01

Market Summery

Executive Summary and Global Market Analysis

Electric vehicle on-board chargers are specialized electronic devices built into electric vehicles. They convert alternating current from external sources into direct current to charge the battery. These chargers are essential for safe and efficient power conversion, as they control voltage and current levels during charging. Manufacturers focus on designing efficient systems that reduce heat and energy loss when vehicles are plugged into the grid.

The global use of on-board chargers is driven by strict carbon reduction policies and the benefits of using standardized charging systems. More companies are switching to electric fleets as cities introduce rules that require cleaner vehicles for deliveries. New semiconductor materials also help make chargers smaller and lighter, so they fit better in compact vehicles.

Most consumer vehicles use mid-range power chargers, while heavy-duty vehicles are starting to use higher-capacity systems. Battery-electric vehicles are the main technology, with plug-in hybrids using smaller chargers for their smaller batteries. Most purchases are for passenger vehicles, but commercial fleets are also growing as they look to reduce charging times.

Engineers are now using wide-bandgap semiconductor materials instead of traditional silicon to make chargers more efficient and heat-resistant. This change lets manufacturers build more powerful chargers without making them bigger. The market includes both large automotive suppliers and smaller companies that are developing advanced, two-way charging solutions.

03

Segment Analysis

Electric Vehicle On-Board Charger Market Segmentation

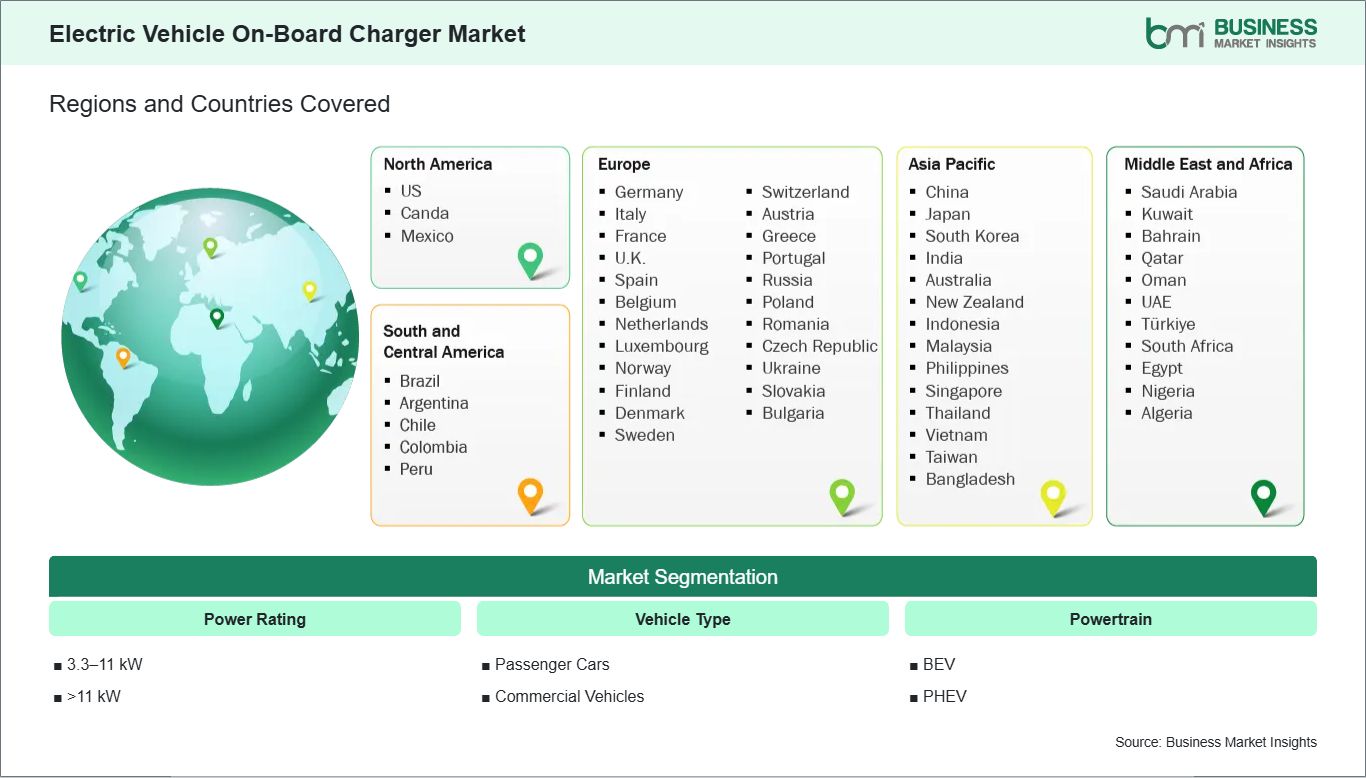

The electric vehicle on-board charger market is segmented based on power rating, vehicle type, and powertrain, reflecting the expanding deployment of advanced power conversion topologies across consumer transit applications and commercial logistics networks.

By Power Rating

- 3-11 kW: Standard power architectures deliver cost-effective charging speeds well-suited for overnight residential applications and workplace destination infrastructure.

- >11 kW: High-capacity multi-phase electronic conversion systems accelerate energy replenishment times for premium passenger platforms and heavy commercial fleets.

By Vehicle Type

- Passenger Cars: High-volume consumer transport applications integrate compact, lightweight power conversion hardware to optimize cabin space and driving range.

- Commercial Vehicles: Medium and heavy logistics platforms require ruggedized, high-power charging modules capable of enduring continuous duty cycles.

By Powertrain

- BEV: Purely electrified powertrains require high-capacity, highly efficient charging units to manage large onboard energy storage reservoirs.

- PHEV: Dual-source propulsion configurations utilize downscaled, cost-optimized conversion systems tailored for smaller battery capacities and short-range operation.

04

Market Forces

Electric Vehicle On-Board Charger Market Drivers and Opportunities

EV adoption and purchase incentives

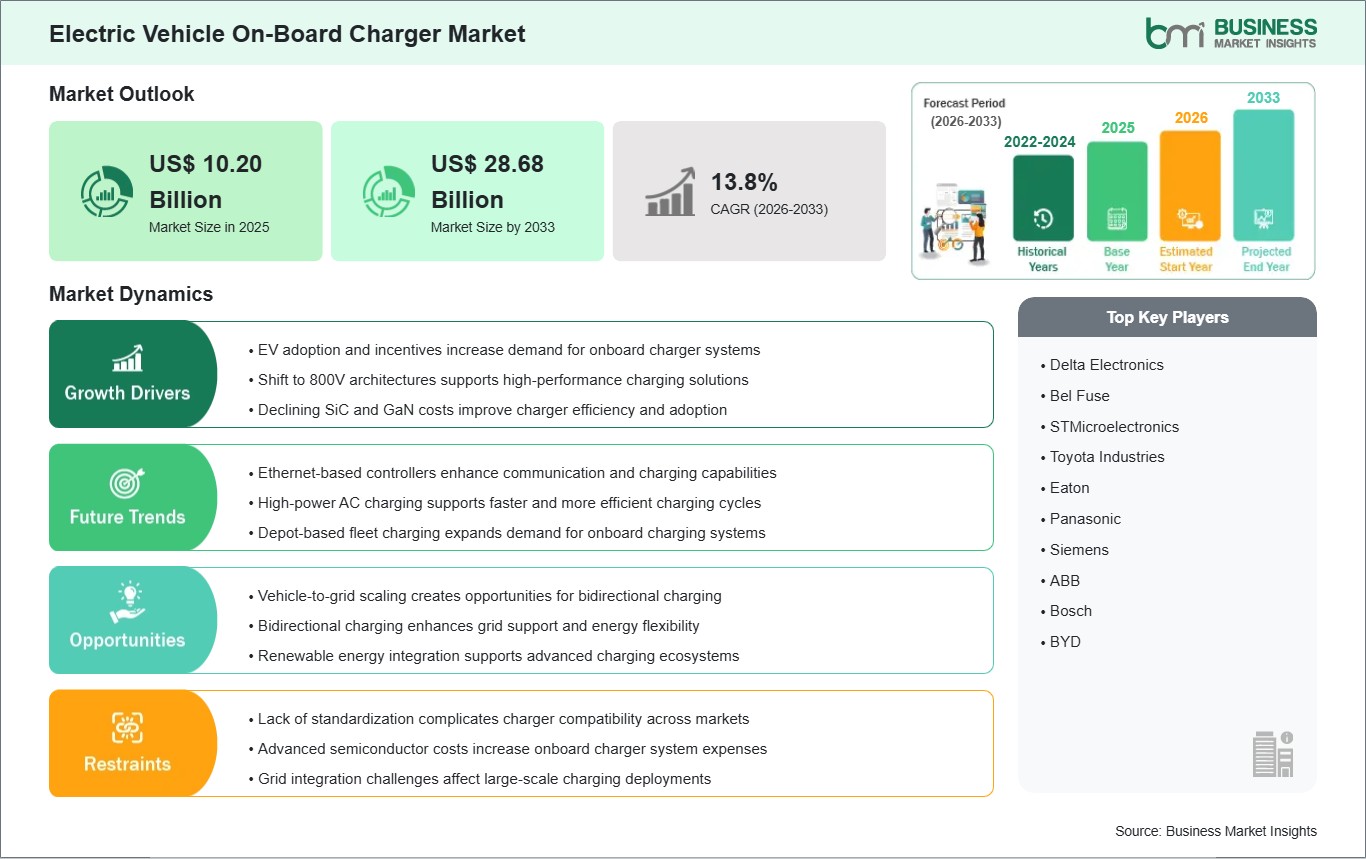

Regulatory bodies globally have been employing strong financial incentives and tax breaks for vehicle acquisitions in order to encourage consumer uptake of zero-emission vehicles. Such regulatory measures necessitate that the buyer move from conventional internal combustion engines to electric alternatives. As a result, there is a need for manufacturers to expand production in order to meet the demands of this market, taking advantage of the subsidies offered by consumers.

The pressure to meet strict regional carbon reduction targets in fleets means that logistics firms and public transit agencies have to realign vehicle acquisition programs to incorporate appropriate facilities for depot infrastructure. The resultant economic incentive has transformed such decisions into economically wise moves as far as different modes of transport are concerned. Finally, these aggressive government buying incentives will alter consumer buying patterns altogether towards electric vehicles.

Vehicle-to-grid scaling

The development of bidirectional power electronics technology facilitates the development of vehicle-to-grid conversion systems capable of returning electrical energy from the battery system to local utility grids. Such an advancement distinguishes stationary vehicles as more than mere electricity consumers but as distributed electricity generators that support grid stability. Thus, one aspect of using these cars results in their functionality becoming more of a two-way energy storage device.

Power grid operators who take advantage of such interconnected battery-powered cars have improved capabilities to manage peak load demands as well as access to secondary electricity storage systems when faced with abnormal peak loads. In turn, advancements in such technologies enable manufacturers of power electronics devices to supply advanced bidirectional charging equipment according to modern communication requirements of smart grids. Eventually, such cooperation helps in increasing the value of hardware equipment used by energy-efficient vehicle owners.

05

Size and Share Analysis

Electric Vehicle On-Board Charger Market Size and Share Analysis

The electric vehicle on-board charger market is projected to grow from US$ 10.20 billion in 2025 to US$ 28.68 billion by 2033, registering a CAGR of 13.8% from 2026 to 2033.

By power rating, the 3.3-11 kW accounts for a significant share due to the widespread installation of residential destination infrastructure and the standard configuration of these capacity systems within mid-market consumer vehicles.

By vehicle type, the passenger cars leads the market owing to the high-volume production scale of consumer platforms and the rapid implementation of residential charging solutions across major metropolitan areas.

07

Report Coverage

Electric Vehicle On-Board Charger Market Report Coverage and Deliverables

The "Electric Vehicle On-Board Charger Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

- Market size and forecast at global, regional, and country levels for all key market segments covered under the scope

- Market trends, along with market dynamics such as drivers, restraints, and key opportunities

- Market analysis covering key trends, global and regional frameworks, major players, regulations, and recent developments

- Industry landscape and competitive analysis covering market concentration, heat map analysis, prominent players, and recent developments

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Electric Vehicle On-Board Charger Market Geographic Insights

The electric vehicle on-board charger market shows diverse regional adoption patterns influenced by localized utility grid infrastructure, residential parking configurations, and regional green transit mandates. Global development remains uneven, with highly urbanized economic zones exhibiting rapid high-power electronic upgrades while rural territories encounter distribution network limitations. The variance in vehicle manufacturing localization policies and domestic silicon carbide fabrication lines further fragments the global landscape, creating distinct technical ecosystems for vehicle power management hardware.

North American deployment is characterized by large-scale consumer SUV electrification trends and a distinct corporate preference for higher power charging configurations to match expansive battery pack capacities. Corporate automotive giants in this region drive manufacturing volumes through specialized domestic gigafactories focused on extended-range light trucks. Federal supply chain directives incentivize local assembly, forcing an emphasis on establishing domestic semiconductor processing facilities to secure critical electrical components.

The Asia Pacific region demonstrates leadership through massive automotive assembly infrastructure, dominant power electronics supply chains, and aggressive government deployment of public alternating current infrastructure. High urban density across major municipal centers accelerates the utilization of cost-effective, highly integrated charging modules optimized for compact passenger commuter platforms. Local component fabricators benefit from streamlined domestic access to refined raw semiconductor materials, allowing swift development of high-efficiency silicon devices.

European markets progress rapidly under the influence of stringent regional carbon compliance penalties and the widespread consumer preference for high-capacity three-phase electrical systems. Emerging markets in Latin America and the Middle East represent nascent territories where adoption is tied to premium urban transport imports and initial localized fleet utility testing. These developing regions face slower initial electronic hardware sales, though momentum builds as public charging infrastructure projects extend beyond core capital cities.

10

Industry Activity

Recent Developments

The electric vehicle on-board charger market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

- In May 2026, Fraunhofer IZM announced that it is leading a European consortium, including semiconductor giant Infineon, under the EU-funded HiPower 5.0 project. The initiative is developing an ultra-compact 22-kilowatt on-board charger featuring monolithically integrated, bidirectional gallium nitride (GaN) switches to drastically reduce the traditional component volume down to just 4 liters.

- In June 2026, Graphion Energy Solutions today announced the launch of EWave, an electric two-wheel fleet platform designed specifically for Southeast Asia's high-utilization urban delivery and mobility markets.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

Society of Automotive Engineers Institute of Electrical and Electronics Engineers (IEEE) European Automobile Manufacturers' Association (ACEA) Japan Automobile Manufacturers Association (JAMA) China Association of Automobile Manufacturers (CAAM) Indian Automotive Component Manufacturers Association (ACMA) International Energy Agency (IEA) Electric Drive Transportation Association (EDTA) International Road Transport Union (IRU) Company Websites Company Annual Reports Company Investor Presentations