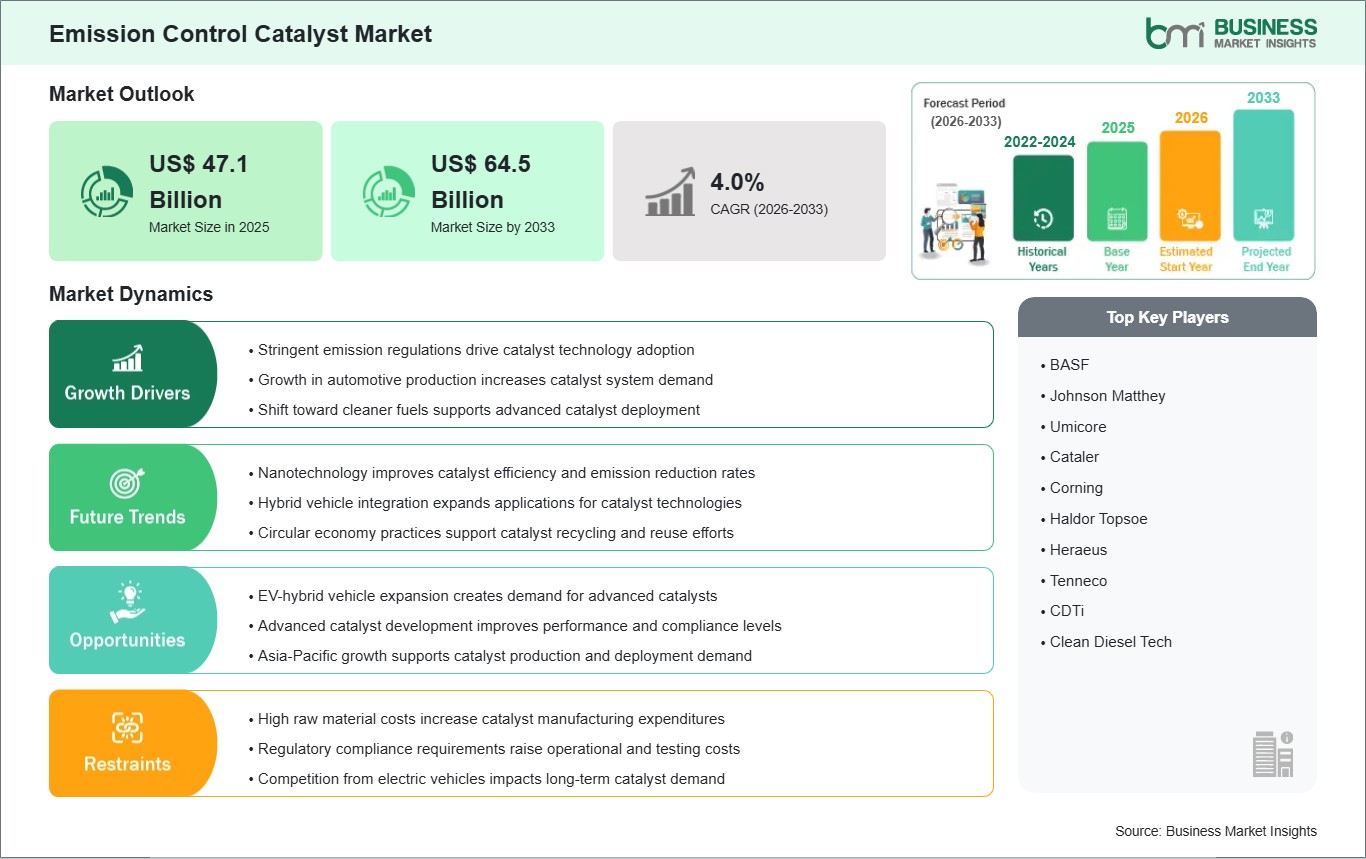

The emission control catalyst market size is expected to reach US$ 64.50 billion by 2033 from US$ 47.10 billion in 2025. The market is estimated to record a CAGR of 4.0% during 2026 to 2033.

Executive Summary and Global Market Analysis:

Emission control catalysts are specialized chemical compounds that act as agents to convert many of the harmful emissions that are created during the combustion of fuel into more environmentally friendly forms. Positioned within exhaust treatment systems, these catalysts also significantly reduce the amount of pollutants produced from vehicles, industrial equipment, and power generation equipment. Their use has been closely associated with efforts to enhance air quality and provide cleaner industrial processes.

As the transportation networks and industrial infrastructures continue to develop, the industry will continue to experience improvements from these advancements. As engines have advanced and environmental expectations have increased, many manufacturers now produce advanced catalyst technologies to continue producing acceptable emission levels regardless of the varied operating conditions. This movement has generated ongoing evolution of catalyst formulations, substrate configurations, and system integration.

The market has numerous types of catalysts available for different types of emissions. For gasoline-powered cars, three-way catalysts are still being extensively used today; for diesel engines, diesel oxidation catalysts and SCR catalysts provide solutions that are useful for diesel engines that operate on trucks and in the industrial setting. Passenger cars, commercial fleets, manufacturing plants and stationary power plants all contribute to demand for catalytic devices due to the critical importance they play in helping companies manage emissions successfully.

Catalytic technology is rapidly expanding its focus on increasing catalyst life, optimizing catalyst use and improving catalyst conversion rates at various temperatures. The industry is continuing to invest in new engineering-based technologies to accommodate the continually evolving regulatory environment and operational obstacles imposed on manufacturers. The means by which companies are able to differentiate themselves in competition is based upon their level of technological knowledge and expertise, as well as their ability to develop dependable products and deliver effective emission control solutions across numerous different types of end users.

Emission Control Catalyst Market - Strategic Insights:

Get more information on this report

Emission Control Catalyst Market Segmentation Analysis:

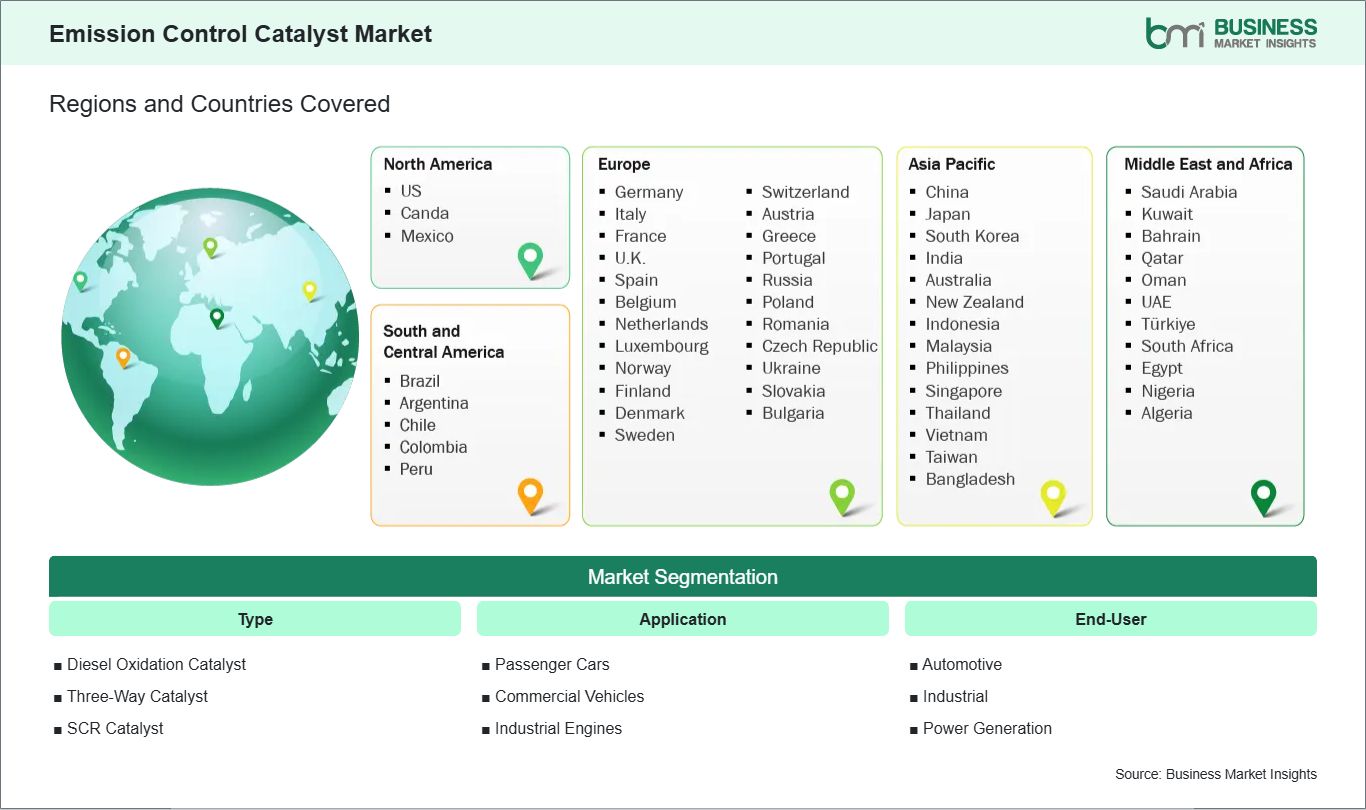

The emission control catalyst market is segmented by catalyst type, application, and end-user industry, reflecting diverse emission management requirements across combustion-based systems.

By Type

Diesel Oxidation Catalyst - Reduces hydrocarbon and carbon monoxide emissions from diesel exhaust streams.

Three-Way Catalyst - Simultaneously converts multiple pollutants in gasoline-powered engines.

SCR Catalyst - Facilitates nitrogen oxide reduction through selective chemical reactions.

By Application

Passenger Cars - Supports compliance across high-volume automotive production programs.

Automotive - Represents extensive catalyst integration across vehicle platforms.

Industrial - Utilizes aftertreatment technologies within manufacturing and processing equipment.

Power Generation - Controls emissions from combustion-based electricity production systems.

Emission Control Catalyst Market Drivers and Opportunities:

Stringent emission regulations

Governments and environmental agencies across the world are progressively tightening emission norms for transportation, industrial operations, and energy generation systems. These regulations are designed to reduce harmful pollutants such as nitrogen oxides, carbon monoxide, and particulate matter, which contribute to air quality degradation and climate-related impacts. To comply with these evolving standards, industries are increasingly adopting advanced exhaust treatment and emission control solutions that can achieve higher conversion efficiency while maintaining system durability and performance. This has led to greater emphasis on engineered catalyst technologies that enhance chemical reactions within exhaust systems and support cleaner output across a wide range of applications.

Compliance with regulations used to be limited to standard certification; it now affects many aspects of engineering including choice of materials, system design, and how systems are planned for the lifecycle. As part of the required performance of emission control systems, manufacturers must make certain that they remain operable when subjected to a variety of load conditions, temperature changes and long-term operational stress. This has led to ongoing innovation in the design of catalyst formulations and substrate types in order to provide improved performance and reliability. Stricter inspection regimes and the global harmonization of environmental standards are forcing manufacturers to find ways to ensure they perform consistently across all markets and, thus, have made emission control technologies central to the strategies companies use to develop sustainable industrially. By utilizing emission control technologies, companies can meet their environmental obligations while being productive and competitive in their respective regulated industries.

Expansion in EV-hybrid vehicles

The growing adoption of hybrid vehicles has created new technical requirements for emission management systems due to their dual reliance on internal combustion engines and electric propulsion. Unlike fully electric vehicles, hybrid platforms continue to generate exhaust emissions during engine operation, requiring efficient aftertreatment systems that can perform effectively under intermittent and variable usage patterns. This includes frequent engine start-stop cycles, fluctuating thermal conditions, and inconsistent load distribution, all of which place unique demands on catalyst performance and durability. Manufacturers are therefore focusing on developing more adaptive catalyst technologies that can maintain efficiency across a wider range of operating environments.

Hybridization has not only spurred innovation in the integration of powertrains but also fostered greater cooperation between combustion engines and electrical control units. Because of this coalescence of these systems, emission control components will need to be both thermally stable and compatible with continually changing vehicle software strategies. At the same time, regulation is continuing to evolve through the recognition of the different types of hybrid-specific emissions; this encourages continual development of aftertreatment solutions. As a growing share of the automobile market expands into both passenger and commercial hybrid vehicles, there has been an increased demand for optimized catalyst systems. Hybrid platforms will continue to comprise a large portion of the mobility spectrum as automobile manufacturers transition between traditional and fully electric mobility. Additionally, hybrid platforms will continue to improve the performance of new control technologies for emissions that can adapt to a variety of operational conditions and comply with various regional emission laws.

Emission Control Catalyst Market Size and Share Analysis:

The emission control catalyst market is projected to grow from US$ 47.10 billion in 2025 to US$ 64.50 billion by 2033, registering a CAGR of 4.0% from 2026 to 2033.

By type, the market is segmented into diesel oxidation catalyst, three-way catalyst, and scr catalyst. Three-way catalyst holds a dominant position due to its extensive use in gasoline-powered vehicles and its ability to simultaneously reduce carbon monoxide, hydrocarbons, and nitrogen oxide emissions. Its widespread integration across passenger vehicle platforms supports consistent utilization within automotive exhaust treatment systems. Diesel oxidation catalyst technologies remain important for controlling emissions from diesel engines, while SCR catalyst systems are increasingly utilized to achieve effective nitrogen oxide reduction in commercial vehicles, industrial equipment, and other heavy-duty applications.

By application, the market is categorized into passenger cars, commercial vehicles, and industrial engines. Passenger cars account for a significant share owing to large-scale vehicle production and the continuous implementation of stricter emission standards across global automotive markets. Manufacturers incorporate advanced catalyst systems to improve exhaust treatment efficiency and maintain regulatory compliance. Commercial vehicles represent a substantial segment due to fleet modernization initiatives and stringent emissions requirements for freight transportation. Industrial engines also contribute notably to market demand as operators deploy emission control technologies to meet environmental regulations and enhance operational performance.

By end-user, the market is segmented into automotive, industrial, and power generation. Automotive represents the leading end-user segment due to the extensive deployment of emission control catalysts across passenger and commercial vehicle platforms. Rising focus on cleaner transportation technologies and regulatory compliance continues to support catalyst integration throughout the automotive sector. Industrial end-users utilize catalyst systems to manage emissions from manufacturing and processing equipment, while the power generation segment incorporates emission control technologies to reduce pollutants from combustion-based energy production facilities and support environmental performance objectives.

Emission Control Catalyst Market Report Highlights:

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

BASF

Johnson Matthey

Umicore

Cataler

Corning

Haldor Topsoe

Heraeus

Tenneco

CDTi

Clean Diesel Tech

Get more information on this report

Emission Control Catalyst Market Report Coverage and Deliverables:

The "Emission Control Catalyst Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all key market segments covered under the scope

Market trends, along with market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key trends, global and regional frameworks, major players, regulations, and recent developments

Industry landscape and competitive analysis covering market concentration, heat map analysis, prominent players, and recent developments

Detailed company profiles, including SWOT analysis

Emission Control Catalyst Market Geographic Insights:

The emission control catalyst market shows diverse regional adoption patterns influenced by environmental legislation, industrial activity levels, vehicle production trends, and energy infrastructure requirements. Across global markets, emission reduction objectives continue to shape investment priorities, encouraging widespread utilization of advanced catalyst technologies. Regulatory alignment remains a primary consideration affecting purchasing decisions and technology deployment strategies throughout the sector.

North America demonstrates consistent demand supported by established emission compliance frameworks and ongoing modernization of transportation fleets. Automotive manufacturers and industrial operators continue implementing advanced exhaust treatment systems to align with environmental objectives. The region's focus on technology innovation and operational efficiency contributes to sustained utilization of catalyst-based emission reduction solutions.

Asia Pacific remains a significant market landscape due to extensive automotive manufacturing activities and expanding industrial operations. Urbanization, transportation demand, and environmental policy initiatives encourage broader implementation of emission control technologies. Regional manufacturers continue enhancing production capabilities while integrating catalyst systems into vehicles and industrial equipment designed for domestic and international markets.

Europe maintains a strong emphasis on emissions management through comprehensive environmental regulations and sustainability objectives. Automotive and industrial sectors continue investing in technologies that support lower pollutant outputs and improved environmental performance. Emerging markets across the Middle East, Africa, and South and Central America are progressively strengthening emission control frameworks, creating opportunities for catalyst deployment as industrial development and transportation infrastructure continue to evolve.

Get more information on this report

Emission Control Catalyst Market Research Report Guidance:

The report includes qualitative and quantitative data in the Emission Control Catalyst Market across type, application, end-user, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by type, application, end-user, and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Emission Control Catalyst Market News and Key Development:

The emission control catalyst market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In May 2026, Johnson Matthey announced the acquisition of Cormetech for approximately US$ 360 million, expanding its emissions-control catalyst portfolio for power generation, industrial facilities, and data centers, particularly technologies used to reduce NOx, CO, and VOC emissions.

In June 2025, Clariant announced that its ShiftMax™ 100 RE catalyst was selected for deployment at INERATEC's commercial-scale e-fuels facility in Germany, enabling efficient production of sustainable fuels with reduced emissions.

Key Sources Referred:

Industry emission control technology reportsGovernment environmental compliance publicationsAutomotive and industrial regulatory databasesPeer-reviewed environmental engineering journalsCompany annual reports and investor filingsAcademic studies on catalyst chemistryTechnical conference proceedingsSustainability and emissions policy documentation

The List of Companies - Emission Control Catalyst Market

BASF

JohnsonMatthey

Umicore

Cataler

Corning

HaldorTopsoe

Heraeus

Tenneco

CDTi

CleanDieselTech

Frequently Asked Questions

How big is the Emission Control Catalyst Market?

The Emission Control Catalyst Market is valued at US$ 47.1 Billion in 2025, it is projected to reach US$ 64.5 Billion by 2033.

What is the CAGR for Emission Control Catalyst Market by (2026 - 2033)?

As per our report Emission Control Catalyst Market, the market size is valued at US$ 47.1 Billion in 2025, projecting it to reach US$ 64.5 Billion by 2033. This translates to a CAGR of approximately 4.0% during the forecast period.

What segments are covered in this report?

The Emission Control Catalyst Market report typically cover these key segments-

Type (Diesel Oxidation Catalyst, Three-Way Catalyst, SCR Catalyst)

End-User (Automotive, Industrial, Power Generation)

What is the historic period, base year, and forecast period taken for Emission Control Catalyst Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Emission Control Catalyst Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Emission Control Catalyst Market?

The Emission Control Catalyst Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

BASF

Johnson Matthey

Umicore

Cataler

Corning

Haldor Topsoe

Heraeus

Tenneco

CDTi

Clean Diesel Tech

Who should buy this report?

The Emission Control Catalyst Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Emission Control Catalyst Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Emission Control Catalyst Market

Get Free Sample For Emission Control Catalyst Market