01

Market Summery

Executive Summary and Global Market Analysis

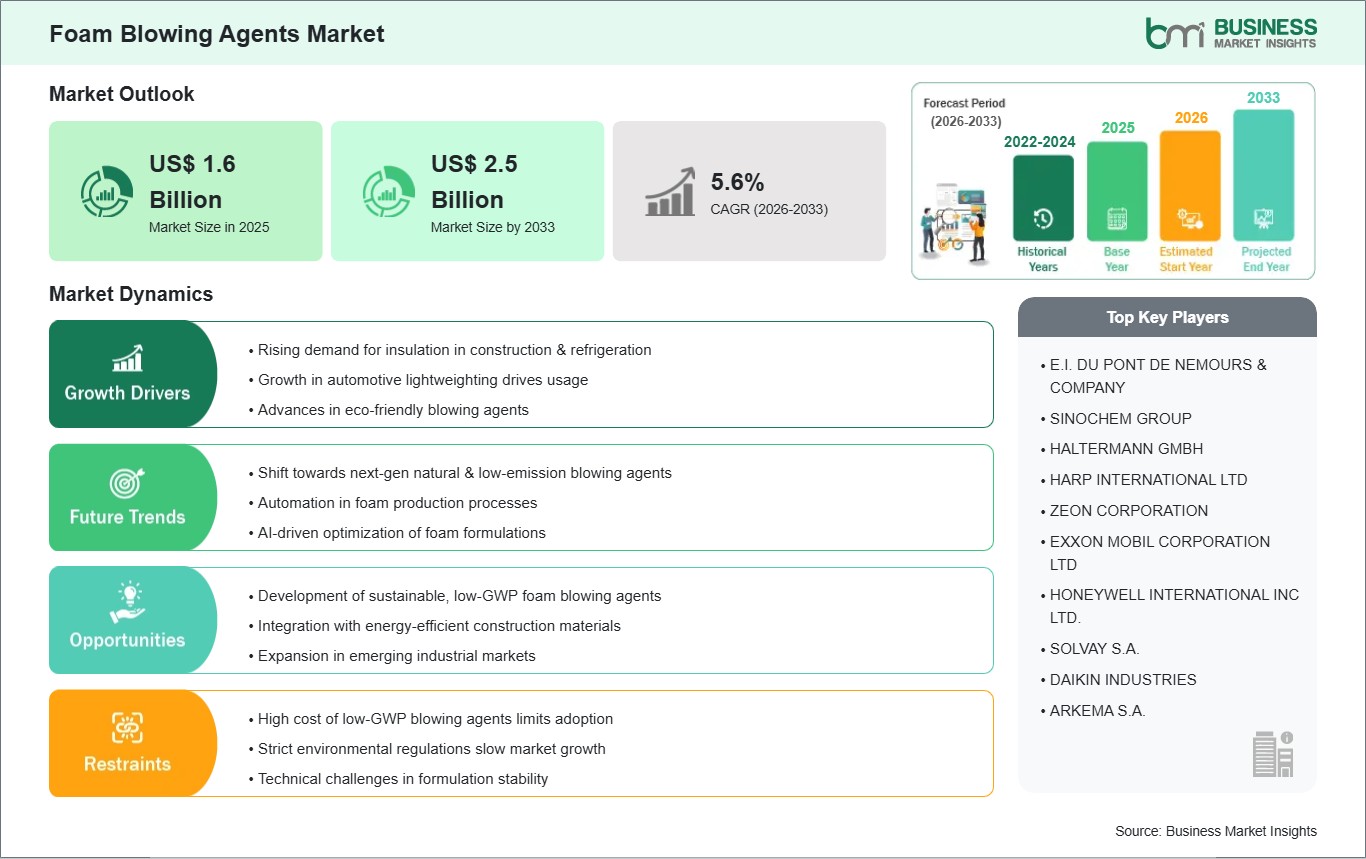

Foam Blowing Agents play a vital role in the production of high-performance polymer foams. These substances offer critical advantages, including the creation of high-R-value thermal insulation for energy-efficient buildings, lightweighting for automotive components, and shock absorption for protective packaging. Growth is driven by stringent global energy efficiency mandates, the rapid expansion of cold chain logistics for food and pharmaceuticals, and the surging demand for sustainable construction materials. Furthermore, the shift toward fourth-generation HFO technologies is fundamentally reshaping the market to meet zero-ODP (Ozone Depletion Potential) and ultra-low-GWP (Global Warming Potential) standards.

However, several challenges can restrain market growth: high capital and R&D costs associated with transitioning from legacy HFCs to advanced HFO formulations remain a significant barrier for smaller manufacturers. Stringent environmental regulations, such as the Kigali Amendment and the EU F-Gas Regulation, impose aggressive phase-down schedules that create supply-side pressures. Additionally, the industry faces constraints due to the flammability and safety risks associated with cost-effective hydrocarbons (like pentane) and persistent volatility in petrochemical feedstock prices. Despite these hurdles, the market holds immense opportunities in the universal mandate for decarbonized infrastructure and the accelerating adoption of bio-based and CO2-derived blowing agents. The expansion into vacuum insulation panels and the integration of AI-driven precision dosing to optimize foam density and cell uniformity are expected to create significant opportunities for market growth.

03

Segment Analysis

Foam Blowing Agents Market Segmentation

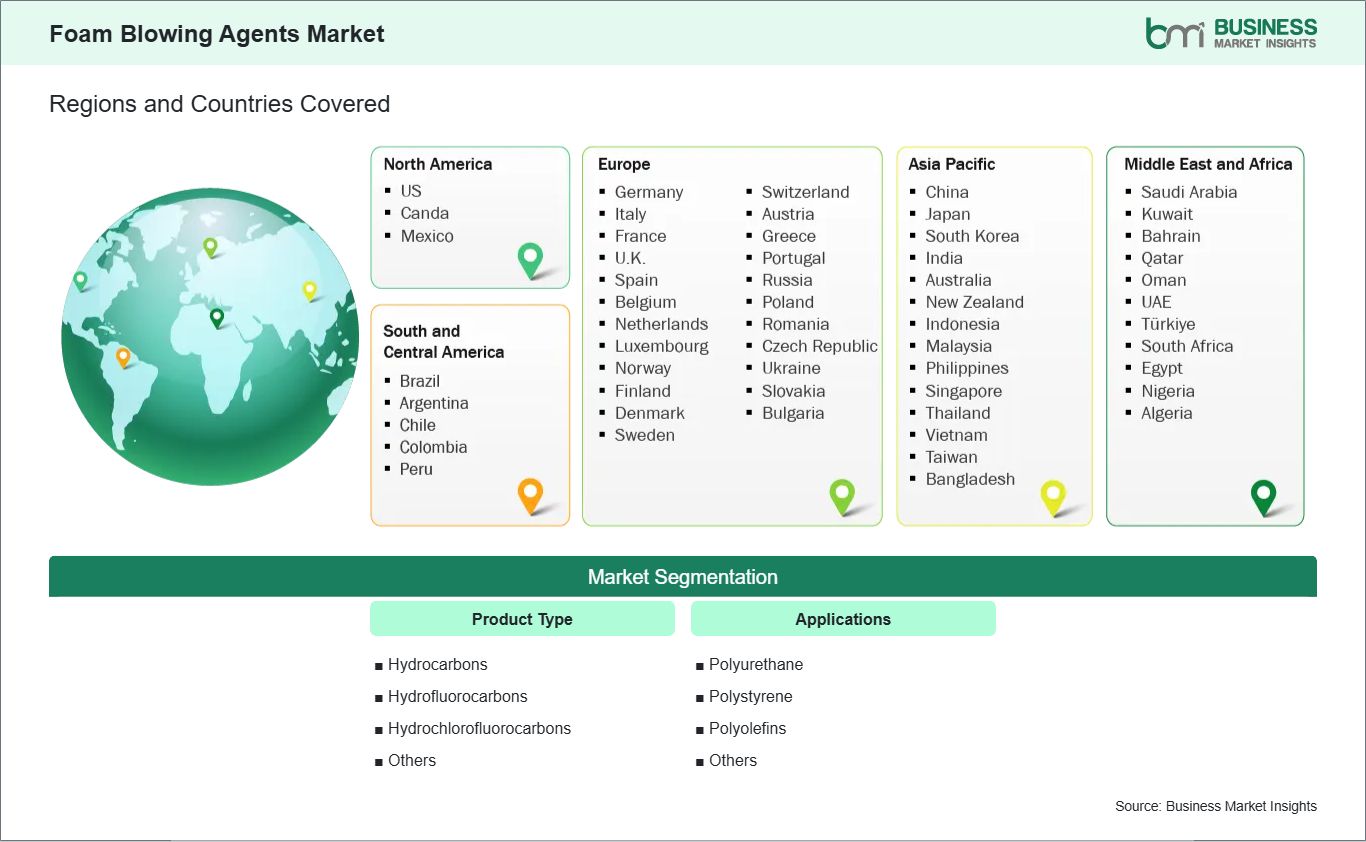

Key segments that contributed to the derivation of the Foam Blowing Agents market analysis are product type and applications.

- By Product Type, the market is segmented into Hydrocarbons, Hydrofluorocarbons, Hydrochlorofluorocarbons, and Others.

- By Applications, the market is segmented into Polyurethane, Polystyrene, Polyolefins, and Others.

04

Market Forces

Foam Blowing Agents Market Drivers and Opportunities

Energy Efficiency Standards and Rapid Urbanization

As governments implement stringent building codes, such as the European Union’s Energy Performance of Buildings Directive and the U.S. Department of Energy’s efficiency standards, there is a surging demand for high-performance thermal insulation. Foam blowing agents are essential in producing rigid polyurethane (PU) and polystyrene (XPS/EPS) foams, which offer superior R-values, helping to drastically reduce energy consumption for heating and cooling. This demand is further amplified by rapid urbanization in emerging economies, particularly in Asia Pacific, where large-scale residential and commercial infrastructure projects are expanding. Additionally, the flourishing "cold chain" logistics and home appliance markets rely on these agents to provide the critical insulation required for refrigerators and temperature-controlled containers. Furthermore, the automotive industry’s shift toward lightweighting to enhance fuel efficiency and electric vehicle (EV) range is driving the use of foamed polymers for seating, headliners, and acoustic insulation, solidifying the market's growth across diverse industrial applications.

Low-GWP Transitions and HFO Innovation

A significant high-value opportunity lies in the global transition toward low Global Warming Potential (GWP) and zero Ozone Depletion Potential (ODP) blowing agents. Under the mandates of the Kigali Amendment to the Montreal Protocol, the industry is phasing out high-GWP hydrofluorocarbons (HFCs) in favor of next-generation Hydrofluoroolefins (HFOs). HFOs offer a massive opportunity for manufacturers, as they combine environmental compliance with superior insulating properties (lower k-factors) compared to traditional hydrocarbons. There is a burgeoning market for specialized HFO blends that balance non-flammability with high thermal efficiency, particularly for spray foam insulation and high-end appliances. Furthermore, the rise of the circular economy presents opportunities for bio-based blowing agents and chemical recycling technologies that allow for the recovery of blowing agents from end-of-life foams. Manufacturers who invest in "liquid blowing agent" (LBA) technologies for 3D-printed construction and advanced battery thermal management systems for EVs are positioned to capture high-margin segments. By bridging the gap between rigorous sustainability regulations and high-performance material demands, companies can lead the shift toward a more climate-resilient and resource-efficient foaming industry.

05

Size and Share Analysis

Foam Blowing Agents Market Size and Share Analysis

The Foam Blowing Agents market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within product type and applications, offering insights into their contribution to overall market performance.

For instance, the Hydrocarbons subsegment holds a significant market share due to its zero-ozone depletion potential (ODP) and low-global warming potential (GWP). These agents, such as cyclopentane and pentane, are extensively used in the production of Polyurethane rigid foams for the appliances and construction sectors. As a cost-effective alternative to fluorinated gases, hydrocarbons are particularly favored in the manufacture of energy-efficient refrigerators and freezers, where they provide a balance of effective thermal insulation and regulatory compliance.

07

Report Coverage

Foam Blowing Agents Market Report Coverage and Deliverables

The "Foam Blowing Agents Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- Foam Blowing Agents market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Foam Blowing Agents market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Foam Blowing Agents market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Foam Blowing Agents market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Foam Blowing Agents Market Geographic Insights

The geographical scope of the Foam Blowing Agents market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

The Asia-Pacific Foam Blowing Agents Market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The market is primarily fueled by the massive expansion of the building and construction sector and the rising production of consumer appliances like refrigerators and air conditioners.

Growth is further bolstered by the global transition toward low-GWP and zero-ODP agents, such as hydrofluoroolefins (HFOs) and hydrocarbons. The increasing demand for energy-efficient insulation in cold chain logistics and the shift toward lightweight materials in the automotive industry to improve fuel efficiency solidify Asia Pacific as a central hub for innovation and the adoption of next-generation blowing agent technologies.

10

Industry Activity

Recent Developments

The Foam Blowing Agents market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Foam Blowing Agents market are:

- In August 2025, Arkema inaugurated the Forane® Foam Blowing Agent (FBA) 1233zd unit at its Calvert City, Ky. manufacturing plant. This expansion increases Arkema’s North American output to 15 Kilotons per year, reinforcing the company’s commitment to meeting growing global market demand. As a non-ozone depleting foam-blowing agent, Forane® FBA 1233zd provides a versatile and more sustainable solution for industries such as construction, roofing, and appliance manufacturing. Forane® FBA 1233zd is designed to tackle key challenges faced by polyurethane foam manufacturers, including thermal performance, environmental impact, and safety.

- In April 2024, Solvay inaugurated its dedicated Alve-One- production unit in Rosignano, Italy, introducing an eco-designed chemical blowing agent for thermoplastic foams. Alve-One- targets automotive, footwear, construction, and consumer goods applications, offering sustainability benefits and enhanced health and safety standards. The product has received recognition from ChemSec, Solar Impulse Foundation, Inovyn, and France Chimie for innovation and efficiency.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations