01

Market Summery

Executive Summary and Global Market Analysis

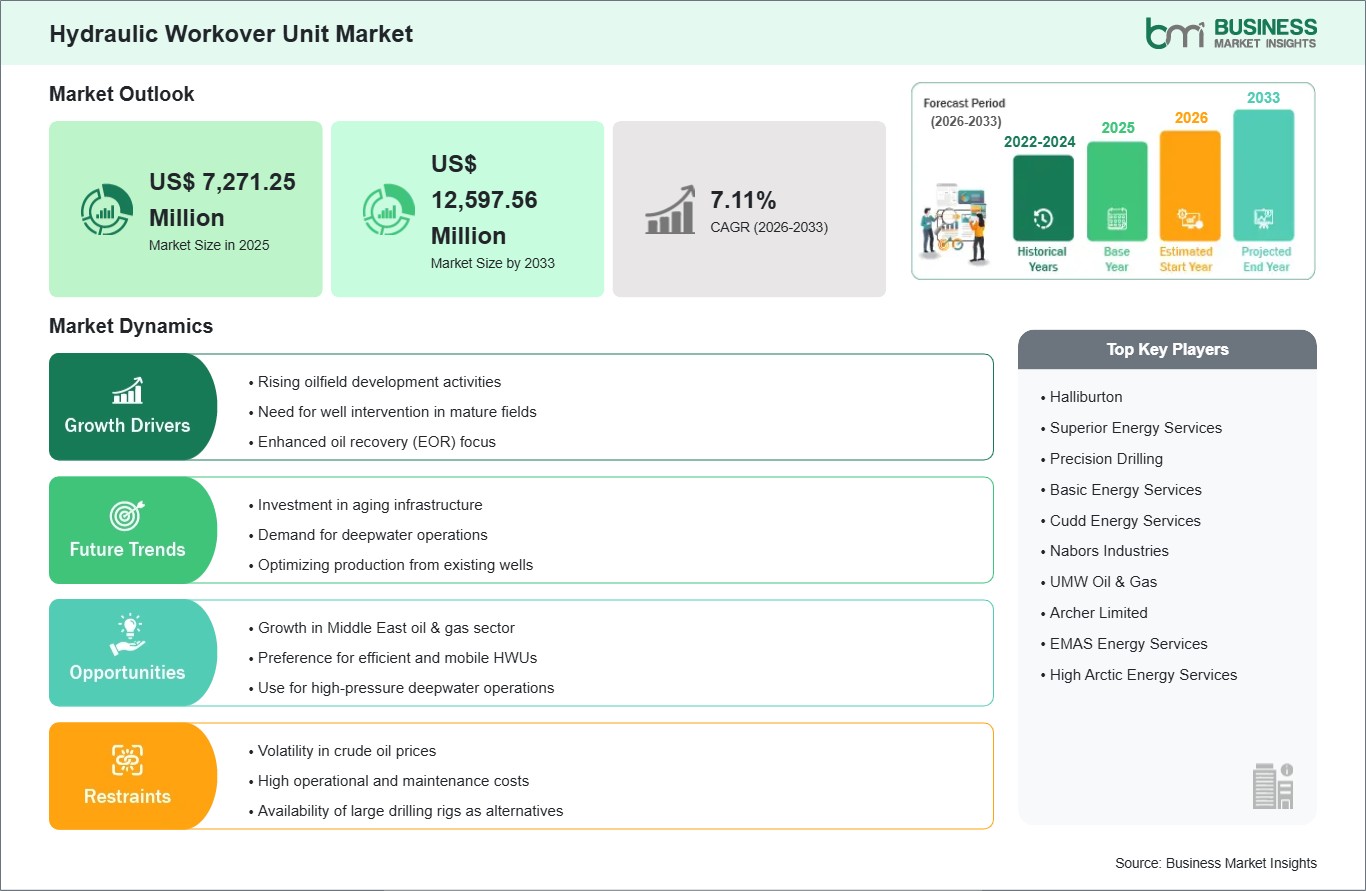

Hydraulic Workover Units refer to mobile well intervention systems engineered to perform workover and snubbing operations on oil and gas wells without killing the well. By utilizing hydraulic force to snub (push) pipe into a live well under pressure, these systems enable a wide range of interventions including well completion, stimulation, logging, and tubing replacement while maintaining production. This technology is fundamental to the operational architecture of mature field management, enabling operators to extend well life, optimize production, and perform maintenance without costly rig mobilization. Market expansion is being propelled by the increasing global inventory of mature wells requiring intervention, the rising demand for enhanced oil recovery (EOR) techniques, and the growing preference for cost-effective, mobile solutions over conventional drilling rigs for well-servicing operations.

However, several factors may restrain market progression. The high operational and maintenance costs associated with hydraulic workover units remain a significant consideration for operators evaluating intervention economics. The industry also faces technical challenges regarding the availability of skilled personnel trained in live-well intervention techniques, particularly in emerging markets. Additionally, volatility in crude oil prices directly impacts operator capital and operational expenditure decisions, creating cyclical demand patterns for workover services. These hurdles, compounded by competition from conventional workover rigs and coiled tubing units for certain applications, increase the complexity of service provider positioning and fleet utilization planning.

Despite these hurdles, the market outlook remains favorable particularly in mature hydrocarbon provinces. Opportunities are emerging through the integration of digital technologies for real-time data acquisition and remote operation, enhancing intervention efficiency and safety. The focus on well productivity and enhanced oil recovery in mature fields is driving demand for interventions such as stimulation, logging, and workovers, with HWUs offering precision and mobility for these tasks without mobilizing large drilling rigs. Furthermore, the growth of deepwater and high-pressure/high-temperature (HPHT) well development is creating demand for specialized HWU configurations. Collectively, these factors position the Hydraulic Workover Unit industry for sustained development as a critical enabler of production optimization in mature and complex well environments.

03

Segment Analysis

Hydraulic Workover Unit Market Segmentation

The Hydraulic Workover Unit market is segmented based on service, installation, and application, reflecting the diverse well intervention requirements across oil and gas operations.

By Service

- Workover: Comprehensive well intervention including tubing replacement, pump change-outs, and completion repairs

- Snubbing: Live-well intervention for pipe handling under pressure; essential for high-pressure and sensitive reservoirs

By Installation

- Onshore: Mobile units on trailers or skids for land-based well intervention; largest segment by volume

- Offshore: Platform-mounted or jack-up deployed units for subsea and platform well intervention

By Application

- Well Intervention: General maintenance and remedial operations to restore or enhance production

- Well Completion: Initial completion activities including perforating and setting production packers

- Well Maintenance: Routine preventive work to maintain production reliability

04

Market Forces

Hydraulic Workover Unit Market Drivers and Opportunities

Rising Oilfield Development and Mature Field Intervention Demand

The hydraulic workover unit market is being driven by increasing oilfield development activities and the growing need for well intervention in mature fields. Unlike conventional workover rigs, hydraulic workover units offer mobility, precision, and the ability to work on live wells without killing production, making them ideal for mature field applications where maintaining production during intervention is critical. Rising demand for enhanced oil recovery (EOR) techniques is amplifying demand, as operators seek to maximize recovery from existing assets. The aging global well inventory, with thousands of wells requiring periodic intervention, creates a sustained demand base for workover services. Additionally, operators are focusing on optimizing production from existing wells rather than pursuing high-cost exploration, driving preference for cost-effective intervention solutions. The expansion of deepwater and HPHT development is creating demand for specialized HWU configurations capable of operating in challenging environments. Collectively, mature field management and production optimization are fueling sustained growth in the global hydraulic workover unit market.

Investment in Aging Infrastructure and Deepwater Operations

Opportunities in the hydraulic workover unit market are expanding through investments in upgrading aging oilfield infrastructure and the increasing complexity of deepwater well interventions. Investment in mature field infrastructure is opening lucrative opportunities for service providers, as operators seek to extend field life through targeted interventions and maintenance. The demand for deepwater operations is driving innovation, as specialized offshore HWUs are required for subsea intervention from floating vessels or platforms. Optimizing production from existing wells through routine and remedial interventions represents a significant market opportunity, particularly in regions where new exploration is constrained by low oil prices or regulatory restrictions. Additionally, the development of HPHT fields requires HWUs with enhanced pressure control capabilities and specialized materials, creating a niche for high-specification equipment providers. Vendors who focus on fleet modernization, digital integration, and specialized capabilities for complex environments are well-positioned to capture growth.

05

Size and Share Analysis

Hydraulic Workover Unit Market Size and Share Analysis

The Hydraulic Workover Unit Market is projected to grow from US$ 7,271.25 Million in 2025 to US$ 12,597.56 Million by 2033 , registering a CAGR of 7.11% from 2026 to 2033.

By service, workover operations account for the majority of market share as comprehensive well interventions are required throughout the well lifecycle. Snubbing services represent a specialized segment for live-well applications where maintaining well control is critical.

By installation, onshore applications dominate due to the global distribution of land-based wells requiring periodic intervention. Offshore installations, while smaller in unit count, command premium pricing due to specialized equipment requirements and operational complexity.

By application, well intervention represents the largest segment as ongoing maintenance and remedial operations are essential for production sustainability. Well completion and maintenance applications provide steady demand throughout well lifecycle stages.

07

Report Coverage

Hydraulic Workover Unit Market Report Coverage and Deliverables

The "Hydraulic Workover Unit Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- Hydraulic Workover Unit Market size and forecast at global, regional, and country levels for all market segments covered under the scope

- Hydraulic Workover Unit Market trends, as well as drivers, restraints, and opportunities

- Hydraulic Workover Unit Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Hydraulic Workover Unit Market Geographic Insights

Middle East represents a key market for hydraulic workover units due to the presence of extensive mature oilfields, large well inventories, and continuous investments in oil and gas production optimization. Countries such as Saudi Arabia and United Arab Emirates are heavily focused on maintaining production from aging wells through efficient well intervention and maintenance activities. Hydraulic workover units are widely used for well servicing, tubing replacement, stimulation, and recompletion operations, particularly in onshore and offshore fields where minimizing downtime is critical. Strong government support for energy sector expansion, coupled with ongoing upstream investments and enhanced oil recovery initiatives, continues to drive market demand across the Gulf region.

North America maintains a significant position in the hydraulic workover units market owing to its vast inventory of conventional and unconventional oil and gas wells, especially across shale formations in the United States and Canada. The region benefits from a highly developed oilfield services industry, advanced intervention technologies, and widespread adoption of specialized well maintenance techniques. Hydraulic workover units are extensively deployed for well servicing, pressure control operations, and production enhancement activities in mature wells and unconventional reservoirs. Rising focus on maximizing well productivity, extending asset life, and reducing operational costs further supports steady market demand in the region.

Asia Pacific shows considerable growth potential in the hydraulic workover units market due to increasing intervention requirements in mature oilfields and expanding offshore exploration activities. Countries such as Indonesia, Malaysia, and China are focusing on maintaining production levels from aging fields through regular well servicing and intervention operations. Growing offshore drilling projects, particularly in Southeast Asia and the South China Sea, are increasing demand for efficient and flexible hydraulic workover solutions. Additionally, rising energy demand, investments in upstream oil and gas infrastructure, and efforts to improve production efficiency are contributing to the region’s market expansion.

09

Report Guidance

Hydraulic Workover Unit Market Report Guidance

The report includes qualitative and quantitative data across service, installation, capacity, application, and geography.

- The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Hydraulic Workover Unit Market.

- Chapter 3 focuses on the research methodology of the study.

- Chapter 4 includes ecosystem analysis.

- Chapter 5 highlights the major industry dynamics in the Hydraulic Workover Unit Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends.

- Chapter 6 discusses the Hydraulic Workover Unit Market scenario, in terms of historical market revenues, and forecast till the year 2033.

- Chapters 7 to 10 cover Hydraulic Workover Unit Market segments by service, installation, capacity, application, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America.

- Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

- Chapter 12 describes the industry landscape analysis with market initiatives, new developments, mergers, and joint ventures globally.

- Chapter 13 provides detailed profiles of major companies operating in the Hydraulic Workover Unit Market.

- Chapter 14 includes a brief overview of the company, list of abbreviations, and disclaimer.

10

Industry Activity

Recent Developments

The Hydraulic Workover Unit Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Hydraulic Workover Unit Market are:

- In October 2025, PETRONAS, through Malaysia Petroleum Management (MPM), has launched the Hydraulic Workover Unit (HWU) Academy to develop Malaysian talent and strengthen national capabilities in well abandonment and decommissioning. Officiated by Senior Vice President of MPM, Datuk Ir. Bacho Pilong on 23 October, the academy underscores PETRONAS’ commitment to ensure the continuous development of skilled talent to support safe, cost-efficient, and sustainable Plug and Abandonment (P&A) operations, a vital component of Malaysia’s upstream lifecycle.

- In November 2025, NEXRAIL has placed an order with Stadler for the supply of up to 200 EURO9000 panto-battery hybrid locomotives. This EURO9000 combines up to 9MW of pantograph power with 1,2MW of high-performance battery power. It will be the first mainline corridor locomotive that can offer zero-emission transport from terminal to terminal. The smart battery module enables battery storage benefits such as brake energy storage, peak shaving and energy trading.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

International Association of Drilling Contractors (IADC)

Society of Petroleum Engineers (SPE)

Company Annual Reports and Investor Presentations

Company Websites and Product Catalogs

Offshore Technology Reports