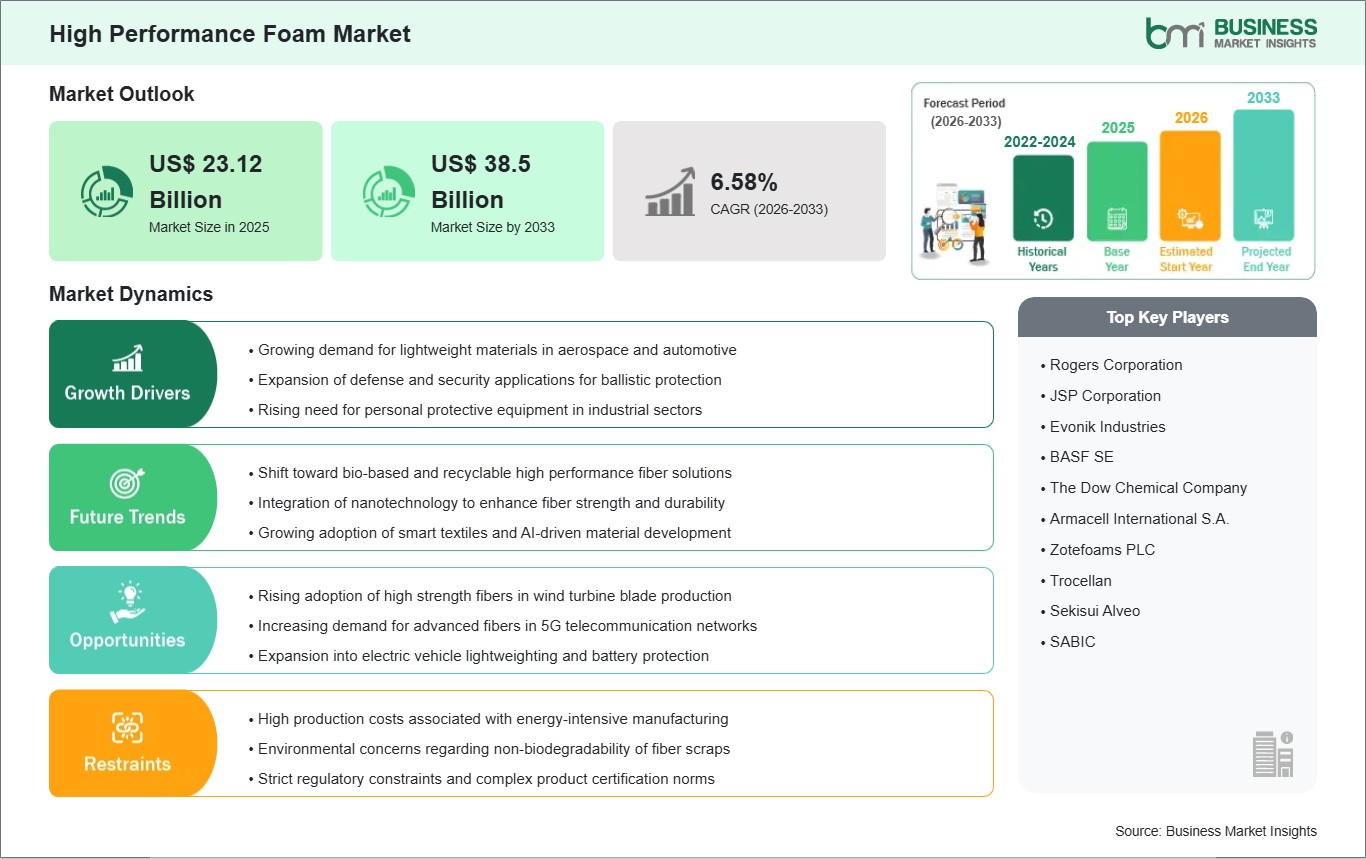

The High Performance Foam Market size is expected to reach US$ 38.5 Billion by 2033 from US$ 23.12 Billion in 2025. The market is estimated to record a CAGR of 6.58% from 2026 to 2033.

Executive Summary and Global Market Analysis:

High-performance foams are advanced cellular materials engineered to provide superior mechanical, thermal, and chemical properties compared to standard commodity foams. These technologies deliver significant clinical and economic value by enabling the extreme lightweighting of aerospace structures, offering efficient thermal barriers for electric vehicle (EV) battery packs, and ensuring the protection of delicate microelectronics from both physical impact and heat. Together, they form a critical portfolio that supports high-quality performance outcomes across the transportation, electronics, construction, and healthcare sectors. Market expansion is primarily attributed to the rising global demand for energy-efficient insulation, the rapid electrification of the automotive industry, and the increasing miniaturization of consumer devices. In addition, digital manufacturing and 3D-printing technologies are making it possible to create custom, complex lattice structures with different densities in specific areas, which is making processes much more efficient.

However, several challenges can restrain market growth: high initial procurement and processing costs, particularly for specialty materials like silicone and PMI (polymethacrylimide) foams, can limit adoption in high-volume, cost-sensitive consumer segments. Stringent regulatory hurdles, especially around certain blowing agents and volatile organic compound emissions, lengthen time-to-market for new formulations and increase compliance costs. The industry also faces constraints from technical complexities in material recycling, as the cross-linked nature of many high-performance thermoset foams makes them difficult to reprocess and conflicts with the global emphasis on circular economy mandates.

Despite these hurdles, the market holds immense opportunities in the universal mandate for sustainable and bio-based materials and the accelerating deployment of mycelium-based and CO2-derived foams. The expansion of medical-grade foams for advanced wound care and surgical positioning and the development of smart, phase-change foams that can actively regulate temperature in aerospace and electronics applications are expected to create significant opportunities for market growth.

High Performance Foam Market - Strategic Insights:

Get more information on this report

High Performance Foam Market Segmentation Analysis:

Key segments that contributed to the derivation of the High Performance Foam market analysis are type and end use industry.

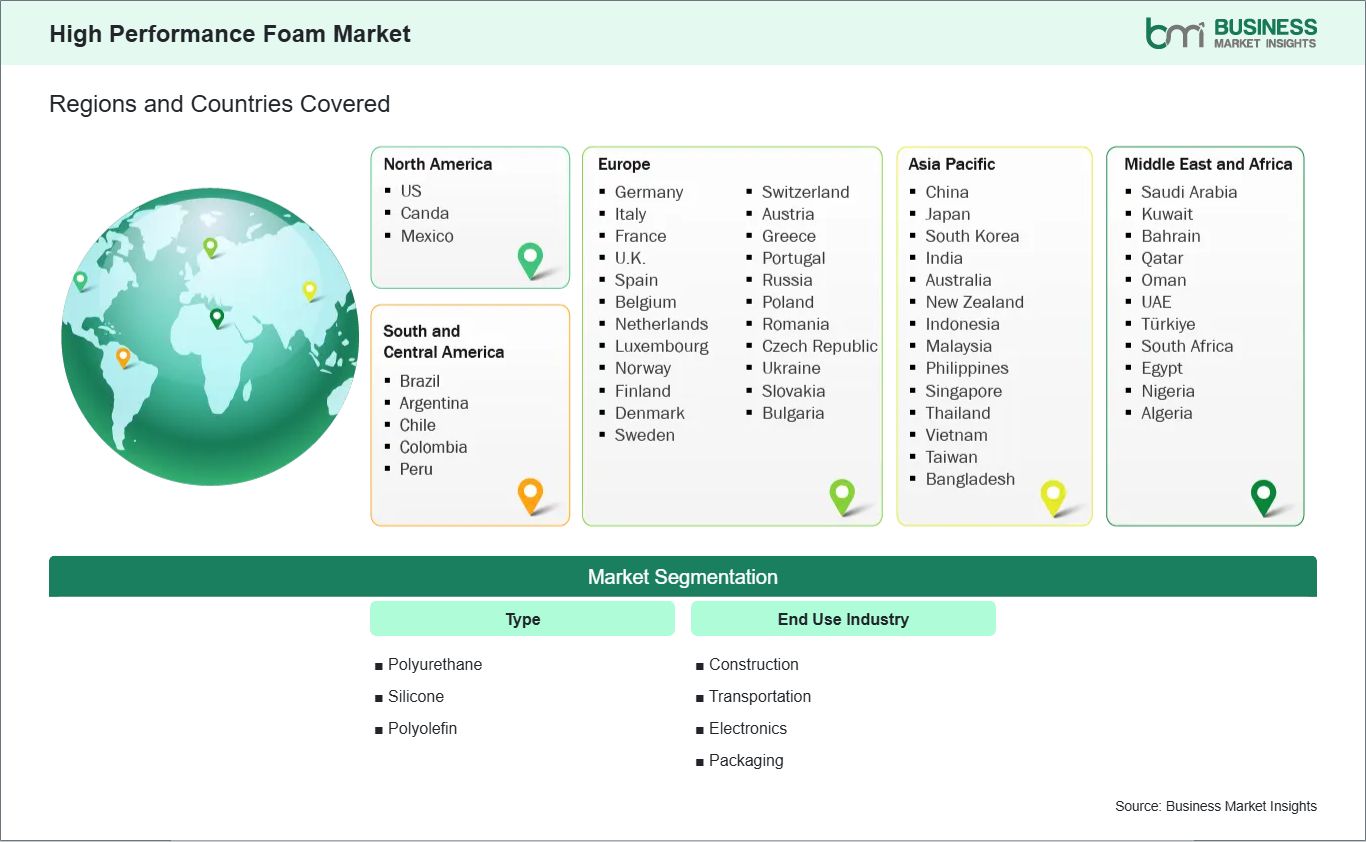

By Type, the market is segmented into Polyurethane, Silicone, and Polyolefin.

By End Use Industry, the market is divided into Construction, Transportation, Electronics, and Packaging.

High Performance Foam Market Drivers and Opportunities:

Advancing Industrial Efficiency and Global Safety Mandates

The primary driver for the High-Performance Foam Market is the growing global demand for materials that offer superior thermal insulation, acoustic dampening, and impact resistance without adding much mass. In the aerospace and automotive sectors, the push for "mass decompression" to improve fuel efficiency and battery range has made high-performance foams like polyetherimide (PEI) and specialized polyurethanes essential. These materials help manufacturers meet strict lightweighting targets and enhance passenger safety through advanced energy absorption.

Demand is also rising as the construction industry quickly shifts toward "Green Building" standards. To meet new energy codes such as the International Building Code (IBC) and net-zero goals, architects are specifying high-performance rigid foams for building envelopes to reduce thermal bridging. These cross-industry needs for energy conservation and structural integrity support steady growth, making high-performance foams a key part of modern industrial design and sustainable infrastructure.

Digital Material Discovery and Circular Economy Transition

Integrating AI-driven material informatics and digital twin technology into foam production represents a significant opportunity for value creation. Machine learning enables the simulation of cellular structures and the prediction of material behavior under extreme conditions, thereby reducing research and development timelines for customized, high-temperature, or chemical-resistant foam grades. The industry is seeing strong growth in the use of bio-based polyols and fully recyclable thermoplastic foams. With increasing pressure from regulations and the market to cut microplastics and lower Scope 3 emissions, making foams from renewable sources like soy, castor oil, or CO2-capture technology is becoming a compelling way for companies to stand out.

The expansion of cold chain logistics and medical packaging sectors presents significant potential for specialized foams engineered to deliver enhanced moisture resistance and temperature stability during the transportation of biologics and pharmaceuticals . Companies that pioneer modular, prefabricated foam insulation kits and those leading in "closed-loop" recycling programs are positioned to capture the highest-margin segments in an increasingly sustainability-focused global landscape.

High Performance Foam Market Size and Share Analysis:

The High Performance Foam market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within type and end use industry, offering insights into their contribution to overall market performance.

Based on type, the Polyurethane subsegment holds a significant market share. Polyurethane foams are indispensable for the Construction and Transportation sectors due to their unmatched versatility in both rigid and flexible forms. A notable trend in 2026 is the adoption of AI-driven "molecular modeling" to create hyper-dense closed-cell PU foams that achieve superior R-values for cryo-insulation and cold-chain logistics. These innovations are particularly vital in the renovation of legacy buildings to meet zero-emission standards, where they provide high-performance thermal barriers with minimal thickness.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Rogers Corporation

JSP Corporation

Evonik Industries

BASF SE

The Dow Chemical Company

Armacell International S.A.

Zotefoams PLC

Trocellan

Sekisui Alveo

SABIC

Get more information on this report

High Performance Foam Market Report Coverage and Deliverables:

The "High Performance Foam Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

High Performance Foam market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

High Performance Foam market trends, as well as market dynamics such as drivers, restraints, and key opportunities

High Performance Foam market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the High Performance Foam market

Detailed company profiles, including SWOT analysis

High Performance Foam Market Geographic Insights:

The geographical scope of the High Performance Foam market report is divided into five regions: North America, Asia Pacific, Europe, Middle East &Africa, and South &Central America.

The Asia-Pacific High Performance Foam Market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The market is primarily fueled by rapid industrialization and the presence of major electronics OEMs. China is the leading contributor, supported by its status as the world's largest producer of appliances and vehicles. India is emerging as a high-growth center driven by government initiatives like "Smart Cities" and the expansion of domestic civil aviation and automotive manufacturing.

Growth is further bolstered by a global shift toward specialty polymer foams, such as silicone and polyolefin foams, which offer superior thermal stability and energy absorption. The increasing adoption of electric vehicles (EVs), requiring lightweight battery-pack insulation, and the rapid build-out of cold-chain logistics for pharmaceuticals solidify Asia-Pacific as a central driver for innovation and the future scaling of the high performance foam industry.

Get more information on this report

High Performance Foam Market Research Report Guidance:

The report includes qualitative and quantitative data in the High Performance Foam market across type end use industry, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the High Performance Foam market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the High Performance Foam market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the High Performance Foam market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover High Performance Foam market segments by type, end use industry, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the High Performance Foam market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

High Performance Foam Market News and Key Development:

The High Performance Foam market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the High Performance Foam market are:

In September 2025, DSC®, a global leader in high performance foam innovation, announced the launch of DURAPONTEX® L-TAC, a next-generation foam technology that redefines sustainable footwear manufacturing. Engineered to mold at significantly lower temperatures, L-TAC not only reduces energy usage and carbon emissions per pair, but also expands design freedom for brands by enabling compatibility with a broader range of textiles.

In August 2025, Zotefoams entered into a joint venture with Seoheung Co. Ltd. to support the construction and commissioning of a new high-performance foam manufacturing facility in Vietnam. The collaboration enables Zotefoams to expand beyond traditional foam sheets into 3D foam preforms for athletic footwear applications, leveraging its expertise in supercritical foams and Seoheung's regional manufacturing capabilities. This strategic partnership strengthens Zotefoams' production footprint in Asia and supports the growing demand for advanced, lightweight foam solutions in footwear manufacturing.

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - High Performance Foam Market

Rogers Corporation

JSP Corporation

Evonik Industries

BASF SE

The Dow Chemical Company

Armacell International S.A.

Zotefoams PLC

Trocellan

Sekisui Alveo

SABIC

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Frequently Asked Questions

How big is the High Performance Foam Market?

The High Performance Foam Market is valued at US$ 23.12 Billion in 2025, it is projected to reach US$ 38.5 Billion by 2033.

What is the CAGR for High Performance Foam Market by (2026 - 2033)?

As per our report High Performance Foam Market, the market size is valued at US$ 23.12 Billion in 2025, projecting it to reach US$ 38.5 Billion by 2033. This translates to a CAGR of approximately 6.58% during the forecast period.

What segments are covered in this report?

The High Performance Foam Market report typically cover these key segments-

Type (Polyurethane, Silicone, and Polyolefin)

End Use Industry (Construction, Transportation, Electronics, and Packaging)

What is the historic period, base year, and forecast period taken for High Performance Foam Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the High Performance Foam Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in High Performance Foam Market?

The High Performance Foam Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Rogers Corporation

JSP Corporation

Evonik Industries

BASF SE

The Dow Chemical Company

Armacell International S.A.

Zotefoams PLC

Trocellan

Sekisui Alveo

SABIC

Who should buy this report?

The High Performance Foam Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the High Performance Foam Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For High Performance Foam Market

Get Free Sample For High Performance Foam Market