an increase in the number of patients with chronic diseases, whereas the emerging economies are suffering from the double burden of infectious and non, communicable diseases. Healthcare guidelines issued by organizations such as WHO and IDF, among others, strongly recommend early screening and personalized monitoring, which in turn leads to increased usage of reagents and kits.

Technological integrations, such as multiplex panels detecting several pathogens at the same time, are improving the efficiency of these processes in high, burden settings. Testing which is supported by reimbursement in many countries, is kept at a good level due to the awareness campaigns that attract people to preventive diagnostics. Major market players such as Roche, Abbott, and Siemens Healthineers are coming up with new ideas to satisfy this request of the market with their high, sensitivity assays.

Advancements in Point-of-Care and Molecular Diagnostics

The IVD market is a transformational opportunity for the IVD market due to advancements in point, of, care (POC) testing and molecular diagnostics. decentralized, rapid, and precise testing beyond conventional labs is possible with the help of these technologies. POC instruments provide results within a few minutes in a home, clinic, or remote location. They are capable of meeting the demands of timely interventions in chronic management, infectious outbreaks, and emergency care, thus lessening the healthcare load and making access better in the areas that are not well served.

The molecular technologies such as next, generation sequencing (NGS), PCR, and CRISPR, based assays that are used in oncology, genetic disorders, and pathogen detection, respectively, have the highest sensitivity possible. They also enable precision medicine and companion diagnostics for targeted therapies. Besides this, AI integration is helping in enhancing data analysis, error reduction, and predictive insights. At the same time, being connected via smartphones and cloud platforms is making telemedicine and real, time monitoring possible.

This opportunity aligns with post-pandemic shifts toward home-based and near-patient testing, rising demand for personalized treatments, and government investments in healthcare infrastructure, particularly in emerging markets such as Asia-Pacific and Africa. Portable, user-friendly multiplex tests expand applications in infectious diseases and oncology, the fastest-growing segments. Companies such as Abbott, bioMérieux, and Thermo Fisher are capitalizing through launches of innovative platforms, partnerships, and acquisitions. Regulatory support for OTC and digital diagnostics accelerates adoption.

In-Vitro Diagnostic Market Size and Share Analysis:

By product, the in-vitro diagnostic market is segmented into reagents & consumables, instruments & systems, services. The reagents & consumables segment dominated the market in 2025. The high volume of routine testing for chronic and infectious diseases, which require frequent replenishment; affordability as compared to instrument, heavy laboratories; the technological advancements allowing multiplex and high, sensitivity assays; and the growth of point, of, care and home testing, which, for the most part, are consumables, based decentralized diagnostics.

By test type, the market is segmented into immunodiagnostics, molecular diagnostics, hematology, microbiology & cytology, and others. The immunodiagnostics segment held the largest share of the market in 2025. Its dominance is attributed to the versatility, short turnaround time, and low cost, of the immunoassays aimed at the detection of antigens, antibodies, and biomarkers. ELISA, chemiluminescence, and lateral flow assays are some of the technologies that facilitate high, throughput screening.

By application, the market is segmented into infectious diseases, oncology, diabetes testing, cardiology, autoimmune diseases, and others. The infectious diseases segment held the largest share of the market in 2025. The growth is strongly influenced by continuous worldwide outbreaks, antimicrobial resistance, and the demand for quick identification of pathogens. The scope of this is the testing of viral, bacterial, fungal, and parasitic infections by means of immunoassays, molecular methods, and microbiology.

By end user, the market is segmented into hospital laboratories, diagnostic laboratories, point-of-care settings, others. The hospital laboratories segment held the largest share of the market in 2025. They are responsible for diverse IVD needs from the emergency department to inpatient monitoring. The leading factors are the rise in hospital admissions due to chronic and critical conditions, implementation of advanced automated systems for efficiency, availability of skilled pathologists, strict regulatory compliance, and the healthcare professionals move towards consolidated testing for cost control and faster turnaround in multidisciplinary healthcare environments.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Roche Diagnostics

Abbott Laboratories

Thermo Fisher Scientific, Inc

QuidelOrtho Corporation

Siemens Healthineers AG

bioMérieux SA

Bio-Rad Laboratories, Inc.

Becton, Dickinson and Company

Sysmex Corporation

QIAGEN N.V.

Get more information on this report

In-Vitro Diagnostic Market Report Coverage and Deliverables:

The In-Vitro Diagnostic Market Size and Forecast (2025-2033) report provides a detailed analysis of the market covering below areas:

In-Vitro Diagnostic market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

In-Vitro Diagnostic market trends, as well as market dynamics such as drivers, restraints, and key opportunities

In-Vitro Diagnostic market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the In-Vitro Diagnostic market

Detailed company profiles, including SWOT analysis

In-Vitro Diagnostic Market Geographic Insights:

The geographical scope of the In-Vitro Diagnostic market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The In-Vitro Diagnostic market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific In-Vitro Diagnostic market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The Asia, Pacific is the major contributor to the rapid growth of in-vitro diagnostics (IVD) market. The growth is primarily due to the increasing incidence of chronic diseases such as diabetes, cancer, and cardiovascular diseases and the infectious disease burdens being kept up with, e.g., tuberculosis, hepatitis, and respiratory infections. Countries such as China, India, and Japan are the main drivers of this growth. China and India are witnessing large numbers of diabetes and cancer cases due to rapid urbanization and lifestyle changes, while Japan's state, of, the art healthcare system and aging population are contributing to the increase in demand for precision and molecular testing.

The increasing elderly population in the region, therefore, contributes to the need for continuous monitoring, early diagnosis, and personalized medicine, which are further advertised by increasing health awareness, preventive screening programs, and post, pandemic rapid diagnostics promotion. The transition to point, of, care (POC) and decentralized testing is very popular and will probably continue to grow due to innovations in immunoassays, molecular diagnostics (including NGS and PCR), AI, integrated platforms, and smartphone, compatible devices that facilitate access to the remote and less privileged areas. As a result of government funding for healthcare infrastructure, expanding health insurance coverage, and public health programs in emerging economies, the use of reagents, kits, and automated systems is becoming more widespread. Large companies such as Roche Diagnostics, Abbott, Siemens Healthineers, Sysmex, as well as local innovators, are committing resources towards cooperations, localized production, and digital solutions in order to tackle issues such as price sensitivity and regulatory diversity. There are also many possibilities in the field of companion diagnostics, testing at home, as well as the application of oncology/infectious diseases, thus making Asia, Pacific a vibrant center for innovative, fair IVD progress.

Get more information on this report

In-Vitro Diagnostic Market Research Report Guidance:

The report includes qualitative and quantitative data in the In-Vitro Diagnostic market across product, test type, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the In-Vitro Diagnostic market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the In-Vitro Diagnostic market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the In-Vitro Diagnostic market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover In-Vitro Diagnostic market segments by product, test type, application and end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the In-Vitro Diagnostic market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

In-Vitro Diagnostic Market News and Key Development:

The In-Vitro Diagnostic market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the in-vitro diagnostic market are:

In February 2025, Aiforia Technologies Plc successfully obtained the In Vitro Diagnostic Regulation (IVDR) certification. At the same time, the company launches three new CE-IVD marked AI models for breast and prostate cancer diagnostics.

In January 2025, ELITechGroup launched the GI Bacterial PLUS ELITe MGB Kit, a robust addition to its diagnostic portfolio. Tailored specifically for diagnosing gastrointestinal bacterial infections, the in vitro assay exclusively targets major bacterial pathogens including Campylobacter spp., Clostridium difficile, Salmonella spp., Shigella spp., and Yersinia enterocolitica. These pathogens are widely acknowledged as significant contributors to global food and waterborne, as well as hospital-acquired, gastrointestinal infections.

In October 2021, Bio-Rad Laboratories Inc., which specializes in life science research and clinical diagnostic products, has introduced two PCR detection systems, the CFX Opus 96 Dx System and the CFX Opus 384 Dx System.

Key Sources Referred:

World Bank – Global Trade IndicatorsEuropean Chemicals AgencyInternational Council of Chemical Associations(International Monetary Fund )IMFWorld Trade Organization (WTO)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - In-Vitro Diagnostic Market

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the In-Vitro Diagnostic Market?

The In-Vitro Diagnostic Market is valued at US$ 82.55 Billion in 2025, it is projected to reach US$ 123.52 Billion by 2033.

What is the CAGR for In-Vitro Diagnostic Market by (2026 - 2033)?

As per our report In-Vitro Diagnostic Market, the market size is valued at US$ 82.55 Billion in 2025, projecting it to reach US$ 123.52 Billion by 2033. This translates to a CAGR of approximately 5.17% during the forecast period.

What segments are covered in this report?

The In-Vitro Diagnostic Market report typically cover these key segments-

End User (Hospital Laboratories, Diagnostic Laboratories, Point-of-Care Settings, Others)

What is the historic period, base year, and forecast period taken for In-Vitro Diagnostic Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the In-Vitro Diagnostic Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in In-Vitro Diagnostic Market?

The In-Vitro Diagnostic Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The In-Vitro Diagnostic Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the In-Vitro Diagnostic Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For In-Vitro Diagnostic Market

Get Free Sample For In-Vitro Diagnostic Market