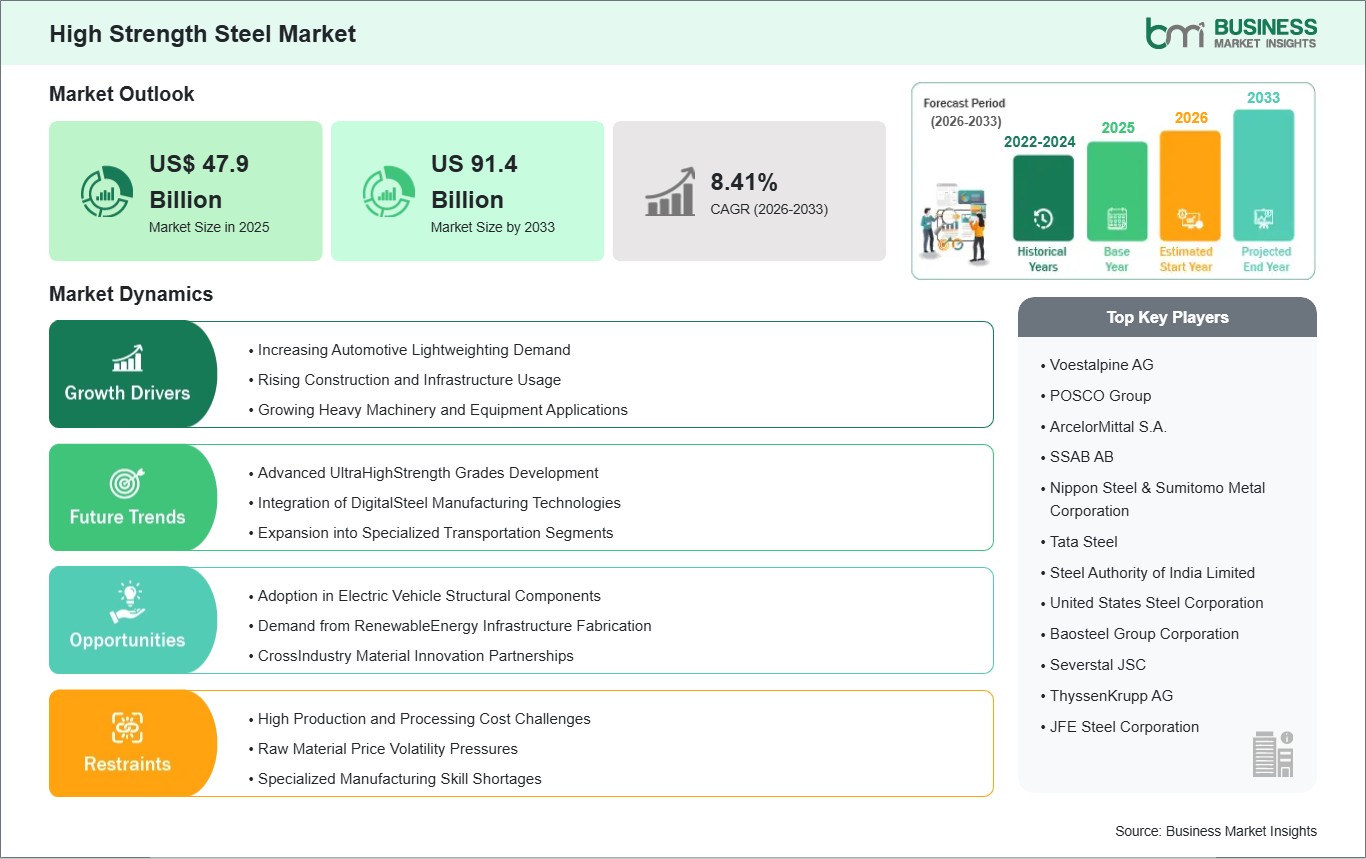

The High Strength Steel Market size is expected to reach US$ 91.4 Billion by 2033 from US$ 47.9 Billion in 2025. The market is estimated to record a CAGR of 8.41% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global high strength steel market is an integral part of the overall steel and construction materials sector, delivering engineering solutions with high strength, durability, and cost-effectiveness. High strength steel products are engineered to achieve higher tensile, fatigue, and impact properties, along with the benefits of reduced material and structural weight. The product has found considerable application in various industries due to its high demand. The increasing global focus on lightweight structures, energy efficiency, and improved safety standards in various industries has given the high strength steel market a considerable boost. The major factors are the rising demand for the use of high strength steel in the automotive industry, especially in the manufacture of lightweight yet crash-resistant car frames, and the extensive use of the material in infrastructure development requiring strong and long-lasting structural materials.

Technological improvements in the production of the material, including improvements in alloying techniques, hot and cold rolling of the material, and surface treatment of the material, have led to the development of different types of high strength steel suitable for specialized applications. However, the production of high strength steel also requires complex processes and quality control techniques, which have resulted in the increased cost of manufacture of the material. In addition, the use of other lightweight materials, like aluminum alloys and composites, has also acted as a constraint in the growth of the market for the material in certain sectors. Overall, the global high strength steel market is driven by the ability of the material to deliver performance and cost-effectiveness in challenging industrial conditions.

High Strength Steel Market - Strategic Insights:

Get more information on this report

High Strength Steel Market Segmentation Analysis:

Key segments that contributed to the derivation of the high strength steel market analysis are type, product type, application, and end‑use industry.

By type, the high strength steel market is segmented into high strength low alloy, dual phase, bake hardenable, carbon manganese, and other types. The high strength low alloy subsegment dominated the market in 2025.

Based on product type, the high strength steel market is classified into cold rolled, hot rolled, metallic coated, and direct rolled. The cold rolled subsegment dominated the market in 2025.

In terms of application, the high strength steel market is divided into body and closures, suspensions, bumper and intrusion beams, and other applications. The body and closures subsegment dominated the market in 2025.

On the basis of end‑use industry, the high strength steel market is segmented into automotive, construction, yellow goods & mining equipment, aviation & marine, and other end‑use industries. The automotive subsegment dominated the market in 2025.

High Strength Steel Market Drivers and Opportunities:

Increasing Automotive Lightweighting Demand

The global demand for high strength steel is being significantly driven by the automotive industry’s focus on lightweighting vehicles to enhance fuel efficiency, reduce emissions, and meet stricter regulatory standards. Automakers are increasingly replacing traditional steel components with high strength steel in structural frames, chassis, body panels, and suspension systems. This allows vehicles to maintain crashworthiness and durability while reducing overall mass. Lightweighting not only improves fuel efficiency in internal combustion engine vehicles but also enhances performance, handling, and safety, making high strength steel a critical material for modern automotive design.

Technological advancements in steel manufacturing processes, such as the creation of advanced high-strength steels (AHSS) and ultra-high-strength steels (UHSS), have increased the utilization of these products in automotive manufacturing. These materials provide an excellent balance of high strength, ductility, and formability. This enables complex designs in lightweight structures without compromising their integrity. The end result is thinner components that can withstand high levels of stress while providing further weight reduction in vehicles without compromising safety standards. This is an international phenomenon in mass-market as well as luxury vehicles.

Moreover, the increasing adoption of lightweight design principles extends beyond passenger vehicles to commercial and specialty vehicles, such as trucks, vans, and buses, where fuel efficiency and payload optimization are crucial. High strength steel allows manufacturers to reduce weight while retaining necessary strength for load-bearing structures. With the rise of urban delivery fleets and eco-conscious transportation initiatives, the demand for lightweight, high-strength materials is growing worldwide. As environmental regulations tighten and consumers demand more efficient vehicles, high strength steel is becoming an essential material for automotive lightweighting strategies globally.

Adoption in Electric Vehicle Structural Components

The shift to electric vehicles (EVs) across the globe is opening doors for the use of high strength steel, especially for structural parts of the vehicle, as weight, safety, and battery protection are major concerns for the material selection of EVs. The use of high strength steel in the battery enclosures, floors, side impact beams, and roof rails of the vehicle helps to meet the required safety parameters without adding weight to the vehicle, which is a major concern for the batteries of the vehicle. High strength steel is the best choice for the platforms of EVs across the globe.

In addition, high strength steel facilitates innovative design approaches in EVs, such as modular platforms and multi-material structures. Automakers are combining high strength steel with aluminum and composites to achieve optimized weight distribution and improved range, while still maintaining structural rigidity. The material’s formability and weldability are crucial for producing complex geometries needed to accommodate large battery modules, electronic systems, and passenger compartments. This has made high strength steel a key enabler in scaling EV production and meeting global demand for environmentally friendly transportation.

Finally, the focus on EV safety, regulatory compliance, and durability further reinforces the adoption of high strength steel. Battery protection, crash energy management, and chassis reinforcement are critical design considerations, and high strength steel provides a cost-effective solution without compromising performance. As the global EV market expands across all continents, high strength steel continues to play a central role in enabling lightweight, safe, and efficient electric vehicles, supporting the transition toward sustainable mobility on a worldwide scale.

High Strength Steel Market Size and Share Analysis:

The high strength steel market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within type, product type, application, and end‑use industry, highlighting their respective contributions to overall market performance.

By type, the High Strength Low Alloy subsegment dominated the High Strength Steel market in 2025. High strength low alloy steels offer an excellent combination of strength, toughness, and formability, making them highly suitable for structural and automotive applications, driving their widespread adoption.

Based on product type, the Cold Rolled subsegment dominated the High Strength Steel market in 2025. Cold rolled steel provides superior surface finish, dimensional accuracy, and mechanical properties, supporting strong demand in precision applications.

In terms of application, the Body and Closures subsegment dominated the High Strength Steel market in 2025. Body and closure components require high strength and crashworthiness, reinforcing the dominance of this segment in automotive manufacturing.

On the basis of end-use industry, the Automotive subsegment dominated the High Strength Steel market in 2025. Automotive applications demand lightweight, high-strength materials to enhance safety, fuel efficiency, and performance, driving widespread adoption of high strength steel in this sector.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Voestalpine AG

POSCO Group

ArcelorMittal S.A.

SSAB AB

Nippon Steel & Sumitomo Metal Corporation

Tata Steel

Steel Authority of India Limited

United States Steel Corporation

Baosteel Group Corporation

Severstal JSC

ThyssenKrupp AG

JFE Steel Corporation

Nucor Corporation

JSW Steel

Get more information on this report

High Strength Steel Market Report Coverage and Deliverables:

The "High Strength Steel Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

High Strength Steel market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

High Strength Steel market trends, as well as drivers, restraints, and opportunities

High Strength Steel market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the High Strength Steel market

Detailed company profiles, including SWOT analysis

High Strength Steel Market Geographic Insights:

The geographical scope of the High Strength Steel market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The High Strength Steel market in North America is expected to grow during the forecast period.

North America holds a large share in the global market for high strength steel, driven by a well-structured industrial environment and extensive infrastructure development. The automotive sector in the United States and Canada is one of the key industries to utilize high strength steel to develop more fuel-efficient vehicles without compromising safety parameters. Vehicle frames, chassis components, and reinforcement structures make extensive use of high strength steel to improve crashworthiness and reduce vehicle weights, keeping in view safety and environmental concerns.

In the construction and infrastructure development sector, North America prefers to utilize high strength steel for building bridges, commercial buildings, and infrastructure, where long-term durability and resistance to environmental conditions are key parameters. Similarly, in the energy sector, high strength steel is being used for developing pipelines, drilling rigs, and offshore platforms, where mechanical properties and fatigue resistance are key requirements to withstand severe operating conditions.

The region’s dominance is further reinforced by its advanced steel production technologies, including sophisticated rolling, alloying, and heat treatment methods that enable the manufacture of high-quality, customized steel grades. Strong research and development capabilities allow North American producers to innovate and supply specialized steel solutions tailored to specific industrial needs. At the same time, environmental regulations and sustainability initiatives are influencing the adoption of recyclable and energy-efficient production practices. North America’s combination of technological expertise, industrial diversity, and high-quality standards ensures its continued leadership in the global high strength steel market.

Get more information on this report

High Strength Steel Market Research Report Guidance:

The report includes qualitative and quantitative data in the High Strength Steel market across type, product type, application, end‑use industry, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the High Strength Steel market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the High Strength Steel market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the High Strength Steel market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover the High Strength Steel market segments by type, product type, application, end‑use industry, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume, revenue forecast, and factors driving the market.

Chapter 12 describes the competitive analysis with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the High Strength Steel market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

High Strength Steel Market News and Key Development:

The high strength steel market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the high strength steel market are:

In February 2026, voestalpine AG announced strong strategic progress in its High Performance Metals Division and ongoing international growth projects, reaffirming its focus on technologically demanding high‑performance steel products (including advanced high strength materials) as part of its broader strategy despite reorganization and challenging market conditions in automotive and European industries.

In April 2025, SSAB AB announced that it signed an Early Services Agreement with SMS group to build a new cold rolling complex in Luleå, Sweden, enabling SSAB to produce third‑generation advanced high‑strength steels (AHSS) with an annual capacity of about 1.3 million tonnes for the automotive sector using sustainable and energy‑efficient production technologies.

Key Sources Referred:

International Organization for Standardization (ISO)American Society for Testing and Materials (ASTM International)Bureau of Indian Standards (BIS)Environmental Protection Agency (EPA), USAEuropean Chemicals Agency (ECHA)Central Pollution Control Board (CPCB), IndiaMinistry of Chemicals and Fertilizers, IndiaAmerican Chemistry Council (ACC)Indian Chemical Council (ICC)European Chemical Industry Council (Cefic)Specialty Chemical Association of India (SCAI)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - High Strength Steel Market

Voestalpine AG

POSCO Group

ArcelorMittal S.A.

SSAB AB

Nippon Steel & Sumitomo Metal Corporation

Tata Steel

Steel Authority of India Limited

United States Steel Corporation

Baosteel Group Corporation

Severstal JSC

ThyssenKrupp AG

JFE Steel Corporation

Nucor Corporation

JSW Steel

About Author— Chemicals and Materials Research Team

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Frequently Asked Questions

How big is the High Strength Steel Market?

The High Strength Steel Market is valued at US$ 47.9 Billion in 2025, it is projected to reach US$ 91.4 Billion by 2033.

What is the CAGR for High Strength Steel Market by (2026 - 2033)?

As per our report High Strength Steel Market, the market size is valued at US$ 47.9 Billion in 2025, projecting it to reach US$ 91.4 Billion by 2033. This translates to a CAGR of approximately 8.41% during the forecast period.

What segments are covered in this report?

The High Strength Steel Market report typically cover these key segments-

Type (High Strength Low Alloy, Dual Phase, Bake Hardenable, Carbon Manganese, Other Types)

Product Type (Cold rolled, Hot rolled, Metallic coated, Direct rolled)

Application (Body and Closures, Suspensions, Bumper and Intrusion Beams, Other Applications)

End-Use Industry (Automotive, Construction, Yellow Goods & Mining Equipment, Aviation & Marine, Other End-Use Industries)

What is the historic period, base year, and forecast period taken for High Strength Steel Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the High Strength Steel Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in High Strength Steel Market?

The High Strength Steel Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Voestalpine AG

POSCO Group

ArcelorMittal S.A.

SSAB AB

Nippon Steel & Sumitomo Metal Corporation

Tata Steel

Steel Authority of India Limited

United States Steel Corporation

Baosteel Group Corporation

Severstal JSC

ThyssenKrupp AG

JFE Steel Corporation

Nucor Corporation

JSW Steel

Who should buy this report?

The High Strength Steel Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the High Strength Steel Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For High Strength Steel Market

Get Free Sample For High Strength Steel Market