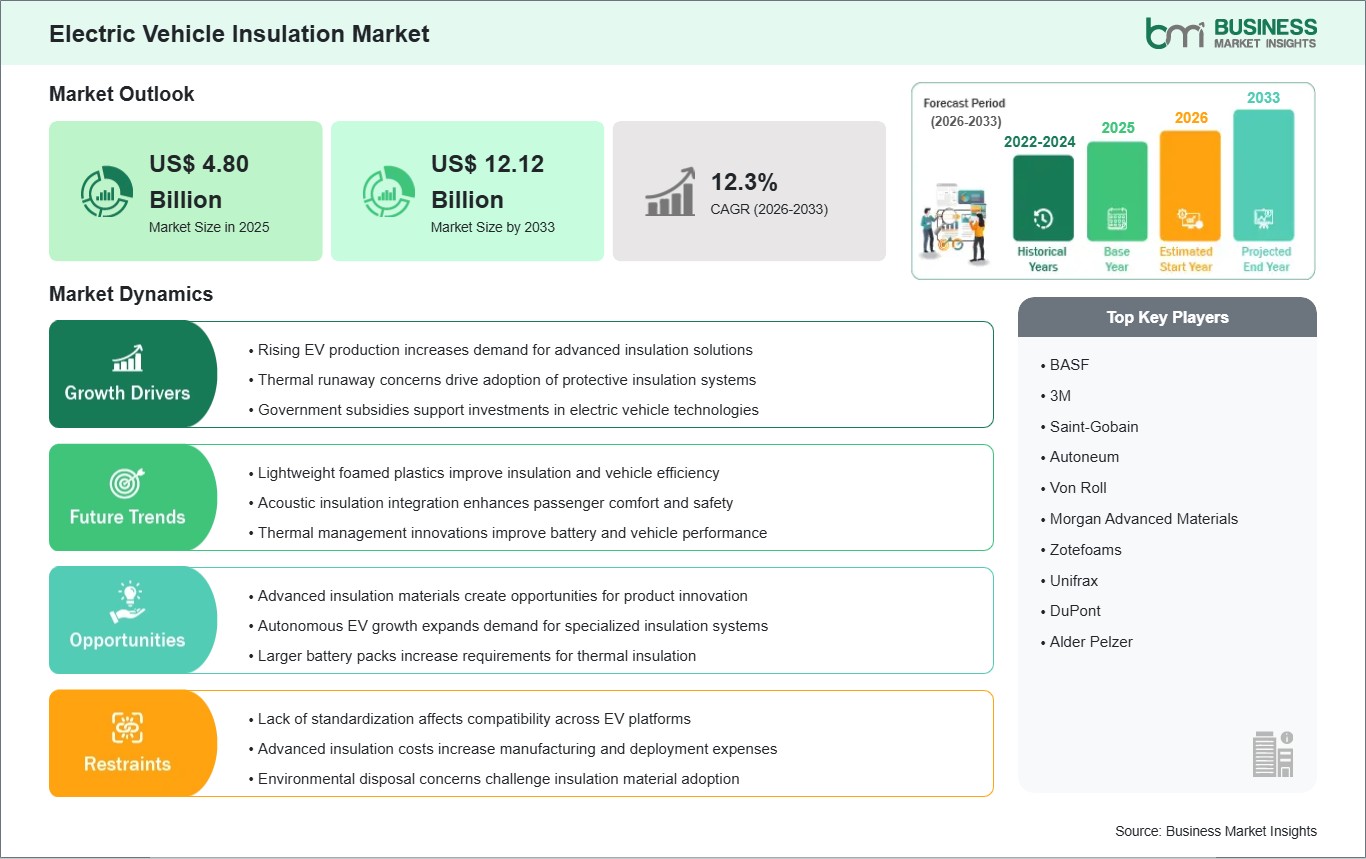

The electric vehicle insulation market size is expected to reach US$ 12.12 billion by 2033 from US$ 4.80 billion in 2025. The market is estimated to record a CAGR of 12.3% from 2026 to 2033.

Executive Summary and Global Market Analysis:

EV insulation involves the utilization of high-tech thermal insulation materials, dielectric barriers, and noise shields designed specifically to manage heat conditions inside the vehicle and insulate the circuits that carry high-voltage power in electrified cars. These novel insulation materials have replaced the insulation systems used on traditional internal combustion cars, helping protect against any thermal runaway incidents as well as controlling the acoustic signature of EVs.

The widespread acceptance of such innovations results from stringent manufacturing guidelines requiring greater vehicle safety during operation and the increased structural longevity offered through superior flame-retardant barriers. The trend towards fleet electrification is fueled by the investments made by global shippers and transportation firms into sustainable zero-emission transport systems that adhere to company environmental policies. New developments in material science help prevent cell-to-cell heat transfer in battery systems.

Thermal interface materials command a substantial footprint within high-voltage component assemblies, while foamed plastics and ceramic elements expand their presence in acoustic cabin linings and high-temperature localized barriers. Battery-powered propulsion systems represent the primary technology pathway, supplemented by plug-in hybrid systems that require dual-purpose insulation arrays capable of shielding both internal combustion machinery and electrical storage cells. Battery packs dictate the bulk of initial procurement volumes, whereas interior cabin components and under-bonnet systems remain crucial developing sectors focused on sound isolation and auxiliary component protection.

Automotive engineering transitions toward highly integrated structural cell-to-pack configurations, moving away from modular battery architectures to maximize energy density within the vehicle chassis. This structural shift allows manufacturers to optimize packaging constraints, requiring ultra-thin insulation barriers that deliver high dielectric strength without expanding physical volume boundaries. The competitive landscape features a mix of established global material conglomerates leveraging scaled chemical processing plants and specialized polymer innovators introducing highly advanced, customizable lightweight shielding solutions.

Electric Vehicle Insulation Market - Strategic Insights:

Get more information on this report

Electric Vehicle Insulation Market Segmentation Analysis:

The electric vehicle insulation market is segmented based on product type, application, and propulsion, reflecting the expanding deployment of advanced thermal barriers and dielectric materials across diversified passenger and commercial electrified transport networks.

By Product Type

TIM: Highly conductive gap fillers and pads transfer heat efficiently away from sensitive battery cells to integrated cooling plates.

Foamed Plastic: Lightweight polyurethane and polyolefin foams provide critical impact absorption, lightweight structure, and structural acoustic dampening inside passenger cabins.

Ceramic: Ultra-high-temperature resistant ceramic sheets deliver exceptional flame-retardant barriers between battery cells to prevent catastrophic thermal propagation events.

By Application

Battery Pack: Comprehensive thermal and electrical encapsulation shields individual energy storage cells from external environment impacts and localized thermal spikes.

Interior: Specialized acoustic and thermal liners insulate passenger cabins from exterior road noise while reducing HVAC energy consumption loads.

Under Bonnet: High-durability insulation wraps safeguard auxiliary power electronics, power inverters, and high-voltage cabling systems from localized environmental stresses.

By Propulsion

BEV: Pure electric drivetrains require extensive, multi-layered dielectric and thermal insulation arrays to manage expansive high-voltage energy storage systems.

PHEV: Dual-source vehicle architectures utilize compact insulation configurations designed to withstand both internal combustion engine heat and electrical current fluctuations.

Electric Vehicle Insulation Market Drivers and Opportunities:

Rising EV production

Automotive assembly plants globally are scaling their manufacturing capabilities to satisfy accelerating consumer demands for zero-emission transportation alternatives. This industrial expansion compels original equipment manufacturers to secure vast quantities of high-durability thermal barriers and dielectric shields to maintain high-throughput manufacturing schedules. Consequently, specialized material processing facilities must accelerate their production outputs to align with the high-volume vehicle assembly rates across key international manufacturing zones.

Strict national transport decarbonization targets are forcing automotive companies to shift their manufacturing to electric vehicle platforms. This systemic, industrial transformation of the auto-parts supply chain means that in purchasing, the conversation is moving away from shielding for the internal combustion engine to high-voltage insulation systems. Overall, the industrial insulation sector sees a permanent change in terms of volume of manufacturing and the nature of raw material consumption toward dedicated E.V. applications.

Development of advanced insulation materials

The continuing shift to high-voltage architectures, 800-volt battery systems, for instance, also presents thermal challenges, as well as a heightened risk of high-energy electrical arcing in powertrain compartments. These conditions have driven the development of new chemistries and have made it possible for composites, aerogels, and phase-change materials to provide better thermal protection. Our engineers wanted to ditch the heavy, bulky fiberglass shields used in the past in favor of something lighter-weight and more performant on a molecular level.

This unique material capability allows chemical processors to offer insulation options that fit precisely around the contours of the tight battery cabinets. These unique chemical architectures allow manufacturers to maximize flame-retardant capability and energy-density optimization. In the long run, this progression of materials will boost the consumption of advanced polymers in the technical automotive components industry as a whole, and ultimately increase overall market revenues.

Electric Vehicle Insulation Market Size and Share Analysis:

The electric vehicle insulation market is projected to grow from US$ 4.80 billion in 2025 to US$ 12.12 billion by 2033, registering a CAGR of 12.3% from 2026 to 2033.

By product type, the TIM accounts for a significant share due to the immediate necessity for continuous heat dissipation from high-power battery cells during rapid charging cycles and heavy operational acceleration phases.

By application, the battery pack leads the market owing to the compounding factors of critical thermal runaway protection requirements and the expanding deployment of dense cell configurations that necessitate comprehensive electrical isolation.

Electric Vehicle Insulation Market Report Highlights:

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

BASF

3M

Saint-Gobain

Autoneum

Von Roll

Morgan Advanced Materials

Zotefoams

Unifrax

DuPont

Alder Pelzer

Get more information on this report

Electric Vehicle Insulation Market Report Coverage and Deliverables:

The "Electric Vehicle Insulation Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all key market segments covered under the scope

Market trends, along with market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key trends, global and regional frameworks, major players, regulations, and recent developments

Industry landscape and competitive analysis covering market concentration, heat map analysis, prominent players, and recent developments

Detailed company profiles, including SWOT analysis

Electric Vehicle Insulation Market Geographic Insights:

The electric vehicle insulation market shows diverse regional adoption patterns influenced by localized automotive manufacturing capacities, regional supply chain maturity, and localized industrial safety standards. Global development remains uneven, with established manufacturing zones exhibiting rapid automated line integration for advanced materials while emerging markets encounter technical scaling constraints. The variance in chemical manufacturing localization subsidies and raw materials processing capabilities further fragments the global landscape, creating distinct geographic ecosystems for technical material innovation.

North American deployment is characterized by large-scale consumer utility vehicle transitions and a distinct corporate preference for heavy-duty, crash-resistant structural foam insulation arrays. Corporate automotive entities in this region drive production volume through centralized manufacturing hubs aimed at mass-producing large light-truck and sport utility platforms. Federal supply chain directives incentivize domestic component production, forcing an emphasis on establishing robust domestic chemical processing facilities to secure localized critical insulation materials.

The Asia Pacific region demonstrates leadership through extensive polymer processing infrastructure, dominant battery cell manufacturing corridors, and aggressive government investments in high-volume passenger car assembly lines. High component density across regional manufacturing clusters accelerates the expanding deployment of precision thermal interface sheets and micro-cellular foam structures. Local material suppliers benefit from direct proximity to massive battery assembly infrastructure, enabling rapid co-development of custom dielectric barriers.

European markets progress rapidly under the influence of stringent regional safety classifications and an intense vehicle engineering focus on utilizing lightweight recyclable foamed plastics to satisfy circular economy mandates. Emerging markets in Latin America and the Middle East represent developing territories where insulation consumption is tied to premium vehicle imports and initial localized fleet assembly joint ventures. These developing regions face slower initial volume growth, though momentum builds as international manufacturers establish regional component assembly operations.

Get more information on this report

Electric Vehicle Insulation Market Research Report Guidance:

The report includes qualitative and quantitative data in the electric vehicle insulation market across product type, application, propulsion, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by product type, application, propulsion, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Electric Vehicle Insulation Market News and Key Development:

The electric vehicle insulation market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In October 2025, Axalta Coating Systems announced the launch of Alesta e-PRO FG Black and Alesta e-PRO Dielectric Gray, new coating solutions engineered to provide enhanced electrical insulation and extreme heat protection for electric vehicle battery applications. The products were introduced to improve battery safety and insulation performance in EVs.

In June 2025, Alkegen announced the start of full-scale commercial production of its proprietary fiber-enhanced aerogel insulation for electric vehicle battery fire protection. The company stated that the material is designed to help OEMs mitigate thermal runaway risks and improve battery pack insulation performance.

Key Sources Referred:

Society of Automotive EngineersInstitute of Electrical and Electronics Engineers (IEEE)European Automobile Manufacturers' Association (ACEA)Japan Automobile Manufacturers Association (JAMA)China Association of Automobile Manufacturers (CAAM)Indian Automotive Component Manufacturers Association (ACMA)International Energy Agency (IEA)Electric Drive Transportation Association (EDTA)International Road Transport Union (IRU)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Electric Vehicle Insulation Market

BASF

3M

Saint-Gobain

Autoneum

Von Roll

Morgan Advanced Materials

Zotefoams

Unifrax

DuPont

Alder Pelzer

Frequently Asked Questions

How big is the Electric Vehicle Insulation Market?

The Electric Vehicle Insulation Market is valued at US$ 4.80 Billion in 2025, it is projected to reach US$ 12.12 Billion by 2033.

What is the CAGR for Electric Vehicle Insulation Market by (2026 - 2033)?

As per our report Electric Vehicle Insulation Market, the market size is valued at US$ 4.80 Billion in 2025, projecting it to reach US$ 12.12 Billion by 2033. This translates to a CAGR of approximately 12.3% during the forecast period.

What segments are covered in this report?

The Electric Vehicle Insulation Market report typically cover these key segments-

Product Type (TIM, Foamed Plastic, Ceramic)

Application (Battery Pack, Interior, Under Bonnet)

Propulsion (BEV, PHEV)

What is the historic period, base year, and forecast period taken for Electric Vehicle Insulation Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Electric Vehicle Insulation Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Electric Vehicle Insulation Market?

The Electric Vehicle Insulation Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

BASF

3M

Saint-Gobain

Autoneum

Von Roll

Morgan Advanced Materials

Zotefoams

Unifrax

DuPont

Alder Pelzer

Who should buy this report?

The Electric Vehicle Insulation Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Electric Vehicle Insulation Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Electric Vehicle Insulation Market

Get Free Sample For Electric Vehicle Insulation Market