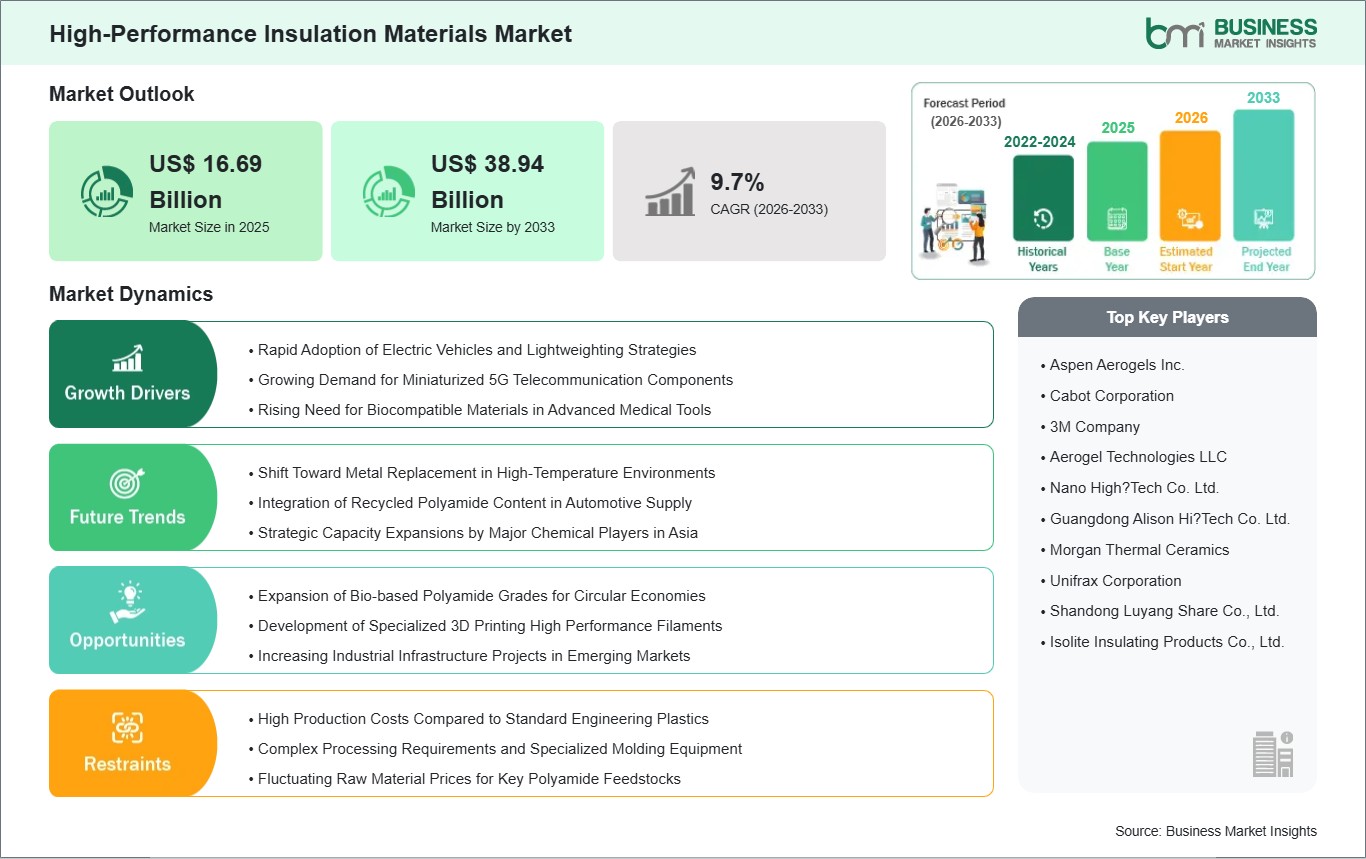

The High-Performance Insulation Materials Market size is expected to reach US$ 38.94 Billion by 2033 from US$ 16.69 Billion in 2025. The market is estimated to record a CAGR of 11.17% from 2026 to 2033.

Executive Summary and Global Market Analysis:

High-performance insulation materials (HPIM) play a critical role in the thermal management of extreme environments, offering superior resistance to heat transfer compared to traditional materials. They are essential for industries such as oil and gas, automotive, aerospace, construction, and power generation. HPIMs have several advantages, including ultra-low thermal conductivity, lightweight profiles, and the ability to operate in space-constrained applications where thickness is a limiting factor. Increasing global energy efficiency mandates, the rise of electric vehicles (EVs) requiring advanced battery thermal barriers, and the growing demand for deep-sea and cryogenic logistics are fueling the market. Additionally, innovations in nanotechnology, bio-based precursors, and smart insulation with integrated sensors are enhancing material efficiency and reliability.

However, some challenges that can hamper the expansion of the market are the high production costs, the intricate process involved in manufacturing certain products (such as aerogels, which require supercritical drying), as well as the complexity involved in the regulations related to the handling of certain fibers. There are certain raw materials used in the process that are high-cost specialty raw materials, thus affecting the costs. Despite the challenges, the market invariably presents some opportunities, including the expansion of LNG infrastructures, the development of zero-energy buildings, the increased demand for industrial-grade high-performance coatings, and the development potential offered by investment in sustainable products with the ability to recycle insulation, amongst others.

Key segments that contributed to the derivation of the high-performance insulation materials market analysis are material type and application.

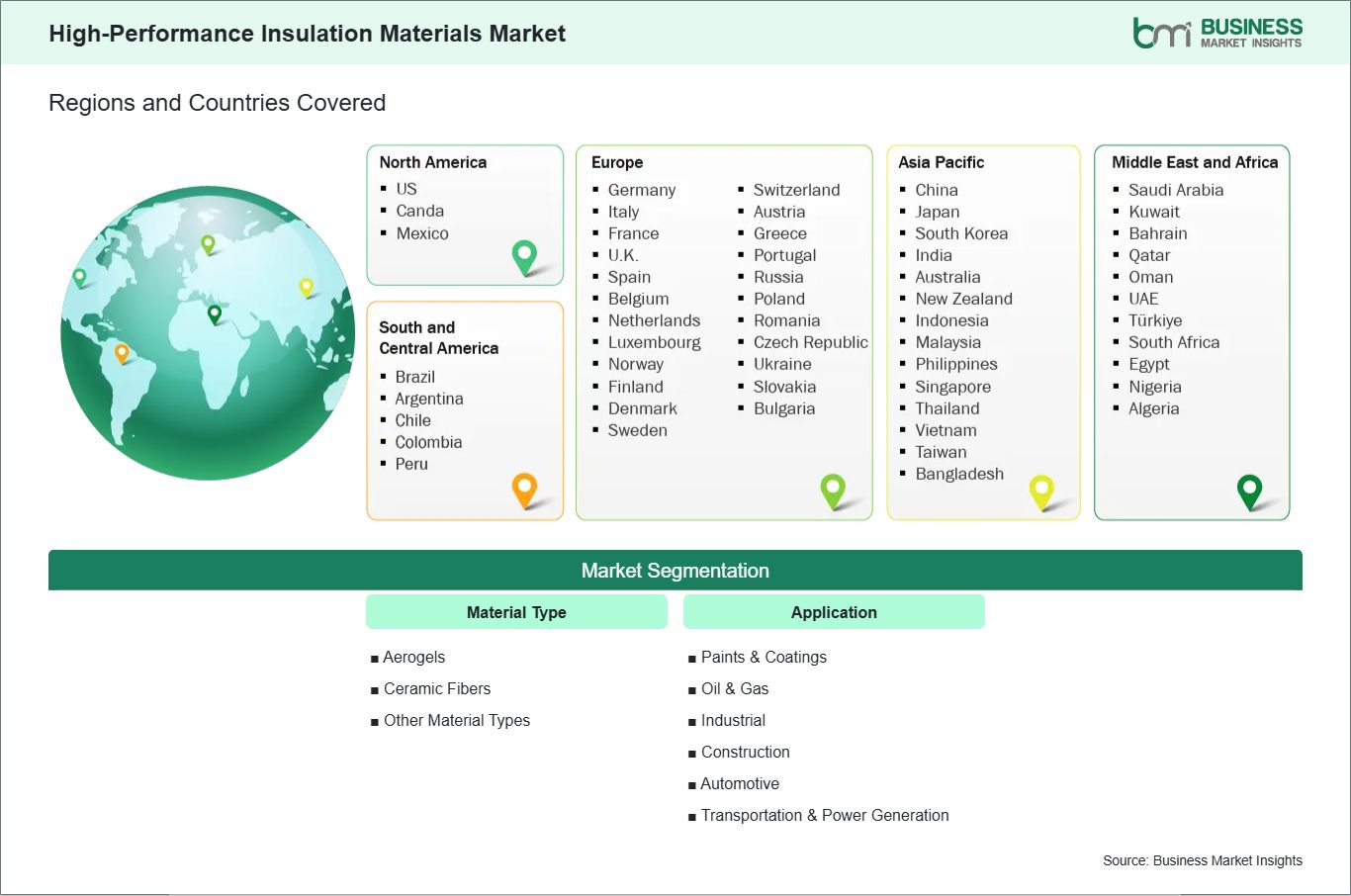

By Material Type, the market is segmented into Aerogels, Ceramic Fibers, and Others.

By Application, the market is categorized into Paints &Coatings, Oil &Gas, Industrial, Construction, Automotive, and Transportation &Power Generation.

High-Performance Insulation Materials Market Drivers and Opportunities:

Strict Government Regulations Regarding Global Energy Efficiency Standards

The global push for decarbonization and energy conservation has emerged as a primary driver for the high-performance insulation materials market. Governments worldwide are implementing stringent building codes and industrial mandates to reduce greenhouse gas emissions and optimize energy consumption. In the European Union and North America, policies such as the Energy Performance of Buildings Directive (EPBD) are compelling builders to adopt materials with superior thermal resistance.

High-performance materials like aerogels and vacuum insulation panels (VIPs) allow for compliance with these strict R-value requirements without increasing the thickness of walls or equipment linings. This is particularly crucial in urban cities where floor spaces have become valuable and where traditional forms of insulation have become unsustainable due to their bulkiness. Moreover, with the climate change demands rising for increased efficiency in the reduction of the generated waste through the retention of less wanted types of waste generated in processes while keeping high levels of temperature in the processes of industries that are likely to become compliance with the new-age philosophy of corporations, high-performance insulations such as high-performance ceramic fibers and foams are rising at a rate that can only be referred to as the fastest rate ever. Such an environment boosts the importance of high-performance insulations as an expenditure rather than a choice.

Growing Demand for Thermal Management in the Electric Vehicle Sector

The rapid global transition toward electric mobility is fundamentally reshaping the demand for high-performance insulation materials. Unlike internal combustion engine vehicles, electric vehicles (EVs) require sophisticated thermal management systems to protect sensitive battery packs and ensure passenger safety. High-performance materials, particularly aerogels and specialty ceramic mats, are increasingly used as "thermal runaway" barriers. These materials prevent the heat from a single failing battery cell from spreading to adjacent cells, thereby mitigating the risk of vehicle fires. Because weight and space are critical factors in EV design, the ultra-thin and lightweight nature of high-performance insulation provides a significant advantage over traditional alternatives.

Manufacturers are investing heavily in these materials to extend battery life and improve vehicle range by maintaining optimal operating temperatures in various climates. Additionally, the need for acoustic insulation in the quiet cabins of EVs is driving the adoption of high-performance foams that offer dual thermal and noise-reduction properties. As EV production scales globally, particularly in China and North America, the automotive application segment is becoming a dominant force in the high-performance insulation market, fostering continuous innovation in material science to meet the rigorous safety standards of the next generation of transportation.

High-Performance Insulation Materials Market Size and Share Analysis:

The high-performance insulation materials market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within material type and application, offering insights into their contribution to overall market performance.

Based on material type, the ceramic fibers typically represent a significant share. These fibers are widely utilized across various industries due to their unmatched thermal stability in environments exceeding 1000°C, making them essential for furnaces and kilns.

In terms of applications, the Construction sector is also a significant contributor, utilizing these materials to achieve LEED and green building certifications. Paints &Coatings with high-performance insulation properties are gaining traction as they provide a versatile, sprayable thermal barrier for irregular industrial surfaces and marine applications.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Aspen Aerogels Inc.

Cabot Corporation

3M Company

Aerogel Technologies LLC

Nano High-Tech Co. Ltd.

Guangdong Alison Hi-Tech Co. Ltd.

Morgan Thermal Ceramics

Unifrax Corporation

Shandong Luyang Share Co., Ltd.

Isolite Insulating Products Co.,Ltd.

Get more information on this report

High-Performance Insulation Materials Market Report Coverage and Deliverables:

The "High-Performance Insulation Materials Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

High-Performance Insulation Materials market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

High-Performance Insulation Materials market trends, as well as market dynamics such as drivers, restraints, and key opportunities

High-Performance Insulation Materials market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the High-Performance Insulation Materials market

Detailed company profiles, including SWOT analysis

The geographical scope of the market is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

The Asia-Pacific high-performance insulation materials market is segmented into China, Japan, South Korea, India, and the Rest of Asia. The region is experiencing robust growth, driven by the rapid expansion of industrial manufacturing, massive infrastructure investments, and the development of free trade zones. Major economies like China and India are leading the way, fueled by increasing power generation needs and the growth of the regional EV supply chain.

The region is also witnessing increased adoption of advanced logistics technologies and temperature-controlled storage systems, particularly relevant for sectors like petrochemicals and heavy industry. Capacity expansion by regional manufacturers, alongside fleet modernization efforts in the transportation sector, is enhancing operational efficiency. Additionally, the rise of regional trade agreements (such as RCEP) further solidifies the region's dominant market position.

The North American market, led by the U.S. and Canada, is projected to witness the fastest growth rate during the forecast period. This acceleration is attributed to the strict enforcement of building codes and energy standards, such as California's Title 24. Significant investments in retrofitting aging industrial infrastructure and the rapid expansion of the electric vehicle (EV) supply chain are creating a robust market for advanced thermal barriers. Meanwhile, Europe remains a mature yet innovative market, driven by the European Green Deal and a strong focus on high-performance materials like vacuum insulation panels (VIPs) for zero-energy building projects.

Get more information on this report

High-Performance Insulation Materials Market Research Report Guidance:

The report includes qualitative and quantitative data in the High-Performance Insulation Materials market across material type, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the High-Performance Insulation Materials market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the High-Performance Insulation Materials market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the High-Performance Insulation Materials market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover High-Performance Insulation Materials market segments by material type, application, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the High-Performance Insulation Materials market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

High-Performance Insulation Materials Market News and Key Development:

The High-Performance Insulation Materials market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the high-performance insulation materials market are:

In January 2026, Henkel announced the launch of Loctite STYCAST US 8000 A/B, a next-generation two-component polyurethane potting compound designed to deliver exceptional electrical insulation, mechanical durability, and long-term reliability in demanding environments. This new solution strengthens Henkel's portfolio of high-performance encapsulation materials and supports customers seeking enhanced protection for mission-critical industrial and power electronics assemblies.

In June 2025, Armacell announced to opens new aerogel insulation plant in India to manufacture the breakthrough ArmaGel XG product line. The new ArmaGel XG product line in Pune is available for high-temperature applications, plus cryogenic and dual-temperature conditions. Specifically, ArmaGel XGH is engineered for operating temperatures up to +650°ׄC (+1200°F) and is compliant with ASTM C1728 Type III and JIP 33. ArmaGel XGC is ideal for cryogenic and dual-temperature conditions between -196°C (-321ºF) and +250°C (+482ºF) and is compliant with ASTM C1728 Type I and Type IV. Consequently, Armacell's aerogel blanket manufacturing available capacity has doubled to meet the rapidly growing demand for aerogel-based insulation solutions.

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - High-Performance Insulation Materials Market

Aspen Aerogels Inc.

Cabot Corporation

3M Company

Aerogel Technologies LLC

Nano High‑Tech Co. Ltd.

Guangdong Alison Hi‑Tech Co. Ltd.

Morgan Thermal Ceramics

Unifrax Corporation

Shandong Luyang Share Co., Ltd.

Isolite Insulating Products Co., Ltd.

Frequently Asked Questions

How big is the High-Performance Insulation Materials Market?

The High-Performance Insulation Materials Market is valued at US$ 16.69 Billion in 2025, it is projected to reach US$ 38.94 Billion by 2033.

What is the CAGR for High-Performance Insulation Materials Market by (2026 - 2033)?

As per our report High-Performance Insulation Materials Market, the market size is valued at US$ 16.69 Billion in 2025, projecting it to reach US$ 38.94 Billion by 2033. This translates to a CAGR of approximately 11.17% during the forecast period.

What segments are covered in this report?

The High-Performance Insulation Materials Market report typically cover these key segments-

Material Type (Aerogels, Ceramic Fibers, and Other Material Types)

Application (Paints & Coatings, Oil & Gas, Industrial, Construction, Automotive, and Transportation & Power Generation)

What is the historic period, base year, and forecast period taken for High-Performance Insulation Materials Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the High-Performance Insulation Materials Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in High-Performance Insulation Materials Market?

The High-Performance Insulation Materials Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Aspen Aerogels Inc.

Cabot Corporation

3M Company

Aerogel Technologies LLC

Nano High-Tech Co. Ltd.

Guangdong Alison Hi-Tech Co. Ltd.

Morgan Thermal Ceramics

Unifrax Corporation

Shandong Luyang Share Co., Ltd.

Isolite Insulating Products Co.,Ltd.

Who should buy this report?

The High-Performance Insulation Materials Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the High-Performance Insulation Materials Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For High-Performance Insulation Materials Market

Get Free Sample For High-Performance Insulation Materials Market