The Electro-Optical System market size is expected to reach US$ 4.06 billion by 2033 from US$ 1.99 billion in 2025. The market is estimated to record a CAGR of 8.9% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Electro-optical (EO) systems refer to the integrated application of electronic and optical technologies engineered to detect, image, and track objects across the electromagnetic spectrum, typically spanning the visible, infrared, and ultraviolet bands. By utilizing a coordinated framework of hardware, including high-resolution sensors, lasers, and thermal detectors, integrated with advanced image processing software, these systems facilitate critical situational awareness and precision targeting. This technology is fundamental to the operational architecture of modern defense platforms, aerospace monitoring, and industrial automation. Market expansion is being propelled by the global transition toward autonomous defense systems, the rising institutional requirement for intelligence, surveillance, and reconnaissance (ISR) dominance, and the increasing integration of artificial intelligence (AI) to enhance real-time object recognition and data fusion.

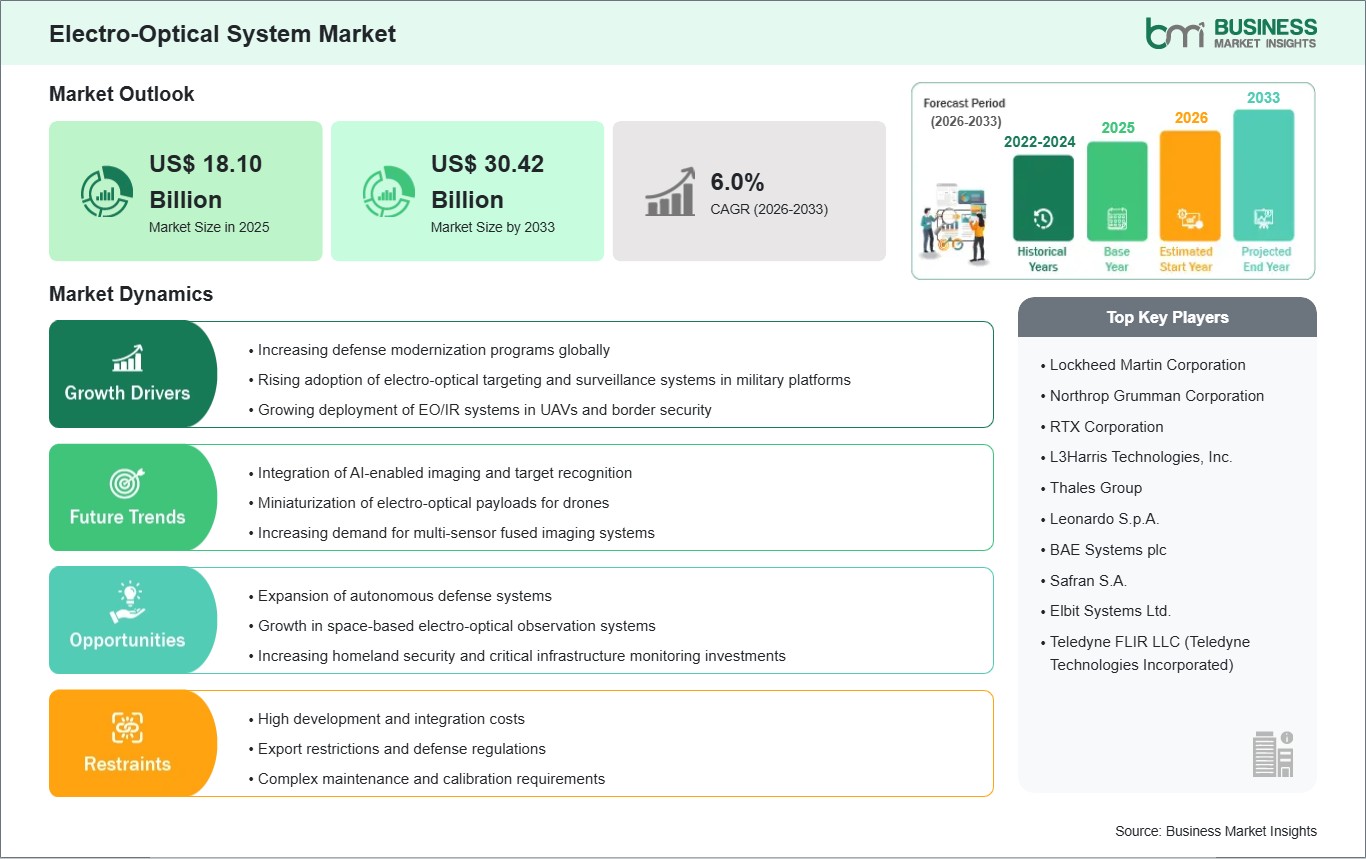

However, several factors may restrain market progression. The high capital intensity associated with the initial procurement and upgrade of advanced multispectral and hyperspectral sensors remains a primary hurdle, particularly for defense agencies and commercial entities facing restrictive budgets. The industry also faces persistent technical challenges regarding the rapid pace of technological obsolescence, where existing systems can quickly become outdated due to emerging innovations, leading to increased lifecycle costs for operators. Additionally, the proliferation of specialized hardware requirements has intensified concerns regarding supply chain vulnerability, as the market relies on a limited number of suppliers for critical materials such as germanium and gallium. These hurdles, compounded by stringent export control regulations on dual-use components and the technical difficulty of maintaining precision optics in harsh environmental conditions, increase the total cost of ownership and may lengthen the modernization cycle for traditional surveillance infrastructures.

Despite these hurdles, the market outlook remains highly favorable as the sector transitions toward intelligent and autonomous sensing ecosystems. Opportunities are emerging through the adoption of AI-Integrated Image Processing; the market is witnessing a surge in intelligent-sensing capabilities that utilize machine learning to distinguish between objects with high precision, significantly reducing false alarm rates. The unmanned systems field is gaining significant traction, with a rising requirement for Low-SWaP (Size, Weight, and Power) EO Payloads for drones and autonomous vehicles. Furthermore, the growth of Space-Based Imaging, utilizing next-generation optical sensors for persistent global monitoring, aligns with global goals for enhanced environmental tracking and planetary security.

Electro-Optical System Market - Strategic Insights:

Get more information on this report

Electro-Optical System Market Segmentation Analysis:

Key segments that contributed to the derivation of the Electro-Optical System market analysis are system, type, and platform.

By System, the market is segmented into Imaging and Non-Imaging.

By Type, the market is divided into Laser, Infrared, and Image Intensifier.

By Platform, the market is segmented into Land-Based, Sea-Based, and Air-Based.

Electro-Optical System Market Drivers and Opportunities:

Rising Demand for Surveillance, Defense, and Precision Imaging

The electro-optical system market is being driven by the rising demand for advanced surveillance, defense capabilities, and precision imaging across military, aerospace, industrial, and healthcare sectors. Electro optical systems, comprising sensors, cameras, infrared devices, and laser-based technologies, are essential for detecting, tracking, and imaging in complex environments where accuracy and reliability are critical. The rapid expansion of defense modernization programs worldwide is amplifying adoption, as armed forces seek enhanced situational awareness, target acquisition, and threat detection. Aerospace and aviation industries are reinforcing demand, with electro-optical systems integrated into navigation, collision avoidance, and unmanned aerial vehicles (UAVs). Healthcare and industrial sectors are also fueling growth, as electro optical technologies support medical imaging, quality inspection, and precision manufacturing. Additionally, stricter regulatory standards for safety, border security, and environmental monitoring are propelling investment in advanced electro-optical solutions. Collectively, surveillance priorities, defense requirements, and precision imaging needs are sustaining momentum and driving sustained growth in the global electro optical system market.

Rising Integration of AI, IoT, and Emerging Applications

Opportunities in the electro‑optical system market are expanding through the integration of artificial intelligence, IoT ecosystems, and emerging cross‑industry applications. AI‑enabled electro‑optical platforms are opening lucrative opportunities by delivering automated image recognition, predictive analytics, and adaptive decision‑making in defense and industrial environments. IoT‑driven solutions are gaining traction, enabling electro‑optical systems to connect seamlessly with smart grids, autonomous vehicles, and digital infrastructure. The growing emphasis on digital transformation is fueling demand for interoperable systems that integrate with cloud platforms, robotics, and advanced analytics. Emerging applications in healthcare are driving innovation, as electro‑optical systems support minimally invasive diagnostics, surgical guidance, and telemedicine. Environmental monitoring and smart cities are reinforcing opportunities, where electro‑optical technologies enable pollution tracking, disaster management, and intelligent traffic systems. Additionally, sustainability trends are encouraging deployment of energy‑efficient, eco‑friendly electro‑optical devices that align with global environmental goals. The expansion of UAVs, autonomous defense systems, and industrial automation is creating new pathways for adoption. Vendors who focus on AI‑driven, IoT‑ready, and industry‑specific electro‑optical solutions are well‑positioned to capture growth. The convergence of smart technology, defense modernization, and precision imaging underscores a transformative trajectory for the global electro‑optical system market.

Electro-Optical System Market Size and Share Analysis:

The Electro-Optical System market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report examines subsegments categorized within system, type, and platform, offering insights into their contribution to overall market performance.

Based on System, the Imaging subsegment dominates adoption, as imaging systems are indispensable for surveillance, reconnaissance, and targeting applications. These systems provide real‑time visuals, enabling situational awareness and precision in both defense and commercial sectors. The Non‑Imaging subsegment is essential for applications such as laser range finding, infrared detection, and communication systems, where data collection and signal processing are prioritized over visuals. Non‑imaging systems anchor demand in aerospace, telecommunications, and scientific research. Together, imaging and non‑imaging systems highlight the versatility of electro‑optical technologies across both visual and analytical domains.

Electro-Optical System Market Report Coverage and Deliverables:

The “Electro-Optical System Market Size and Forecast (2022–2033)” report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, global and regional framework, major players, and recent developments

Market concentration, heat map analysis, prominent players, and recent developments

Detailed company profiles, including SWOT analysis

Electro-Optical System Market Geographic Insights:

The geographical scope of the Electro-Optical System market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

North America maintains a preeminent position within the global industry, a status reinforced by the region's advanced defense and aerospace sectors and substantial investments in research and development. The regional landscape is characterized by a mature innovation ecosystem in the United States and Canada, where the transition toward high-performance imaging and multi-spectral sensors has become a strategic priority for maintaining situational awareness and precision targeting. This market leadership is supported by a robust presence of technology pioneers, including Lockheed Martin Corporation, RTX Corporation (Raytheon), Northrop Grumman Corporation, and L3Harris Technologies, who drive the commercialization of sophisticated airborne, land, and naval electro-optical platforms.

Industrial and enterprise trends in the region reflect a decisive shift toward AI-Integrated Target Recognition and Autonomous System Deployment. Organizations are increasingly moving away from manual surveillance to adopt intelligent sensing capabilities that utilize deep learning and hyperspectral imaging to enhance detection accuracy and reduce false positives. Furthermore, the region is witnessing an escalating demand for Unmanned Aerial Vehicle (UAV) Payloads and Space-Based Imaging. This focus on "Information Superiority" is particularly evident in the rapid adoption of compact, lightweight electro-optical gimbals for tactical drones and the expansion of satellite-based earth observation networks for both military and commercial applications.

Get more information on this report

Electro-Optical System Market Research Report Guidance:

The report includes qualitative and quantitative data in the Electro-Optical System market across system, type, platform, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by system, type, platform, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Electro-Optical System Market News and Key Development:

The Electro-Optical System market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Electro-Optical System market are:

In February 2026, Ciena Corporation unveiled the Vesta 200 6.4T CPX, a high-density, low-power pluggable optical engine designed to accelerate the adoption of co-packaged optics (CPO) in AI-driven data center networks. The solution delivers up to 70% reduction in power consumption while enabling high-speed 200G/lane optical interconnects for next-generation 100T and 200T systems. By combining advanced silicon photonics with an open, standards-based ecosystem, the development highlights growing innovation in electro-optical technologies aimed at improving scalability, efficiency, and interoperability in high-performance computing and cloud infrastructure.

In March 2026, Eoptolink Technology Inc., Ltd. unveiled its NX200 and NX300 Optical Circuit Switching (OCS) solutions at OFC 2026, designed to enhance AI-driven data center network performance. The systems leverage MEMS-based optical beam steering to create direct, reconfigurable light paths, eliminating the need for power-intensive optical-electrical-optical conversions. This innovation significantly reduces latency and energy consumption while improving scalability and efficiency, highlighting the growing adoption of advanced electro-optical technologies in next-generation AI infrastructure.

Key Sources Referred:

World Bank & Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Electro-Optical System Market

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the Electro-Optical System Market?

The Electro-Optical System Market is valued at US$ 18.10 Billion in 2025, it is projected to reach US$ 30.42 Billion by 2033.

What is the CAGR for Electro-Optical System Market by (2026 - 2033)?

As per our report Electro-Optical System Market, the market size is valued at US$ 18.10 Billion in 2025, projecting it to reach US$ 30.42 Billion by 2033. This translates to a CAGR of approximately 6.0% during the forecast period.

What segments are covered in this report?

The Electro-Optical System Market report typically cover these key segments-

System( Imaging and Non-Imaging)

Type (Laser, Infrared, Image Intensifier)

Platform ( Land-Based, Sea-Based Air-Based)

What is the historic period, base year, and forecast period taken for Electro-Optical System Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Electro-Optical System Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Electro-Optical System Market?

The Electro-Optical System Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Electro-Optical System Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Electro-Optical System Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Electro-Optical System Market

Get Free Sample For Electro-Optical System Market