Analysis- by Type (Group 1, Group 2, Group 3, Group 4, and Group 5), Application (ISR, Warfare, and Others), Range (Short Range, Medium Range, and Long Range), and Technology (Fixed Wing and Rotary Wing)

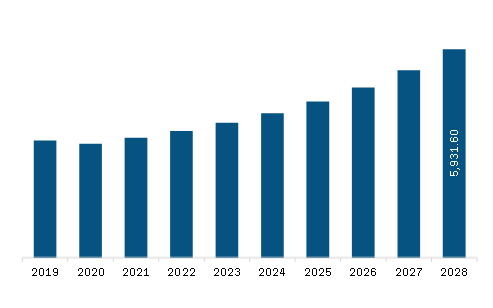

The Europe military drones market is expected to grow from US$ 3,834.49 million in 2023 to US$ 5,931.60 million by 2028. It is estimated to grow at a CAGR of 9.1% from 2023 to 2028.

Surge in Global Defense Sector Fuels Europe Military Drones Market

Changes in the modern warfare system have been urging governments across the region to allocate higher funds for respective military forces. Budget allocation enables military forces to procure advanced technologies and equipment from domestic or international manufacturers. On the same lines, soldier and military vehicle modernization practices are also on the rise across numerous countries. With the growing need to strengthen military forces with advanced technologies, armaments, artilleries, and vehicles, among others, defense forces across the world are investing substantial amounts in the aforementioned products. A continuous urge to deploy new technologies in combat and non-combat operations by the defense forces is further boosting defense spending.

Asymmetric warfare or modern battlefields demand enormous information to carry out operations successfully. Fiscal budgets, nowadays, are focused on robotic platforms and related technologies, contributing to the development and procurement of military drones.

According to the European Union (EU) data published in December 2022, defense sector spending in the EU reached US$ 242 billion (EUR 214 billion) in 2021, recording an increase of 6% compared to 2020. Such a rise in the defense sector contributes to the adoption of many technologies and weapons to strengthen the country’s defense and security. According to January 2023 updates from Ukraine's Defense Minister Oleksiy Reznikov, the country is planning to invest US$ 550 million in the procurement of drones in 2023. The government has signed 16 supply deals with Ukrainian drone manufacturers. Thus, such investments and initiatives by different country governments in their defense sectors contribute to the proliferation of the military drones market.

Europe Military Drones Market Overview

Based on country, the Europe military drones market is segmented into France, Germany, Italy, the UK, Russia, and the Rest of Europe. The government authorities in Europe are introducing new rules for military drones. According to a news article by the European Commission in January 2023, new European Union (EU) rules focused on establishing a dedicated airspace for drones—U-space—were enforced, allowing operators to provide a broader range of services. This space creates a condition for drones to operate in a safe environment and further allows for the scaling up of the drone industry and services. These rules will help improve military drones' performance by carrying out complex, long-distance operations. These rules are also focused on the technological development of drones under Drone Strategy 2.0 and support the full implementation of the U-space by 2030. Further, in May 2022, Indian government conducted Bharat Drone Mahotsav 2022 to promote the use of drone technologies in defense. Such government initiatives will contribute to the adoption and technological development of military drones, propelling the market growth.

European countries are investing in military drones to strengthen national security. For instance, according to Italy's budgetary plan for 2021, the Ministry of Defense is scheduled to invest ~US$ 63 million over 7 years to arm Italy's Reaper drones. In addition, under the Eurodrone project, European countries such as Italy, Germany, Spain, and France got the green light to develop 20 Medium-Altitude and Long-Endurance (MALE) drones to compete against Israel and US-made UAVs. In January 2022, Pedro Sanchez, the Prime Minister of Spain, agreed to authorize an investment of US$ 1.98 billion (EUR 1.75 billion) for the partnership between Italy, Germany, Spain, and France to develop Europe's largest military drone, where Leonardo, a top global player for the drone technology, will provide drone parts for Europe military. All these factors are fueling the growth of the market.

Europe Military Drones Market Revenue and Forecast to 2028 (US$ Million)

Europe Military Drones Market Segmentation

The Europe military drones market is segmented into type, application, range, technology, and country.

Based on type, the Europe military drones market is segmented into group 1, group 2, group 3, group 4, and group 5. The group 5 segment held the largest share of the Europe military drones market in 2023.

Based on application, the Europe military drones market is segmented into ISR, warfare, and others. The ISR segment held the largest share of the Europe military drones market in 2023.

Based on range, the Europe military drones market is segmented into short range, medium range, and long range. The medium range segment held the largest share of the Europe military drones market in 2023.

Based on technology, the Europe military drones market is segmented into fixed wing and rotary wing. The fixed wing segment held the larger share of the Europe military drones market in 2023.

Based on country, the Europe military drones market is segmented into France, Germany, Italy, the UK, Russia, and the Rest of Europe. The Russia dominated the share of the Europe military drones market in 2023.

AeroVironment Inc, BAE Systems Plc, Elbit Systems Ltd, General Atomics, Lockheed Martin Corp, Northrop Grumman Corp, Textron Systems Corp, Thales SA, The Boeing Co, and Israel Aerospace Industries Ltd. are the leading companies operating in the Europe military drones market.

Europe Military Drones Market Strategic Insights

Get more information on this report

Europe Military Drones Market Segmentation Analysis

Europe Military Drones Market Report Highlights

Europe Military Drones Report Scope

Report Attribute

Details

Market size in 2023

US$ 3,834.49 Million

Market Size by 2028

US$ 5,931.60 Million

CAGR (2023 - 2028)

9.1%

Historical Data

2021-2022

Forecast period

2024-2028

Segments Covered

By Type

Group 1

Group 2

Group 3

Group 4

Group 5

By Application

ISR

Warfare

By Range

Short Range

Medium Range

Long Range

By Technology

Fixed Wing

Rotary Wing

Regions and Countries Covered

Europe

UK, Germany, France, Russia, Italy, Rest of Europe

Market leaders and key company profiles

AeroVironment Inc

BAE Systems Plc

Elbit Systems Ltd

General Atomics

Lockheed Martin Corp

Northrop Grumman Corp

Textron Systems Corp

Thales SA

The Boeing Co

Israel Aerospace Industries Ltd

Get more information on this report

Europe Military Drones Market Country and Regional Insights

Get more information on this report

Identical Market Reports with other Region/Countries

The List of Companies - Europe Military Drones Market

AeroVironment Inc BAE Systems Plc Elbit Systems Ltd General Atomics Lockheed Martin Corp Northrop Grumman Corp Textron Systems Corp Thales SA The Boeing CoIsrael Aerospace Industries Ltd

Frequently Asked Questions

How big is the Europe Military Drones Market?

The Europe Military Drones Market is valued at US$ 3,834.49 Million in 2023, it is projected to reach US$ 5,931.60 Million by 2028.

What is the CAGR for Europe Military Drones Market by (2023 - 2028)?

As per our report Europe Military Drones Market, the market size is valued at US$ 3,834.49 Million in 2023, projecting it to reach US$ 5,931.60 Million by 2028. This translates to a CAGR of approximately 9.1% during the forecast period.

What segments are covered in this report?

The Europe Military Drones Market report typically cover these key segments-

Type (Group 1, Group 2, Group 3, Group 4, Group 5)

Application (ISR, Warfare)

Range (Short Range, Medium Range, Long Range)

Technology (Fixed Wing, Rotary Wing)

What is the historic period, base year, and forecast period taken for Europe Military Drones Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Europe Military Drones Market report:

Historic Period : 2021-2022

Base Year : 2023

Forecast Period : 2024-2028

Who are the major players in Europe Military Drones Market?

The Europe Military Drones Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

AeroVironment Inc

BAE Systems Plc

Elbit Systems Ltd

General Atomics

Lockheed Martin Corp

Northrop Grumman Corp

Textron Systems Corp

Thales SA

The Boeing Co

Israel Aerospace Industries Ltd

Who should buy this report?

The Europe Military Drones Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Europe Military Drones Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Europe Military Drones Market

Get Free Sample For Europe Military Drones Market