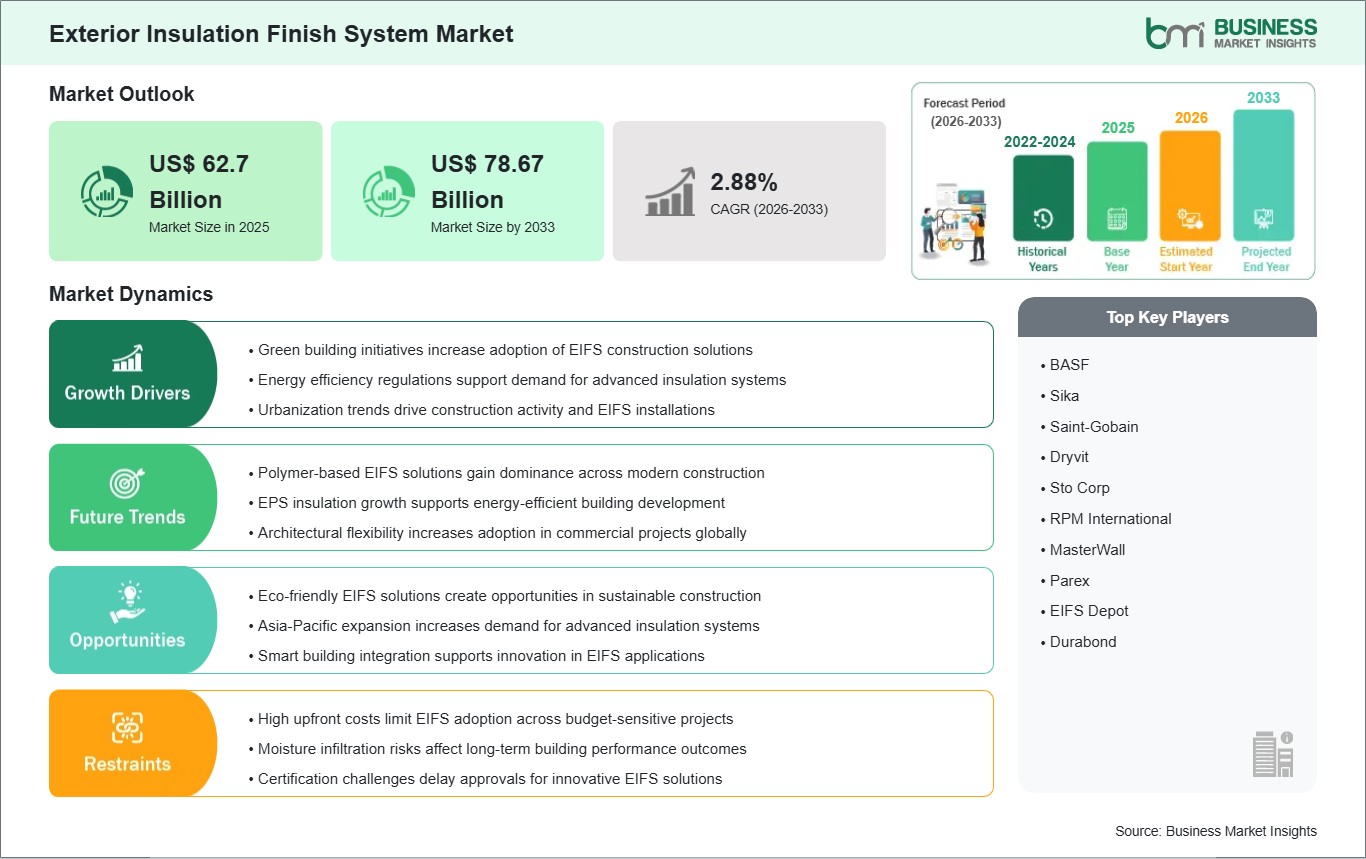

The exterior insulation finish system market size is expected to reach US$ 78.67 billion by 2033 from US$ 62.7 billion in 2025. The market is estimated to record a CAGR of 2.88% during 2026 to 2033.

Executive Summary and Global Market Analysis:

The systems of exterior insulation offer improved strength and increased function of existing structures by having the ability to insulate up to a quarter of the thermal resistance required by many types of exterior construction. The design of the insulation, combined with exterior weather protection, keeps exterior walls cool during the summer months and warm during the winter. In addition to providing thermal insulation, they also provide a weatherproof, low-maintenance and aesthetically pleasing surface to add value to any existing structure.

Most contemporary building codes will require compliance with the latest version of the International Building Code (IBC). In recent years, some types of exterior coatings have been developed specifically for use as an exterior insulation finish system (EIFS). These newer EIFS coatings have increased sealing properties and strength over older versions. As a result of architectural demand for lightweight cladding systems with reduced structural loads while also maintaining thermal stability, many residential towers, commercial complexes and institutional buildings are undergoing renovation or upgrades that are driven by energy efficiency requirements.

Material segmentation identifies performance priorities based on building environments and construction requirements for exterior building envelopes. Flexible facade system design incorporates polymer-based systems that provide flexibility and weather resistance, while fire-rated walls are generally constructed using mineral wool-based systems. Much of the material usage in the residential sector is due to housing modifications and insulation retrofits, while commercial improvement projects and institutional mandates for energy compliance have resulted in an increase in the use of these materials in non-residential buildings.

Material engineering advances to improve durability, moisture resistance and/or precision of installation have led to the improvement of pre-fabricated insulation panels and adhesive technologies, which have streamlined the application of insulation on-site and reduced timelines associated with construction. The use of digital modeling tools, designed to model the thermal performance of facades before the installation of those materials, has further improved the accuracy of facade designs. Collectively, these advancements are helping to increase the implementation of insulation systems in a variety of building construction contexts, thus establishing the longer-term relevance of insulation systems with respect to the design of building envelopes in the construction sector.

Exterior Insulation Finish System Market - Strategic Insights:

Get more information on this report

Exterior Insulation Finish System Market Segmentation Analysis:

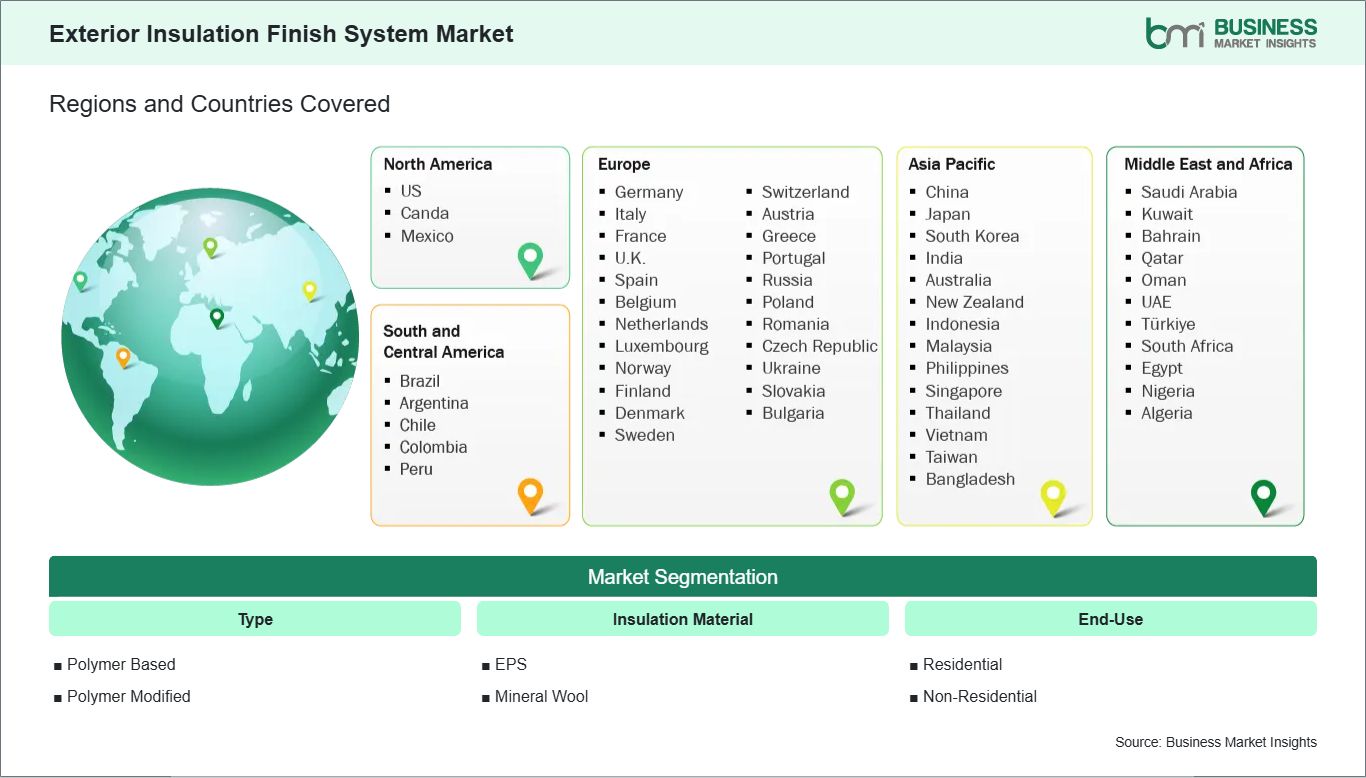

The exterior insulation finish system market is segmented by type, insulation material, and end-use, reflecting varying performance requirements and installation needs across building envelope applications.

By Type

Polymer Based - Flexible exterior coating systems for varied façade applications

Polymer Modified - Enhanced durability formulations with improved adhesion performance

By Insulation Material

EPS - Lightweight insulation with cost-efficient thermal performance characteristics

Mineral Wool - Fire-resistant insulation suitable for high-safety construction environments

By End-Use

Residential - Large-scale housing insulation upgrades and renovation projects

Non-Residential - Commercial and institutional façade modernization applications

Exterior Insulation Finish System Market Drivers and Opportunities:

Green building initiatives

Policy frameworks promoting energy-efficient construction have strengthened the adoption of exterior insulation systems across global building projects. Governments and urban planning bodies are tightening energy performance standards for buildings, encouraging developers to improve thermal envelope efficiency. Exterior insulation finish systems provide a practical method to reduce heat loss without requiring major structural redesign, making them suitable for both new construction and retrofit applications. Their compatibility with diverse façade designs further supports integration into modern architectural planning.

Material selection practices in the residential, commercial, and institutional building sectors are changing due to government regulations that have led to increased incorporation of insulation systems in the design phase to meet the certifications required for these systems, as well as achieving energy performance goals over the life of the building. In addition, the continual push for lower energy usage in buildings has led to the greater use of building envelope insulation in larger urban redevelopment projects. Insulation systems for façades are now considered a standard expectation for construction projects. Construction project participants are developing their projects in accordance with sustainability-related mandates. The continued movement toward green building compliance will also have an impact on supply chain practices and project evaluation processes, with builders and designers giving priority to insulation systems that have the potential to provide measurable improvements in thermal performance while providing savings from an economic perspective.

Eco-friendly EIFS

Eco-friendly exterior insulation finish systems are gaining attention due to increasing emphasis on reducing environmental impact across the construction value chain. Manufacturers are focusing on developing insulation materials that incorporate recyclable components, low-emission binders, and reduced volatile organic compound content. These improvements aim to lower the environmental footprint of building envelopes while maintaining strong thermal insulation performance. Such innovations are increasingly aligned with sustainable construction certification requirements and environmental compliance frameworks.

Innovation of new material types is aimed at improving the performance of these products throughout their life cycles as well as to improve their long-term durability, water resistance and ability to be recycled. New product formulations have been developed to minimize upkeep requirements while increasing their longevity, thereby improving the use of resources. Such innovations will have particular implications for large-scale residential and commercial developments, as assessing the long-term environmental impact of these methods will become a significant factor in decision making. As the adoption of green building codes becomes more widespread globally, future uses of these products are expected to increase. Institutional and commercial buildings are expected to be the primary drivers of this change, given that they will face the greatest amount of pressure to be compliant with increasingly stringent building codes. This trend will lead to greater emphasis on environmental factors in the design and planning of a construction project and will allow EIFS products as a group to play a leading role in the development of next generation facade systems.

Exterior Insulation Finish System Market Size and Share Analysis:

The exterior insulation finish system market size is expected to reach US$ 78.67 billion by 2033 from US$ 62.7 billion in 2025. The market is estimated to record a CAGR of 2.88% during 2026 to 2033.

By type, polymer-based systems hold a significant position due to their installation flexibility and compatibility with diverse facade designs. Polymer modified variants maintain steady utilization in projects requiring enhanced adhesion and weather resistance performance. Both segments continue gaining traction as construction stakeholders prioritize facade durability and thermal efficiency across varying climatic conditions and building structures.

By insulation material, EPS accounts for substantial demand driven by cost efficiency and lightweight thermal insulation characteristics in residential construction. Mineral wool maintains strong adoption in fire-sensitive applications where higher safety compliance and acoustic insulation performance are required. Material selection trends remain closely linked to building regulations, climatic exposure levels, and long-term energy efficiency targets across construction projects.

By end-use, residential applications dominate deployment due to large-scale housing renovation programs and energy efficiency upgrades in urban developments. Non-residential structures show consistent adoption supported by commercial façade modernization and institutional infrastructure improvements. Increasing focus on reducing building energy consumption continues to influence material integration decisions across both segments, strengthening demand stability in the overall market.

Exterior Insulation Finish System Market Report Highlights:

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

BASF

Sika

Saint-Gobain

Dryvit

Sto Corp

RPM International

MasterWall

Parex

EIFS Depot

Durabond

Get more information on this report

Exterior Insulation Finish System Market Report Coverage and Deliverables:

The "Exterior Insulation Finish System Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all key market segments covered under the scope

Market trends, along with market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key trends, global and regional frameworks, major players, regulations, and recent developments

Industry landscape and competitive analysis covering market concentration, heat map analysis, prominent players, and recent developments

Detailed company profiles, including SWOT analysis

Exterior Insulation Finish System Market Geographic Insights:

The exterior insulation finish system market shows diverse regional adoption patterns influenced by building energy efficiency mandates, construction modernization trends, and varying climatic insulation requirements across geographies. Regulatory enforcement levels, construction quality standards, and material accessibility significantly shape the pace and scale of system deployment in different regions. Urban redevelopment activities and retrofit programs further contribute to uneven but steadily expanding adoption across global construction markets.

North America demonstrates structured adoption supported by stringent energy codes and consistent renovation-driven construction activity. Demand is reinforced by strong preference for high-performance facade systems in residential upgrades, commercial building retrofits, and institutional infrastructure improvements. The region's focus on reducing building energy consumption has encouraged early integration of exterior insulation systems in both private and public sector projects. Material innovation and compliance with certification frameworks continue to influence specification choices across urban construction developments.

Asia Pacific reflects expanding construction momentum supported by large-scale housing projects, rapid urbanization, and increasing infrastructure investments. Rising energy optimization priorities are encouraging broader integration of facade insulation systems in both high-rise and low-rise developments. Manufacturers in the region emphasize scalable, cost-effective solutions suitable for diverse climatic zones ranging from humid coastal areas to colder inland regions. Growing awareness of building energy performance is further strengthening system adoption across emerging urban centers and industrial corridors.

Europe maintains strong alignment with sustainability-driven construction policies and strict building performance regulations. High emphasis on carbon reduction targets and energy-efficient building envelopes supports sustained demand for exterior insulation solutions. Emerging markets within adjacent regions are gradually adopting these systems, supported by infrastructure modernization and urban development initiatives. Across these regions, adoption patterns remain closely tied to regulatory frameworks, construction quality upgrades, and long-term energy efficiency objectives in the built environment.

Get more information on this report

Exterior Insulation Finish System Market Research Report Guidance:

The report includes qualitative and quantitative data in the Exterior Insulation Finish System Market across type, insulation material, end-use, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by type, insulation material, end-use, and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Exterior Insulation Finish System Market News and Key Development:

The exterior insulation finish system market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In March 2026, Sika Corporation, announced that it entered a strategic collaboration with Georgia-Pacific Building Products to launch an integrated EIFS solution featuring the DensElement Barrier System, aimed at improving weather resistance, installation efficiency, and building envelope performance across commercial construction projects.

In January 2025, Sto SE & Co. KGaA, announced that it had expanded its StoTherm external wall insulation system portfolio with upgraded fire-resistant insulation boards designed to improve façade safety and thermal performance in high-rise buildings.

Key Sources Referred:

International Energy Agency (IEA) building efficiency publicationsS. Department of Energy building envelope studiesEuropean Commission energy performance of buildings directivesASTM International façade material standards documentationJournal of Building Engineering research papersWorld Bank construction and urban development reportsIndustry whitepapers on exterior insulation technologiesGlobal construction material market outlook publications

The List of Companies - Exterior Insulation Finish System Market

BASF

Sika

Saint-Gobain

Dryvit

Sto Corp

RPM International

MasterWall

Parex

EIFS Depot

Durabond

Frequently Asked Questions

How big is the Exterior Insulation Finish System Market?

The Exterior Insulation Finish System Market is valued at US$ 62.7 Billion in 2025, it is projected to reach US$ 78.67 Billion by 2033.

What is the CAGR for Exterior Insulation Finish System Market by (2026 - 2033)?

As per our report Exterior Insulation Finish System Market, the market size is valued at US$ 62.7 Billion in 2025, projecting it to reach US$ 78.67 Billion by 2033. This translates to a CAGR of approximately 2.88% during the forecast period.

What segments are covered in this report?

The Exterior Insulation Finish System Market report typically cover these key segments-

Type (Polymer Based, Polymer Modified)

Insulation Material (EPS, Mineral Wool)

End-Use (Residential, Non-Residential)

What is the historic period, base year, and forecast period taken for Exterior Insulation Finish System Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Exterior Insulation Finish System Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Exterior Insulation Finish System Market?

The Exterior Insulation Finish System Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

BASF

Sika

Saint-Gobain

Dryvit

Sto Corp

RPM International

MasterWall

Parex

EIFS Depot

Durabond

Who should buy this report?

The Exterior Insulation Finish System Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Exterior Insulation Finish System Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Exterior Insulation Finish System Market

Get Free Sample For Exterior Insulation Finish System Market