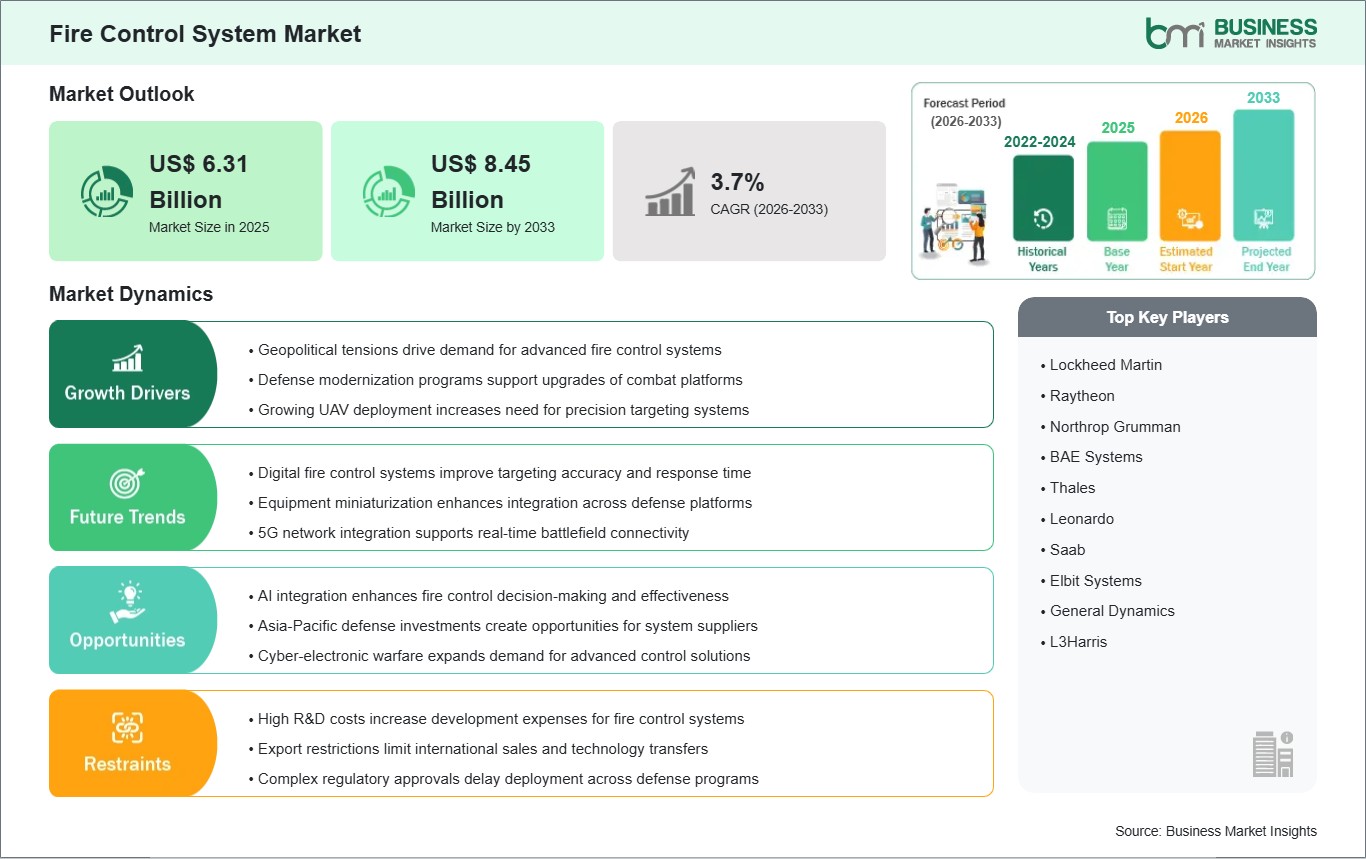

The fire control system market size is expected to reach US$ 8.45 billion by 2033 from US$ 6.31 billion by 2025. The market is estimated to record a CAGR of 3.7% during 2026 to 2033.

Executive Summary and Global Market Analysis:

Fire control systems refer to integrated defense platforms that compute targeting solutions, coordinate weapon deployment, and enhance engagement precision across military operations. The systems are made up of a sensor suite, tracking device, and computing unit. The use of such systems is widespread in both land and sea warfare scenarios as well as aerial warfare missions where the importance of coordinated firing cannot be overlooked.

The increasing number of military modernization programs is driving the adoption of technology by the armed forces of the world. Militaries have been working on advanced targeting mechanisms in order to increase efficiency and decrease the reaction time in the event of any engagement. The increasing emphasis on situational awareness and effective coordination on battlefields has also boosted procurement efforts.

Patterns of demand differ according to different system categories, platforms, and needs. The target acquisition module helps in identifying threats through the use of cutting-edge sensory devices. Ballistics systems make it possible to engage in firing calculations despite changes in circumstances, while navigational modules make sure that positioning is achieved at all times when attacking. Land-based systems involve integration with armored vehicles, while sea-based systems are characterized by maritime precision.

Changes are being introduced by technology to the performance of systems through sensor fusion, digital fire networks, and automatic targeting systems. The use of radar, electro-optics, and intelligent machines improves decision-making accuracy in real time. Contemporary system designs stress the importance of interoperability among military assets, which facilitates joint operations between various entities.

Fire Control System Market - Strategic Insights:

Get more information on this report

Fire Control System Market Segmentation Analysis:

The fire control system market is segmented based on type, platform, and end-user, reflecting increasing emphasis on precision targeting, real-time battlefield coordination, and integrated defense operations across multi-domain military environments.

By Type

Target Acquisition - Enables detection and tracking of targets using advanced sensing technologies.

Ballistics - Computes firing solutions to enhance accuracy under dynamic combat conditions.

Navigation - Supports positional accuracy and targeting alignment across operational missions.

By Platform

Land - Integrated into armored vehicles and artillery systems for ground combat precision.

Naval - Enhances targeting accuracy in ship-based weapon and maritime defense systems.

Airborne - Provides rapid targeting support for aircraft engaged in high-speed operations.

By End Use

Defense - Primary user segment focused on military modernization and combat readiness.

Homeland Security - Utilized for surveillance-driven response and tactical threat management.

Fire Control System Market Drivers and Opportunities:

Rising geopolitical tensions

Increasing geopolitical uncertainties are encouraging defense organizations to strengthen operational readiness and targeting precision capabilities. There is an increasing use of fire control technologies in military organizations that aims at increasing reaction times and preventing engagement mistakes during the performance of vital missions. There is an increasing demand for fire control technologies in military modernization processes that emphasize precision targeting and synchronization.

Security considerations continue to shape procurement processes that are geared towards multi-domain defense systems. This trend is associated with investments in technology that facilitates improved awareness on the battlefield and efficient neutralization of threats. Fire control systems play an important role in military preparations due to their capacity to assist in the coordination and accuracy of weapons deployment.

Integration with AI systems

Artificial intelligence integration is transforming fire control systems through automated target recognition and predictive engagement capabilities. AI-based components analyze sensor inputs in order to improve target accuracy and decrease dependence on operators. The use of such tools facilitates quicker decision making through the analysis of the battlefield situation. In combination with state-of-the-art sensors and digital networking, it increases responsiveness and effectiveness.

Expansion in the future seems to be inevitable due to increased utilization of AI-based defense architecture. There will be better automation and data fusion, which will enable greater coordination among the different systems during multi-platform attacks. The increased implementation of such fire control methods in modern warfare is being made possible by growing implementation of network-based defense architectures.

Fire Control System Market Size and Share Analysis:

The fire control system market size is expected to reach US$ 8.45 billion by 2033 from US$ 6.31 billion by 2025. The market is estimated to record a CAGR of 3.7% during 2026 to 2033. Market expansion is supported by increasing defense modernization programs, rising demand for precision engagement capabilities, and continuous upgrades of integrated combat systems across land, naval, and airborne platforms worldwide. Growing emphasis on network-centric warfare is further strengthening adoption across global military forces.

By Type, target acquisition systems account for a dominant share due to their critical role in identifying and tracking threats in real time. Ballistics systems hold a significant position as they enhance firing accuracy through advanced computation, while navigation systems support operational precision across multi-platform defense environments.

By Platform, land-based systems lead the market owing to widespread deployment in armored vehicles and artillery units. Naval platforms maintain strong relevance through advanced ship-based targeting systems, while airborne platforms are expanding steadily with increasing integration of high-speed precision engagement technologies in modern aircraft systems.

By End-User, defense applications dominate the market due to large-scale procurement of advanced fire control solutions for military modernization initiatives. Homeland security applications continue to expand as agencies invest in surveillance-enabled targeting systems and rapid response capabilities to enhance national security and threat mitigation effectiveness.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Lockheed Martin

Raytheon

Northrop Grumman

BAE Systems

Thales

Leonardo

Saab

Elbit Systems

General Dynamics

L3Harris

Get more information on this report

Fire Control System Market Report Coverage and Deliverables:

The "Fire Control System Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all key market segments covered under the scope

Market trends, along with market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key trends, global and regional frameworks, major players, regulations, and recent developments

Industry landscape and competitive analysis covering market concentration, heat map analysis, prominent players, and recent developments

Detailed company profiles, including SWOT analysis

Fire Control System Market Geographic Insights:

The Fire Control System Market shows diverse regional adoption patterns influenced by defense modernization programs, geopolitical conditions, technological advancement levels, and military procurement strategies. Across global regions, armed forces are increasingly integrating advanced targeting and control systems to enhance operational precision and multi-domain coordination. The growing complexity of modern warfare is encouraging adoption of integrated fire control solutions across defense platforms.

North America demonstrates strong adoption driven by advanced defense infrastructure and continuous military technology upgrades. Defense agencies in the region focus on integrating high-precision targeting systems across land, naval, and airborne platforms. Strong emphasis on digital battlefield systems and interoperability further supports deployment across multiple defense applications, strengthening operational effectiveness and mission coordination capabilities.

In Asia Pacific, the rise in usage can be attributed to increasing defense expenditures and development of military capabilities. Nations in the region are developing fire control systems to increase the efficiency of their border security and military preparedness. Increased emphasis on indigenously produced and integrated systems is adding impetus to the usage of fire control systems.

Europe maintains steady adoption driven by defense collaboration programs and modernization initiatives across member states. Emerging markets in the Middle East, Africa, and Latin America are gradually increasing procurement of advanced targeting systems as security requirements intensify. Growing emphasis on tactical readiness and surveillance-driven defense strategies continues to support market expansion across these regions.

Get more information on this report

Fire Control System Market Research Report Guidance:

The report includes qualitative and quantitative data in the Fire Control System Market across type, platform, end-user, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by type, platform, end-user, and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Fire Control System Market News and Key Development:

The fire control system market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In June 2026, Allen Control Systems announced that it raised $200 million in a Series B funding round led by Smash Capital, to scale its autonomous fire control and weapon station systems, including its AI-enabled "Bullfrog“ platform for defense applications.

In June 2026, Fire Point announced that it successfully tested its FP-7.X missile system, intended as part of a next-generation air defense fire control and interceptor system ("Freyja“), aimed at improving ballistic missile engagement capability in Europe.

Key Sources Referred:

S. Department of DefenseNATO Defence ReportsStockholm International Peace Research Institute (SIPRI)Jane‘s Defence Industry PublicationsEuropean Defence Agency ReportsIndian Ministry of Defence PublicationsAerospace and defense engineering journalsGovernment procurement and military modernization databases

The List of Companies - Fire Control System Market

Lockheed Martin

Raytheon

Northrop Grumman

BAE Systems

Thales

Leonardo

Saab

Elbit Systems

General Dynamics

L3Harris

Frequently Asked Questions

How big is the Fire Control System Market?

The Fire Control System Market is valued at US$ 6.31 Billion in 2025, it is projected to reach US$ 8.45 Billion by 2033.

What is the CAGR for Fire Control System Market by (2026 - 2033)?

As per our report Fire Control System Market, the market size is valued at US$ 6.31 Billion in 2025, projecting it to reach US$ 8.45 Billion by 2033. This translates to a CAGR of approximately 3.7% during the forecast period.

What segments are covered in this report?

The Fire Control System Market report typically cover these key segments-

Type (Target Acquisition, Ballistics, Navigation)

Platform (Land, Naval, Airborne)

End-User (Defense, Homeland Security)

What is the historic period, base year, and forecast period taken for Fire Control System Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Fire Control System Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Fire Control System Market?

The Fire Control System Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Lockheed Martin

Raytheon

Northrop Grumman

BAE Systems

Thales

Leonardo

Saab

Elbit Systems

General Dynamics

L3Harris

Who should buy this report?

The Fire Control System Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Fire Control System Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Fire Control System Market

Get Free Sample For Fire Control System Market