01

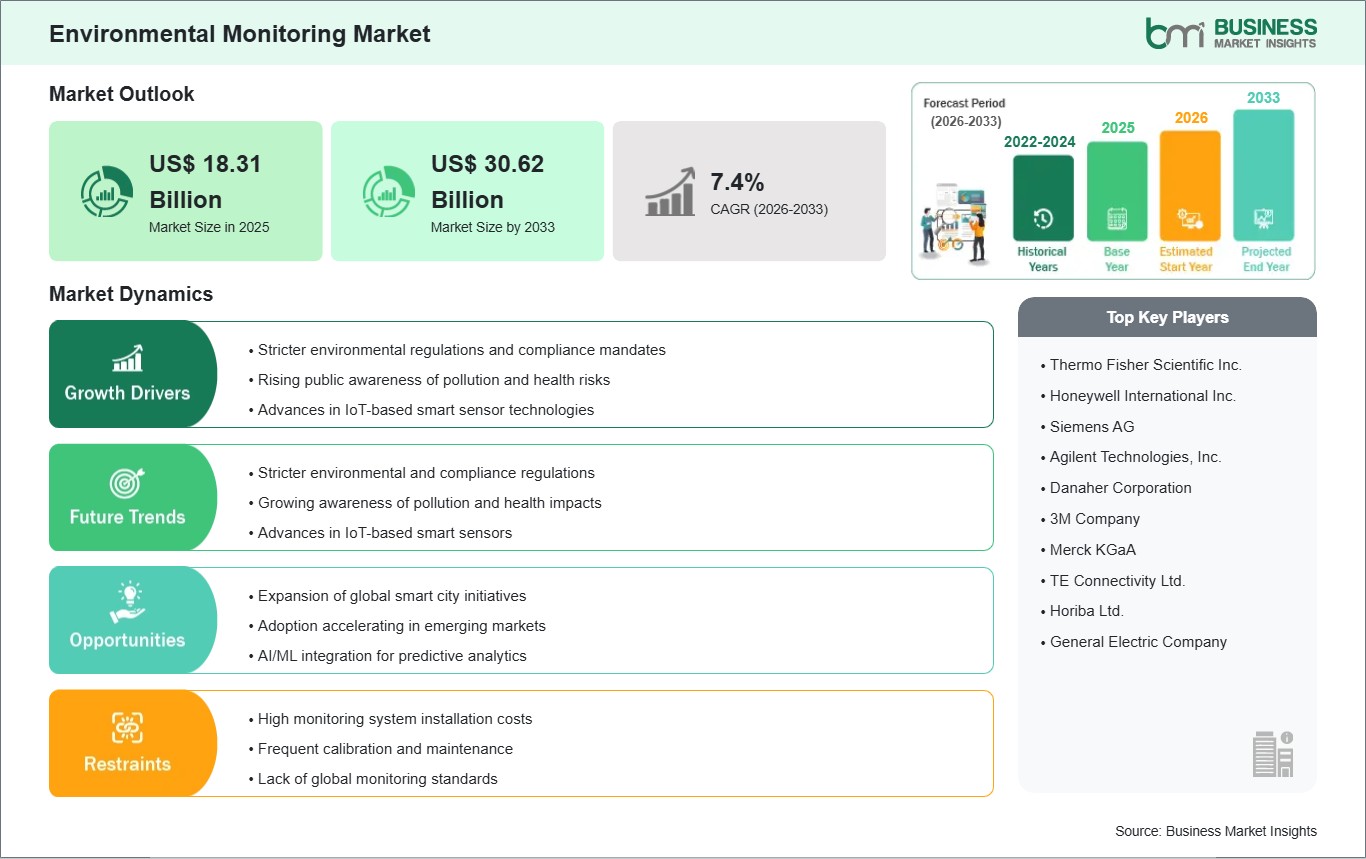

Market Summery

Executive Summary and Global Market Analysis

The global environmental monitoring market has emerged as a critical technological ecosystem dedicated to tracking, analyzing, and reporting environmental parameters across air, water, soil, and noise pollution. These systems employ a sophisticated array of hardware sensors, software platforms, and analytical services to measure particulate matter (PM2.5/PM10), greenhouse gases (CO2, CH4), volatile organic compounds (VOCs), and other pollutants. The market is experiencing robust growth propelled by escalating concerns about climate change, stringent government regulations worldwide, and rising public awareness about the adverse health effects of pollution. The integration of advanced technologies such as the Internet of Things (IoT), artificial intelligence (AI), and remote sensing has revolutionized environmental data collection, enabling real-time monitoring, predictive analytics, and more accurate environmental assessments. This technological evolution is empowering governments, industries, and communities to make data-driven decisions for environmental protection and sustainable development.

However, the market faces significant challenges, including the high initial capital costs associated with deploying comprehensive monitoring infrastructure, particularly in developing economies with limited resources. The complexity of system integration, the need for specialized technical personnel for operation and maintenance, and the lack of standardized data collection protocols across different regions also pose substantial hurdles. Despite these constraints, compelling opportunities emerging from rapid industrialization across Asia-Pacific and Africa, the expansion of smart city initiatives worldwide, and the development of AI-powered analytics that transform raw environmental data into actionable intelligence for predictive pollution modeling and proactive mitigation strategies.

03

Segment Analysis

Environmental Monitoring Market Segmentation

Key segments that contributed to the derivation of the environmental monitoring market analysis are component, monitoring type, sampling method, and end-user.

- By component, the market is segmented into hardware (sensors, monitors), software, and services. The hardware segment dominated the market in 2025, constituting the essential physical infrastructure for data acquisition through sensors and monitoring devices deployed across monitoring stations worldwide.

- By monitoring type, the market is categorized into air quality monitoring, water quality monitoring, soil monitoring, and noise monitoring. Air quality monitoring held the largest market share in 2025.

- By sampling method, the market is segmented into continuous monitoring, active monitoring, passive monitoring, and intermittent monitoring. Continuous monitoring is widely regarded as the dominant segment.

- By end-user, the market is segmented into government agencies, industrial sector, commercial & residential, and research & academic institutions. Government agencies and municipalities represented the largest end-user segment in 2025.

04

Market Forces

Environmental Monitoring Market Drivers and Opportunities

Stringent Environmental Regulations and Compliance Mandates

A primary driver for the environmental monitoring market is the increasingly rigorous global regulatory landscape mandating real-time emissions tracking and comprehensive environmental surveillance. International agreements like the Paris Agreement, coupled with regional directives such as the European Union's Industrial Emissions Directive and national legislation like the U.S. Clean Air Act amendments, compel industries and governments to implement robust monitoring systems. These regulations now mandate particulate matter and emissions monitoring across high-impact industries, driving a projected significant increase in compliance-related monitoring system deployments. The need to adhere to evolving environmental standards creates sustained, long-term demand for accurate, reliable, and certified monitoring solutions across all regulated sectors.

Smart City Initiatives and AI-Powered Analytics

A transformative opportunity lies in the convergence of environmental monitoring with smart city development and advanced data analytics. Municipal investments in IoT-based environmental sensing networks are transforming urban air quality management, with major cities worldwide deploying permanent sensor arrays integrated with 5G connectivity for real-time data transmission to centralized command centers. This urban digitization enables dynamic pollution response strategies and accounts for a substantial portion of environmental monitoring hardware sales. Furthermore, advanced machine learning algorithms are revolutionizing environmental data interpretation, enabling predictive pollution modeling with significantly greater accuracy than traditional methods. AI-powered analytics can identify emission patterns and recommend corrective actions before regulatory thresholds are exceeded, creating premium value-added services while reducing customer compliance risks.

05

Size and Share Analysis

Environmental Monitoring Market Size and Share Analysis

By component, hardware maintains the largest revenue share due to the continuous need for deploying and upgrading monitoring infrastructure globally, including sensors, monitors, and samplers. The software and data analytics platforms segment is the fastest-growing, driven by the imperative to process, visualize, and interpret vast datasets to generate actionable intelligence for decision-making and predictive analysis.

By monitoring type, air quality monitoring dominates the market, reinforced by the deployment of extensive monitoring networks in cities and industrial zones, supported by technological integration with IoT and cloud platforms. Water quality monitoring is the fastest-growing segment, driven by increasing concerns about water scarcity, industrial pollution, and the need for safe drinking water.

By sampling method, continuous monitoring leads due to its superior data granularity and reliability compared to intermittent sampling, making it indispensable for proactive environmental management. Passive and active monitoring methods maintain significant shares in specific applications, such as occupational exposure assessment and research studies.

By end-user, government agencies drive market standards and technological adoption, with initiatives often funded by public budgets aimed at achieving climate goals. The industrial sector, including manufacturing, oil & gas, and energy, represents a substantial and growing segment driven by compliance requirements and corporate sustainability initiatives.

07

Report Coverage

Environmental Monitoring Market Report Coverage and Deliverables

The "Environmental Monitoring Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Environmental Monitoring Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Environmental Monitoring Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Environmental Monitoring Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the environmental monitoring market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Environmental Monitoring Market Geographic Insights

The geographical scope of the environmental monitoring market report is divided into five regions: North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America. North America currently holds the largest market share, while Asia Pacific is projected to witness the highest growth rate during the forecast period.

North America, led by the United States, is the most technologically advanced and mature market, characterized by strong regulatory frameworks from agencies like the U.S. Environmental Protection Agency (EPA), significant investments in sustainability initiatives, and extensive deployment of monitoring infrastructure. The Clean Air Act and other stringent environmental regulations mandate comprehensive monitoring across industries, creating sustained demand.

Europe is a key player with stringent environmental directives and a strong emphasis on achieving carbon neutrality. The European Union's ambitious environmental targets and robust industrial monitoring practices drive adoption of advanced monitoring solutions across member states.

Asia Pacific is the fastest-growing regional market, fueled by rapid industrialization and urbanization, particularly in China, India, Japan, and Southeast Asian nations. Government-led initiatives to address severe pollution challenges, coupled with massive investments in smart city projects and expanding regulatory enforcement, are creating unprecedented demand for comprehensive environmental monitoring solutions.

South and Central America and the Middle East & Africa represent emerging markets with steady growth potential, supported by evolving environmental policies, improving technological capabilities, and increasing awareness of environmental issues. Countries like Brazil, Mexico, UAE, and South Africa are showing growing traction in monitoring technology investments.

10

Industry Activity

Recent Developments

The environmental monitoring market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the environmental monitoring market are:

- In February 2026, The Dickson Company announces the introduction today of Cobalt XS Wi-Fi, designed to simplify environmental monitoring in critical environments. Compact and intuitive, this launch expands the market leading Cobalt X/XS product line, delivering the power of Wi-Fi in an easy-to-use format with universal connectivity.

- In January 2026, Veeva Systems (NYSE: VEEV) announced a new environmental monitoring (EM) solution to advance quality control (QC) for manufacturing operations. Veeva Environmental Monitoring, a cloud-native application unified with Veeva LIMS, will enable laboratories and manufacturing facilities to schedule, collect, and analyze environmental samples to ensure compliance with GMP and internal sterility standards.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations