01

Market Summery

Executive Summary and Global Market Analysis

Headlight Control Module (HCM) refers to an advanced automotive electronic system responsible for managing and regulating vehicle headlight functions, including adaptive lighting, beam leveling, automatic high beam control, daytime running lights (DRL), cornering lights, and intelligent illumination adjustments based on driving conditions. These modules integrate sensors, electronic control units (ECUs), and software-driven lighting algorithms to optimize road visibility, improve driver safety, and enhance energy efficiency. Modern headlight control modules increasingly leverage adaptive front-lighting systems (AFS), matrix LED technologies, laser lighting, and AI-enabled lighting intelligence to dynamically respond to vehicle speed, steering angle, weather conditions, and surrounding traffic environments. The growing integration of Advanced Driver Assistance Systems (ADAS), rising demand for premium vehicle lighting technologies, and increasingly stringent automotive safety regulations are significantly driving market expansion. Additionally, the rapid adoption of LED and adaptive lighting systems in passenger and commercial vehicles is accelerating the deployment of intelligent headlight control modules across global automotive platforms.

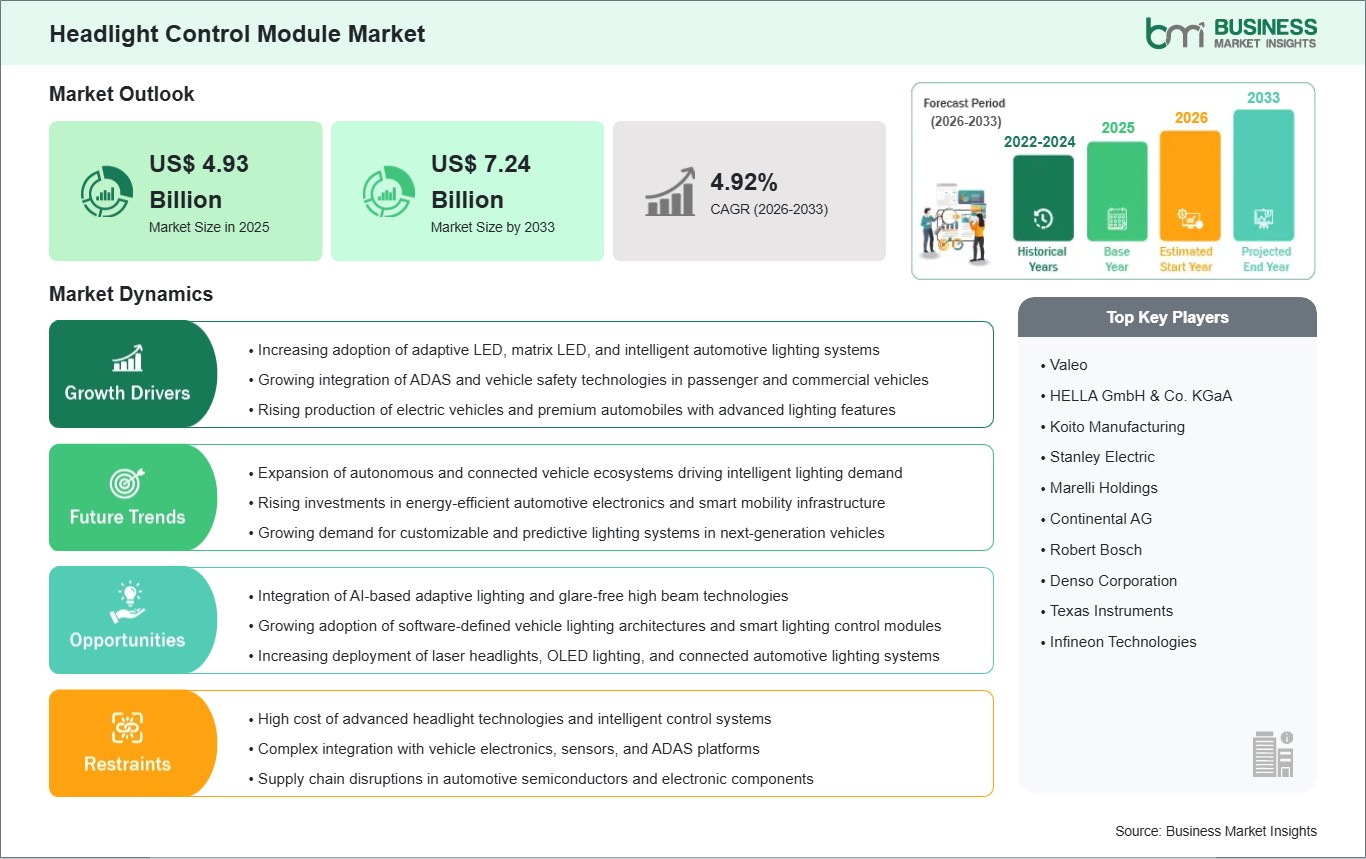

However, several factors may restrain market growth. The high cost associated with advanced lighting technologies such as matrix LED, laser headlights, and adaptive lighting systems remains a significant challenge, particularly in entry-level and cost-sensitive vehicle segments. Integration complexities with vehicle electronic architectures, ADAS platforms, and sensor networks further increase development and implementation costs for automotive manufacturers. The market also faces technical challenges related to software calibration, thermal management, and system reliability under diverse environmental and driving conditions. In addition, varying automotive lighting regulations across different countries create compliance complexities for OEMs operating globally. Supply chain disruptions in automotive semiconductor and electronic component manufacturing may also impact production timelines and increase overall system costs. Furthermore, cybersecurity concerns related to connected vehicle electronics and intelligent lighting communication systems are emerging as an additional challenge for next-generation automotive lighting platforms.

Despite these challenges, the long-term outlook for the headlight control module market remains highly favorable as the automotive industry transitions toward intelligent, connected, and autonomous mobility ecosystems. Significant opportunities are emerging through the integration of AI-powered adaptive lighting, vehicle-to-vehicle (V2V) communication, and sensor fusion technologies capable of delivering highly responsive and predictive illumination control. The increasing adoption of electric vehicles (EVs) and autonomous driving technologies is creating strong demand for energy-efficient and software-defined lighting systems that improve both safety and vehicle aesthetics. Furthermore, advancements in matrix LED, OLED, and laser headlight technologies are enabling highly customizable lighting patterns, glare-free high beams, and enhanced nighttime visibility. The expansion of smart mobility infrastructure and connected transportation ecosystems is also supporting the development of intelligent lighting systems capable of interacting with road environments and traffic management systems in real time. Collectively, these technological advancements and increasing consumer demand for premium automotive safety features are positioning the headlight control module market for sustained long-term growth as a critical component of next-generation automotive electronics and intelligent vehicle architectures..

03

Segment Analysis

Headlight Control Module Market Segmentation

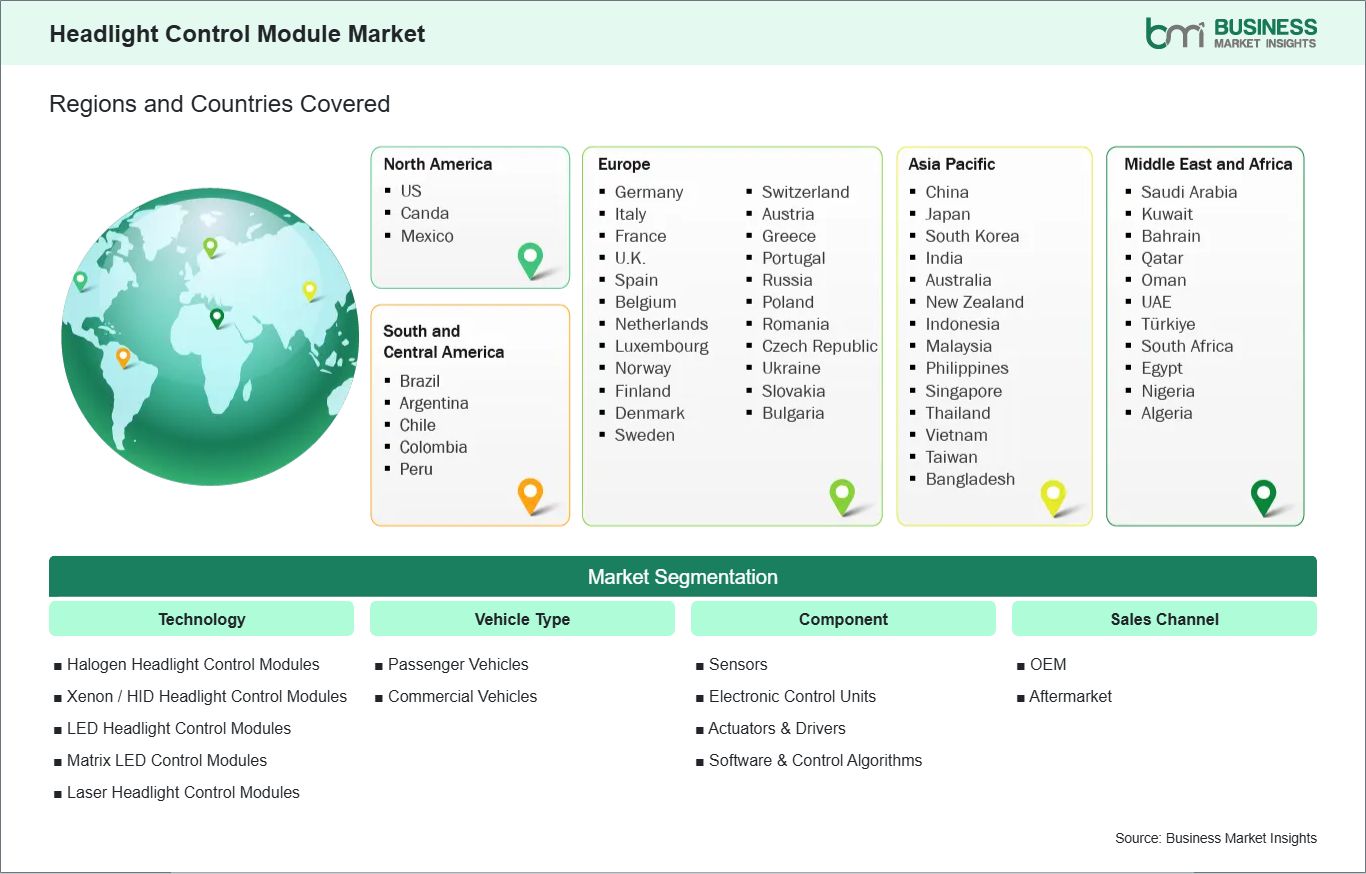

The headlight control module market is segmented based on technology, vehicle type, component, sales channel, and application, reflecting the increasing integration of intelligent lighting systems, adaptive illumination technologies, and advanced automotive electronics across modern vehicles.

By Technology

- Halogen Headlight Control Modules: Includes conventional lighting control systems used for managing halogen headlamp operations in cost-sensitive vehicle segments

- Xenon / HID Headlight Control Modules: Covers modules designed for high-intensity discharge lighting systems offering improved brightness and energy efficiency

- LED Headlight Control Modules: Includes intelligent controllers for LED-based lighting systems enabling adaptive lighting, energy optimization, and enhanced durability

- Matrix LED Control Modules: Supports advanced matrix beam management systems capable of selective light distribution and glare-free high beam functionality

- Laser Headlight Control Modules: Covers high-performance lighting control systems designed for laser-based automotive headlamp technologies with extended illumination range

By Vehicle Type

- Passenger Vehicles: Includes sedans, hatchbacks, SUVs, and luxury vehicles increasingly equipped with adaptive and intelligent lighting systems

- Commercial Vehicles: Covers trucks, buses, and fleet vehicles adopting advanced headlight control systems for improved nighttime visibility and operational safety

By Component

- Sensors: Includes ambient light sensors, steering angle sensors, vehicle speed sensors, and camera systems supporting adaptive lighting functionality

- Electronic Control Units (ECUs): Covers processing units responsible for lighting control logic, beam adjustment, and communication with vehicle systems

- Actuators & Drivers: Includes motorized beam leveling systems, LED drivers, and adaptive lighting actuators controlling headlamp positioning and intensity

- Software & Control Algorithms: Covers embedded software, AI-based lighting intelligence, and adaptive illumination control platforms

By Sales Channel

- OEM (Original Equipment Manufacturer): Includes factory-installed headlight control modules integrated into new vehicles by automotive manufacturers

- Aftermarket: Covers replacement and upgrade headlight control modules sold through automotive parts distributors and service providers

By Application

- Adaptive Front Lighting System (AFS): Enables dynamic headlight adjustment based on steering direction, vehicle speed, and road conditions

- Automatic High Beam Control: Automatically switches between high and low beams to improve visibility and reduce glare for oncoming traffic

- Daytime Running Lights (DRL): Supports automatic daytime illumination systems for improved vehicle visibility and compliance with safety regulations

- Cornering Light Control: Provides additional illumination during turns and cornering maneuvers to enhance nighttime driving safety

- Intelligent Lighting & Beam Leveling: Includes automatic beam alignment, glare reduction, and real-time illumination optimization technologies

04

Market Forces

Headlight Control Module Market Drivers and Opportunities

Rising Adoption of Advanced Automotive Lighting Systems, Vehicle Safety Regulations, and ADAS Integration

The Headlight Control Module Market is being driven by the increasing adoption of advanced automotive lighting technologies, growing integration of Advanced Driver Assistance Systems (ADAS), and stringent global vehicle safety regulations aimed at improving nighttime driving visibility and road safety. Modern headlight control modules enable intelligent management of adaptive front-lighting systems, automatic high beam control, beam leveling, daytime running lights (DRL), and cornering illumination functions through integrated sensors, ECUs, and software-driven control algorithms. Unlike conventional lighting systems, advanced headlight control modules dynamically adjust lighting intensity, beam direction, and illumination patterns based on vehicle speed, steering angle, weather conditions, and surrounding traffic environments. The growing penetration of LED, matrix LED, and laser headlight technologies in passenger and commercial vehicles is significantly accelerating demand for intelligent lighting control systems. Additionally, rising consumer preference for premium vehicle features, enhanced driving comfort, and improved road visibility is further supporting market expansion.

The increasing production of electric vehicles (EVs), luxury vehicles, and semi-autonomous vehicles is also driving adoption of sophisticated headlight control modules capable of supporting energy-efficient and software-defined lighting architectures. Automotive manufacturers are increasingly integrating adaptive lighting systems into vehicle safety platforms to comply with evolving road safety standards and improve NCAP safety ratings. Furthermore, advancements in automotive electronics, sensor technologies, and embedded control systems are enabling more compact, responsive, and energy-efficient headlight control modules. Collectively, these factors are contributing to sustained market growth as intelligent automotive lighting becomes an essential component of next-generation vehicle safety and driving assistance ecosystems.

Growing Integration of AI-Based Lighting Intelligence, Smart Mobility, and Autonomous Driving Platforms

Opportunities in the Headlight Control Module Market are expanding through the integration of artificial intelligence, sensor fusion technologies, and connected vehicle ecosystems capable of delivering highly adaptive and predictive automotive lighting functions. AI-powered lighting control systems are enabling advanced capabilities such as real-time glare-free high beam adjustment, predictive road illumination, traffic-responsive beam distribution, and environment-aware lighting optimization. The increasing development of autonomous and semi-autonomous vehicles is creating strong demand for intelligent headlight systems that can interact dynamically with vehicle sensors, cameras, radar systems, and navigation platforms to enhance driving safety and situational awareness.

05

Size and Share Analysis

Headlight Control Module Market Size and Share Analysis

The Headlight Control Module Market is projected to grow from US$ 4.93 Billion in 2025 to US$ 7.24 Billion by 2033 , registering a CAGR of 4.92% from 2026 to 2033.

By technology, LED headlight control modules account for a significant share due to the rapid adoption of LED lighting systems in passenger and commercial vehicles driven by their superior energy efficiency, longer lifespan, and advanced adaptive lighting capabilities. Matrix LED control modules are witnessing strong growth as automotive manufacturers increasingly integrate glare-free high beam systems and intelligent beam distribution technologies into premium and luxury vehicles. Xenon / HID headlight control modules continue to maintain steady demand in mid-range vehicle segments where enhanced brightness and visibility remain important. Laser headlight control modules are also gaining traction in high-end automotive applications due to their extended illumination range and advanced lighting performance.

By vehicle type, passenger vehicles dominate the market owing to increasing consumer demand for advanced lighting systems, premium safety features, and enhanced nighttime driving visibility across sedans, SUVs, and luxury vehicles. Commercial vehicles are also experiencing notable growth as fleet operators and transportation companies adopt adaptive lighting technologies to improve road safety, reduce nighttime driving risks, and comply with vehicle safety regulations in logistics and heavy transportation operations.

07

Report Coverage

Headlight Control Module Market Report Coverage and Deliverables

The "Headlight Control Module Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- headlight control module market size and forecast at global, regional, and country levels for all market segments covered under the scope

- headlight control module market trends, as well as drivers, restraints, and opportunities

- headlight control module market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the headlight control module market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Headlight Control Module Market Geographic Insights

The Headlight Control Module Market demonstrates strong regional growth patterns influenced by automotive production trends, adoption of advanced vehicle safety technologies, increasing penetration of electric vehicles, and evolving automotive lighting regulations across global markets.

North America holds a significant position in the headlight control module market due to the strong presence of leading automotive manufacturers, advanced automotive electronics suppliers, and rapid adoption of intelligent vehicle safety technologies. The United States and Canada are witnessing increasing integration of adaptive front-lighting systems, automatic high beam control, and matrix LED technologies across passenger vehicles, SUVs, and premium automotive segments. The region is strongly focused on enhancing vehicle safety, nighttime driving visibility, and integration of advanced driver assistance systems (ADAS). Rising consumer demand for luxury vehicles, increasing electric vehicle adoption, and ongoing investments in connected vehicle technologies are further supporting market growth. Additionally, the presence of advanced semiconductor and automotive electronics ecosystems is accelerating innovation in AI-based lighting control systems and software-defined vehicle architectures.

Asia Pacific is experiencing the fastest growth in the headlight control module market, driven by rapid automotive production, expanding electric vehicle adoption, and increasing demand for advanced vehicle safety features. Countries such as China, Japan, South Korea, and India are witnessing strong integration of LED lighting systems, adaptive front-lighting technologies, and intelligent headlight control modules across both passenger and commercial vehicles. The region benefits from a large automotive manufacturing base, cost-competitive electronics production, and rising investments in automotive semiconductor technologies. Increasing consumer demand for premium vehicles, government safety regulations, and rapid urbanization are further accelerating market adoption. Additionally, growing investments in autonomous driving technologies and connected mobility platforms are creating new opportunities for AI-enabled lighting control systems across Asia Pacific.

Overall, all major regions are contributing to the expansion of the Headlight Control Module Market through increasing adoption of intelligent automotive lighting systems, vehicle safety technologies, electric mobility platforms, and connected automotive ecosystems.

10

Industry Activity

Recent Developments

The headlight control module market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the headlight control module marketare:

- In March 2026, Diodes Incorporated has launched the AL8859Q, a multi-phase SPI boost controller designed for advanced automotive headlight control units supporting multiple lighting functions. The device supports high beams, low beams, daytime running lights, turn indicators, fog lights and cornering lights within a single integrated lighting module.

- In April 2025, Valeo, with Appotronics, inventor of ALPD laser display technology have announced a strategic partnership to offer a new generation of automotive front lighting solutions integrating exclusive Appotronics’ ALL-in-ONE full-color laser headlight system. Valeo will bring its unique expertise in lighting systems design and electronic control units design, along with unrivaled software capabilities, to integrate Appotronics recognized knowledge in projection systems design based on laser display technologies into new generation front lighting solutions.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank – Global Trade Indicators World Trade Organization (WTO) (International Monetary Fund )IMF International Trade Administration (ITA) Company website Company annual reports Company investor presentations