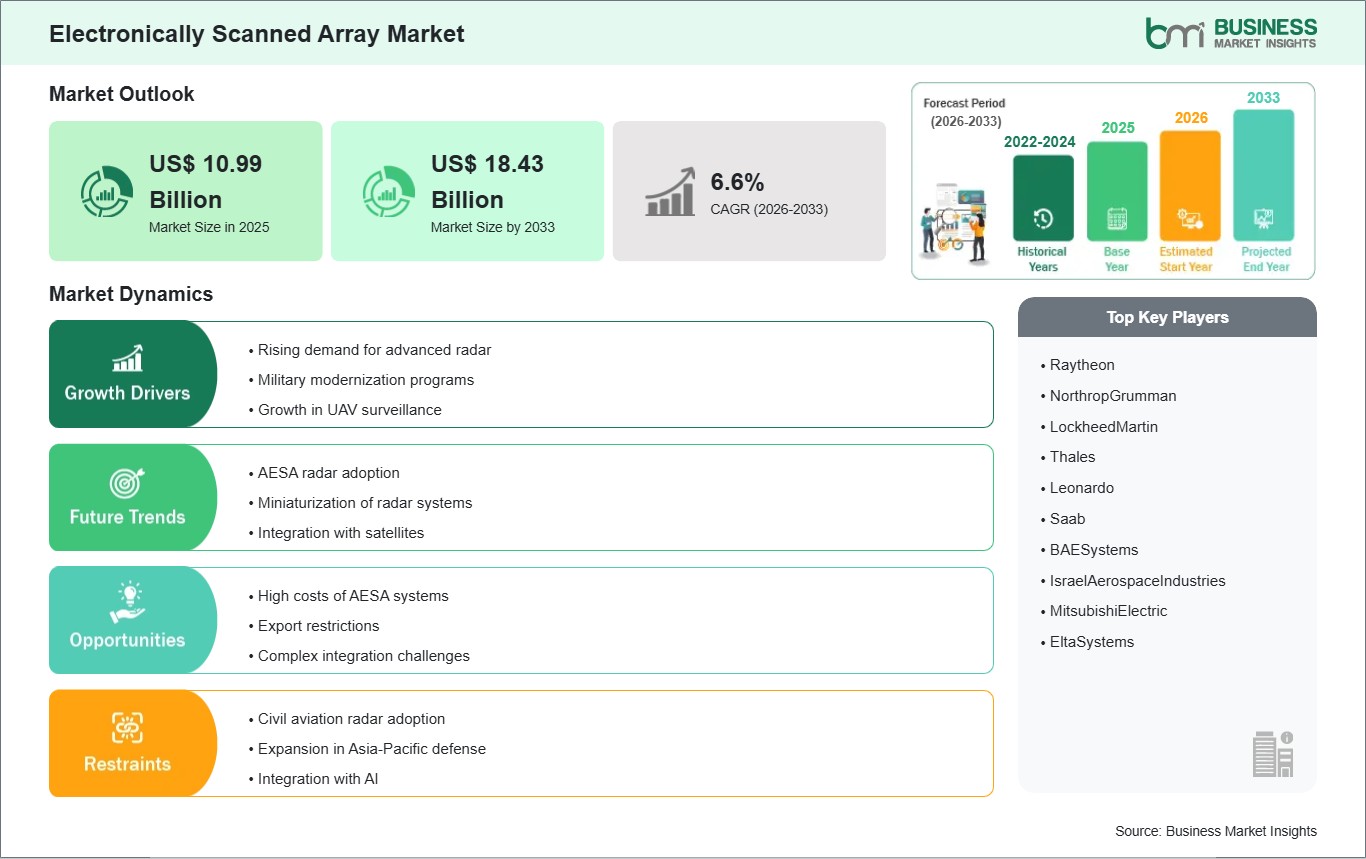

Rising demand for advanced radar

Modern defense operations are increasingly focused on achieving faster target detection, higher tracking precision, and improved situational awareness in complex and contested environments. Conventional mechanically scanned radar systems often face limitations when required to track multiple fast-moving airborne and surface threats simultaneously. These systems can struggle with slower beam steering, higher maintenance needs, and reduced adaptability in dynamic operational scenarios. In contrast, electronically scanned array (ESA) radars provide rapid, software-controlled beam steering, allowing near-instantaneous direction changes and continuous multi-target tracking. This makes them highly suitable for modern warfare environments where speed and accuracy are critical for mission success.

Besides the increased detection capabilities enabled by ESA radar, they play a significant role in integrated defense networks by providing support for engagement coordination, fire control, and electronic warfare capabilities. ESA radars are an important part of the modernization of contemporary military forces due to their capability to operate on air, land and sea platforms; their increased reliability; and low level of mechanical complexity. ESA radar technologies provide improved resilience against electronic countermeasures and, therefore, increase the chance of survival in hostile environments. Moreover, as many nations' defense forces are shifting from traditional defense to networked, multi-domain operations, demand for advanced radar technology is rising. Additionally, current investments in surveillance infrastructure and the changing nature of threats (hypersonic weapons, swarming drones) only reinforce the need for high-performance radar systems, thereby assuring continued use of electronically scanned array technology in future defense procurement.

Civil aviation radar adoption

The civil aviation sector is witnessing a steady shift toward advanced radar technologies as air traffic volumes continue to rise and operational environments become more complex. Traditional radar systems, while reliable, often face challenges in managing dense traffic scenarios efficiently. Electronically scanned array (ESA) radars offer a significant upgrade by enabling faster scanning speeds, improved tracking accuracy, and the ability to monitor multiple aircraft simultaneously without mechanical rotation. This makes them highly suitable for modern airport surveillance, en-route monitoring, and terminal airspace management where precision and responsiveness are critical for maintaining safety.

Additionally, the ESA radar technology and the ongoing digital transformation of Air Traffic Management (ATM) is closely aligned. Thanks to their capacity to interface with automated systems and real-time data platforms, ESA radar systems will enable improved coordination between aircraft, airports and Air Navigation Service Providers. The result will be enhanced situational awareness and decreased risks associated with runway incursions and mid-air collisions. Less mechanical complexity in ESA systems will produce lower maintenance needs, increased operational reliability, and is critical to enable continuous airport operations. As the industry moves forward, the increased adoption of ESA radar capabilities will be driven by the commitment of aviation authorities to invest in smart airport initiatives and next-generation ATM frameworks. Such investments will help make aviation ecosystems safer, more efficient and scalable across the globe.