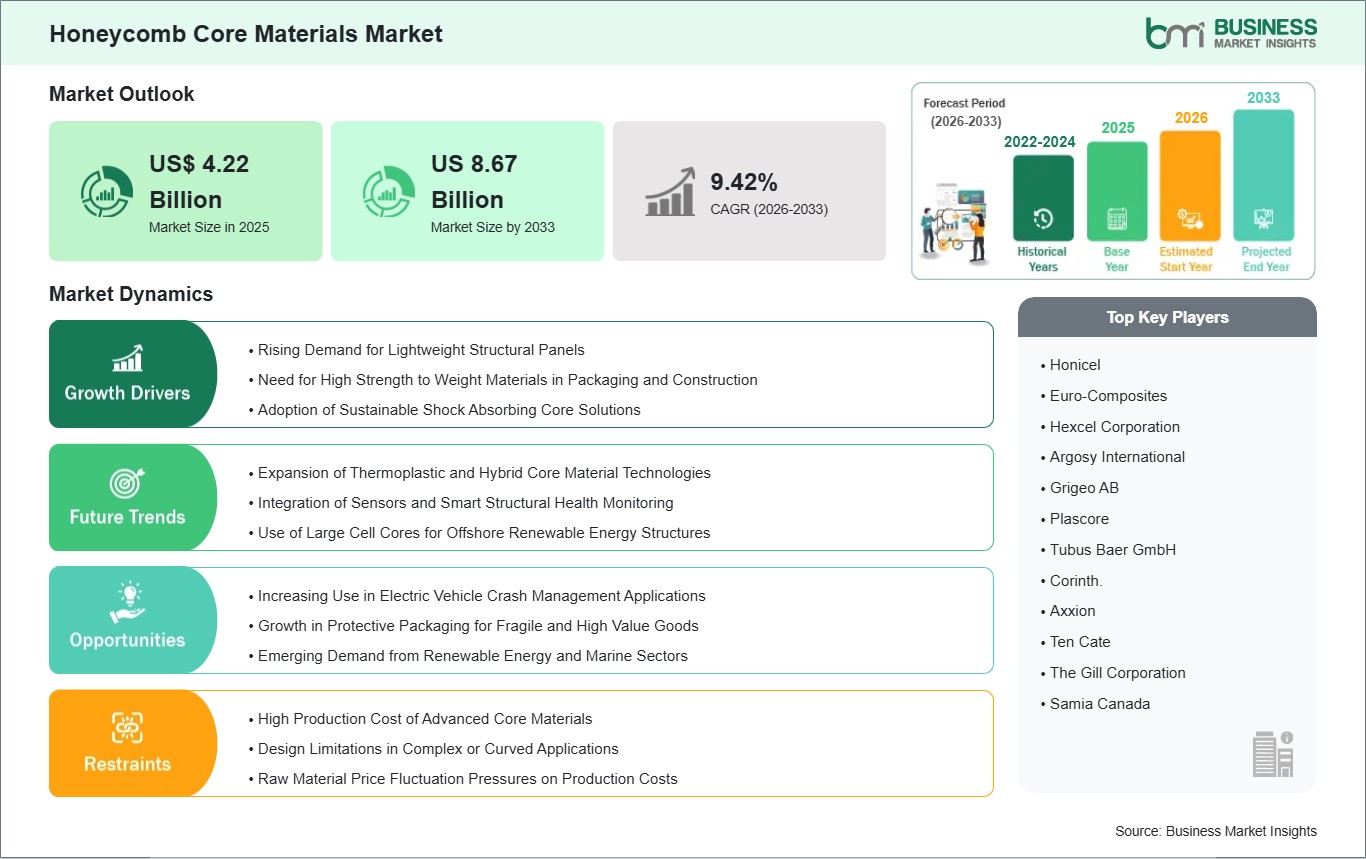

The Honeycomb Core Materials Market size is expected to reach US$ 8.67 Billion by 2033 from US$ 4.22 Billion in 2025. The market is estimated to record a CAGR of 9.42% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global honeycomb core materials market represents a niche segment of advanced composite materials, which are engineered materials that have the best strength-to-weight ratios and energy absorption characteristics. Honeycomb core materials are the internal layers of composite materials, which are used to make the structure rigid and stable with minimal weight. The industry scope of honeycomb core materials is vast and includes aerospace, automotive, marine, construction, wind energy, and industrial packaging sectors, indicating the increasing requirement for lightweight, durable, and high-performance materials. In the aerospace and transportation industry, honeycomb core materials play a vital role in reducing the weight of vehicles and ensuring the safety of the vehicles. The major driving forces for the market are industrial and environmental requirements, which emphasize the use of lightweight, high-strength, and environmentally friendly materials.

The growing requirements for energy-efficient automobiles, fuel-efficient aircraft, and environmentally friendly building materials have increased the popularity of using honeycomb core materials. The improvements made to the materials, including aluminum, Nomex, polymer, and thermoplastic core materials, have improved the versatility of the materials for a wide range of applications. However, there are challenges in production complexity and cost. The production of honeycomb core materials involves complex processes that require strict control in cell geometry, materials used, and bonding techniques. Besides that, there is competition from other lightweight materials such as lattice materials, foams, and other composite materials. To keep up with the competition, manufacturers of honeycomb core materials are challenged to be innovative and meet design expectations. The global market for honeycomb core materials is characterized by cutting-edge materials and the needs of modern industrial applications.

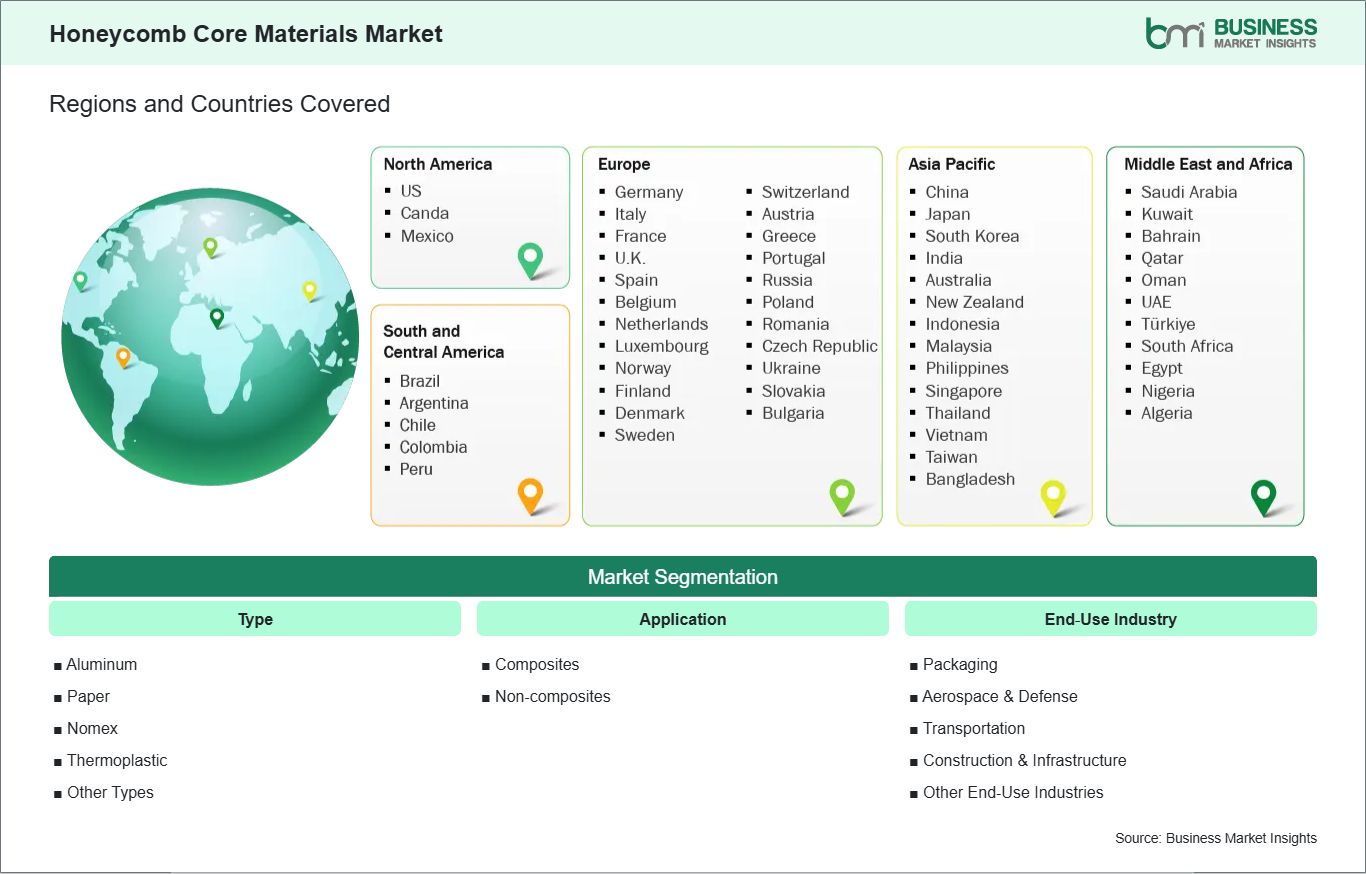

Key segments that contributed to the derivation of the honeycomb core materials market analysis are type, application, and end‑use industry.

By type, the honeycomb core materials market is segmented into aluminum, paper, Nomex, thermoplastic, and others. The aluminum subsegment dominated the market in 2025.

Based on application, the honeycomb core materials market is classified into composites and non‑ The composites subsegment dominated the market in 2025.

In terms of end‑use industry, the honeycomb core materials market is divided into packaging, aerospace & defense, transportation, construction & infrastructure, and other end‑use industries. The aerospace & defense subsegment dominated the market in 2025.

Honeycomb Core Materials Market Drivers and Opportunities:

Rising Demand for Lightweight Structural Panels

The global demand for honeycomb core materials is being strongly driven by the need for lightweight structural panels across multiple industries. In aerospace, automotive, and marine applications, reducing the weight of panels is essential for improving fuel efficiency, operational performance, and overall sustainability. Honeycomb cores provide an ideal combination of high strength and low weight, allowing manufacturers to create panels that are structurally robust while minimizing mass. This lightweighting strategy is becoming increasingly critical as transportation sectors aim to meet stricter emission regulations and optimize energy efficiency without compromising safety or durability.

In construction and industrial applications, honeycomb panels are also being adopted for their superior strength-to-weight ratio and ease of installation. Building facades, partition walls, and flooring systems benefit from materials that offer rigidity while remaining lightweight, reducing structural load and simplifying logistics. Honeycomb cores can be combined with different surface skins, such as aluminum, composite, or polymer layers, to tailor properties like thermal insulation, fire resistance, and acoustic performance. This adaptability makes honeycomb core panels a versatile solution for modern engineering challenges worldwide, from high-rise buildings to modular construction systems.

Moreover, the general trend towards more sustainable and efficient designs within the international arena is also adding to the usage of honeycomb core materials. Industries are using these materials to ensure that the overall usage of raw materials does not increase while providing the necessary strength to the panels. This way, engineers can ensure that the panels are not only light in weight but also more efficient and environmentally friendly. This way, the overall trend within the industry will be to ensure that honeycomb core materials are used to provide the necessary support to the panels.

Increasing Use in Electric Vehicle Crash Management Applications

The growing adoption of electric vehicles (EVs) is creating significant opportunities for honeycomb core materials in crash management applications. EVs require advanced structural solutions to protect battery packs, passenger compartments, and critical electronics during collisions. Honeycomb cores are increasingly integrated into door panels, bumpers, floor structures, and energy-absorbing zones to manage crash energy effectively while maintaining lightweight construction. Their high energy absorption capacity and ability to deform in a controlled manner make them an ideal material for meeting stringent safety standards without adding unnecessary mass.

The honeycomb cores are also useful in innovative designs for EVs that emphasize the safety of passengers. Vehicle manufacturers are using this material to develop multi-layered materials and modules that can be used to make the cars more crashworthy. This is because the honeycomb core can be used in combination with metals, composites, and polymers to produce the desired mechanical properties. This is important in designing EVs because the weight and battery need to be taken into account to ensure the safety and efficiency of the vehicle.

The honeycomb cores have also played a significant role in the development and implementation of international initiatives for improving the safety of EVs. Vehicle manufacturers are using this material to ensure that the objectives of making the cars more efficient and safe are met. This is important in meeting the demands of consumers for more efficient and safe cars. The use of honeycomb cores in modern designs for EVs has ensured that the cars are more efficient and safe. In addition, the material has helped in the promotion of sustainability in the automotive industry. This has made the honeycomb core materials essential in managing crashes in cars in the international automotive industry.

Honeycomb Core Materials Market Size and Share Analysis:

The honeycomb core materials market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within type, application, and end‑use industry, highlighting their respective contributions to overall market performance.

By type, the Aluminum subsegment dominated the Honeycomb Core Materials market in 2025. Aluminum core materials offer high strength-to-weight ratio, corrosion resistance, and structural stability, making them highly suitable for advanced engineering applications, driving their widespread adoption.

Based on application, the Composites subsegment dominated the Honeycomb Core Materials market in 2025. Composite applications benefit from enhanced mechanical performance, lightweight design, and durability, supporting strong demand in industries requiring high-performance materials.

In terms of end-use industry, the Aerospace & Defense subsegment dominated the Honeycomb Core Materials market in 2025. Aerospace and defense applications require lightweight, strong, and reliable core materials for structural components, reinforcing the dominance of this segment in the market.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Honicel

Euro-Composites

Hexcel Corporation

Argosy International

Grigeo AB

Plascore

Tubus Baer GmbH

Corinth.

Axxion

Ten Cate

The Gill Corporation

Samia Canada

Corex Honeycomb

Get more information on this report

Honeycomb Core Materials Market Report Coverage and Deliverables:

The "Honeycomb Core Materials Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Honeycomb Core Materials market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Honeycomb Core Materials market trends, as well as drivers, restraints, and opportunities

Honeycomb Core Materials market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Honeycomb Core Materials market

Detailed company profiles, including SWOT analysis

The geographical scope of the Honeycomb Core Materials market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Honeycomb Core Materials market in North America is expected to grow during the forecast period.

North America has a commanding position in the honeycomb core materials market due to its mature industrial base and advanced manufacturing infrastructure. North America is also home to a number of end-user industries that require honeycomb core materials. The aerospace industry is one of the prominent segments that make use of honeycomb core materials in aircraft floors, aircraft bodies, aircraft wings, and aircraft interior fitments. These materials are also used in the automotive industry to manufacture high-performance cars and electric cars. The weight-reducing properties of honeycomb core materials make them suitable for automotive applications. Other than the transportation industry, North America's construction industry and renewable energy industry also make significant use of honeycomb core materials. In the construction industry, honeycomb core materials are used to make building facades and building panels.

The weight-reducing properties and insulating properties of honeycomb core materials make them suitable for the construction industry. In the renewable energy industry, wind turbine blade manufacturers make significant use of honeycomb core materials. This is because the weight-reducing properties of honeycomb core materials make them suitable for wind turbine blade manufacturing.

North America’s market leadership is further reinforced by the development of an efficient supply chain, where the production, purification, and precise manufacturing of materials are well established. Companies are investing heavily in R&D activities to create customized solutions for specific applications, ensuring the optimal performance of the product. Sustainability programs are also helping the industry adopt recyclable aluminum and polymer-based core materials. With quality being an integral part of the industry, along with the development of the sector through innovation, North America has maintained its position as the leader in the global honeycomb core materials market.

Get more information on this report

Honeycomb Core Materials Market Research Report Guidance:

The report includes qualitative and quantitative data in the Honeycomb Core Materials market across type, application, end‑use industry, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Honeycomb Core Materials market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Honeycomb Core Materials market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Honeycomb Core Materials market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the Honeycomb Core Materials market segments by type, application, end‑use industry, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume, revenue forecast, and factors driving the market.

Chapter 11 describes the competitive analysis with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Honeycomb Core Materials market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Honeycomb Core Materials Market News and Key Development:

The honeycomb core materials market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the honeycomb core materials market are:

In December 2024, Hexcel Corporation announced that it partnered with Boeing to support development of the U.S. Navy’s MQ‑25 Stingray unmanned aerial refueling aircraft by evaluating Hexcel’s Flex‑Core HRH‑302 honeycomb core materials for use in high‑temperature structural components, showcasing expanded application of its advanced honeycomb solutions in aerospace defense programs.

In September 2024, Hexcel Corporation announced the launch of its new Flex‑Core HRH‑302 mid‑temperature honeycomb core product, designed to offer enhanced thermal performance for aerospace and advanced applications while maintaining high strength and lightweight characteristics.

Key Sources Referred:

International Organization for Standardization (ISO)American Society for Testing and Materials (ASTM International)Bureau of Indian Standards (BIS)Environmental Protection Agency (EPA), USAEuropean Chemicals Agency (ECHA)Central Pollution Control Board (CPCB), IndiaMinistry of Chemicals and Fertilizers, IndiaAmerican Chemistry Council (ACC)Indian Chemical Council (ICC)European Chemical Industry Council (Cefic)Specialty Chemical Association of India (SCAI)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Honeycomb Core Materials Market

Honicel

Euro-Composites

Hexcel Corporation

Argosy International

Grigeo AB

Plascore

Tubus Baer GmbH

Corinth.

Axxion

Ten Cate

The Gill Corporation

Samia Canada

Corex Honeycomb

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Honeycomb Core Materials Market?

The Honeycomb Core Materials Market is valued at US$ 4.22 Billion in 2025, it is projected to reach US 8.67 Billion by 2033.

What is the CAGR for Honeycomb Core Materials Market by (2026 - 2033)?

As per our report Honeycomb Core Materials Market, the market size is valued at US$ 4.22 Billion in 2025, projecting it to reach US 8.67 Billion by 2033. This translates to a CAGR of approximately 9.42% during the forecast period.

What segments are covered in this report?

The Honeycomb Core Materials Market report typically cover these key segments-

Type (Aluminum, Paper, Nomex, Thermoplastic, Other Types)

Application (Composites, Non-composites)

End-Use Industry (Packaging, Aerospace & Defense, Transportation, Construction & Infrastructure, Other End-Use Industries)

What is the historic period, base year, and forecast period taken for Honeycomb Core Materials Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Honeycomb Core Materials Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Honeycomb Core Materials Market?

The Honeycomb Core Materials Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Honicel

Euro-Composites

Hexcel Corporation

Argosy International

Grigeo AB

Plascore

Tubus Baer GmbH

Corinth.

Axxion

Ten Cate

The Gill Corporation

Samia Canada

Corex Honeycomb

Who should buy this report?

The Honeycomb Core Materials Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Honeycomb Core Materials Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Honeycomb Core Materials Market

Get Free Sample For Honeycomb Core Materials Market