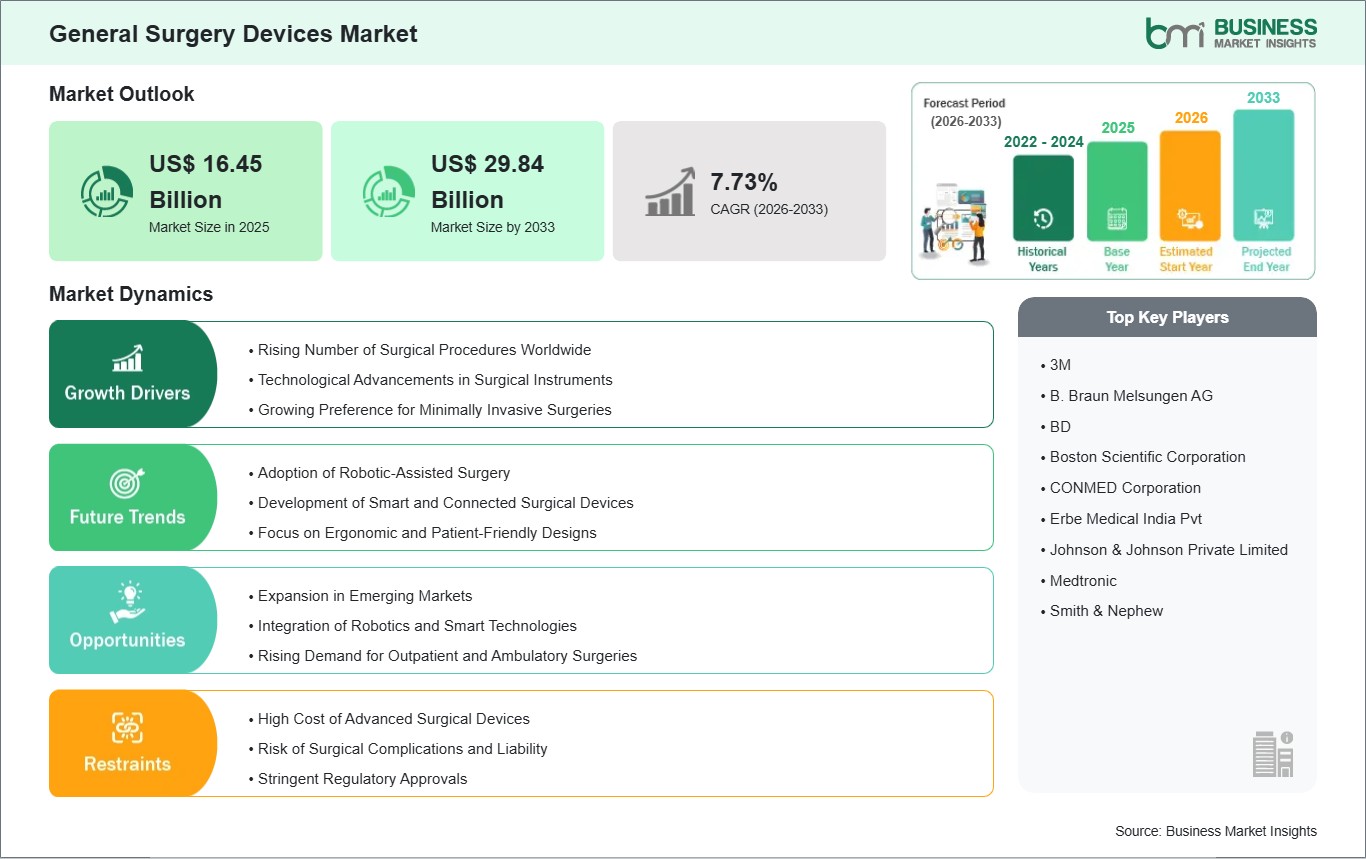

Rising Number of Surgical Procedures Worldwide

The overall increase of surgical operations around the world is the main reason for the growth of the market for general surgery devices, as the rise in the number of operations lifts the demand directly for the supporting instruments, consumables, and advanced technologies needed for operative care. Every year, hundreds of millions of major surgical operations are performed worldwide, with an estimated 300 million surgeries taking place annually. Projections indicate that this number will continue to rise as the population grows and ages. As nations progress and the healthcare system becomes more accessible, there are more patients that have undergone necessary interventions for trauma, chronic diseases like cancer and cardiovascular conditions, and elective or cosmetic surgeries, all requiring a variety of general surgery devices. This increase in surgical procedures is seen in every specialty — from minimally invasive laparoscopic procedures to complex open surgeries — and the hospitals and surgical centers are therefore compelled to increase their inventories of staplers, energy-based devices, retractors, and other tools that not only assist but also improve precision and outcomes.

Furthermore, although the preference for minimally invasive surgeries is still growing, it is due to the advantages like less pain, faster recovery, and lower infection risks that eventually lead to a higher number of these types of procedures which in turn require specialized instruments suitable for their techniques. Meanwhile, the advanced technologies — such as robot-assisted systems and smart energy platforms — are being increasingly integrated into the operating room as they are the ones that can manage the rising number of patients in an efficient and safe way, thus leading to further device adoption.

Integration of Robotics and Smart Technologies

The amalgamation of robots and intelligent technologies presents a powerful growth prospect in the surgical devices market, as it enhances precision, efficacy, and patient outcomes in a fundamental way. The introduction of robotic-assisted systems in hospitals has been increasing not only for general surgeries like cholecystomies and hernia repairs but also for complex cancer and heart surgeries. They enable surgeons to operate with accuracy down to a millimeter, with better skills, and excellent 3D vision, which surpasses that of traditional methods. Research indicates that the use of AI in robotics helps reduce operative time and complications during operations, thereby enhancing clinical safety and increasing throughput and efficiency in hospitals.

The real-life usage growth of the technology is a clear demonstration of this trend: in the UK's NHS, the number of surgeries that are robot-assisted is anticipated to skyrocket in the next decade, with the use of robots in laparoscopic surgeries planned to be the most common across many specialties. Likewise, the da Vinci system, for instance, has recorded a global rise in procedure volume of more than ten percent, which is indicative of the strong clinical demand and the confidence of surgeons and healthcare facilities.

The use of smart technologies such as AI, machine learning, and advanced imaging integration is paving the way for the next generation of surgical robots that can assist in surgical planning, provide real-time decision support, and even perform some semi-autonomous functions. This technology allows for the reduction of inter-operator variability and at the same time, it may improve the consistency while the connected data analytics further enhance the performance and provide support in training.