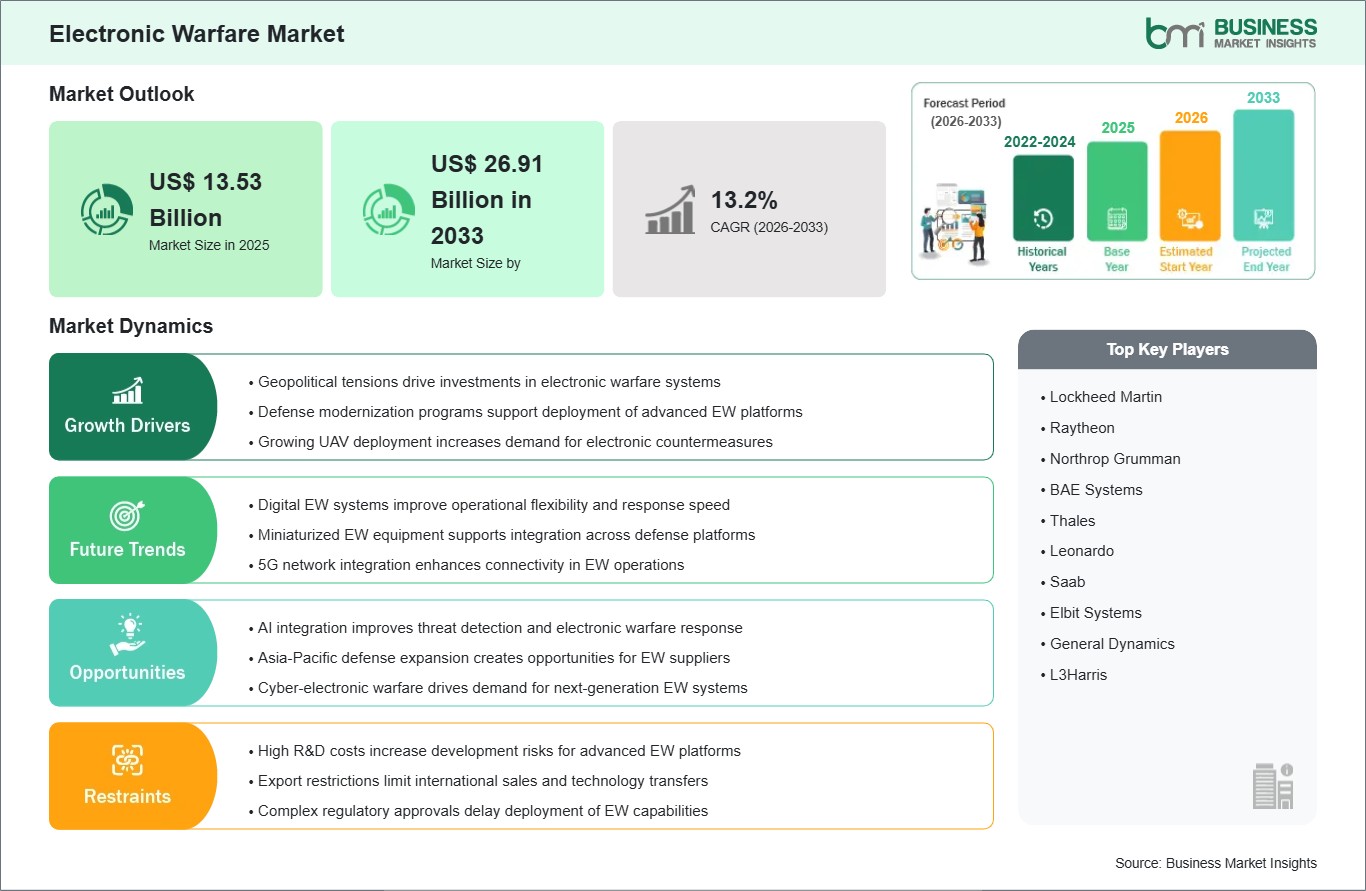

The electronic warfare market size is expected to reach US$ 26.91 billion by 2033 from US$ 13.53 billion in 2025. The market is estimated to record a CAGR of 13.2% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Electronic Warfare's (EW) is a rapidly evolving segment of modern defense systems, centered on the strategic use of the electromagnetic spectrum to detect, intercept, disrupt, or deceive enemy communications, radar, and navigation systems. As military operations become increasingly dependent on networked and sensor-driven technologies, control of the electromagnetic environment has emerged as a decisive factor in achieving battlefield superiority. Electronic warfare systems are now embedded across air, land, sea, space, and cyber domains, forming a core layer of multi-domain defense strategies.

A key driver of this market is the rising sophistication of adversarial threats, particularly advanced radar-guided weapons, integrated air defense systems, and encrypted communication networks. Modern conflicts increasingly rely on spectrum dominance, where the ability to jam, spoof, or degrade enemy signals can significantly alter operational outcomes. This has led to growing deployment of electronic support measures, electronic attack systems, and electronic protection capabilities integrated into both offensive and defensive military platforms.

Technological advancements are also accelerating market expansion, particularly in areas such as software-defined radios, cognitive electronic warfare, artificial intelligence-enabled signal processing, and miniaturized RF systems. These innovations are enabling faster threat identification, adaptive jamming techniques, and real-time spectrum management. The integration of EW capabilities into unmanned platforms, fighter aircraft, naval vessels, and ground-based systems is further enhancing operational flexibility and mission effectiveness.

Despite strong strategic demand, the market faces challenges including high system complexity, rapid technological obsolescence, and the need for continuous spectrum monitoring in highly contested environments. Additionally, evolving electronic counter-countermeasure techniques require constant upgrades and investment. Nevertheless, increasing geopolitical tensions and the growing importance of information dominance are expected to sustain strong long-term growth in the global Electronic Warfare

Electronic Warfare Market - Strategic Insights:

Get more information on this report

Electronic Warfare Market Segmentation Analysis:

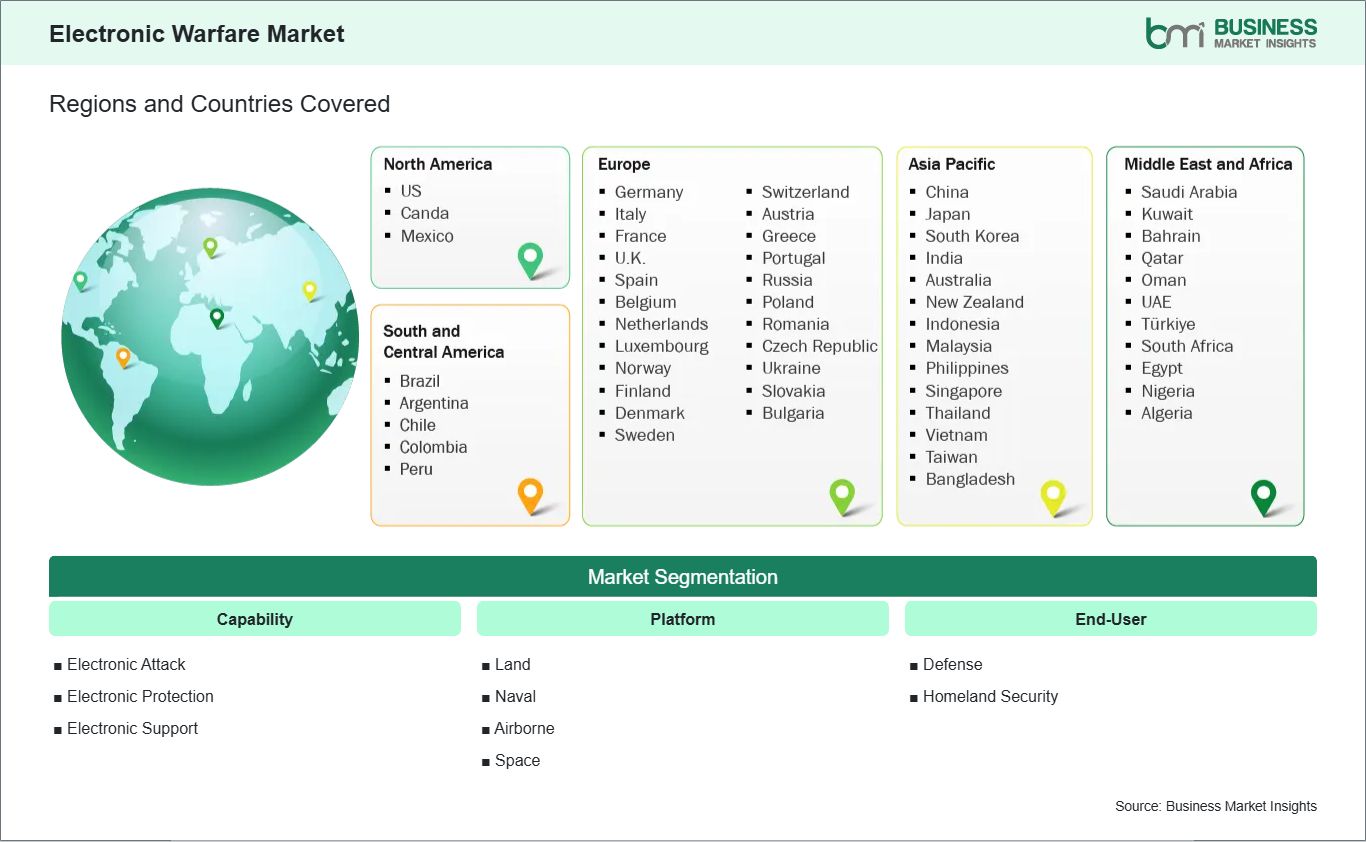

The electronic warfare (EW) market is segmented based on capability, platform, and end-user, driven by increasing spectrum dominance requirements, modernization of defense systems, and the rising use of advanced electronic and cyber-electromagnetic operations across multi-domain battlefields.

By Capability

Electronic Attack: Involves offensive use of electromagnetic energy to jam, deceive, or disrupt enemy radar, communication systems, and sensors. It is widely used for disabling adversary situational awareness and degrading battlefield coordination.

Electronic Protection: Focuses on safeguarding friendly forces from enemy electronic attacks through techniques such as encryption, frequency hopping, signal hardening, and adaptive countermeasure systems.

Electronic Support: Enables detection, interception, identification, and geolocation of electromagnetic emissions, providing real-time intelligence and situational awareness of enemy activities.

By Platform

Land: Ground-based EW systems mounted on vehicles or deployed as fixed installations, used for battlefield signal control, jamming operations, and force protection.

Naval: Installed on ships, submarines, and carrier strike groups to detect and counter missile threats, secure maritime communications, and perform electronic surveillance and jamming.

Airborne: Integrated into fighter jets, reconnaissance aircraft, helicopters, and UAVs for threat detection, self-protection, and electronic attack missions in contested airspace.

Space: Includes satellite-based EW systems used for signal intelligence, communications disruption, early warning, and space-based surveillance supporting strategic defense operations.

By End User

Defense: The primary segment, comprising army, navy, and air force units that deploy EW systems for combat operations, intelligence gathering, electronic surveillance, and strategic deterrence.

Homeland Security: Includes border security agencies and internal security forces using EW technologies for counter-drone operations, critical infrastructure protection, and counter-terrorism missions.

Electronic Warfare Market Drivers and Opportunities:

Rising Geopolitical Tensions

The electronic warfare (EW) market is expanding as global geopolitical tensions intensify and defense modernization programs accelerate across multiple regions. The military has started focusing more on electronic warfare, specifically electronic spectrum dominance, for the security of its communication systems and interference with that of the enemy. This is one reason why the use of advanced Electronic Warfare systems has become more common in recent times.

Modern conflicts have demonstrated the growing importance of non-kinetic warfare, where control of the electromagnetic spectrum can be as critical as traditional firepower.In this respect, the military is modernizing existing systems in order to fight new threats that are emerging. Some examples of threats include encrypted communications, weapons guided by radars, and drones equipped with surveillance technology. In addition, the importance of EW systems has increased greatly due to their application in multiple-domain battles.

Another key driver is the rapid proliferation of unmanned and network-centric warfare technologies. As military operations become more dependent on interconnected technologies, the risk posed by communications and navigation networks will become greater, which creates great incentive for the development of electronic countermeasures that can effectively address threats from enemy electronic devices.

Integration with AI systems

A major opportunity in the electronic warfare market lies in the integration of artificial intelligence (AI) to enhance speed, adaptability, and decision-making accuracy. Conventional EW systems tend to utilize pre-defined databases of threat profiles, whereas AI-based systems are able to provide real-time analysis of the electromagnetic environment and detect any emerging threats that may not be present in the database at all.

AI integration enables automated signal classification, intelligent jamming pattern selection, and predictive threat detection. The machine learning algorithms can analyze substantial amounts of spectrum data to classify whether it is a friendly signal or an unfriendly one. It becomes especially useful in contemporary warfare scenarios, when there are multiple electronic signals available, which are constantly changing and encrypted.

Additionally, AI-powered EW systems support adaptive and autonomous operations, allowing platforms to self-optimize based on mission conditions. This ability has become even more relevant in a networked defense system, since rapid decisions may often determine mission success or failure. With ongoing digitization and integration of intelligence within defense capabilities, AI-powered electronic warfare will play an integral part in future military capability development efforts.

Electronic Warfare Market Size and Share Analysis:

The electronic warfare market is projected to grow from US$ 13.53 billion in 2025 to US$ 26.91 billion by 2033, registering a CAGR of 13.2% from 2026 to 2033.

By capability, Electronic Support dominates the market as it forms the foundation of electronic warfare operations by detecting, intercepting, and identifying electromagnetic signals. Growing reliance on situational awareness, signal intelligence, and spectrum dominance in modern battlespaces is driving strong demand for advanced ES systems across all defense platforms.

By platform, the airborne segment dominates the market due to the extensive integration of electronic warfare suites in fighter aircraft, surveillance platforms, and UAVs. Airborne systems provide superior range, flexibility, and real-time threat response capabilities, making them central to modern multi-domain warfare strategies.

By end-user, the defense segment dominates the market as electronic warfare systems are primarily developed and deployed for military applications, including battlefield awareness, communication disruption, and protection against guided weapons. Increasing defense modernization programs and rising geopolitical tensions continue to drive significant investment in EW capabilities worldwide.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Lockheed Martin

Raytheon

Northrop Grumman

BAE Systems

Thales

Leonardo

Saab

Elbit Systems

General Dynamics

L3Harris

Get more information on this report

Electronic Warfare Market Report Coverage and Deliverables:

The "Electronic Warfare Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all key market segments covered under the scope

Market trends, along with market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key trends, global and regional frameworks, major players, regulations, and recent developments

Industry landscape and competitive analysis covering market concentration, heat map analysis, prominent players, and recent developments

Detailed company profiles, including SWOT analysis

Electronic Warfare Market Geographic Insights:

In terms of geographical distribution of the Electronic Warfare Market, there is a highly concentrated and strategically driven pattern of adoption based on defense modernization programs, increasing geopolitical tensions, rising investment in network-centric warfare capabilities, and rapid integration of advanced technologies such as AI-enabled signal processing, cyber-electromagnetic activities, and real-time threat detection systems.

North America is a leading market for electronic warfare systems, supported by strong defense budgets, advanced R&D capabilities, and the presence of major defense contractors and technology providers. The U.S. has established dominance through its consistent deployment of air, naval, and terrestrial electronic warfare systems for increasing spectrum domination and situational awareness. The development initiatives undertaken for the modernization of fighters, warships, and ground troops have led to the implementation of advanced ESM, EA, and EP technologies. In addition, the use of artificial intelligence and software-based warfare solutions is increasingly contributing to regional electronic warfare capabilities.

Asia Pacific is experiencing rapid growth in the electronic warfare market due to increasing defense expenditures, regional security challenges, and accelerated military modernization initiatives. The countries in question have been making substantial investments towards developing homegrown electronic warfare solutions for their surveillance, jamming, and countermeasures systems. There has been an increased focus on building multi-domain capability and enhancing situational awareness in the realms of air, land, sea, and cyber. Growth in the manufacture of defense electronics and a greater focus on indigenous military equipment have also contributed to growth in the market.

Both regions are key contributors to the expansion of the electronic warfare market, driven by intensifying defense modernization efforts, increasing demand for spectrum dominance capabilities, and growing deployment of advanced electronic attack and defense systems across modern military platforms.

Get more information on this report

Electronic Warfare Market Research Report Guidance:

The report includes qualitative and quantitative data in the electronic warfare market across capability, platform, end-user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by capability, platform, end-user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Electronic Warfare Market News and Key Development:

The electronic warfare market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In May 2026, Bharat Electronics Limited (BEL), announced that it had secured a ₹1,476 crore contract to supply five Ground-Based Mobile Electronic Systems (GBMES) for the Indian Army, designed to enhance battlefield electronic support measures, situational awareness, and electronic warfare operations in mobile and contested environments.

In July 2025, BAE Systems, announced that it had received a contract from L3Harris to support the conversion of Gulfstream G550 aircraft into airborne electronic attack platforms for the Italian Air Force, providing key hardware and integration components to strengthen airborne electronic warfare and jamming capabilities.

Key Sources Referred:

World BankWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)North Atlantic Treaty Organization (NATO)S. Department of Defense (DoD)S. Department of Energy (DOE)Defense Advanced Research Projects Agency (DARPA)European Defence Agency (EDA)European CommissionUnited Nations Institute for Disarmament Research (UNIDIR)Stockholm International Peace Research Institute (SIPRI)International Organization for Standardization (ISO)Society of Automotive Engineers (SAE International) Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Electronic Warfare Market

Lockheed Martin

Raytheon

Northrop Grumman

BAE Systems

Thales

Leonardo

Saab

Elbit Systems

General Dynamics

L3Harris

Frequently Asked Questions

How big is the Electronic Warfare Market?

The Electronic Warfare Market is valued at US$ 13.53 Billion in 2025, it is projected to reach US$ 26.91 Billion in 2033 by .

What is the CAGR for Electronic Warfare Market by (2026 - 2033)?

As per our report Electronic Warfare Market, the market size is valued at US$ 13.53 Billion in 2025, projecting it to reach US$ 26.91 Billion in 2033 by . This translates to a CAGR of approximately 13.2% during the forecast period.

What segments are covered in this report?

The Electronic Warfare Market report typically cover these key segments-

What is the historic period, base year, and forecast period taken for Electronic Warfare Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Electronic Warfare Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Electronic Warfare Market?

The Electronic Warfare Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Lockheed Martin

Raytheon

Northrop Grumman

BAE Systems

Thales

Leonardo

Saab

Elbit Systems

General Dynamics

L3Harris

Who should buy this report?

The Electronic Warfare Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Electronic Warfare Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Electronic Warfare Market

Get Free Sample For Electronic Warfare Market