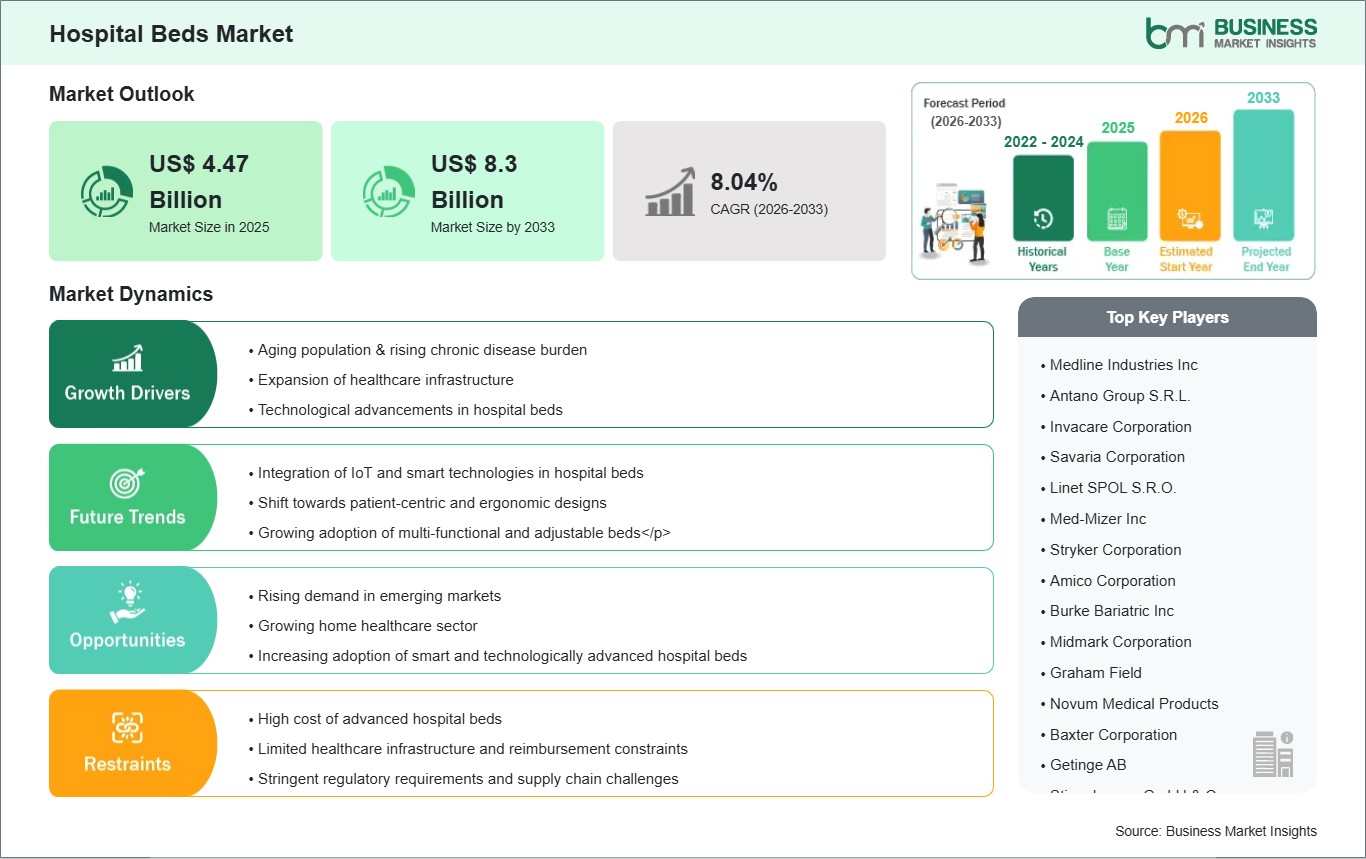

The Hospital Beds Market size is expected to reach US$ 8.3 Billion by 2033 from US$ 4.47 Billion in 2025. The market is estimated to record a CAGR of 8.04% from 2026 to 2033.

Executive Summary and Global Market Analysis:

In the healthcare service, hospital beds are the most important and basic items for use by patients and their care in hospitals, clinics, long-term care facilities, and home healthcare. All the medical treatment, recovery, monitoring, and patient comfort related to a wide variety of functions and settings such as critical care, general wards, maternity, pediatrics, and geriatrics get along with the bed. The modern hospital bed has very nice features like adjustable positioning, pressure relief, integrated monitoring support, and enhanced safety features, all of which have either improved the clinical outcomes or the caregivers' efficiency. Among the several factors fueling the hospital beds market, the most striking ones are the increasing burden of chronic diseases, rising hospitalization rates, an aging population worldwide, and the demand for advanced healthcare infrastructure. Besides, the developments in technology like electric beds, smart beds with connectivity features, and beds particularly designed for bariatric and intensive care use, are improving their adoption and functionality.

Nevertheless, the market is still challenged by high acquisition and maintenance costs, budget constraints in public healthcare systems, and unequal healthcare infrastructure across developing regions even when the demand is very strong. Supply chain problems and regulatory compliance requirements can also influence procurement and deployment. However, expanding healthcare access in emerging economies, the growth of home healthcare and long-term care facilities, and the rising investments in hospital modernization projects are some of the market's major opportunities. These along with the increasing focus on patient safety, infection control, and ergonomic design as well as the integration of digital health technologies are expected to be the main factors driving market expansion and innovation in the global hospital beds industry

Hospital Beds Market - Strategic Insights:

Get more information on this report

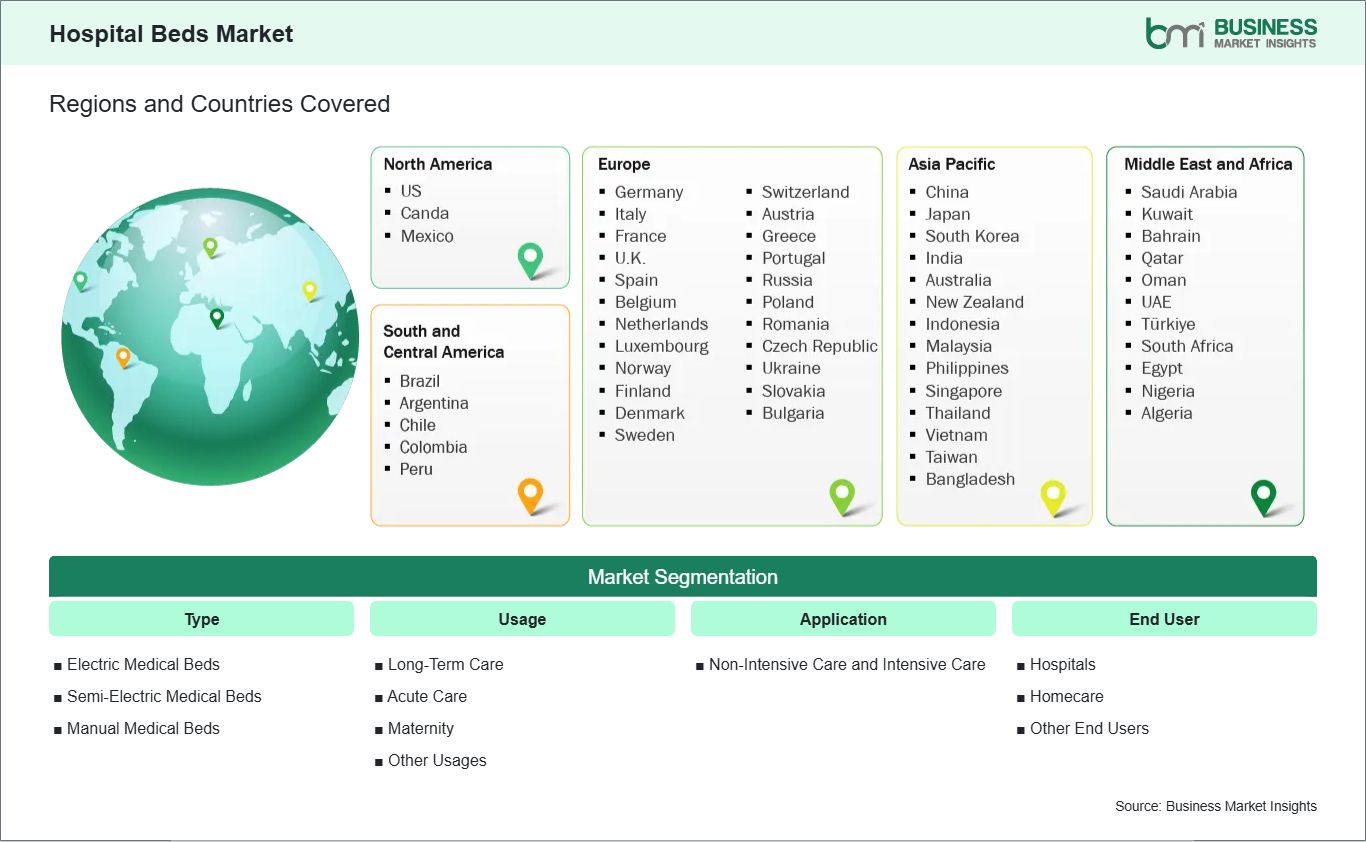

Hospital Beds Market Segmentation Analysis:

Key segments that contributed to the derivation of the Hospital Beds market analysis are type, usage, application, and end user.

By type, the Hospital Beds market is segmented into electric medical beds, semi-electric medical beds, manual medical beds. The electric medical beds segment dominated the market in 2025.

By usage, the market is divided into long-term care, acute care, maternity, and other usages. The acute care segment held the largest share of the market in 2025.

By application, the market is bifurcated into non-intensive care and intensive care. The intensive care segment held the largest share of the market in 2025.

• By end user, the market is segmented into hospitals, homecare, other end users. The hospitals segment held the largest share of the market in 2025

Hospital Beds Market Drivers and Opportunities:

Rising Demand for Acute and Long-Term Care Capacity

The hospital beds market all over the world is mainly driven by the higher demand for both acute and long-term care capacity which is confirmed by government health system data and official prevalence statistics. The World Health Organization (WHO) reports that hospital bed density was 27 beds per 10,000 people in the year 2025 on average all over the world, it is expected to rise to 28 in the year 2023 and 29 in the year 2025 besides the already existing regional variations. In the European region, Germany was reported by the OECD to have one of the highest hospital bed ratios of 7.8 beds per 1,000 people in the year 2025 which increased a bit to 7.9 in 2023 and 8.0 in 2025 while Italy and France had only 3.2 and 6.0 beds per 1,000 respectively in 2025 which shows that there is still a considerable amount of investment in inpatient infrastructure going on.

Out of all the countries in the Asia region, Japan was the one that most substantially led the global ranking with 12.7 beds per 1,000 population in the year 2025 which then increased to 12.9 in the year 2023 and 13.1 in 2025 thereby showing clearly that Japan is putting major emphasis on elderly care capacity. On the other hand, Canada had a very low report of only 2.6 beds per 1,000 in 2025 which brings into focus the concern of regional shortages and at the same time encourages procurement initiatives. Not only in terms of prevalence, but also in terms of new product developments - which in fact reinforce this driver - Stryker, LINET, and Getinge were among those major manufacturers that provided advanced electric and ICU beds with integrated patient monitoring and mobility support during the years of 2023-2025 as an answer to the government's demand for better critical care readiness. These advancements in technology along with increasing hospitalization rates and aging population show that the global hospital beds market is mainly driven by the need to have a perfect mix of capacity, technology, and patient safety across the various healthcare systems.

Rising Hospitalization and Chronic Disease Burden Driving Demand for Advanced Hospital Beds

The market for global hospital beds is an attractive one, as it is greatly affected by chronic diseases, the aging population, and hospitalization rates that require specialized and multifunctional beds for patient care. WHO (World Health Organization) estimates that chronic diseases were responsible for 74% of global deaths in 2025, with the main causes being cardiovascular diseases, cancers, and diabetes, which in turn resulted in lengthy hospitalization and intensive care requirements. In the U.S., over 1.7 million sepsis cases were reported by the Centers for Disease Control and Prevention (CDC) in 2023, and many patients ended up in the hospital requiring advanced beds equipped with pressure relief and mobility features. Data from Eurostat showed that by 2025 the percentage of the European population aged 65 and over had reached 21.6% of the total (approximately 97 million), thereby increasing the need for hospital beds in geriatric and long-term care.

In India, the Ministry of Health and Family Welfare conducted a screening of chronic conditions for over 5.82 crore beneficiaries from 2020-2023 and found that there were a large number of diabetes and hypertension cases that needed hospital-based management. The recent introduction of smart hospital beds that have been FDA-cleared and which come with built-in monitoring sensors for vital signs and pressure ulcer prevention is an example of new product development in 2025. EMA (European Medicines Agency) in 2023 was promoting the advanced bed technologies that have been developed for infection control and patient safety in critical care. All these factors together with WHO’s 2025 focus on the upgrading of health care infrastructure in the low- and middle-income countries create strong demand for the beds that offer adjustable positions, are made of infection-resistant materials, and have the technology integrated for the improvement of comfort, safety, and clinical outcomes of patients in different health care systems across the globe

Hospital Beds Market Size and Share Analysis:

By type, the Hospital Beds market is segmented into electric medical beds, semi-electric medical beds, manual medical beds. The electric medical beds segment dominated the market in 2025. The electric medical beds segment dominated due to advanced features, ease of use, and enhanced patient comfort. Automated adjustments, remote controls, and better support for medical procedures made them preferred in hospitals, boosting efficiency and improving patient care outcomes.

By usage, the market is divided into long-term care, acute care, maternity, and other usages. The acute care segment held the largest share of the market in 2025. The acute care segment held the largest share of the hospital beds market due to the high demand for beds in hospitals and critical care units, driven by increasing patient admissions, emergency cases, and the need for advanced, adjustable, and specialized beds.

By application, the market is bifurcated into non-intensive care and intensive care. The intensive care segment held the largest share of the market in 2025. The intensive care segment led the market because electric medical beds offer precise positioning, easy monitoring, and rapid adjustments, crucial for critical patients. Their advanced features enhance patient safety, comfort, and caregiver efficiency, making them essential in intensive care units.

By end user, the market is segmented into hospitals, homecare, other end users. The hospitals segment held the largest share of the market in 2025. Hospitals dominated the market due to high patient inflow and diverse medical needs. Their demand for advanced, durable, and easy-to-operate beds, especially electric models, ensured efficient patient care, enhanced safety, and streamlined hospital operations.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Medline Industries Inc

Antano Group S.R.L.

Invacare Corporation

Savaria Corporation

Linet SPOL S.R.O.

Med-Mizer Inc

Stryker Corporation

Amico Corporation

Burke Bariatric Inc

Midmark Corporation

Graham Field

Novum Medical Products

Baxter Corporation

Getinge AB

Get more information on this report

Hospital Beds Market Report Coverage and Deliverables:

The Hospital Beds Market Size and Forecast (2025-2033) report provides a detailed analysis of the market covering below areas:

Hospital Beds market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Hospital Beds market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Hospital Beds market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Hospital Beds market

Detailed company profiles, including SWOT analysis

Hospital Beds Market Geographic Insights:

The geographical scope of the Remote Patient Monitoring market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Remote Patient Monitoring market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific Remote Patient Monitoring market is anticipated to achieve remarkable growth in the years to come, thanks to the increasing occurrence of chronic diseases, the growing number of aged people, and the acceptance of digital health technologies in a swift manner. The Asia-Pacific RPM market is categorized into different countries, namely, China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. China, Japan, and India which are considered as some of the major regions are at the forefront of the adoption owing to the digitization of healthcare by the government, increased smartphone usage, and greater telemedicine infrastructure investment.

There is a huge crush for cardiology, diabetes, and respiratory care in the region through the use of connected medical devices, wearable sensors, and cloud-based monitoring platforms. The removal of barriers to healthcare access in the countryside, the existence of favorable regulations, and the establishment of partnerships between hospitals and digital health providers are the main factors that are propelling the growth of RPM. Moreover, the upsurge in healthcare costs, better internet connectivity, and the use of AI-powered analytics are making the Asia-Pacific region an important contributor to the global Remote Patient Monitoring market.

Get more information on this report

Hospital Beds Market Research Report Guidance:

The report includes qualitative and quantitative data in the Hospital Beds market across type, usage, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Hospital Beds market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Hospital Beds market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Hospital Beds market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover Hospital Beds market segments by type, usage, application, and end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Hospital Beds market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer

Hospital Beds Market News and Key Development:

The Hospital Beds market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Hospital Beds market are:

In February 2025, Agiliti Launches Essentia, an Innovative Multi-Acuity Hospital Bed that Helps Lower Patient Risk and Accelerate Mobility.

In February 2025, Stryker announced the launch of the ProCeed hospital bed, offering simplicity while enhancing care across various regions.

In March 2025, Stryker launched SmartMedic, India’s first ICU bed upgrade platform to enhance patient care and caregiver safety

Key Sources Referred:

World Bank – Global Trade IndicatorsEuropean Chemicals AgencyInternational Council of Chemical Associations(International Monetary Fund )IMFWorld Trade Organization (WTO)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Hospital Beds Market

Medline Industries Inc

Antano Group S.R.L.

Invacare Corporation

Savaria Corporation

Linet SPOL S.R.O.

Med-Mizer Inc

Stryker Corporation

Amico Corporation

Burke Bariatric Inc

Midmark Corporation

Graham Field

Novum Medical Products

Baxter Corporation

Getinge AB

Stiegelmeyer GmbH & Co

Frequently Asked Questions

How big is the Hospital Beds Market?

The Hospital Beds Market is valued at US$ 4.47 Billion in 2025, it is projected to reach US$ 8.3 Billion by 2033.

What is the CAGR for Hospital Beds Market by (2026 - 2033)?

As per our report Hospital Beds Market, the market size is valued at US$ 4.47 Billion in 2025, projecting it to reach US$ 8.3 Billion by 2033. This translates to a CAGR of approximately 8.04% during the forecast period.

What segments are covered in this report?

The Hospital Beds Market report typically cover these key segments-

Type (Electric Medical Beds, Semi-Electric Medical Beds, Manual Medical Beds)

Usage (Long-Term Care, Acute Care, Maternity, Other Usages)

Application (Non-Intensive Care and Intensive Care)

End User (Hospitals, Homecare, Other End Users)

What is the historic period, base year, and forecast period taken for Hospital Beds Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Hospital Beds Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Hospital Beds Market?

The Hospital Beds Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medline Industries Inc

Antano Group S.R.L.

Invacare Corporation

Savaria Corporation

Linet SPOL S.R.O.

Med-Mizer Inc

Stryker Corporation

Amico Corporation

Burke Bariatric Inc

Midmark Corporation

Graham Field

Novum Medical Products

Baxter Corporation

Getinge AB

Stiegelmeyer GmbH & Co

Who should buy this report?

The Hospital Beds Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Hospital Beds Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Hospital Beds Market

Get Free Sample For Hospital Beds Market