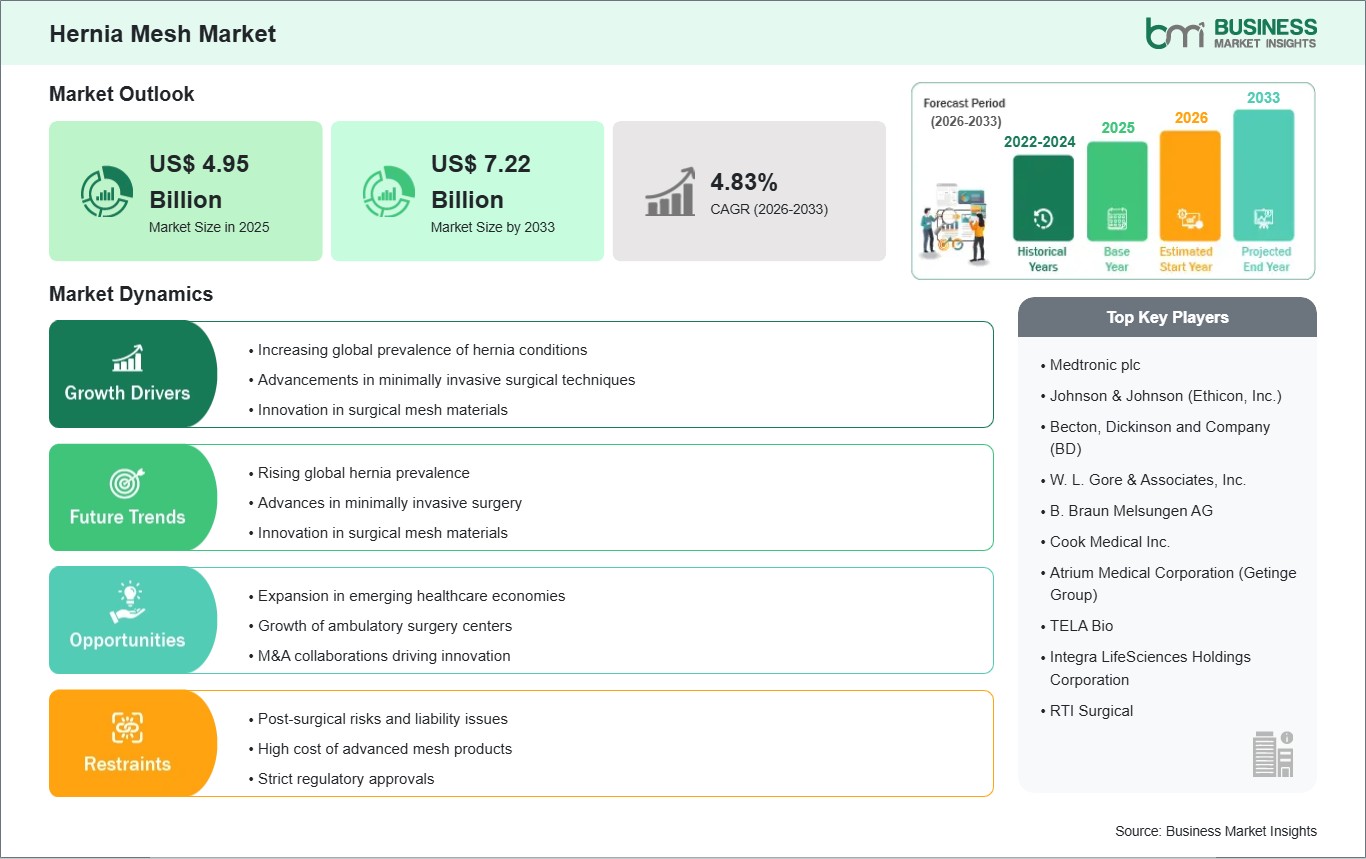

The Hernia Mesh Market size is expected to reach US$ 7.22 Billion by 2033 from US$ 4.95 Billion in 2025. The market is estimated to record a CAGR of 4.83% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global market for hernia mesh devices is seeing healthy growth due to several factors such as an increasing number of people with hernias, obesity rates rising and an aging population. Many of the newest products on the market are based on laparoscopic (minimally-invasive) surgery to repair hernias and create new types of mesh products for hernia repair surgeries. The majority of hernia meshes sold today are synthetic-based because they are less expensive than biologic & composite meshes and have been shown to have the best clinical success rates to date however both the biologic & composite meshes are being used in higher-risk/complex hernia cases, thus lowering the rate of complications associated with surgery and increasing patient safety. Many of the advancements in technology such as lightweight meshes, anti-adhesion coatings and 3D-printed mesh specifically created for individual patients are also contributing to the overall growth of the hernia mesh market in the future.

The largest region for sales of hernia meshes currently is North America, primarily due to the strong presence of large healthcare systems that support widespread use of mini-invasive surgery followed closely by Europe and Asia Pacific where there is also a growing healthcare spending and increased surgical activity that presents opportunities for growth. Additionally, the growth of outpatient surgery centers, new entrants into the global marketplace and collaborating partnerships between manufacturers will continue to fuel demand and innovation that will drive competitive differentiation in the global hernia mesh devices marketplace going forward.

Hernia Mesh Market - Strategic Insights:

Get more information on this report

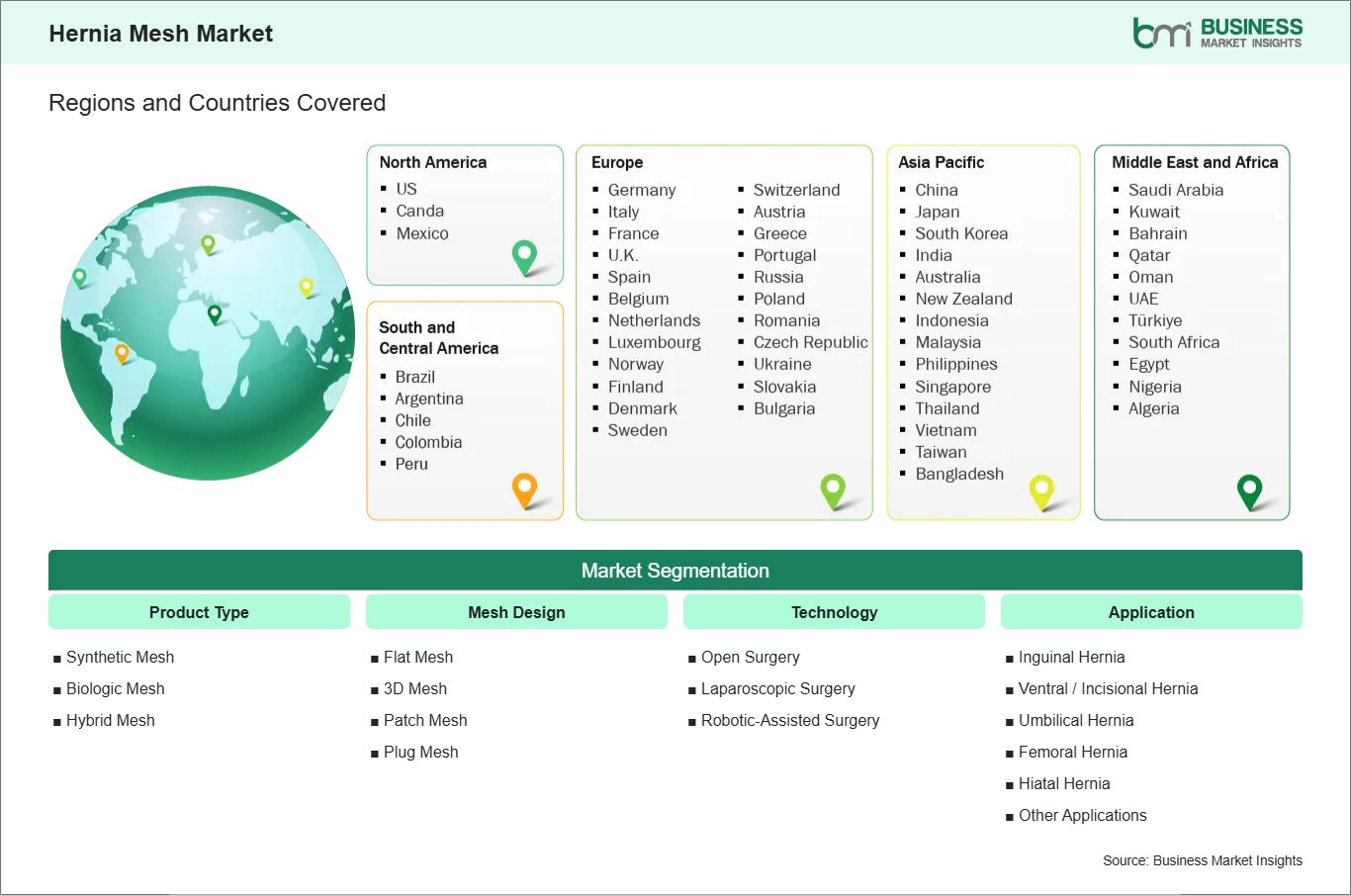

Hernia Mesh Market Segmentation Analysis:

Key segments that contributed to the derivation of the Hernia Mesh market analysis are product type, mesh design, technology, application, and end user.

By product type, the hernia mesh market is segmented into synthetic mesh, biologic mesh, hybrid mesh. The synthetic mesh segment dominated the market in 2025.

By mesh design, the market is segmented into flat mesh, 3D mesh, patch mesh, plug mesh. The flat mesh segment held the largest share of the market in 2025.

By technology, the market is segmented into open surgery, laparoscopic surgery, robotic‑assisted surgery. The laparoscopic surgery segment held the largest share of the market in 2025.

By application, the market is segmented into inguinal hernia, ventral / incisional hernia, umbilical hernia, femoral hernia, hiatal hernia, others. The inguinal hernia segment held the largest share of the market in 2025.

By end user, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics, and others. The hospitals segment held the largest share of the market in 2025.

Hernia Mesh Market Drivers and Opportunities:

Rising Prevalence of Hernia and Increasing Surgical Volume

The hernia mesh devices market is primarily driven by the increasing number of hernia cases worldwide, resulting in an ongoing rise in surgical repair volume.4 In addition to being associated with population aging, obesity, physically demanding lifestyles, and post-operative complications, each of these factors also contributes to the occurrence of inguinal, ventral, umbilical, and incisional hernias. Since worldwide life expectancy continues to increase and the population aged 65 and older will continue to grow, there will be an increasing number of people who are most susceptible to recurrences and weak rectus abdominis walls, which leads to an increase in the volume of surgeries performed. As well, obesity is an important global health issue and contributes to an increase in intra-abdominal pressure, thereby increasing hernia risk. The latest clinical guidelines recommend mesh versus suture-only repairs as they provide lower recurrence rate and better long-term outcomes. These findings establish a consistent market for mesh products. The continued use of laparoscopic and robotic-assisted minimal invasive surgical techniques would also contribute to the growing use of mesh since these techniques require the use of specific mesh implants. Finally, adequate diagnosis rates, improved patient awareness and access to health care in developing countries contribute to the increased volume of surgical interventions for hernias. Demographic, clinical and technological factors collectively will provide a sustained demand for hernia mesh devices as an integral part of the standard treatment for hernia repair worldwide.

Expansion in Emerging Markets and Ambulatory Surgical Centers

The hernia mesh device market is being driven by the rapid growth of healthcare infrastructure in developing countries and an increase in the use of ambulatory surgical centers (ASCs). Countries in Asia Pacific, Latin America, the Middle East and parts of Africa are investing heavily in the construction of hospitals, increasing surgical capacity and providing health insurance coverage. As a result, the number of elective and necessary surgeries, such as hernia repairs will increase. These developments, along with rising disposable income levels, urbanization and growing public awareness of health issues, will lead to more hernia repairs being performed in these nations. At the same time, the worldwide shift toward lower-cost healthcare delivery systems has fuelled new ASCs that perform many hernia repairs on an outpatient basis, thus creating demand for easy-to-handle, ready-to-use and inexpensive mesh products appropriate for high-volume surgery due to the cost-effectiveness and improved efficiency of practice at the ASC. Manufacturers that develop innovative yet affordable mesh solutions or establish strong distribution networks within the emerging markets are likely to achieve substantial competitive advantage. Establishing strategic partnerships, manufacturing locally and conforming to regulations within the emerging regions will further enhance long-term growth opportunities for industry participants.

Hernia Mesh Market Size and Share Analysis:

By product type, the hernia mesh market is segmented into synthetic mesh, biologic mesh, hybrid mesh. The synthetic mesh segment dominated the market in 2025. The growth is attributed to cost-effectiveness, strong clinical outcomes, and lower recurrence rates compared to suture repair.

By mesh design, the market is segmented into flat mesh, 3D mesh, patch mesh, plug mesh. The flat mesh segment held the largest share of the market in 2025. The segment offers wide applicability, ease of placement, and suitability for both open and laparoscopic procedures.

By technology, the hernia mesh market is segmented into open surgery, laparoscopic surgery, robotic‑assisted surgery. The laparoscopic surgery segment dominated the market in 2025. The growth is growing preference for minimally invasive procedures with faster recovery and reduced complications.

By application, the market is segmented into inguinal hernia, ventral / incisional hernia, umbilical hernia, femoral hernia, hiatal hernia, others. The inguinal hernia segment held the largest share of the market in 2025 owing to high global prevalence and frequent surgical intervention rates.

By end user, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics, and others. The hospitals segment held the largest share of the market in 2025. The segment growth is attributed to higher surgical volumes, advanced infrastructure, and availability of skilled surgeons and robotic systems.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Medtronic plc

Johnson & Johnson (Ethicon, Inc.)

Becton, Dickinson and Company (BD)

W. L. Gore & Associates, Inc.

B. Braun Melsungen AG

Cook Medical Inc.

Atrium Medical Corporation (Getinge Group)

TELA Bio

Integra LifeSciences Holdings Corporation

RTI Surgical

Get more information on this report

Hernia Mesh Market Report Coverage and Deliverables:

The "Hernia Mesh Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Hernia Mesh market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Hernia Mesh market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Hernia Mesh market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Hernia Mesh market

Detailed company profiles, including SWOT analysis

Hernia Mesh Market Geographic Insights:

The geographical scope of the Hernia Mesh market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Hernia Mesh market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific Hernia Mesh market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. Demand for Asia Pacific hernia mesh devices is being driven by improvements in healthcare infrastructure, increased surgical volumes and enhanced awareness of innovative treatments. Rapid urbanisation and increasing disposable earnings will improve elective and minimally invasive surgery access across China, India, Japan, South Korea and Australia and consequently increase the number of surgeries performed (hernia repairs), due to greater population growth among an elderly population and an increasing number of patients with inguinal and ventral hernias (hernias of the groin and lower abdomen). Increased levels of obesity and risk factors associated with lifestyle-related obesity are also contributing to the increase in surgeries performed on these types of patients. In addition, governments are investing heavily in modernising hospitals and enhancing public dental health care systems and programs supporting these surgical procedures in urban and sub-urban areas both within and outside their own country.

The increasing number of multinational medical device companies and strong domestic manufacturers who are able to compete on price are also providing an opportunity to increase penetration in Asia Pacific's hernia markets. While price sensitivity in developing markets will impact sales in these countries, demand for synthetic mesh products remains strong as prices are affordable throughout Asia Pacific; however, composite and biologic mesh products will gradually be adopted by higher levels of healthcare providers. The increase in ambulatory surgical centres and private specialty clinics has also contributed to the continued development of the hernia market in Asia Pacific. On balance, the Asia Pacific hernia market continues to provide the highest growth rates in the world due to their relatively large population, healthcare growth and growth in use of modern surgical technology.

Get more information on this report

Hernia Mesh Market Research Report Guidance:

The report includes qualitative and quantitative data in the Hernia Mesh market across product type, mesh design, technology, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Hernia Mesh market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Hernia Mesh market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Hernia Mesh market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Hernia Mesh market segments by product type, mesh design, technology, application, end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Hernia Mesh market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Hernia Mesh Market News and Key Development:

The Hernia Mesh market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the hernia mesh market are:

In June 2025, TELA Bio, Inc. had the European launch of OviTex Inguinal Reinforced Tissue Matrix, the only reinforced tissue matrix specifically engineered for laparoscopic and robotic-assisted inguinal hernia repair.

In April 2025, BD received 510(k) clearance from the US Food and Drug Administration (FDA) and the commercial launch of Phasix ST Umbilical Hernia Patch, the first and only fully absorbable hernia patch on the market designed specifically for umbilical hernias.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Hernia Mesh Market?

The Hernia Mesh Market is valued at US$ 4.95 Billion in 2025, it is projected to reach US$ 7.22 Billion by 2033.

What is the CAGR for Hernia Mesh Market by (2026 - 2033)?

As per our report Hernia Mesh Market, the market size is valued at US$ 4.95 Billion in 2025, projecting it to reach US$ 7.22 Billion by 2033. This translates to a CAGR of approximately 4.83% during the forecast period.

What segments are covered in this report?

The Hernia Mesh Market report typically cover these key segments-

Product Type (Synthetic Mesh, Biologic Mesh, Hybrid Mesh)

Mesh Design (Flat Mesh, 3D Mesh, Patch Mesh, Plug Mesh)

What is the historic period, base year, and forecast period taken for Hernia Mesh Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Hernia Mesh Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Hernia Mesh Market?

The Hernia Mesh Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medtronic plc

Johnson & Johnson (Ethicon, Inc.)

Becton, Dickinson and Company (BD)

W. L. Gore & Associates, Inc.

B. Braun Melsungen AG

Cook Medical Inc.

Atrium Medical Corporation (Getinge Group)

TELA Bio

Integra LifeSciences Holdings Corporation

RTI Surgical

Who should buy this report?

The Hernia Mesh Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Hernia Mesh Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Hernia Mesh Market

Get Free Sample For Hernia Mesh Market