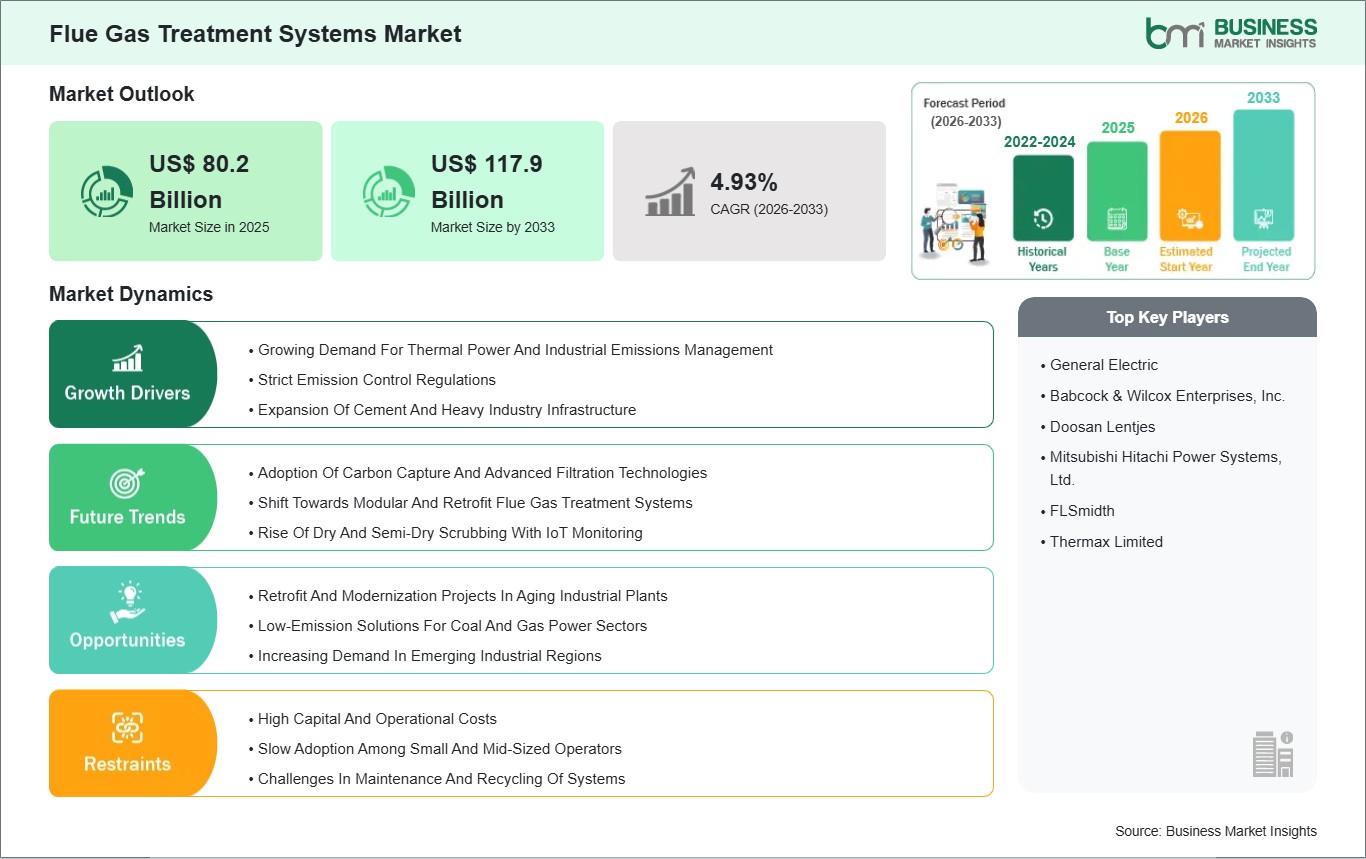

The Flue Gas Treatment Systems Market size is expected to reach US$ 117.9 Billion by 2033 from US$ 80.2 Billion in 2025. The market is estimated to record a CAGR of 4.93% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The flue gas treatment systems market provides various technologies that help to reduce dangerous emissions from industrial processes, power generation plants, and manufacturing operations. The systems function as essential equipment that controls emissions from sulfur oxides, nitrogen oxides and particulate matter and other dangerous gases that endanger both human life and environmental safety. The market grows because industries and consumers become more environmentally conscious while businesses work to satisfy strict air quality standards through their regulatory obligations. Modern industries are increasingly implementing advanced treatment technologies, which include scrubbers and fabric filters, electrostatic precipitators and selective catalytic reduction systems that deliver high operational efficiency with dependable performance and low system downtime.

The growth of new plants and the retrofitting of existing plants receive support from industrial expansion in the energy sector, the chemical industry, the cement industry and the steel industry. The market for innovative emission control technologies expands because companies need to adopt sustainable business practices while the world moves toward environmentally friendly industrial methods. Multiple obstacles exist that challenge the market for new emission control technologies. The market faces challenges because the installation costs of technologies and their maintenance requirements need specialized outside expertise. The market for new emission control technologies will experience growth challenges because of the transition to renewable energy sources.

Flue Gas Treatment Systems Market - Strategic Insights:

Get more information on this report

Flue Gas Treatment Systems Market Segmentation Analysis:

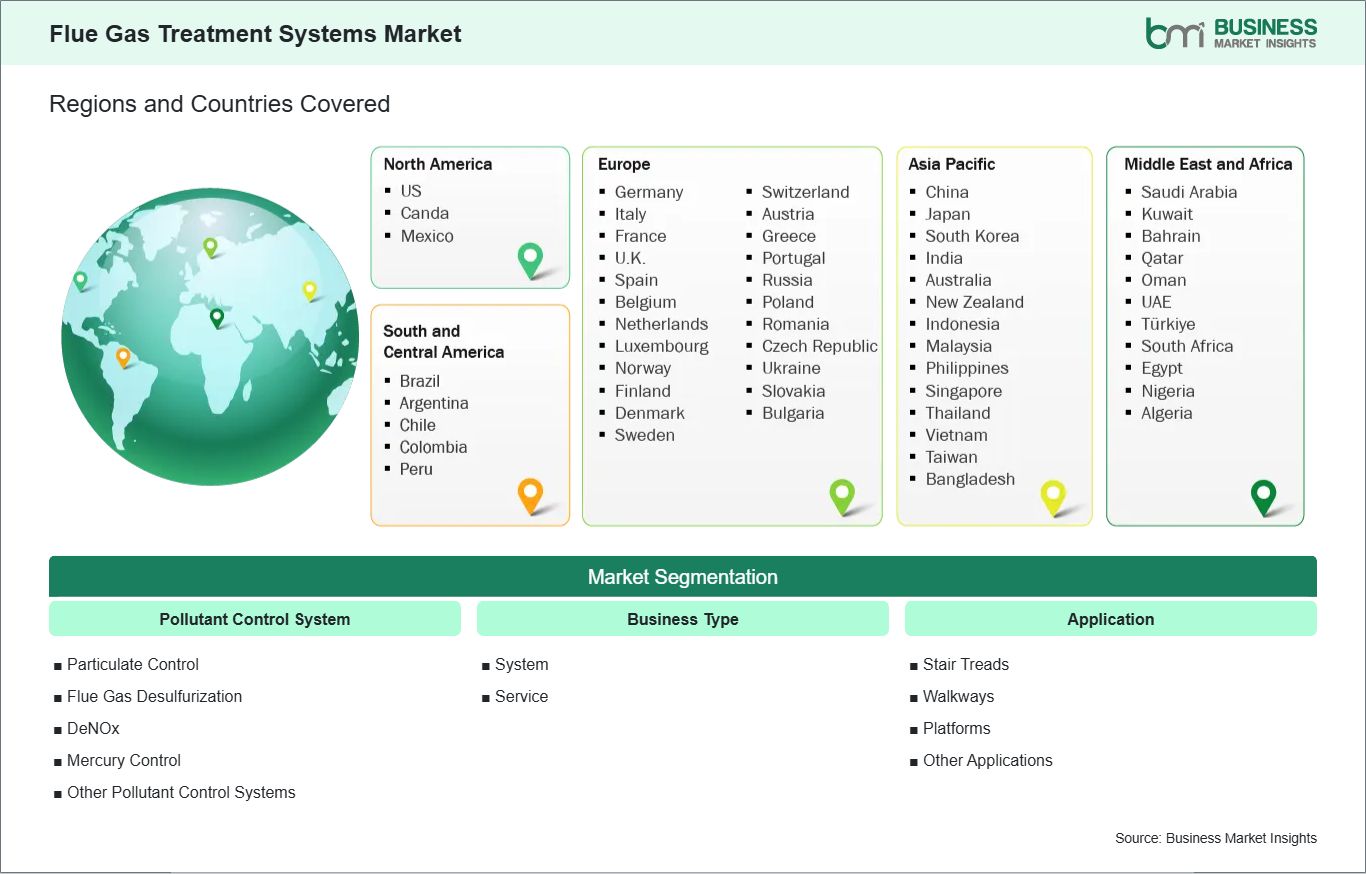

Key segments that contributed to the derivation of the flue gas treatment systems market analysis are pollutant control system, business type, and end‑use industry.

By pollutant control system, the flue gas treatment systems market is segmented into particulate control, flue gas desulfurization (FGD), DeNOx, mercury control, and other pollutant control systems. The particulate control subsegment dominated the market in 2025.

Based on business type, the flue gas treatment systems market is classified into system and service. The system subsegment dominated the market in 2025.

In terms of end‑use industry, the flue gas treatment systems market is divided into power, chemical & petrochemical, iron & steel, non‑ferrous metal, cement, and other industries. The power subsegment dominated the market in 2025.

Flue Gas Treatment Systems Market Drivers and Opportunities:

Growing Demand For Thermal Power And Industrial Emissions Management

The global flue gas treatment systems market is increasingly driven by the growing need to control emissions from thermal power plants and other industrial operations. As industrialization and energy demand continue to rise, plants are seeking reliable technologies to reduce pollutants such as sulfur dioxide, nitrogen oxides, and particulate matter. Flue gas treatment systems, including scrubbers, electrostatic precipitators, and selective catalytic reduction units, play a critical role in ensuring compliance with stricter environmental regulations while maintaining operational efficiency. The adoption of these systems allows facilities to minimize environmental impact while sustaining high output levels.

Regions have their own distinct patterns of demand, depending on the mix of energy used and the nature of industries. In regions where there is a high demand for coal or fossil fuel-based electricity generation, flue gas treatment systems are being adopted to meet local regulations and environmental norms. In regions where there is a mix of industries, including chemical, cement, and metal processing industries, the adoption of flue gas treatment systems ensures the clean operation of industries, meeting local regulations for air quality standards.

Environmental awareness and sustainability goals further support the adoption of flue gas treatment systems. Companies are investing in modern technologies that reduce emissions while optimizing energy consumption and operational costs. Advanced monitoring, automation, and integrated control systems enhance treatment efficiency, enabling operators to manage complex emissions profiles effectively. As global regulatory frameworks evolve and stakeholders emphasize cleaner industrial processes, the demand for flue gas treatment systems is expected to remain strong, particularly in regions balancing industrial growth with environmental responsibility.

Retrofit And Modernization Projects In Aging Industrial Plants

Retrofit and modernization projects in aging industrial facilities represent a significant opportunity for the flue gas treatment systems market. Older power plants, manufacturing units, and chemical facilities often operate with outdated emissions control equipment, which may not meet contemporary environmental or efficiency standards. Upgrading these plants with advanced flue gas treatment solutions helps operators comply with current regulations, enhance operational reliability, and improve energy efficiency. Such projects also reduce maintenance requirements, extend equipment lifespans, and minimize operational disruptions.

Regional industrial characteristics also have an effect on the demand for industrial retrofits and the technologies that are chosen for the process. This is particularly true for regions with a well-developed industrial infrastructure, where older plants present the best opportunities for retrofitting and the implementation of technologies such as selective catalytic reduction, wet and dry scrubbing systems, and sophisticated filtration systems to meet the new emission targets. Regions with a growing industrial infrastructure present opportunities for retrofitting that incorporate modular technologies with minimal process downtime.

Sustainability and environmental performance goals amplify the importance of modernization initiatives. Many industrial operators aim to achieve cleaner operations while reducing their carbon footprint, and advanced flue gas treatment systems enable these objectives without significant process overhauls. The integration of real-time monitoring, predictive maintenance, and energy-optimized technologies ensures that retrofitted plants operate efficiently while meeting strict emission requirements. As a result, modernization and retrofit projects are expected to remain a vital component of market growth, with demand spanning across aging thermal, industrial, and chemical production facilities worldwide.

Flue Gas Treatment Systems Market Size and Share Analysis:

The flue gas treatment systems market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within pollutant control system, business type, and end‑use industry, highlighting their respective contributions to overall market performance.

By pollutant control system, the Particulate Control subsegment dominated the Flue Gas Treatment Systems market in 2025. Particulate control systems offer effective removal of dust and particulate matter from flue gases, making them highly suitable for industrial emission control, which drives their widespread adoption.

Based on business type, the System subsegment dominated the Flue Gas Treatment Systems market in 2025. Complete system solutions provide integrated technology and operational efficiency, making them highly suitable for industrial and utility applications, which drives their widespread adoption.

Based on end‑use industry, the Power subsegment dominated the Flue Gas Treatment Systems market in 2025. Power generation applications demand reliable and efficient flue gas treatment to comply with environmental regulations, making this segment highly suitable for emission control, which drives its widespread adoption.

Flue Gas Treatment Systems Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

General Electric

Babcock & Wilcox Enterprises, Inc.

Doosan Lentjes

Mitsubishi Hitachi Power Systems, Ltd.

FLSmidth

Thermax Limited

Get more information on this report

Flue Gas Treatment Systems Market Report Coverage and Deliverables:

The "Flue Gas Treatment Systems Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Flue Gas Treatment Systems market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Flue Gas Treatment Systems market trends, as well as drivers, restraints, and opportunities

Flue Gas Treatment Systems market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Flue Gas Treatment Systems market

Detailed company profiles, including SWOT analysis

Flue Gas Treatment Systems Market Geographic Insights:

The geographical scope of the Flue Gas Treatment Systems market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Flue Gas Treatment Systems market in North America is expected to grow during the forecast period.

North America maintains its leading role in the worldwide flue gas treatment systems market because of its developed industrial sector, strict environmental laws and dedicated environmental conservation efforts. The power generation industry, with chemical production and cement and steel manufacturing sectors, maintains continuous demand for emission control technologies, which creates market potential for new equipment and upgrades of existing facilities.

The regulatory agencies mandate strict air quality requirements, which force facilities to implement state-of-the-art flue gas treatment systems for compliance purposes. The regulatory authorities maintain ongoing pressure, driving technological development while creating persistent market needs for systems that achieve pollution control without hindering operational performance. The region maintains its position as the leading market area through ongoing technological progress. Manufacturers enhance flue gas treatment equipment performance and reliability through the utilization of advanced control systems with automation and monitoring technologies.

Environmental sustainability objectives, with corporate social obligations and environmental protection commitments, drive businesses to adopt technologies that use less energy and produce cleaner emissions. North America maintains a secure and expanding market because businesses face obstacles, including expensive system setup costs and the requirement for specialized knowledge and changes in energy patterns. North America drives the worldwide expansion of the flue gas treatment systems market because it possesses advanced infrastructure, environmental preservation goals and industrial requirements.

Get more information on this report

Flue Gas Treatment Systems Market Research Report Guidance:

The report includes qualitative and quantitative data in the Flue Gas Treatment Systems market across pollutant control system, business type, end‑use industry, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Flue Gas Treatment Systems market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Flue Gas Treatment Systems market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Flue Gas Treatment Systems market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the Flue Gas Treatment Systems market segments by pollutant control system, business type, end‑use industry, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume, revenue forecast, and factors driving the market.

Chapter 11 describes the competitive analysis with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Flue Gas Treatment Systems market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Flue Gas Treatment Systems Market News and Key Development:

The flue gas treatment systems market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the flue gas treatment systems market are:

In March 2024, ANDRITZ AG announced that it was selected to upgrade flue gas treatment systems at the Mörrum pulp mill in Sweden, replacing and modernizing three electrostatic precipitators (ESPs) with new high‑efficiency components to extend their lifecycle and improve emission control performance.

In February 2024, Babcock & Wilcox Enterprises, Inc. announced that its Babcock & Wilcox Canada Corp. was awarded a contract worth US$ ~13 million to supply low‑NOx burners and design flue gas recirculation systems and related equipment for a North American petroleum refinery, helping reduce NOx emissions and comply with environmental standards.

Key Sources Referred:

International Organization for Standardization (ISO)American Society for Testing and Materials (ASTM International)Bureau of Indian Standards (BIS)Environmental Protection Agency (EPA), USAEuropean Chemicals Agency (ECHA)Central Pollution Control Board (CPCB), IndiaMinistry of Chemicals and Fertilizers, IndiaAmerican Chemistry Council (ACC)Indian Chemical Council (ICC)European Chemical Industry Council (Cefic)Specialty Chemical Association of India (SCAI)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Flue Gas Treatment Systems Market

General Electric

Babcock & Wilcox Enterprises, Inc.

Doosan Lentjes

Mitsubishi Hitachi Power Systems, Ltd.

FLSmidth

Thermax Limited

Frequently Asked Questions

How big is the Flue Gas Treatment Systems Market?

The Flue Gas Treatment Systems Market is valued at US$ 80.2 Billion in 2025, it is projected to reach US$ 117.9 Billion by 2033.

What is the CAGR for Flue Gas Treatment Systems Market by (2026 - 2033)?

As per our report Flue Gas Treatment Systems Market, the market size is valued at US$ 80.2 Billion in 2025, projecting it to reach US$ 117.9 Billion by 2033. This translates to a CAGR of approximately 4.93% during the forecast period.

What segments are covered in this report?

The Flue Gas Treatment Systems Market report typically cover these key segments-

Pollutant Control System (Particulate Control, Flue Gas Desulfurization [FGD], DeNOx, Mercury Control, Other Pollutant Control Systems)

Business Type (System, Service)

Application (Stair Treads, Walkways, Platforms, Other Applications)

What is the historic period, base year, and forecast period taken for Flue Gas Treatment Systems Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Flue Gas Treatment Systems Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Flue Gas Treatment Systems Market?

The Flue Gas Treatment Systems Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

General Electric

Babcock & Wilcox Enterprises, Inc.

Doosan Lentjes

Mitsubishi Hitachi Power Systems, Ltd.

FLSmidth

Thermax Limited

Who should buy this report?

The Flue Gas Treatment Systems Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Flue Gas Treatment Systems Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Flue Gas Treatment Systems Market

Get Free Sample For Flue Gas Treatment Systems Market