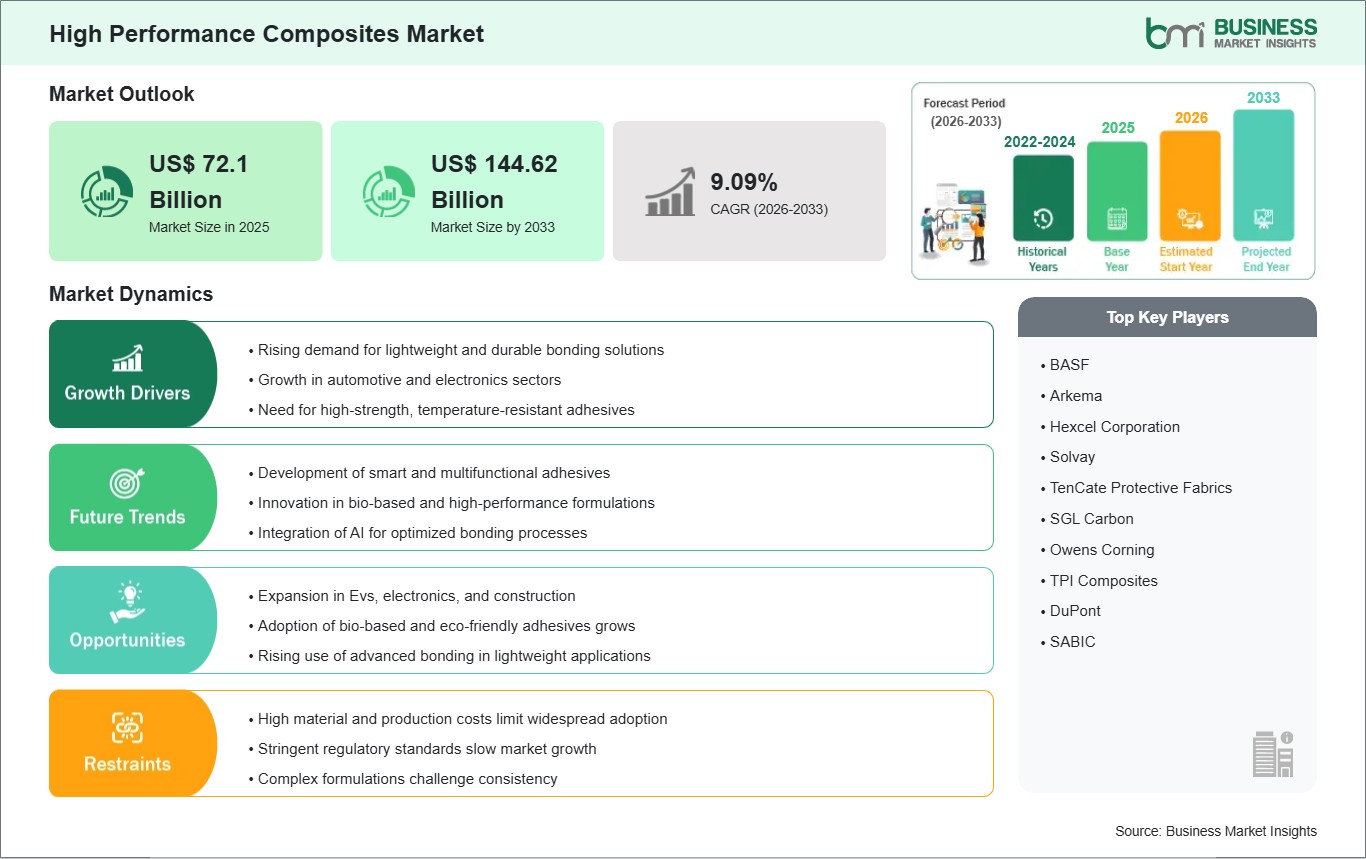

The High Performance Composites Market size is expected to reach US$ 144.62 Billion by 2033 from US$ 72.1 Billion in 2025. The market is estimated to record a CAGR of 9.09% from 2026 to 2033.

Executive Summary and Global Market Analysis:

High-performance composites are advanced material systems engineered by combining high-strength reinforcing fibers, such as carbon, aramid, or S-glass, with a high-performance polymer matrix (thermoset or thermoplastic). These technologies deliver significant clinical and economic value by enabling the production of fuel-efficient aircraft such as the Boeing 787, offering high-strength solutions for massive offshore wind turbine blades, and ensuring the structural integrity of high-pressure hydrogen storage tanks. Together, they form a critical portfolio that supports high-quality performance outcomes across the aerospace, automotive, renewable energy, and defense sectors. Market expansion is primarily attributed to the rising global demand for lightweighting to extend EV battery range, the rapid acceleration of commercial aircraft production post-pandemic, and the shift toward sustainable energy infrastructure. Furthermore, the integration of Automated Fiber Placement (AFP) and 3D printing of composites, which reduce material waste and cycle times, is substantially improving procedural efficiency.

However, several challenges can restrain market growth: high initial procurement and production costs, particularly for high-modulus carbon fibers and expensive autoclave processing, can limit adoption in price-sensitive consumer segments. Stringent regulatory hurdles and the technical difficulty of recycling thermoset composites, which are hard to break down at end-of-life, lengthen the time-to-market for sustainable variations and increase environmental overhead. Additionally, the industry faces constraints due to long manufacturing cycle times and a persistent shortage of specialized composite engineers capable of designing for non-isotropic material properties, which can result in sub-optimal design and slower innovation cycles.

Despite these hurdles, the market holds immense opportunities in the universal mandate for decarbonized transportation and the accelerating deployment of thermoplastic composites, which offer faster processing and easier recyclability. The expansion of bio-based resins and natural fiber reinforcements for interior automotive parts and the development of AI-driven material optimization, where machine learning predicts structural failures before they occur, are expected to create significant opportunities for market growth.

High Performance Composites Market - Strategic Insights:

Get more information on this report

High Performance Composites Market Segmentation Analysis:

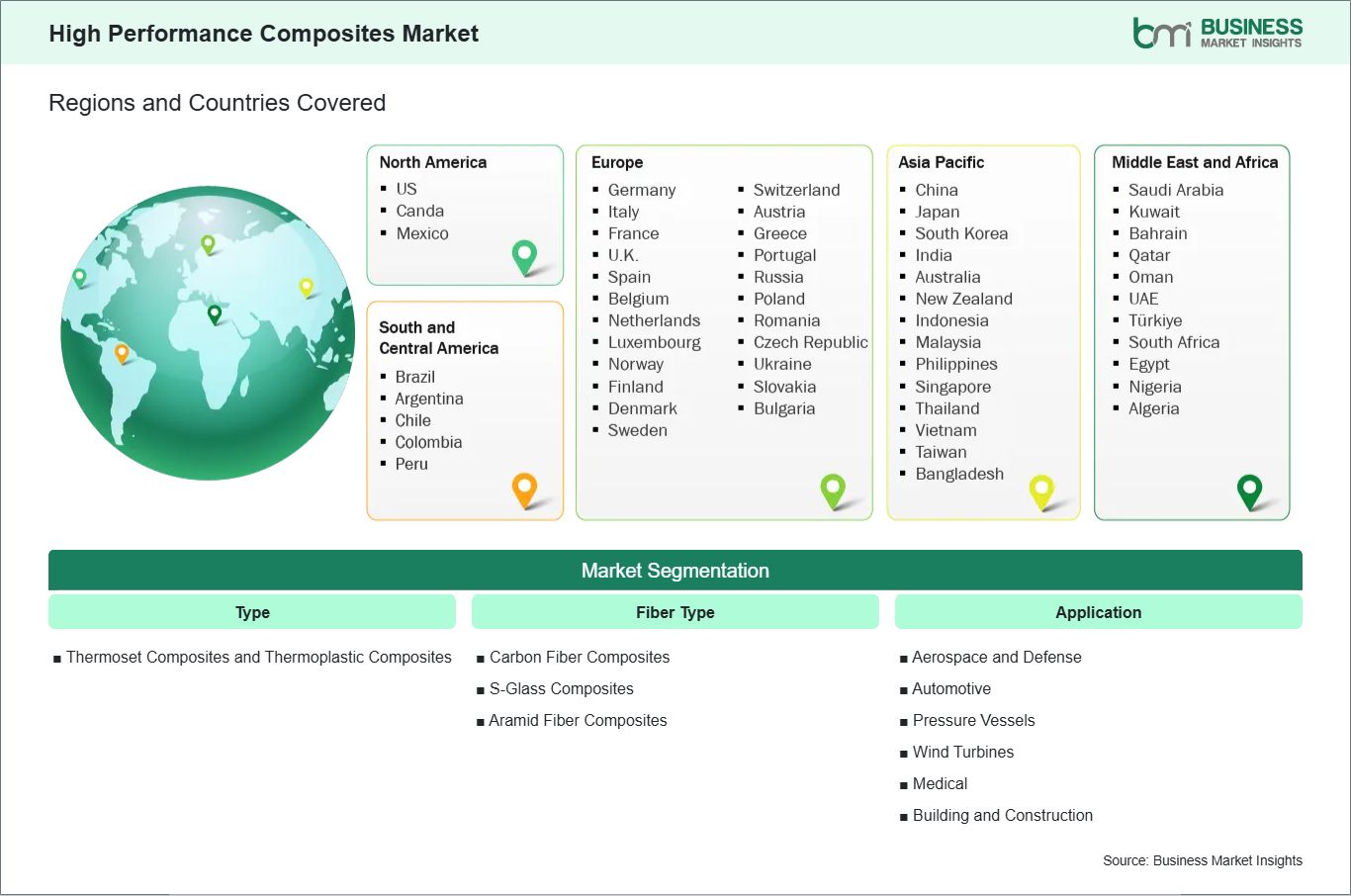

Key segments that contributed to the derivation of the High Performance Composites market analysis are type, fiber type, and application.

By Type, the market is segmented into Thermoset Composites and Thermoplastic Composites.

By Fiber Type, the market is divided into Carbon Fiber Composites, S-Glass Composites, and Aramid Fiber Composites.

By Application, the market is categorized into Aerospace and Defense, Automotive, Pressure Vessels, Wind Turbines, Medical, and Building and Construction.

High Performance Composites Market Drivers and Opportunities:

Aerospace Fleet Renewal and the Electric Mobility Mandate

The primary driver for the High-Performance Composites Market is the intensifying requirement for structural lightweighting within the aerospace and automotive sectors. In the commercial aviation industry, the transition toward next-generation aircraft, such as the Boeing 787 and Airbus A350, which utilize nearly 50% composite content, is driven by the urgent need to reduce fuel consumption and carbon emissions. This biological pressure is mirrored in the automotive sector, where the accelerating shift toward electric vehicles (EVs) has made "mass decompression" a critical engineering priority. Reducing vehicle weight is essential for extending battery range and offsetting the significant mass of heavy battery packs.

Consequently, there is a surging demand for carbon fiber reinforced polymers (CFRP) and thermoplastic composites for structural components, battery enclosures, and chassis reinforcements. Furthermore, the global expansion of offshore wind energy, requiring larger, stiffer, and more corrosion-resistant turbine blades, acts as a non-discretionary driver, ensuring a high-velocity growth path for the market as industries strive to meet stringent decarbonization targets.

Hydrogen Economy and Recyclable Thermoplastic Innovation

A significant high-value opportunity lies in the rapid development of the hydrogen economy and the associated demand for Type IV and Type V pressure vessels. High-performance carbon fiber composites are the only materials capable of providing the necessary strength-to-weight ratio for the high-pressure storage tanks required in hydrogen-powered trucks, buses, and aircraft. There is also a major growth frontier in the transition toward recyclable thermoplastic composites and vitrimers. Unlike traditional thermosets, these next-generation resins can be re-melted and reshaped, addressing the industry's critical challenge of end-of-life composite waste and aligning with circular economy mandates.

Additionally, the rise of automated fiber placement (AFP) and 3D printing of composites presents an opportunity to decentralize manufacturing and reduce the high labor costs and waste associated with manual layup. Manufacturers who focus on multifunctional composites, integrating sensing capabilities directly into the material for real-time structural health monitoring, are positioned to lead in the evolving smart infrastructure and advanced urban air mobility segments.

High Performance Composites Market Size and Share Analysis:

The High Performance Composites market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within type, fiber type, and application, offering insights into their contribution to overall market performance.

Based on type, the Thermoset Composites subsegment holds a significant market share. Thermoset resins are indispensable for Aerospace and Defense subsegment primary structures, such as wings and fuselages, due to their exceptional thermal stability and fatigue resistance. A notable trend in 2026 is the adoption of "Out-of-Autoclave" (OoA) curing processes, which allow for the production of large-scale parts without the capacity constraints of traditional pressurized ovens. These innovations are particularly vital in high-stakes environments where structural integrity is non-negotiable, ensuring that next-generation aircraft such as the Boeing 777X can meet rigorous safety certifications while achieving maximum fuel efficiency.

High Performance Composites Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

BASF

Arkema

Hexcel Corporation

Solvay

TenCate Protective Fabrics

SGL Carbon

Owens Corning

TPI Composites

DuPont

SABIC

Get more information on this report

High Performance Composites Market Report Coverage and Deliverables:

The "High Performance Composites Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

High Performance Composites market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

High Performance Composites market trends, as well as market dynamics such as drivers, restraints, and key opportunities

High Performance Composites market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the High Performance Composites market

Detailed company profiles, including SWOT analysis

High Performance Composites Market Geographic Insights:

The geographical scope of the High Performance Composites market report is divided into five regions: North America, Asia Pacific, Europe, Middle East &Africa, and South &Central America.

The Asia-Pacific High Performance Composites Market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The market is primarily propelled by the region's aggressive adoption of lightweight materials in transportation and renewable energy. China is a significant contributor, with its demand estimated to reach 3 million tons in the coming years. Japan and South Korea remain technological leaders, particularly in high-grade carbon fiber production for the global supply chain.

Growth is further bolstered by the global transition toward sustainable energy, where high-performance composites are essential for manufacturing large-scale wind turbine blades that exceed 100 meters in length. The rising demand for EV battery enclosures and the integration of thermoplastic composites, which offer faster processing cycles and recyclability, solidify Asia-Pacific as the central hub for innovation and volume growth in the high performance composites industry.

Get more information on this report

High Performance Composites Market Research Report Guidance:

The report includes qualitative and quantitative data in the High Performance Composites market across type, fiber type, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the High Performance Composites market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the High Performance Composites market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the High Performance Composites market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover High Performance Composites market segments by type, fiber type, application, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the High Performance Composites market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

High Performance Composites Market News and Key Development:

The High Performance Composites market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the High Performance Composites market are:

In January 2026, Karman Space &Defense Acquired Seemann Composites and Material Sciences. The acquisition enhances Karman's IP portfolio, production capabilities, and access to multi-decade U.S. Navy programs, supporting next-generation propulsion, shielding, and strategic defense applications. This strategic move represents a significant positive development for the high-performance composites

In January 2025, ARRIS®Composites, an advanced manufacturer with a breakthrough technology enabling the highest-performing fiber-reinforced composites at scale, announced a strategic technology partnership with Henry Repeating Arms to develop lightweight, high-strength firearm components using advanced fiber-reinforced composites. This collaboration highlights the expanding application of high-performance composites and showcases innovation in material science and additive manufacturing technologies.

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - High Performance Composites Market

BASF

Arkema

Hexcel Corporation

Solvay

TenCate Protective Fabrics

SGL Carbon

Owens Corning

TPI Composites

DuPont

SABIC

Frequently Asked Questions

How big is the High Performance Composites Market?

The High Performance Composites Market is valued at US$ 72.1 Billion in 2025, it is projected to reach US$ 144.62 Billion by 2033.

What is the CAGR for High Performance Composites Market by (2026 - 2033)?

As per our report High Performance Composites Market, the market size is valued at US$ 72.1 Billion in 2025, projecting it to reach US$ 144.62 Billion by 2033. This translates to a CAGR of approximately 9.09% during the forecast period.

What segments are covered in this report?

The High Performance Composites Market report typically cover these key segments-

Type (Thermoset Composites, and Thermoplastic Composites)

Fiber Type (Carbon Fiber Composites, S-Glass Composites, and Aramid Fiber Composites)

Application (Aerospace and Defense, Automotive, Pressure Vessels, Wind Turbines, Medical, and Building and Construction)

What is the historic period, base year, and forecast period taken for High Performance Composites Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the High Performance Composites Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in High Performance Composites Market?

The High Performance Composites Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

BASF

Arkema

Hexcel Corporation

Solvay

TenCate Protective Fabrics

SGL Carbon

Owens Corning

TPI Composites

DuPont

SABIC

Who should buy this report?

The High Performance Composites Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the High Performance Composites Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For High Performance Composites Market

Get Free Sample For High Performance Composites Market