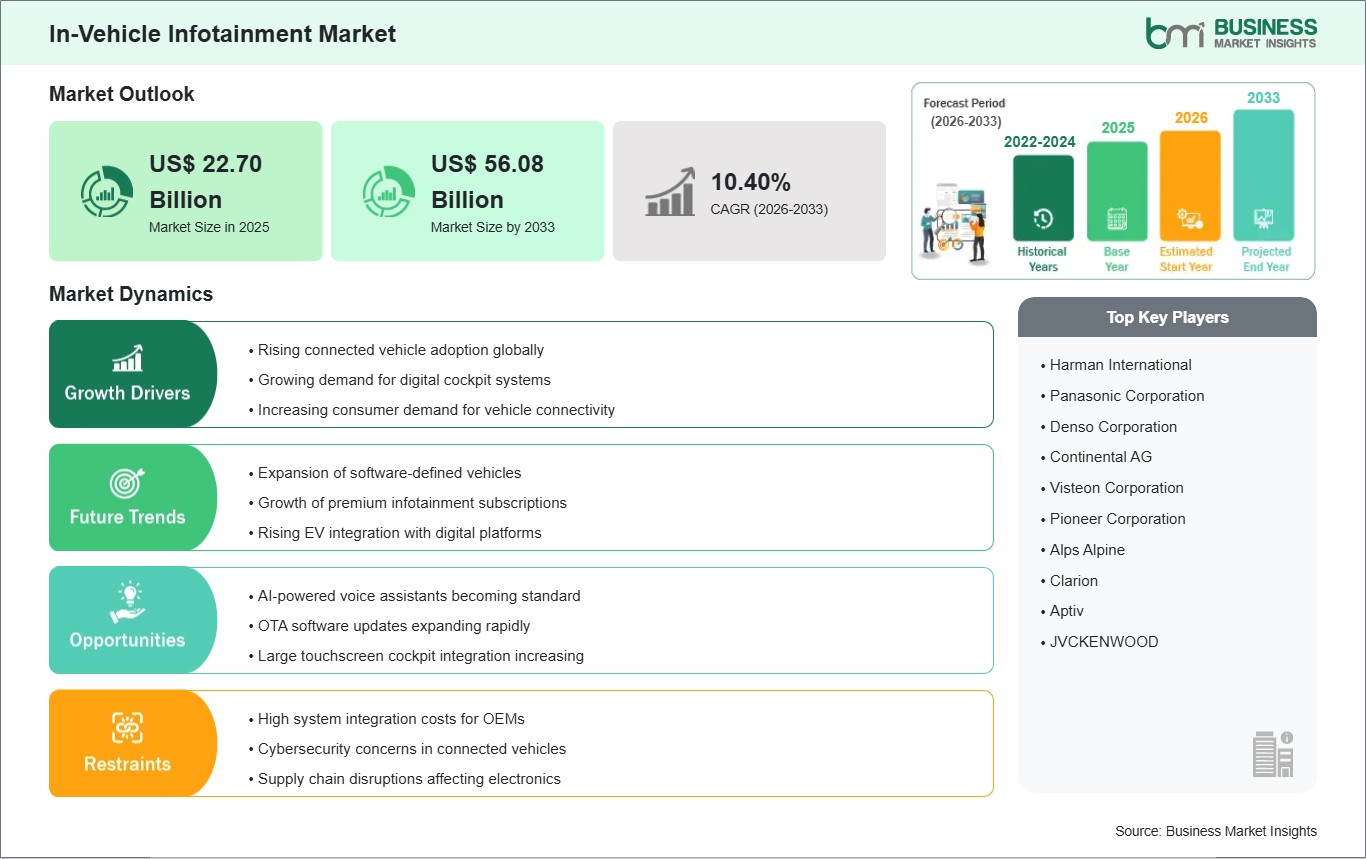

The In-Vehicle Infotainment market size is expected to reach US$ 56.08 billion by 2033 from US$ 22.70 billion in 2025. The market is estimated to record a CAGR of 10.40% from 2026 to 2033.

Executive Summary and Global Market Analysis:

In-vehicle infotainment systems integrate audio, visual, communication, and navigation functions within the cabin environment to support information access, media control, and connected user experiences during travel. These platforms have shifted from standalone entertainment modules to software-led interfaces that coordinate displays, voice interaction, smartphone connectivity, and route guidance across vehicle architectures.

Automakers are expanding deployment of infotainment platforms as buyers place greater value on connected driving, intuitive interfaces, and seamless access to digital services. Cabin design priorities now extend beyond mechanical performance, with user experience, device integration, and software responsiveness influencing purchasing decisions across both personal and fleet mobility categories.

Segmentation patterns indicate broad relevance across component, vehicle type, and installation categories. Display units remain central to interface design, while communication and navigation units support connected functions and trip management. Passenger cars represent the widest deployment base, whereas SUVs and MPVs increasingly incorporate larger screens and multi-zone content access. In-dash systems continue as the standard format, while rear-seat infotainment retains importance in comfort-oriented vehicle configurations.

Technology evolution within this sector reflects a move toward integrated cockpit computing, sharper display formats, voice-enabled control layers, and software platforms that support over-the-air upgrades. Interface design increasingly emphasizes reduced driver distraction, faster menu logic, and compatibility with advanced vehicle electronics, allowing infotainment functions to align more closely with safety systems and digital services.

Competitive conditions are shaped by platform integration capabilities, software expertise, display engineering, and alignment with evolving automotive design cycles. Market participants compete through modular architectures, interface refinement, and collaboration across hardware and software layers. As infotainment becomes more embedded in overall cockpit strategy, product differentiation increasingly depends on system reliability, update flexibility, and quality of user interaction.

The market is segmented by component, vehicle type, and installation. Each category reflects distinct interface priorities, content access models, and cabin integration needs.

By Component

Display Units : Anchor interface visibility and centralize driver-passenger interaction.

Communication Units : Enable connectivity, telematics exchange, and external service access.

Navigation Units : Support route intelligence and trip-focused decision assistance.

Audio Units : Deliver media output and enhance in-cabin acoustic experience.

By Vehicle Type

Passenger Cars : Lead interface standardization and mass-market feature integration.

Commercial Vehicles : Prioritize communication, routing, and operational continuity.

SUVs and MPVs : Favor larger displays and richer multi-occupant content delivery.

By Installation

In-Dash Systems : Remain the default architecture for integrated cockpit control.

Rear-Seat Infotainment Systems : Extend media access for passenger-focused travel settings.

In-Vehicle Infotainment Market Drivers and Opportunities:

Connected Cabin Expectations Across Vehicle Platforms

Consumer preference has shifted toward vehicles that deliver familiar digital experiences through embedded screens, voice control, and device synchronization. This change has created a clear need for infotainment platforms that combine communication, media access, and navigation within a unified cabin interface. Automakers are responding by integrating broader software functionality into mainstream and premium vehicles, expanding deployment across multiple body styles and installation formats.

The effect of this shift extends beyond entertainment, shaping cockpit design, interface hierarchy, and brand differentiation. Infotainment quality now influences perceived vehicle sophistication and everyday usability. In this context, manufacturers and suppliers are refining display clarity, interface speed, and content accessibility to align with evolving user expectations. The driver remains highly relevant because infotainment increasingly serves as a visible expression of digital value within the cabin.

Software-Defined Cockpit Expansion

A broader shift toward software-defined vehicles is opening new opportunities for infotainment platforms that support updates, personalization, and function layering over time. This trend encourages innovation in interface frameworks, cloud-connected services, and centralized cockpit computing. Use cases now include profile-based media settings, contextual navigation prompts, and synchronized display environments that adapt to vehicle modes, occupant needs, and connected ecosystems.

Future scope is widening as infotainment becomes a flexible software layer rather than a fixed hardware feature. This creates room for service expansion, interface upgrades, and closer integration with advanced cockpit electronics. As automakers pursue scalable digital architectures, infotainment systems can influence long-term revenue models and user retention. The opportunity matters because it links cabin experience with ongoing feature evolution and post-sale differentiation.

In-Vehicle Infotainment Market Size and Share Analysis:

The In-Vehicle Infotainment market size is expected to reach US$ 56.08 billion by 2033 from US$ 22.70 billion in 2025. The market is estimated to record a CAGR of 10.40% from 2026 to 2033.

This trajectory reflects the rising strategic importance of digital cabin systems within vehicle design, where software functionality, interface quality, and connected services increasingly shape product positioning and user value perception.

Among segments, display units hold a leading position because they define the primary interaction layer for media, navigation, and vehicle information access. Passenger cars represent the broadest deployment base due to higher production volumes and wide feature standardization. In-dash systems maintain segment prominence as they remain the most established format for integrating core infotainment functions within the dashboard architecture.

Application leadership remains centered on everyday cabin functions that combine route guidance, communication access, media control, and user interface management within a single operating environment. These use patterns favor systems that can support frequent interaction without disrupting vehicle use. Rear-seat infotainment retains relevance in passenger-oriented vehicle formats, yet integrated front-cabin applications continue to account for the most consistent share of demand.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Harman International

Panasonic Corporation

Denso Corporation

Continental AG

Visteon Corporation

Pioneer Corporation

Alps Alpine

Clarion

Aptiv

JVCKENWOOD

Get more information on this report

In-Vehicle Infotainment Market Report Coverage and Deliverables:

The report provides a detailed analysis of the market covering the below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

The In-Vehicle Infotainment market shows diverse regional adoption patterns influenced by automotive production strategies, digital feature preferences, connectivity ecosystems, and regulatory attention to in-cabin interface design. At the global level, the industry is moving toward larger displays, software-centric cockpit platforms, and tighter integration between navigation, communication, and media functions. Demand also reflects the broader transition toward connected mobility, where vehicle interiors are increasingly designed as digital interaction environments rather than purely mechanical spaces.

North America demonstrates strong market maturity, supported by consumer preference for feature-rich vehicles and early acceptance of connected cabin services. Automakers in the region place considerable emphasis on interface responsiveness, smartphone compatibility, and subscription-enabled digital functions. Demand is also shaped by attention to driver distraction and usability, encouraging infotainment designs that balance broad functionality with simpler interaction pathways across passenger cars, utility vehicles, and fleet-oriented platforms.

Asia Pacific represents the most dynamic regional landscape, supported by large vehicle production volumes, expanding middle-class mobility demand, and intense competition around cabin technology differentiation. Manufacturers across the region are incorporating wider display formats, connected navigation features, and integrated communication functions to strengthen vehicle appeal. Local innovation in electronics and software ecosystems further reinforces this direction, allowing infotainment offerings to evolve quickly across both entry-level and premium vehicle segments.

Europe maintains a strong position through its focus on interface quality, design coherence, and alignment with safety-oriented cabin development. The region favors infotainment systems that integrate clean visual architecture with advanced communication and route guidance functions. Emerging markets in the Middle East and Africa and South and Central America are developing more gradually, with adoption linked to vehicle mix, affordability, and localization priorities. Even so, infotainment remains an increasingly visible differentiator as connected vehicle expectations extend across broader geographies.

Get more information on this report

In-Vehicle Infotainment Market Research Report Guidance:

The report includes qualitative and quantitative data in the market across component, vehicle type, and installation and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by component, vehicle type, installation and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

In-Vehicle Infotainment Market News and Key Development:

Recent developments reflect a clear shift toward software-led cockpit experiences and more intuitive display environments. Product announcements continue to emphasize interface refinement, personalization, and tighter integration of connected in-cabin functions.

In May 2026, LG Electronics (LG) showcased its latest suite of in-vehicle infotainment (IVI) and software-defined vehicle (SDV) solutions, which earned strong recognition from Google and global automakers. A new range of solutions is built on Android Automotive OS (AAOS) and AAOS SDV technologies. While AAOS SDV enables software to define and control core vehicle functions from driving performance and convenience features to safety systems, AAOS serves as the foundation for delivering infotainment experiences to passengers.

In March 2026, Panasonic Automotive Systems Co., Ltd. announced that the companys in-vehicle infotainment (IVI) system has debuted in Toyota Motor Corporation's (Toyota) 2026 RAV4 vehicle. This cutting-edge platform is designed to keep drivers connected, informed and entertained with speed, personalization and future-ready technology.

Key Sources Referred:

World Bank -Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - In-Vehicle Infotainment Market

Harman International

Panasonic Corporation

Denso Corporation

Continental AG

Visteon Corporation

Pioneer Corporation

Alps Alpine

Clarion

Aptiv

JVCKENWOOD

Frequently Asked Questions

How big is the In-Vehicle Infotainment Market?

The In-Vehicle Infotainment Market is valued at US$ 22.70 Billion in 2025, it is projected to reach US$ 56.08 Billion by 2033.

What is the CAGR for In-Vehicle Infotainment Market by (2026 - 2033)?

As per our report In-Vehicle Infotainment Market, the market size is valued at US$ 22.70 Billion in 2025, projecting it to reach US$ 56.08 Billion by 2033. This translates to a CAGR of approximately 10.40% during the forecast period.

What segments are covered in this report?

The In-Vehicle Infotainment Market report typically cover these key segments-

Component (Display Units, Communication Units, Navigation Units, Audio Units)

Vehicle Type (Passenger Cars, Commercial Vehicles, SUVs and MPVs)

What is the historic period, base year, and forecast period taken for In-Vehicle Infotainment Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the In-Vehicle Infotainment Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in In-Vehicle Infotainment Market?

The In-Vehicle Infotainment Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Harman International

Panasonic Corporation

Denso Corporation

Continental AG

Visteon Corporation

Pioneer Corporation

Alps Alpine

Clarion

Aptiv

JVCKENWOOD

Who should buy this report?

The In-Vehicle Infotainment Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the In-Vehicle Infotainment Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For In-Vehicle Infotainment Market

Get Free Sample For In-Vehicle Infotainment Market