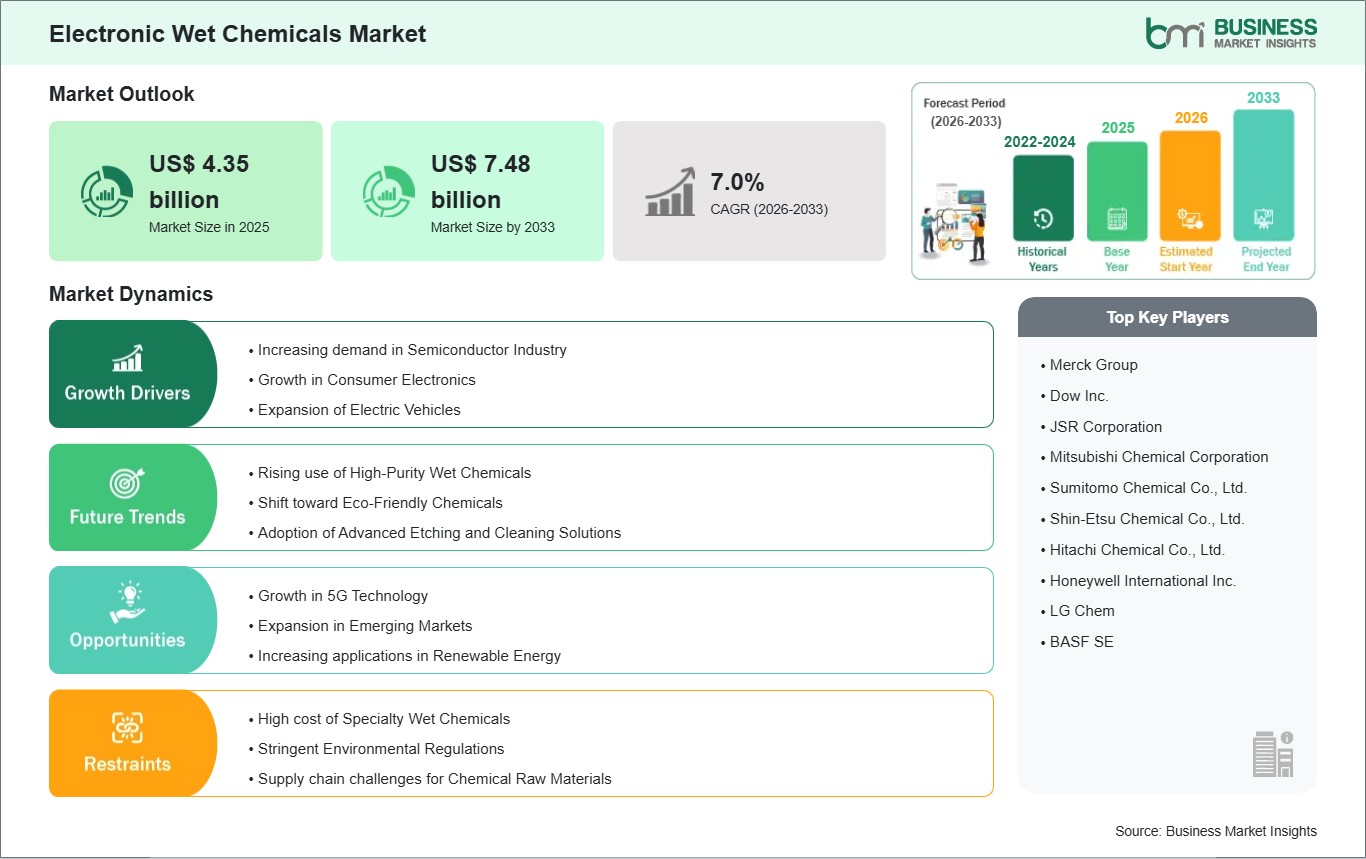

The Electronic Wet Chemicals Market size is expected to reach US$ 7.48 billion by 2033 from US$ 4.35 billion in 2025. The market is estimated to record a CAGR of 7.01% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global market for electronic wet chemicals is an important part of the larger semiconductor and electronics manufacturing landscape. These chemicals are crucial in wafer processing and device fabrication, supporting vital tasks such as cleaning, etching, stripping, and surface preparation. Made with ultra-high purity, electronic wet chemicals prevent contamination and ensure the precision needed for advanced semiconductor nodes and miniaturized components. They are commonly used in integrated circuits, printed circuit boards, flat panel displays, and photovoltaic devices. As electronic devices get smaller and more powerful, the demand for high-quality wet chemicals has grown across various industries, including consumer electronics, automotive, telecommunications, healthcare, and renewable energy. Typical categories of electronic wet chemicals include acids, solvents, bases, and specialty cleaning solutions. Each type is designed for specific stages of semiconductor and electronics production, providing high selectivity, controlled reactivity, and residue-free processing, which are crucial for maintaining product integrity and yield. Manufacturing electronic wet chemicals requires sophisticated processes like purification, distillation, and strict quality control to achieve very low impurity levels. Precision formulation and the use of specialized additives allow for customization of properties such as concentration, volatility, and compatibility with sensitive materials. Innovations in this area increasingly focus on developing eco-friendly chemistries, reducing hazardous waste, and ensuring compatibility with next-generation technologies like extreme ultraviolet lithography and advanced packaging. These chemicals are essential for driving advancements in electronics manufacturing. In the semiconductor industry, they help produce smaller, faster, and more energy-efficient chips used in smartphones, computers, and data centers. In the automotive sector, especially with the growth of electric and autonomous vehicles, these chemicals are crucial for making sensors, microcontrollers, and power electronics. Telecommunications infrastructure, including high-speed networks and next-generation connectivity, relies heavily on semiconductor components processed with wet chemicals. Renewable energy systems, such as solar panels, depend on these materials for efficient production and long-term performance. Additionally, medical devices and industrial automation technologies need highly reliable electronic components, further boosting demand. Market growth comes from the rapid expansion of semiconductor manufacturing, increased use of advanced electronics, and the global trend toward digital transformation. New technologies like artificial intelligence, 5G, and the Internet of Things are greatly increasing the need for high-purity wet chemicals. At the same time, sustainability trends and regulatory pressures are pushing for greener formulations and more efficient manufacturing processes. Government initiatives that support domestic semiconductor production and supply chain resilience also encourage market growth. However, the industry faces challenges such as high production and purification costs, strict environmental and safety regulations, and the need for continual innovation. Supply chain disruptions and the difficulty of maintaining ultra-high purity standards can further affect growth. Despite these obstacles, advancements in chemical processing technologies, increased investment in research and development, and strong demand from key industries are expected to keep the market moving forward. Overall, the electronic wet chemicals market is well-positioned to support the future of electronics by providing essential materials for precise, reliable, and sustainable manufacturing processes across global industries.

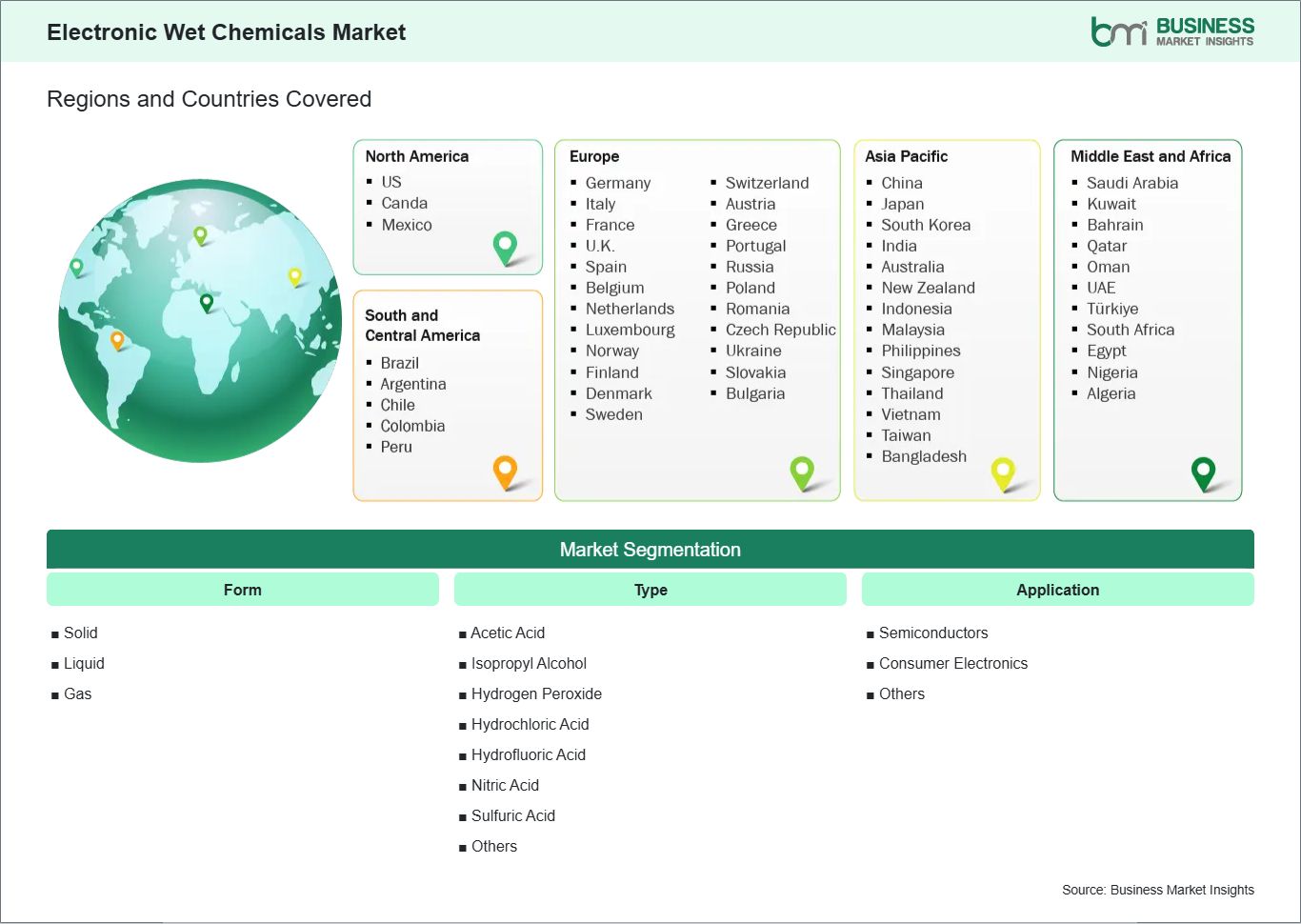

Key segments that contributed to the derivation of the Electronic Wet Chemicals market analysis are form, type, and application.

By form, the Electronic Wet Chemicals market is segmented into solid, liquid, and gas. The solid segment dominated the market in 2025.

By type, the Electronic Wet Chemicals market is segmented into acetic acid, isopropyl alcohol, hydrogen peroxide, hydrochloric acid, hydrofluoric acid, nitric acid, sulfuric acid, and others. The hydrogen peroxide segment dominated the market in 2025.

By application, the Electronic Wet Chemicals market is segmented into semiconductors, consumer electronics, and others. The semiconductors segment dominated the market in 2025.

Electronic Wet Chemicals Market Drivers and Opportunities:

Rising Demand from Semiconductor Fabrication, Advanced Electronics, and Electric Mobility

The global market for electronic wet chemicals is growing quickly due to increasing demand from semiconductor fabrication, advanced electronics, and the automotive sector. The widespread use of consumer electronics like smartphones, tablets, and wearable devices has greatly raised the need for ultra-high-purity wet chemicals used in wafer cleaning, etching, and surface preparation. These chemicals are vital for maintaining precision, removing contaminants, and ensuring optimal performance in smaller components. The rise of electric vehicles also plays a significant role, as wet chemicals are essential for making power semiconductors, sensors, and battery-related electronic systems. They help improve efficiency, reliability, and thermal management in automotive applications. In addition, the growth of data centers and high-performance computing infrastructure is driving semiconductor production, which increases the use of wet chemicals like acids, bases, and solvents. Industrial automation and smart manufacturing technologies depend on high-quality semiconductor devices, highlighting the importance of wet chemicals for ensuring consistency and durability. Government support for semiconductor manufacturing, localization strategies, and the development of digital infrastructure is speeding up market growth. As devices keep getting smaller, faster, and more interconnected, the demand for electronic wet chemicals is expected to rise steadily in both developed and emerging markets.

Technological Advancements and Increasing Focus on Eco-Friendly Wet Chemical Solutions

Technological progress is a major factor shaping the global electronic wet chemicals market. Ongoing innovation focuses on improving chemical purity, boosting process efficiency, and ensuring compatibility with advanced semiconductor technologies. The creation of ultra-high-purity acids, solvents, and cleaning solutions allows for precise processing needed for smaller and more complex semiconductor nodes. These advancements support new technologies like artificial intelligence, 5G networks, and the Internet of Things, which require high-performance electronic components. At the same time, the industry is shifting strongly toward environmentally friendly and low-toxicity wet chemical formulations due to stricter environmental regulations and corporate sustainability goals. Manufacturers are increasingly adopting green chemistry practices, cutting down hazardous waste, and using energy-efficient production methods to lessen environmental impact. Improvements in chemical engineering and materials science are increasing the selectivity, stability, and effectiveness of wet chemicals, leading to better yields and fewer defects in manufacturing. Additionally, innovations in chemical delivery systems and recycling processes help optimize usage and reduce operational costs without sacrificing quality. Ongoing research and development efforts are also working to ensure compatibility with next-generation semiconductor designs and enable further miniaturization. As industries focus on sustainability, operational efficiency, and high-performance materials, technological advancements will keep driving long-term growth in the electronic wet chemicals market.

Electronic Wet Chemicals Market Size and Share Analysis:

The solid segment is the leader because of its stability, easy storage, and precise handling in controlled semiconductor environments. Solid wet chemicals are preferred for tasks that need accurate dosing and lower contamination risks, which support high-purity manufacturing processes.

Hydrogen peroxide is at the top of the market due to its strong oxidizing properties and effectiveness in cleaning wafers and preparing surfaces. It is commonly used in semiconductor fabrication to get rid of organic and metallic contaminants, ensuring the high performance and reliability of electronic components.

The semiconductor segment leads because of the widespread use of wet chemicals in cleaning wafers, etching, and processing steps. Rapid progress in chip manufacturing and the growing demand for smaller, more efficient devices keep increasing the need for high-purity wet chemicals in this segment.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Merck Group

Dow Inc.

JSR Corporation

Mitsubishi Chemical Corporation

Sumitomo Chemical Co., Ltd.

Shin-Etsu Chemical Co., Ltd.

Hitachi Chemical Co., Ltd.

Honeywell International Inc.

LG Chem

BASF SE

Get more information on this report

Electronic Wet Chemicals Market Report Coverage and Deliverables:

The "Electronic Wet Chemicals Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Electronic Wet Chemicals market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Electronic Wet Chemicals market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Electronic Wet Chemicals market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Electronic Wet Chemicals market

Detailed company profiles, including SWOT analysis

The geographical scope of the Electronic Wet Chemicals market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Electronic Wet Chemicals market in the Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific Electronic Wet Chemicals market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia.

The Asia-Pacific region is the fastest-growing market for electronic wet chemicals. This growth comes from quick industrialization, strong semiconductor manufacturing, and a rising demand for high-purity process chemicals. China, Japan, India, South Korea, and Taiwan are experiencing significant growth in semiconductor fabrication, consumer electronics, and automotive electronics industries. These sectors depend on electronic wet chemicals like ultra-pure acids, bases, and solvents for key processes such as wafer cleaning, etching, and surface preparation. The increasing need for advanced chips and smaller components is driving the demand for ultra-high-purity wet chemicals across the region. The rise of electric vehicles also plays a role in market growth since these chemicals are crucial for making power semiconductors, sensors, and battery-related electronic systems that ensure efficiency, safety, and durability. Additionally, higher investments in semiconductor fabrication plants, electronics manufacturing, and advanced communication infrastructure are increasing the demand for wet chemicals as essential materials. Rapid urbanization, growing disposable incomes, and expanding digital ecosystems are boosting the need for smartphones, computers, and connected devices, which in turn raises the demand for enhanced semiconductor production. The growth of renewable energy technologies, especially solar panels, is also increasing the use of wet chemicals in wafer processing and cell manufacturing. The region benefits from a strong electronics manufacturing ecosystem, integrated supply chains, and cost-effective production capabilities, which support large-scale production and exports of electronic wet chemicals. Governments across Asia-Pacific are working to strengthen domestic semiconductor industries, encourage digital change, and promote better manufacturing technologies, which help drive market growth. Environmental regulations are leading manufacturers to adopt eco-friendly and low-toxicity wet chemical formulations, which reduce hazardous waste and emissions. Technological improvements, including the creation of ultra-high-purity chemicals, better purification methods, and precise chemical delivery systems, enhance process efficiency and product quality. The availability of skilled labor, access to raw materials, and increasing investments in research and development boost the region`s competitive edge. With ongoing industrial growth, supportive policies, and a strong focus on innovation and sustainability, Asia-Pacific is likely to remain a major center for production, consumption, and technological advancements in the global electronic wet chemicals market.

Get more information on this report

Electronic Wet Chemicals Market Research Report Guidance:

The report includes qualitative and quantitative data in the Electronic Wet Chemicals market across form, type, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Electronic Wet Chemicals market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Electronic Wet Chemicals market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Electronic Wet Chemicals market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover Electronic Wet Chemicals market segments by form, type, and application across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue and forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Electronic Wet Chemicals market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Electronic Wet Chemicals Market News and Key Development:

The Electronic Wet Chemicals market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Electronic Wet Chemicals market are:

In October 2025, BASF announced the construction of a state-of-the-art Electronic Grade Ammonium Hydroxide (NH4OH EG) plant in Ludwigshafen, Germany, in support of wafer cleaning, etching and other precision processes in semiconductor manufacturing. This critical ultra-pure chemical will support the growth and expansion of semiconductor companies in Europe, ensuring a robust local supply chain for the production of advanced chips.

In November 2025, Sumitomo Chemical entered into a definitive agreement to acquire 100% of the shares of Asia Union Electronic Chemical Corporation (“AUECC”), a Taiwanese semiconductor process chemicals company. The transaction is subject to customary closing conditions, including obtaining required regulatory approvals. The acquisition of AUECC will enable Sumitomo Chemical to strengthen its global footprint and establish its first manufacturing base for semiconductor process chemicals in Taiwan and a second base in the United States, alongside its Texas site, further accelerating the expansion of its semiconductor process chemicals business worldwide.

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Electronic Wet Chemicals Market

Merck Group

Dow Inc.

JSR Corporation

Mitsubishi Chemical Corporation

Sumitomo Chemical Co., Ltd.

Shin-Etsu Chemical Co., Ltd.

Hitachi Chemical Co., Ltd.

Honeywell International Inc.

LG Chem

BASF SE

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Electronic Wet Chemicals Market?

The Electronic Wet Chemicals Market is valued at US$ 4.35 billion in 2025, it is projected to reach US$ 7.48 billion by 2033.

What is the CAGR for Electronic Wet Chemicals Market by (2026 - 2033)?

As per our report Electronic Wet Chemicals Market, the market size is valued at US$ 4.35 billion in 2025, projecting it to reach US$ 7.48 billion by 2033. This translates to a CAGR of approximately 7.01% during the forecast period.

What segments are covered in this report?

The Electronic Wet Chemicals Market report typically cover these key segments-

Form (Solid, Liquid, and Gas)

Type (Acetic Acid, Isopropyl Alcohol, Hydrogen Peroxide, Hydrochloric Acid, Hydrofluoric Acid, Nitric Acid, Sulfuric Acid, and Others)

Application (Semiconductors, Consumer Electronics, and Others)

What is the historic period, base year, and forecast period taken for Electronic Wet Chemicals Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Electronic Wet Chemicals Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Electronic Wet Chemicals Market?

The Electronic Wet Chemicals Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Merck Group

Dow Inc.

JSR Corporation

Mitsubishi Chemical Corporation

Sumitomo Chemical Co., Ltd.

Shin-Etsu Chemical Co., Ltd.

Hitachi Chemical Co., Ltd.

Honeywell International Inc.

LG Chem

BASF SE

Who should buy this report?

The Electronic Wet Chemicals Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Electronic Wet Chemicals Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Electronic Wet Chemicals Market

Get Free Sample For Electronic Wet Chemicals Market