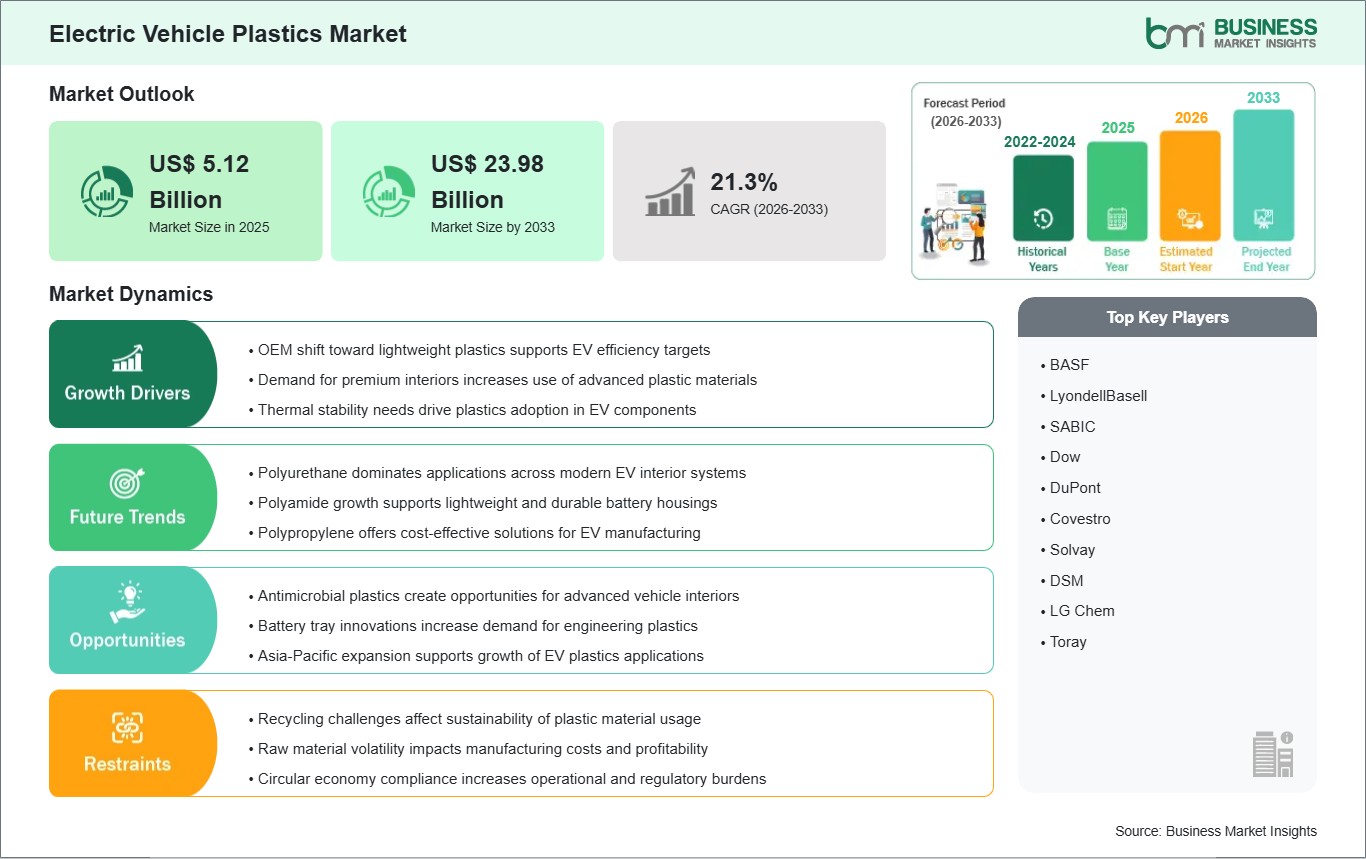

The electric vehicle plastics market size is expected to reach US$ 23.98 billion by 2033 from US$ 5.12 billion in 2025. The market is estimated to record a CAGR of 21.3% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Electric vehicle plastics refer to the utilization of engineering polymers and resins that replace the use of heavy metals and glass in the construction of the electrified vehicles' components. The modern lightweight materials provide enhanced strength-to-weight ratios, electrical insulation properties, chemical resistance, and optimized mechanical designs of the transit structures used by passengers. The use of such materials in electric cars is aimed at enhancing the driving efficiency, energy density, and meeting the safety standards for crashworthiness set by the manufacturers.

The global adoption of such innovations in the manufacture of electric cars is mainly attributable to the need for the reduction of the vehicle's weight through advanced polymer injection-molding techniques. Such materials become necessary for fleet electrification as stricter greenhouse gas regulations drive manufacturers to increase the range of transportation provided per charge in freight or consumer delivery transport networks. Additionally, improvements in chemical engineering allow the protection of electronic control units from the damaging effects of the environment.

The compounds of polypropylene and polyurethane materials are prominent in structural and interior assemblies, while polyamides and polycarbonates have seen increased use in thermal enclosures and advanced optical lighting assemblies. Passenger car design requirements determine the majority of the procurement volumes for the main materials used, but commercial transportation is another vital growth area that centers on strength and optimized components. The main source of volume is from interior surface materials, with exteriors and engines being other segments that need unique properties.

Automotive manufacturing is evolving to adopt multi-material designs in structures, which will involve less stamping and more plastics to create lightweight designs with roomy interiors. This will necessitate the use of plastic materials that are easy to mold around complex electronic wiring and sensor systems. The competition within this industry segment comprises the major global chemical companies that rely on large polymer compounding capabilities and innovative startups specializing in advanced, recyclable composite materials.

Electric Vehicle Plastics Market - Strategic Insights:

Get more information on this report

Electric Vehicle Plastics Market Segmentation Analysis:

The electric vehicle plastics market is segmented based on type, application, and vehicle type, reflecting the expanding deployment of high-performance engineering polymers across diversified interior, exterior, and powertrain transport systems.

By Type

ABS: Rigid thermoplastic polymers deliver exceptional impact resistance and dimensional stability for structural vehicle trim and electronic component housings.

PU: Versatile polyurethane formulations provide superior cushioning comfort, acoustic dampening insulation, and structural flexibility across interior seating networks.

PA: High-performance polyamides offer unmatched thermal endurance and chemical resistance required for high-stress powertrain applications.

PC: Optically clear polycarbonates provide excellent impact strength and advanced dimensional stability for sophisticated exterior lighting and sensor lenses.

PVB: Specialized polyvinyl butyral sheets serve as a core acoustic and protective safety binding layer within multi-layered windshield structures.

PP: Low-density polypropylene compounds offer cost-effective structural strength, driving widespread utilization across interior dashboards and exterior bumper assemblies.

PVC: Durable polyvinyl chloride resins supply excellent electrical insulation properties and vital flame retardancy for high-voltage internal wiring protection.

PMMA: Premium polymethyl methacrylate polymers deliver superior scratch resistance and glass-like optical clarity for advanced interactive instrument displays.

By Application

Dashboard: Multi-component polymer structures house digital instrument arrays while providing integrated structural support and driver impact safety protection.

Seat: Ergonomic polymer frames and specialized foam layers minimize cabin weight while maximizing long-distance passenger comfort and spinal support.

Trim: High-finish interior and exterior accents improve vehicle aerodynamics while providing a premium, wear-resistant consumer aesthetic.

Bumper: High-impact polymer structures absorb low-speed collisions to shield structural frame elements and expensive internal electronics.

Body: Lightweight composite panels replace conventional steel sheet metals to reduce overall vehicle mass and prevent corrosion over extended lifecycles.

Battery: Fire-retardant structural enclosures and internal cell holders isolate high-voltage currents and safeguard modules against thermal propagation.

Engine: Heat-stabilized technical plastics insulate auxiliary drive motors, inverters, and onboard power conversion components from localized heat build-up.

Lighting: Precision molded covers protect forward illumination systems and rear signaling arrays from moisture ingress and stone impacts.

Wiring: Flexible, non-conductive insulation sleeves shield complex high-voltage power lines and low-voltage digital communication networks from electromagnetic interference.

By Vehicle Type

Passenger Cars: High-volume consumer transit platforms utilize advanced engineering resins to maximize battery driving ranges and interior aesthetic appeal.

Commercial EVs: Fleet distribution trucks and municipal transport assets require heavy-duty, wear-resistant structural polymers to endure continuous daily service.

Electric Vehicle Plastics Market Drivers and Opportunities:

OEMs shifting to lightweight plastics

The global automobile industry is developing innovative platform designs centered around eliminating any unneeded component mass in order to combat the considerable added weight provided by the battery packs. This mass reduction effort forces original equipment manufacturers to utilize more lightweight alternatives made out of engineering polymers reinforced with fibers rather than standard metallic materials such as steel and aluminum throughout the chassis. As a result, technical plastics require more rapid approval cycles in order to maintain vehicle range and optimize payload metrics.

Efforts to adhere to stringent fleet requirements force design engineers to redesign the entire material billings used to produce each vehicle type with an emphasis on lighter-density compounds. Mass savings efforts force design engineering teams to incorporate polymer-based compounds not only for financial reasons but rather as fundamental enabling factors for modernized transport platforms. This process fundamentally changes the entire source material pipeline for the automotive industry.

Anti-microbial plastics adoption

The transition toward shared mobility services, autonomous ride-hailing networks, and multi-user commercial delivery systems elevates the risk of surface contamination within vehicle cabins. This public health consideration drives the integration of advanced silver-ion and zinc-based additive technologies directly into interior polymer compounding formulations during the manufacturing stage. Consequently, high-touch interior components transition from passive structural elements into active, self-sanitizing surfaces that continuously inhibit bacterial replication.

Fleet operators utilizing these advanced self-cleaning polymers achieve enhanced vehicle cleanliness standards and reduce the operational downtime associated with frequent manual cabin sanitization protocols. This specialized compounding capability allows chemical formulation enterprises to deliver highly customized, premium interior plastics tailored to the precise sanitation needs of high-frequency shared mobility assets. Over the long term, this hygiene-focused material evolution accelerates specialty additive consumption and expands commercial revenue streams within the global polymer industry.

Electric Vehicle Plastics Market Size and Share Analysis:

The electric vehicle plastics market is projected to grow from US$ 5.12 billion in 2025 to US$ 23.98 billion by 2033, registering a CAGR of 21.3% from 2026 to 2033.

By type, the PP accounts for a significant share due to its exceptionally low material density, structural versatility, and optimized production cost profiles when deployed in high-volume injection-molded components throughout passenger cabins and exterior structures.

By application, the dashboard leads the market owing to its substantial physical volume requirements, complex multi-component assembly architecture, and the expanding deployment of integrated electronic displays that require precise polymer housing configurations.

Electric Vehicle Plastics Market Report Highlights:

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

BASF

LyondellBasell

SABIC

Dow

DuPont

Covestro

Solvay

DSM

LG Chem

Toray

Get more information on this report

Electric Vehicle Plastics Market Report Coverage and Deliverables:

The "Electric Vehicle Plastics Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all key market segments covered under the scope

Market trends, along with market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key trends, global and regional frameworks, major players, regulations, and recent developments

Industry landscape and competitive analysis covering market concentration, heat map analysis, prominent players, and recent developments

Detailed company profiles, including SWOT analysis

Electric Vehicle Plastics Market Geographic Insights:

The electric vehicle plastics market shows diverse regional adoption patterns influenced by localized chemical processing infrastructures, vehicle assembly plant automation levels, and regional circular economy mandates. Global development remains uneven, with highly industrialized manufacturing corridors exhibiting rapid automated polymer processing transitions while developing territories encounter technical precision tooling limitations. The variance in local raw monomer availability and regional recycling infrastructure investments further fragments the global landscape, creating distinct geographic ecosystems for technical compound innovation.

North American deployment is characterized by large-scale consumer light-truck electrification initiatives and a distinct corporate preference for high-strength, impact-resistant thermoplastic polyolefins. Corporate automotive entities in this region drive manufacturing volumes through centralized assembly plants designed to mass-produce oversized passenger and fleet utility vehicles. Federal supply chain circularity targets incentivize localized polymer compounding, forcing an emphasis on establishing robust regional chemical recycling networks to supply post-consumer resins back into manufacturing pipelines.

The Asia Pacific region demonstrates leadership through extensive petrochemical processing infrastructure, dominant injection molding tooling ecosystems, and aggressive state investments in high-volume passenger electric vehicle production lines. High industrial concentration across key economic zones accelerates the expanding deployment of precision engineering polyamides and optical polycarbonates for local electronics integration. Local compounding enterprises benefit from direct proximity to major battery manufacturing hubs, enabling rapid co-development of customized flame-retardant enclosures.

European markets progress rapidly under the influence of strict regional end-of-life vehicle directives and an intense engineering focus on utilizing bio-based and fully recyclable polymer composites. Emerging markets in Latin America and the Middle East represent developing frontiers where plastic utilization is tied to premium consumer car imports and initial localized fleet assembly ventures. These developing regions face slower initial technical polymer consumption volumes, though momentum builds as international manufacturers establish regional component molding operations.

Get more information on this report

Electric Vehicle Plastics Market Research Report Guidance:

The report includes qualitative and quantitative data in the electric vehicle plastics market across type, application, vehicle type, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by type, application, vehicle type, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Electric Vehicle Plastics Market News and Key Development:

The electric vehicle plastics market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In September 2025, Covestro announced a strategic cooperation agreement with Anko Optics to advance the use of transparent engineering plastics in electric vehicles. The collaboration focuses on innovative automotive glazing applications that can reduce vehicle weight and support next-generation EV designs.

In June 2026, LyondellBasell (LYB) and Toyota Motor Europe announced a recycled automotive plastics partnership focused on circular polymers. Under this initiative, the companies successfully scaled a mechanical recycling pipeline that transforms recovered end-of-life maritime waste into high-performance structural plastic compounds for upcoming commercial vehicles.

Key Sources Referred:

Society of Automotive EngineersInstitute of Electrical and Electronics Engineers (IEEE)European Automobile Manufacturers' Association (ACEA)Japan Automobile Manufacturers Association (JAMA)China Association of Automobile Manufacturers (CAAM)Indian Automotive Component Manufacturers Association (ACMA)International Energy Agency (IEA)Electric Drive Transportation Association (EDTA)International Road Transport Union (IRU)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Electric Vehicle Plastics Market

BASF

LyondellBasell

SABIC

Dow

DuPont

Covestro

Solvay

DSM

LG Chem

Toray

Frequently Asked Questions

How big is the Electric Vehicle Plastics Market?

The Electric Vehicle Plastics Market is valued at US$ 5.12 Billion in 2025, it is projected to reach US$ 23.98 Billion by 2033.

What is the CAGR for Electric Vehicle Plastics Market by (2026 - 2033)?

As per our report Electric Vehicle Plastics Market, the market size is valued at US$ 5.12 Billion in 2025, projecting it to reach US$ 23.98 Billion by 2033. This translates to a CAGR of approximately 21.3% during the forecast period.

What segments are covered in this report?

The Electric Vehicle Plastics Market report typically cover these key segments-

What is the historic period, base year, and forecast period taken for Electric Vehicle Plastics Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Electric Vehicle Plastics Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Electric Vehicle Plastics Market?

The Electric Vehicle Plastics Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

BASF

LyondellBasell

SABIC

Dow

DuPont

Covestro

Solvay

DSM

LG Chem

Toray

Who should buy this report?

The Electric Vehicle Plastics Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Electric Vehicle Plastics Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Electric Vehicle Plastics Market

Get Free Sample For Electric Vehicle Plastics Market