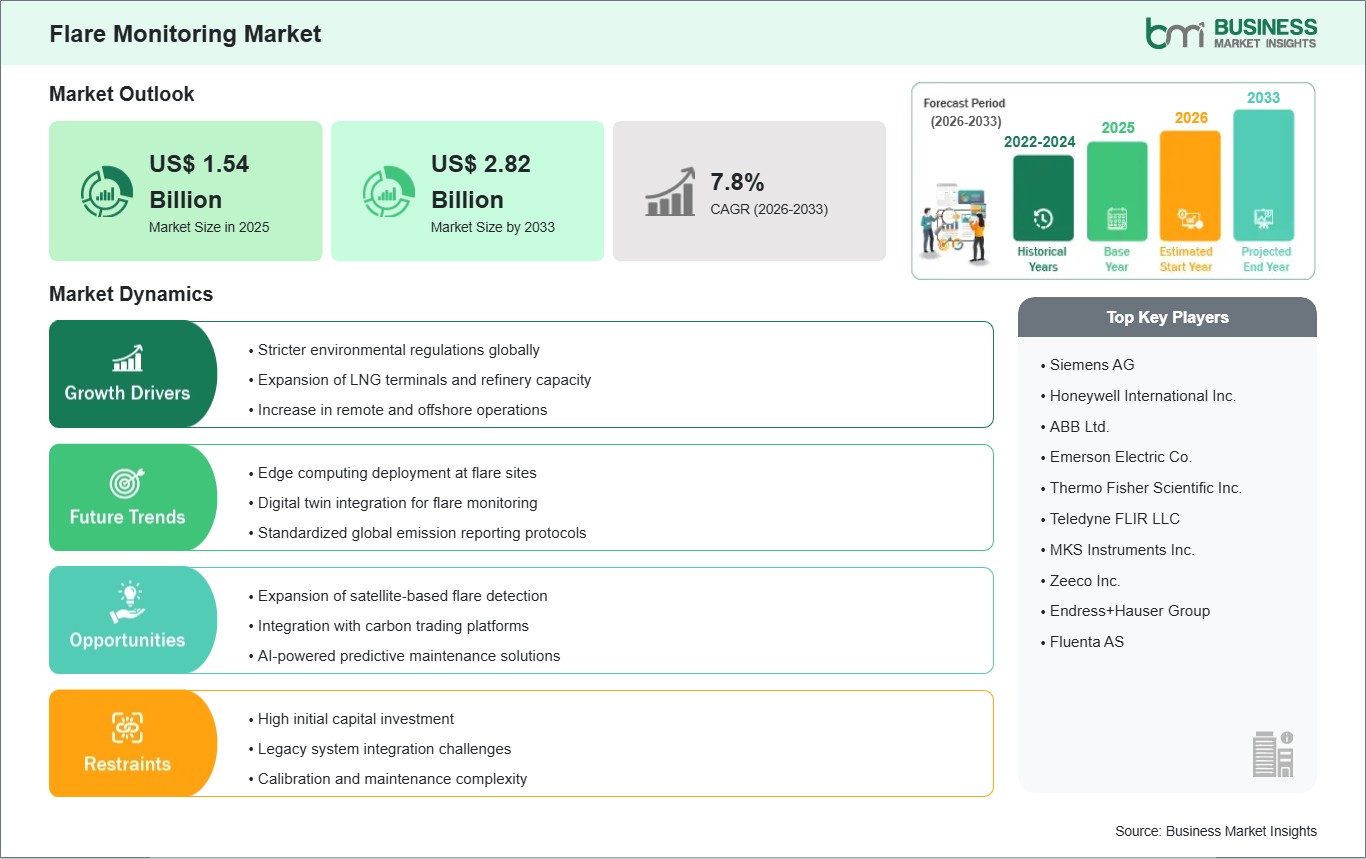

The Flare Monitoring Market size is expected to reach US$ 2.82 Billion by 2033 from US$ 1.54 Billion in 2025. The market is estimated to record a CAGR of 7.86% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global flare monitoring market is a critical component of industrial safety and environmental compliance, encompassing technologies and services designed to measure, analyze, and monitor flare emissions from industrial facilities such as oil refineries, petrochemical plants, offshore platforms, and landfills. Flare monitoring systems are essential for detecting and quantifying gases released during the flaring process, ensuring regulatory compliance, operational efficiency, and environmental protection. The market is experiencing robust growth propelled by stringent environmental regulations enforced by government agencies worldwide, increasing corporate focus on zero-flaring goals and sustainability commitments, and technological advancements in monitoring solutions. The integration of advanced technologies such as infrared cameras, thermal imaging, remote sensing, gas analyzers, and software-based monitoring platforms has revolutionized flare monitoring capabilities, enabling real-time visualization of flare emissions, continuous combustion efficiency assessment, and automated reporting for regulatory compliance.

The market's expansion is further driven by the global emphasis on reducing greenhouse gas emissions, the World Bank's Zero Routine Flaring by 2030 initiative, and the financial motivation for operators to enhance gas recovery and reduce product loss. However, the market faces significant challenges, including the high initial capital investment required for advanced monitoring systems, technical complexities in retrofitting legacy infrastructure, and the need for skilled personnel to operate sophisticated monitoring equipment. Despite these constraints, compelling opportunities are emerging from the adoption of satellite-based and drone remote monitoring technologies, the incorporation of artificial intelligence and machine learning for predictive analytics, and the expansion of flare monitoring into emerging markets undergoing rapid industrialization. The shift toward intelligent, AI-enabled systems facilitates proactive operational control, enabling operators to dynamically adjust process parameters, optimize flare efficiency, and minimize waste gas volumes.

Flare Monitoring Market - Strategic Insights:

Get more information on this report

Flare Monitoring Market Segmentation Analysis:

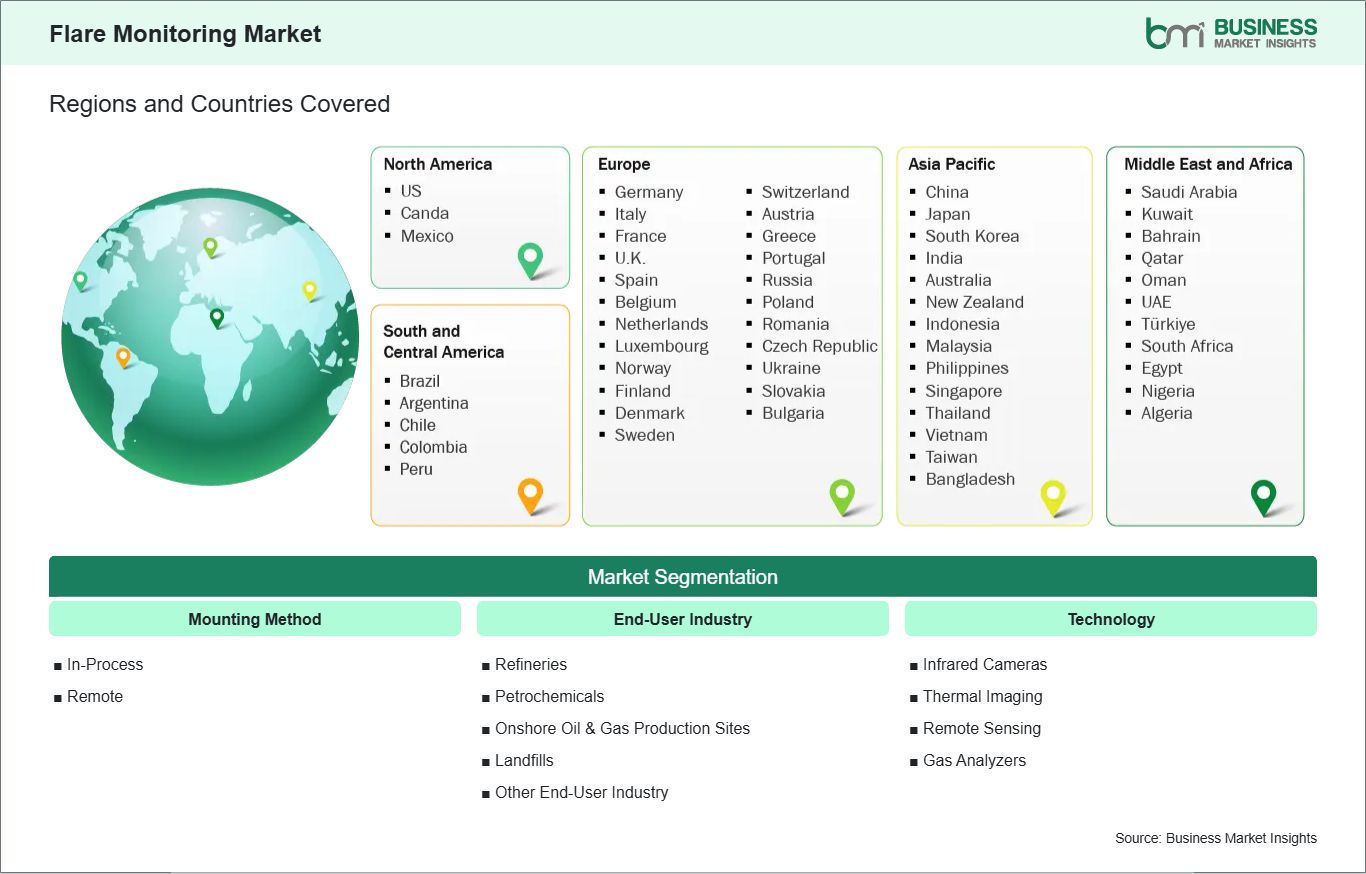

Key segments that contributed to the derivation of the flare monitoring market analysis are mounting method, end-user industry, and technology.

By mounting method, the market is segmented into in-process and remote monitoring systems. The in-process segment dominated the market in 2025.

By end-user industry, the market is categorized into refineries, petrochemicals, onshore oil & gas production sites, landfills, and other end-users. The refineries segment held the largest share in 2025.

By technology, the market is segmented into infrared cameras, thermal imaging, remote sensing, gas analyzers, and other types. The infrared cameras segment accounts for the largest revenue share in 2025.

Flare Monitoring Market Drivers and Opportunities:

Stringent Environmental Regulations and Emission Compliance Mandates

A primary driver for the flare monitoring market is the increasingly rigorous global regulatory landscape mandating real-time emissions tracking and comprehensive environmental surveillance. Governments and regulatory bodies worldwide, including the U.S. Environmental Protection Agency, the European Environment Agency, and similar agencies in Canada, China, and India, are imposing stringent requirements for monitoring and reporting flare emissions from industrial facilities. Regulations such as the U.S. EPA's 40 CFR Part 60 Subpart Ja and the European Union's Industrial Emissions Directive require continuous monitoring of volatile organic compounds, sulfur dioxide, and carbon dioxide emissions. Non-compliance can lead to severe penalties, operational restrictions, and reputational damage, compelling operators to invest in advanced flare monitoring systems. The enforcement of rigorous environmental compliance mandates forces operators to implement high-precision monitoring systems to avoid legal consequences and financial penalties. The implementation of waste emissions charges, setting fees on wasteful methane emissions, creates powerful economic incentives for accurate monitoring and emissions reduction. This regulatory environment necessitates the use of automated metering solutions that can differentiate between routine and non-routine flaring events to ensure regulatory adherence and accurate fee calculations.

Technological Advancements in Non-Contact and AI-Powered Monitoring

A transformative opportunity lies in the convergence of advanced monitoring technologies with artificial intelligence and predictive analytics. The widespread adoption of non-contact flare monitoring systems, including thermal infrared imaging, ultraviolet detection, and drone-based monitoring solutions, is revolutionizing flare monitoring by providing precise, continuous measurements without physical intervention. Thermal cameras with infrared sensors enable real-time visualization of flare emissions, while UV-based systems offer rapid flame detection even in adverse weather conditions such as fog or heavy rain. Furthermore, the incorporation of artificial intelligence and machine learning for predictive analytics is converting flare monitoring from a passive recording role into a tool for proactive operational control. Advanced algorithms can now process combustion data in real-time to predict potential flaring events before they occur, allowing operators to dynamically adjust process parameters and optimize flare efficiency. This shift toward intelligent systems facilitates immediate corrective actions that ensure optimal combustion performance and minimize waste gas volumes. The application of AI across various functions, including emissions monitoring, has resulted in significant reductions in flaring and methane emissions, proving the value of strict monitoring protocols combined with advanced analytics.

Flare Monitoring Market Size and Share Analysis:

By mounting method, remote monitoring systems are gaining significant market share due to their advantages in ease of deployment, reduced maintenance requirements, and ability to monitor multiple flare stacks from a single location. The remote segment's growth is driven by increasing adoption of infrared imaging and drone-based monitoring solutions that offer comprehensive coverage without interrupting operations.

By end-user industry, refineries currently hold the largest revenue share, accounting for a significant portion of global flare monitoring investments. This dominance is attributed to the extensive use of flaring systems in refining operations, the complexity of emission streams, and stringent regulatory oversight in developed regions. The onshore oil and gas production sites segment is projected to experience the fastest growth, driven by increasing upstream activities, rising environmental scrutiny, and global initiatives to reduce routine flaring in production operations.

By technology, infrared cameras and thermal imaging systems represent the largest and fastest-growing segment, driven by their ability to provide real-time visualization, accurate temperature measurement, and reliable performance in harsh environmental conditions. The integration of these imaging systems with advanced analytics platforms enhances their value proposition by enabling automated emissions quantification and compliance reporting.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Siemens AG

Honeywell International Inc.

ABB Ltd.

Emerson Electric Co.

Thermo Fisher Scientific Inc.

Teledyne FLIR LLC

MKS Instruments Inc.

Zeeco Inc.

Endress+Hauser Group

Fluenta AS

Get more information on this report

Flare Monitoring Market Report Coverage and Deliverables:

The "Flare Monitoring Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Flare Monitoring Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Flare Monitoring Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Flare Monitoring Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the flare monitoring market

Detailed company profiles, including SWOT analysis

Flare Monitoring Market Geographic Insights:

The geographical scope of the flare monitoring market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America currently holds the largest market share, while Asia Pacific is projected to witness the highest growth rate during the forecast period.

North America, led by the United States, is the most technologically advanced and mature market, characterized by strong regulatory frameworks, significant investments in emissions monitoring infrastructure, and a strong emphasis on reducing emissions from upstream activities. The oil and gas industry in the region is undergoing structural reforms in which facility modernization is a key area of intervention, creating lucrative opportunities for market players. The call for flare monitoring is predicted to remain strong in North America during the evaluation period, driven by stringent enforcement of environmental regulations and corporate sustainability commitments.

Asia Pacific is the fastest-growing regional market, fueled by rapid industrialization, substantial expansion of the oil and gas sector, and tightening environmental controls in China, India, and Southeast Asian nations. India and China have become two of the world's largest oil and gas consumers and present attractive expansion opportunities for the worldwide flare monitoring market. The need to respect the environment has generated commitments from several countries to improve air quality and address the problems associated with rising levels of pollution. To meet regulatory standards, various large-scale industries in China have been forced to install emission monitoring devices to measure the concentration of harmful gases emitted by flares, stimulating demand for new installations of flare monitoring systems.

Europe maintains a strong market presence as the second-largest market for flare monitoring, with healthy expansion rates projected for years to come. The region's stringent environmental directives, robust industrial monitoring practices, and strong emphasis on achieving carbon neutrality drive adoption of advanced flare monitoring solutions across member states. Countries like Germany, France, and the United Kingdom are at the forefront of adopting innovative monitoring technologies to comply with EU regulations and meet sustainability targets.

Get more information on this report

Flare Monitoring Market Research Report Guidance:

The report includes qualitative and quantitative data in the flare monitoring market across mounting method, end-user industry, technology, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the flare monitoring market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the flare monitoring market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the flare monitoring market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover flare monitoring market segments by mounting method, end-user industry, technology, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the flare monitoring market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Flare Monitoring Market News and Key Development:

The flare monitoring market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the flare monitoring market are:

In May 2025, Chevron Richmond recently installed flare.IQ, a real-time, automated system that will improve the facility`s flaring performance. The technology, developed by Panametrics, a Baker Hughes business, uses sensors to monitor, reduce and control flaring in real time. It collects and assesses data on refinery processes, such as temperature, pressure, gas flow and gas composition, and adjusts accordingly to ensure flares burn more efficiently and cleanly, leading to fewer emissions.

In December 2024, Flotek Industries, Inc. ("Flotek" or the "Company") (NYSE: FTK) provided an update regarding flare monitoring regulations issued by the Environmental Protection Agency ("EPA"). On December 20, 2024, the EPA issued proposed amendments to its New Source Performance Standards and Emission Guidelines for Existing Sources for the Crude Oil and Natural Gas Source Category ("OOOOb") rules issued on May 8, 2024, with respect to monitoring the Net Heating Value ("NHV") of flares to ensure that methane emissions are minimized. While the proposed amendments address many industry concerns regarding the complexity of the testing, they do not materially change the Company's outlook regarding the potential addressable market for monitoring services including the scope of installations that will be subject to compliance.

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Flare Monitoring Market

Siemens AG

Honeywell International Inc.

ABB Ltd.

Emerson Electric Co.

Thermo Fisher Scientific Inc.

Teledyne FLIR LLC

MKS Instruments Inc.

Zeeco Inc.

Endress+Hauser Group

Fluenta AS

Frequently Asked Questions

How big is the Flare Monitoring Market?

The Flare Monitoring Market is valued at US$ 1.54 Billion in 2025, it is projected to reach US$ 2.82 Billion by 2033.

What is the CAGR for Flare Monitoring Market by (2026 - 2033)?

As per our report Flare Monitoring Market, the market size is valued at US$ 1.54 Billion in 2025, projecting it to reach US$ 2.82 Billion by 2033. This translates to a CAGR of approximately 7.86% during the forecast period.

What segments are covered in this report?

The Flare Monitoring Market report typically cover these key segments-

Mounting Method (In-Process (Mass Spectrometers, Gas Chromatographs, Gas Analyzers), Remote (IR Imagers, MSIR Imagers))

End-User Industry (Refineries, Petrochemicals, Onshore Oil & Gas Production Sites, Landfills, Other End-User Industry)

Technology (Infrared Cameras, Thermal Imaging, Remote Sensing, Gas Analyzers)

What is the historic period, base year, and forecast period taken for Flare Monitoring Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Flare Monitoring Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Flare Monitoring Market?

The Flare Monitoring Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Siemens AG

Honeywell International Inc.

ABB Ltd.

Emerson Electric Co.

Thermo Fisher Scientific Inc.

Teledyne FLIR LLC

MKS Instruments Inc.

Zeeco Inc.

Endress+Hauser Group

Fluenta AS

Who should buy this report?

The Flare Monitoring Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Flare Monitoring Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Flare Monitoring Market

Get Free Sample For Flare Monitoring Market