01

Market Summery

Executive Summary and Global Market Analysis

Electric vehicle adhesives are specialized materials used for bonding, sealing, and managing heat in electric cars. They replace traditional mechanical fasteners, providing strong support and helping to build high-voltage battery packs and electronic control units more efficiently. Car makers are using these materials more often to meet insulation needs and handle the heat challenges found in today's electric vehicles.

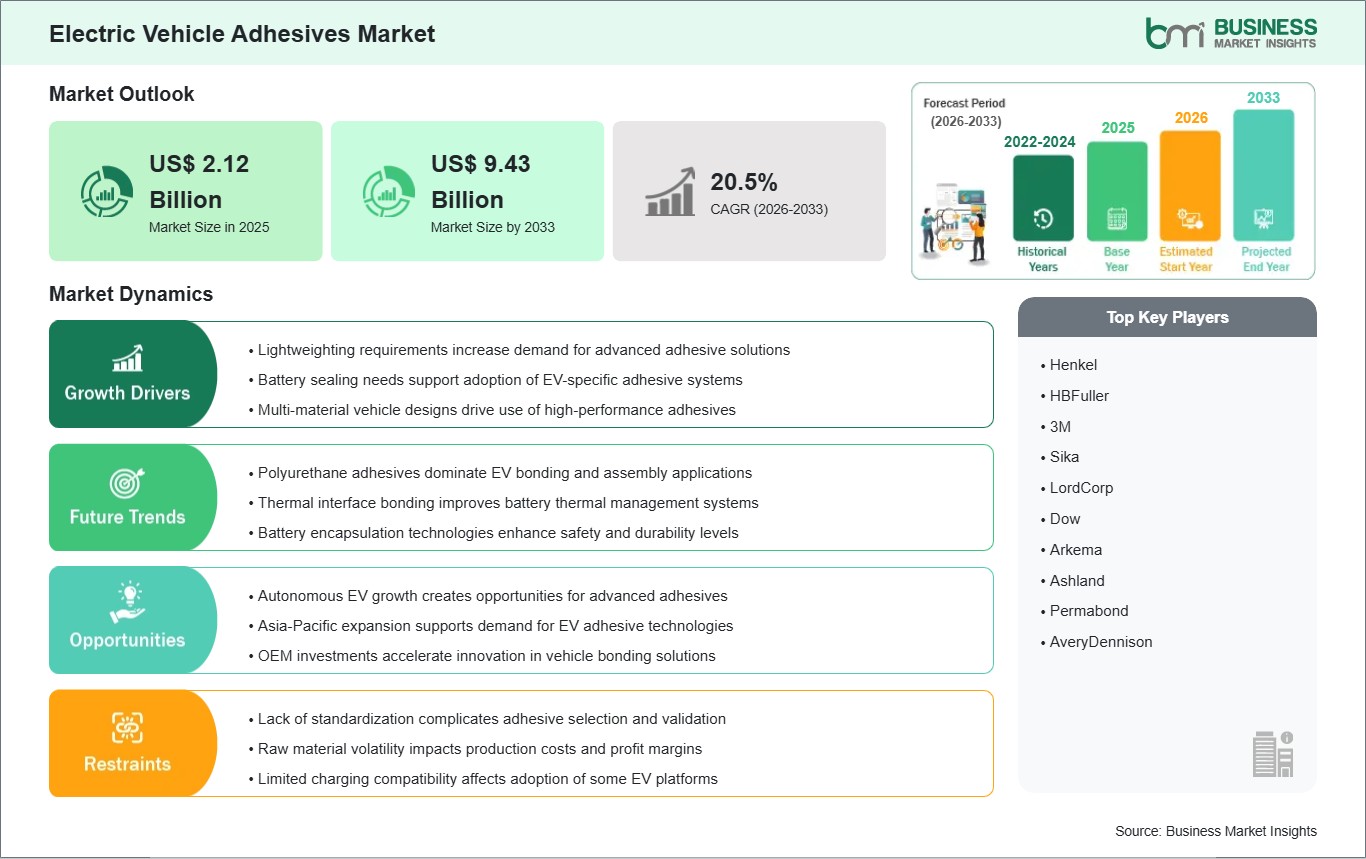

Global use is driven by stringent policies implemented by firms regarding weight loss and the durable nature of the structures developed due to the uniform distribution of stresses in bonded joints. The development and implementation of electric propulsion systems is becoming more prevalent as stringent international regulations drive the need to enhance the overall range of operations and efficiencies of the vehicles developed. Moreover, recent progress made in the development of the formulas used in structural adhesives makes them suitable for high-voltage component housings.

Powertrains form a large percentage of the components assembled, while optical and sensing components increase their dominance in advanced intelligent driver assistance systems. Polyurethane and epoxy technologies lead in the use of adhesives, supported by silicon-based adhesives used due to their thermal dissipation and waterproofing qualities. Passenger cars form the largest consuming segment, while heavy commercial and public transport form emerging markets, emphasizing their structural longevity.

Automotive engineering transitions toward dedicated multi-material architectures, moving away from uniform steel chassis designs to incorporate lightweight aluminum alloys and carbon composites. This structural shift allows manufacturers to optimize component placement, requiring specialized bonding materials to prevent galvanic corrosion between dissimilar substrates. The competitive landscape features a mix of established global chemical conglomerates leveraging scaled synthesis capacity and specialized formulation pioneers introducing highly customized, rapid-curing structural bonding solutions.

03

Segment Analysis

Electric Vehicle Adhesives Market Segmentation

The electric vehicle adhesives market is segmented based on vehicle type, resin type, and application, reflecting the expanding deployment of specialized bonding, sealing, and thermal management formulations across diversified electrified transportation ecosystems.

By Vehicle Type

- Passenger Cars: High-volume manufacturing lines utilize automated bonding systems to secure battery cells and electronic modules in consumer vehicles.

- Commercial EVs: Medium and heavy distribution fleets rely on high-durability structural adhesives to withstand persistent vibrational stresses.

- Buses: Large-scale municipal transit platforms require extensive sealing and heavy-duty structural bonding for roof-mounted battery packs.

By Resin Type

- Epoxy: Structural formulations deliver exceptional mechanical strength, chemical resistance, and rigid bonding capabilities for load-bearing battery enclosures.

- Polyurethane: Flexible compound structures provide superior impact resistance and essential thermal conductivity needed for battery pack cell-to-pack bonding.

- Silicone: High-temperature elastomeric sealants offer unmatched moisture protection and excellent dielectric properties for sensitive high-voltage control units.

- Acrylic: Rapid-curing bonding solutions accelerate assembly line throughput by adhering efficiently to diverse metal and plastic substrates without primers.

By Application

- Powertrain System: Thermal interface materials and structural bonding compounds secure battery cells, inverters, and electric motors against extreme thermal cycling.

- Optical Element: Optically clear adhesive solutions provide precise, distortion-free bonding for advanced heads-up displays and instrument cluster glass panels.

- Sensors: Encapsulating sealants protect critical radar, lidar, and camera modules from moisture ingress, thermal shock, and environmental contaminants.

- Body Frame: High-modulus structural adhesives join multi-material lightweight body panels, enhancing crashworthiness and reducing overall vehicle weight.

04

Market Forces

Electric Vehicle Adhesives Market Drivers and Opportunities

Lightweighting demand

Globally, regulators are enforcing a strict set of fleet efficiency regulations on vehicle manufacturers to increase the distance an electric vehicle can travel on a single charge. As a result, automotive engineers are under pressure to remove the use of large metal fasteners, which in turn requires vehicle weight to be optimized as soon as possible throughout the vehicle engineering process. Likewise, manufacturing companies have a duty to expedite changing over to advanced chemical bonding processes so that they can meet the regulations in place, while also meeting consumers' expectations of vehicle range.

In order for automotive companies to comply with these efficiency regulations, they are making significant changes to the design of their vehicles' structures by creating composite body designs and using more than one type of material in their vehicle's construction (e.g., aluminum, composites). This engineering change to begin utilizing adhesive bonding has turned adhesive bonding into an enabler to create a more structurally sound vehicle than if traditional assembly methods were utilized. As a result of these structural weight-reducing initiatives, the previous methods of assembling components will be altered for the entire automotive industry by utilizing high-performance bonding materials in their construction processes.

Growth in autonomous EVs

The transition toward self-driving electrified platforms enables the integration of extensive sensor suites, radar modules, telematics systems, and complex onboard computing units. This technological innovation separates traditional mechanical driving systems from digitized navigation architectures, allowing software to dictate vehicle pathing through continuous data collection. Consequently, a single autonomous platform requires thousands of delicate electronic connections that must remain perfectly insulated from external environmental interferences.

Manufacturers utilizing these intricate electronic arrays achieve unprecedented data processing accuracy but require specialized non-conductive potting compounds and low-stress encapsulants to protect fragile circuitry. This technological requirement allows specialty chemical companies to deliver highly advanced adhesive solutions tailored to the precise signal-integrity needs of autonomous guidance hardware. Over the long term, this computational evolution accelerates specialized formulation consumption and expands the total market value within the electronics assembly sector.

05

Size and Share Analysis

Electric Vehicle Adhesives Market Size and Share Analysis

The electric vehicle adhesives market is projected to grow from US$ 2.12 billion in 2025 to US$ 9.43 billion by 2033, registering a CAGR of 20.5% from 2026 to 2033.

By vehicle type, the passenger cars accounts for a significant share due to the exponential rise of global consumer electric vehicle procurement and the subsequent pressure on high-volume manufacturing facilities to deploy automated bonding solutions for rapid battery pack assembly and structural body integration.

By resin type, the polyurethane leads the market owing to the compounding benefits of high impact absorption, exceptional flexibility, and reliable thermal conductivity required to manage heat dissipation effectively between individual battery cells and cooling plates within high-capacity energy storage modules.

07

Report Coverage

Electric Vehicle Adhesives Market Report Coverage and Deliverables

The "Electric Vehicle Adhesives Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

- Market size and forecast at global, regional, and country levels for all key market segments covered under the scope

- Market trends, along with market dynamics such as drivers, restraints, and key opportunities

- Market analysis covering key trends, global and regional frameworks, major players, regulations, and recent developments

- Industry landscape and competitive analysis covering market concentration, heat map analysis, prominent players, and recent developments

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Electric Vehicle Adhesives Market Geographic Insights

The electric car adhesives industry witnesses different trends of adoption across various regions based on their manufacturing processes, charging station development, and engineering standards in the automotive field. Development of the global market is not equal; while highly industrialized areas are experiencing fast development of automated assembly, the less developed areas are having challenges during mass production. In addition to this difference in subsidies for clean energy production and processing of chemicals, there are various geographic hubs for automotive formulary development.

North American deployment is characterized by large-scale commercial vehicle electrification contracts and a distinct corporate preference for high-strength, crash-resistant structural body bonding formulations. Corporate automotive giants in this region drive manufacturing volume through centralized gigafactories aimed at mass-producing high-capacity consumer trucks and sport utility platforms. Federal manufacturing initiatives incentivize local component sourcing, forcing an emphasis on establishing robust domestic chemical supply chains to support regional battery enclosure assembly facilities.

The Asia Pacific region demonstrates leadership through extensive electronics manufacturing ecosystems, dominant battery cell supply chains, and aggressive government investments in electrified public transit networks. High electronic component density across regional manufacturing corridors accelerates the expanding deployment of precision potting resins and sensor-encapsulating sealants. Local adhesive formulators benefit from direct proximity to major battery cell manufacturers, enabling rapid iteration and co-development of customized thermal interface materials.

European markets progress rapidly under the influence of stringent regional carbon reduction mandates and the widespread establishment of dedicated advanced automotive engineering research hubs. Emerging markets in Latin America and the Middle East represent developing frontiers where adoption is tied to initial premium passenger car imports and localized assembly joint ventures. These developing regions face slower initial compound consumption, though momentum builds as international manufacturers establish regional component assembly plants.

10

Industry Activity

Recent Developments

The electric vehicle adhesives market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

- In May 2026, Henkel AG & Co. KGaA announced that it added two new thermal interface materials to its EV portfolio-Loctite SI 5643 and Loctite SI 5637. These multi-functional potting and bonding adhesives were developed to address evolving fast-charging requirements and new cell-to-pack or cell-to-chassis structural architectures.

- In January 2026, Dow MobilityScience announced that its VORATRON MA 8300 adhesive system won the 2026 BIG Innovation Award. This advanced material acts as both a structural bonding agent and a high-performance thermal interface, streamlining battery pack assembly for electric vehicles and energy storage systems (ESS).

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

Society of Automotive Engineers Institute of Electrical and Electronics Engineers (IEEE) European Automobile Manufacturers' Association (ACEA) Japan Automobile Manufacturers Association (JAMA) China Association of Automobile Manufacturers (CAAM) Indian Automotive Component Manufacturers Association (ACMA) International Energy Agency (IEA) Electric Drive Transportation Association (EDTA) International Road Transport Union (IRU) Company Websites Company Annual Reports Company Investor Presentations