01

Market Summery

Executive Summary and Global Market Analysis

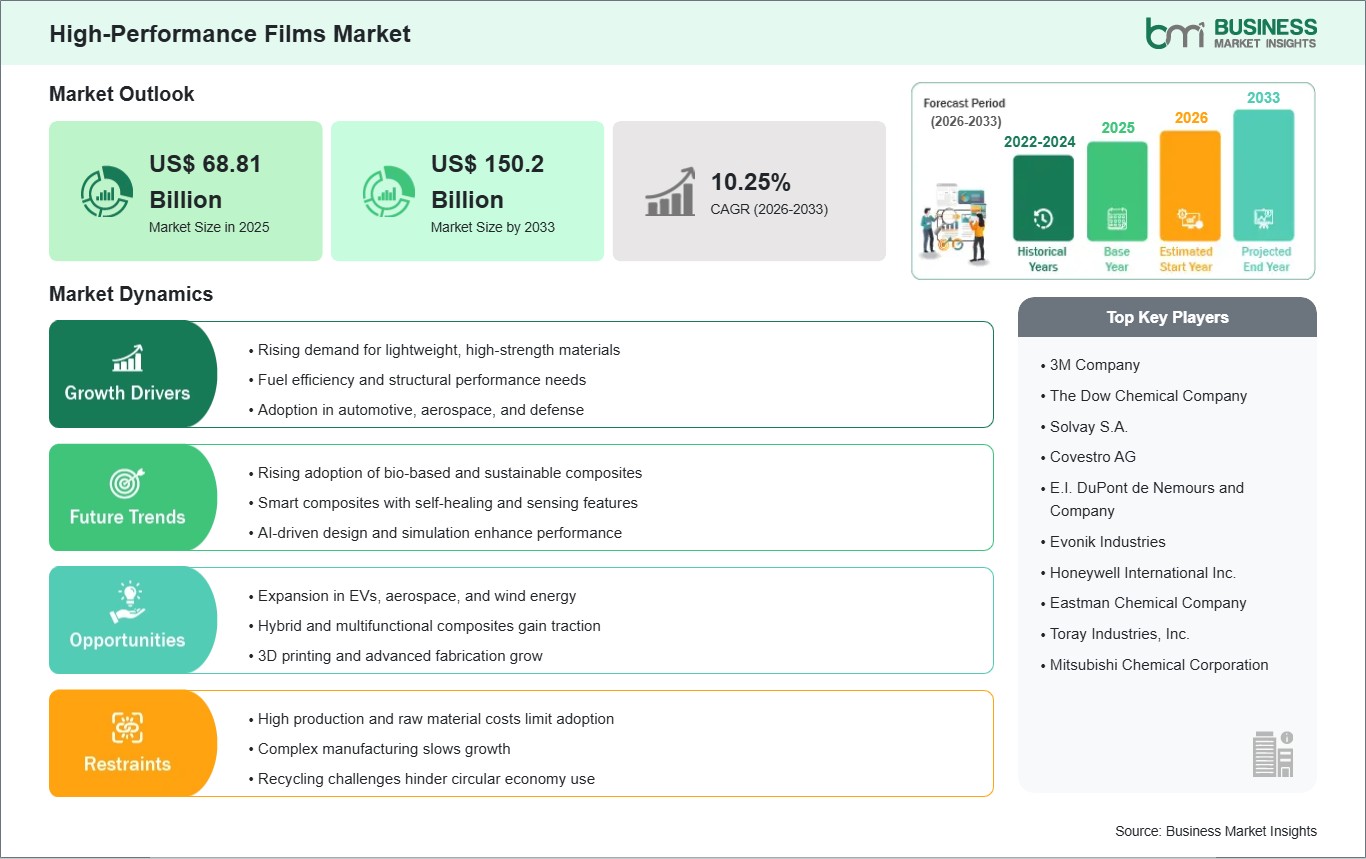

High-performance films (HPFs) are advanced polymer-based materials engineered to provide exceptional mechanical, thermal, and chemical properties that far exceed those of conventional films. These films are indispensable in demanding environments where stability, durability, and resistance to extreme conditions are paramount. They serve as critical components in industries such as electronics, healthcare, automotive, and aerospace, where they facilitate everything from flexible circuitry to high-barrier medical packaging. The primary advantages of high-performance films include superior tensile strength, high dielectric constant, excellent heat resistance, and advanced barrier protection against moisture and gases. Growing industrialization in emerging economies, the rapid transition toward electric mobility, and the rising demand for sophisticated consumer electronics are the primary catalysts for market growth. Furthermore, the integration of Artificial Intelligence (AI) in material science is accelerating the development of customized film properties and enhancing manufacturing efficiency.

However, several challenges can restrain market growth, such as the high cost of specialty resins (e.g., fluoropolymers and polyimides) and the technical complexities involved in high-precision extrusion processes. Stringent environmental regulations and the difficulty of recycling multi-layer film structures also present significant hurdles. Despite these challenges, the market holds significant opportunities driven by the global push for renewable energy, specifically solar photovoltaics, and the expansion of 5G infrastructure. Additionally, the shift toward sustainable and mono-material barrier films presents a substantial avenue for innovation as companies strive to align with circular economy goals.

03

Segment Analysis

High-Performance Films Market Segmentation

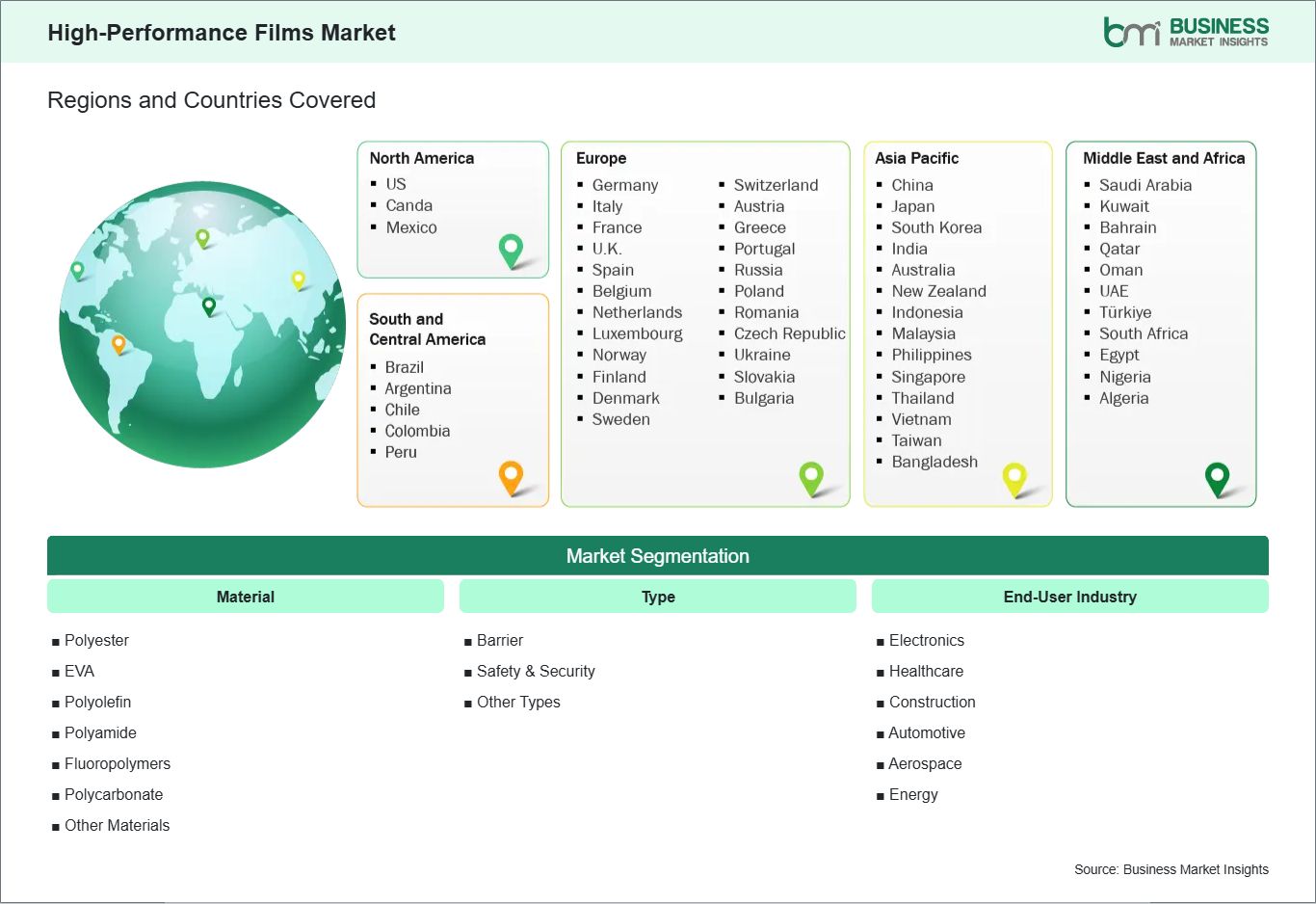

Key segments that contributed to the derivation of the high-performance films market analysis are material, type, and end-user industry.

- By Material, the market is segmented into Polyester, EVA, Polyolefin, Polyamide, Fluoropolymers, Polycarbonate, and Others.

- By Type, the market is divided into Barrier, Safety &Security, and Others.

- By End-User Industry, the market is categorized into Electronics, Healthcare, Construction, Automotive, Aerospace, and Energy.

04

Market Forces

High-Performance Films Market Drivers and Opportunities

Proliferation of 5G Infrastructure and Next-Generation Electronics

The rapid global deployment of 5G and the unending quest to miniaturize electronics are major driving forces behind the growth of the high-performance films industry. This is because, as telecommunications migrate to higher frequencies, there is a dramatically increasing requirement for materials that have very low dielectric loss and are thermally stable. High-performance films, such as Liquid Crystal Polymers and Polyimide, are essential materials used in the fabrication of flexible printed circuits and high-speed connectors necessary in 5G-enabled mobile communications and base stations.

Simultaneously, the consumer electronics market is concurrently shifting to newer form factors, starting from foldable to wearable devices, which demand the fabrication of very flexible substrates that can endure thousands of bending cycles. Furthermore, apart from the telecommunication sector, incorporating smarter technology into all types of appliances, ranging from IoT-enabled home devices to sophisticated biomedical devices, demands films characterized by unique electrical and optical properties. Technologically, the market is constrained to move from the production of commodity films to high-temperature films.

Integration of High-Functionality Films in Sustainable Energy Systems

The global transition toward a low-carbon economy and the surge in electric vehicle (EV) adoption present a transformative opportunity for the high-performance films industry. Renewable energy infrastructure, particularly solar photovoltaics, relies heavily on high-durability films for backsheet protection and encapsulation to shield sensitive solar cells from moisture, UV radiation, and mechanical stress over a 25-year lifespan. As countries accelerate their net-zero targets, the demand for fluoropolymer and EVA-based films in large-scale solar farms is projected to hit record levels.

Furthermore, the electrification of the automotive sector has opened a massive new frontier for film applications. Electric vehicles need specialized high-performance films for insulation of battery cells, thermal management, and lightweight components for enhanced range and safety of passengers. The usage of novel “smart” window films for energy-efficient solar control in buildings is increasing for green building certifications. To satisfy global ESG requirements for companies, investments in bio-resins and recyclable barrier films can tap into the niche market for sustainable developments. The convergence of material innovation and energy change makes high-performance films an indispensable ingredient of future growth.

05

Size and Share Analysis

High-Performance Films Market Size and Share Analysis

The high-performance films market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within material, type, and end-user industry, offering insights into their contribution to overall market performance.

In terms of material, polyester remains a significant segment, due to its excellent balance of cost, clarity, and mechanical strength, making it the preferred choice for both packaging and industrial applications.

Based on type, barriers represent a critical type of segment, widely utilized in the food and pharmaceutical sectors to extend shelf life by preventing the ingress of oxygen and moisture. This segment is benefiting from the rising consumer demand for convenience and packaged goods in emerging markets.

By end-user industry, the automotive subsegment is witnessing rapid growth, driven by the need for lightweight materials and the electrification of vehicles. High-performance films are used extensively in battery insulation and thermal management systems for electric vehicles (EVs).

07

Report Coverage

High-Performance Films Market Report Coverage and Deliverables

The "High-Performance Films Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- High-performance films market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- High-performance films market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- High-performance films market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the high-performance films market.

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

High-Performance Films Market Geographic Insights

The geographical scope of the high-performance films market report is divided into five regions: North America, Asia Pacific, Europe, Middle East &Africa, and South &Central America.

The Asia Pacific region significantly dominates the global landscape. This leadership is fueled by the region's status as a global manufacturing powerhouse, particularly in China, Japan, South Korea, and India. Rapid urbanization and the massive expansion of the electronics and automotive sectors are primary contributors. China remains the single largest consumer, driven by extensive construction projects and its leading role in EV battery production. India is also a key growth engine, with government initiatives like "Make in India" pushing for an electronics manufacturing target.

North America maintains a significant market position, with steady growth anchored by high-specification requirements in the aerospace, defense, and healthcare industries. The United States leads the region, where demand is focused on high-barrier medical packaging and advanced films for semiconductor fabrication. Europe follows closely, with a strong emphasis on sustainability and circular economy regulations. European manufacturers are at the forefront of developing recyclable mono-material films to comply with strict EU plastic waste directives. Meanwhile, the Middle East &Africa and South &Central America are emerging as high-potential markets due to increasing investments in infrastructure, solar energy projects, and a rising demand for packaged consumer goods.

10

Industry Activity

Recent Developments

The High-Performance Films market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the high-performance films market are:

- In December 2025, Cosmo Films announced the expansion of its flexible packaging portfolio with a new range of BOPP, CPP, and BOPET-based films engineered specifically for pet food packaging. The introduction includes a new high-heat-resistant TR-BOPP film along with advanced barrier and lidding films, strengthening the company's commitment to delivering next-generation, food-safe packaging solutions.

- In December 2025, BASF, San Fang Chemical Industrial Co., Ltd., and Nichetech Advanced Materials Co., Ltd. signed a Memorandum of Understanding (MoU) to jointly develop sustainable solutions for the footwear industry, with a focus on thermoplastic polyurethane (TPU) products and a shared ambition to achieve net-zero carbon emissions by 2050. The first milestone of this collaboration will be the introduction of Global Recycled Standard (GRS)-certified TPU films, combining high performance with environmental responsibility. These films will enable footwear brands to incorporate recycled materials without compromising quality or durability.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations