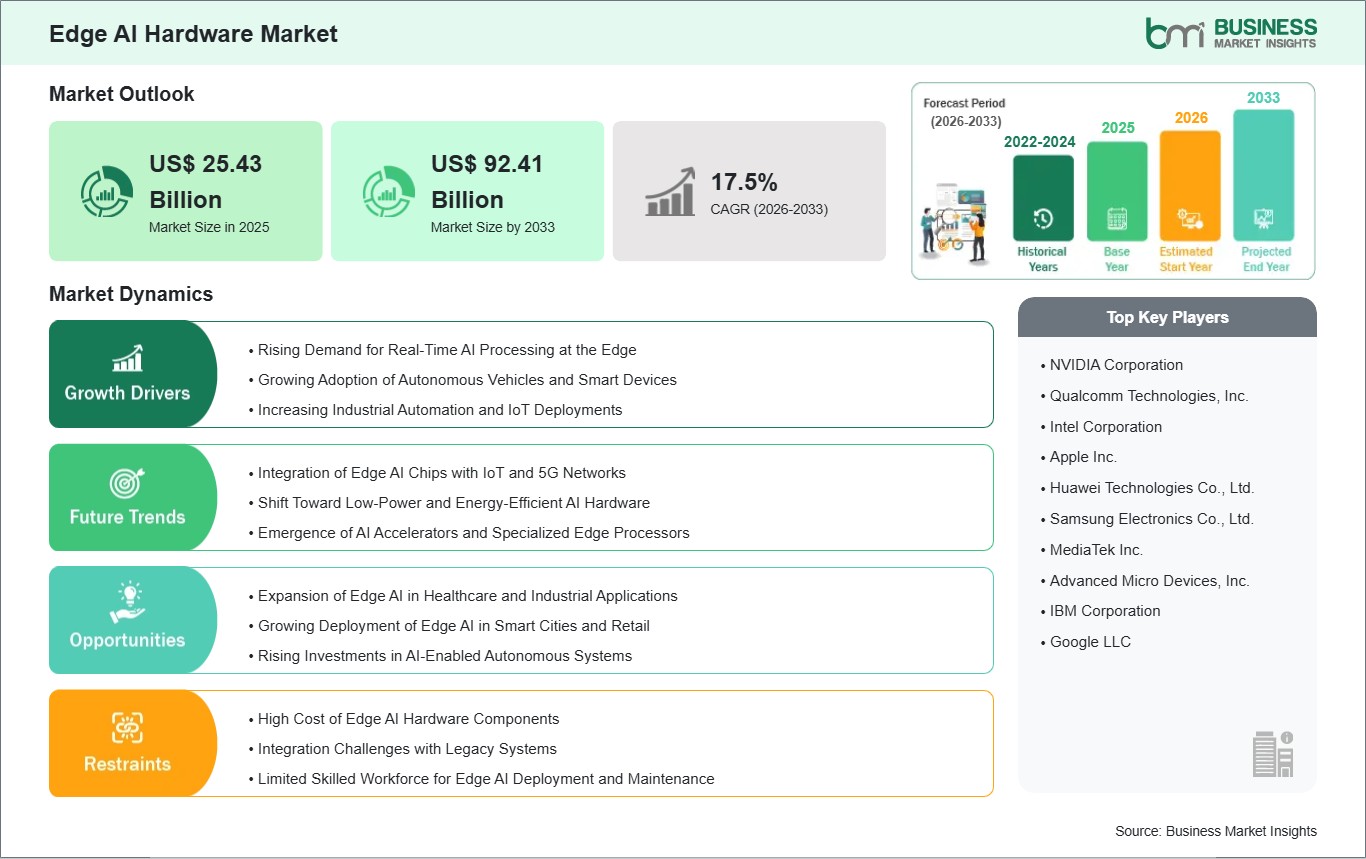

The Edge AI Hardware Market size is expected to reach US$ 92.41 Billion by 2033 from US$ 25.43 Billion in 2025. The market is estimated to record a CAGR of 17.50% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Edge AI hardware has emerged as a critical component in modern computing systems worldwide, enabling real-time data processing and intelligent decision-making at the edge of networks. Edge AI processors, AI accelerators, connectivity modules, memory, storage devices, and embedded hardware solutions are increasingly deployed in autonomous vehicles, industrial automation systems, smart cameras, IoT devices, and healthcare equipment, and these solutions have also gained significant adoption in telecom, retail, and consumer electronics applications. Edge AI hardware provides numerous advantages, including low-latency processing, reduced dependence on cloud computing, improved energy efficiency, and enhanced operational intelligence. Rising demand for intelligent edge applications, 5G deployment, and data privacy requirements have generated intense focus on deploying edge AI hardware.

However, the edge AI hardware market faces challenges that may slow its growth. These include high costs of advanced processors and accelerators, integration complexity with existing devices, and thermal management and power efficiency issues. Capital expenditure constraints, technology standardization gaps, and compatibility with legacy systems also affect market adoption. Despite these challenges, the edge AI hardware market offers significant growth opportunities, driven by increasing deployment in autonomous vehicles, industrial automation, smart retail, healthcare monitoring, and AI-enabled IoT devices, along with the growing need for on-device AI processing.

Edge AI Hardware Market - Strategic Insights:

Get more information on this report

Edge AI Hardware Market Segmentation Analysis:

Key segments that contributed to the derivation of the edge AI hardware market analysis are component, and end-user industry.

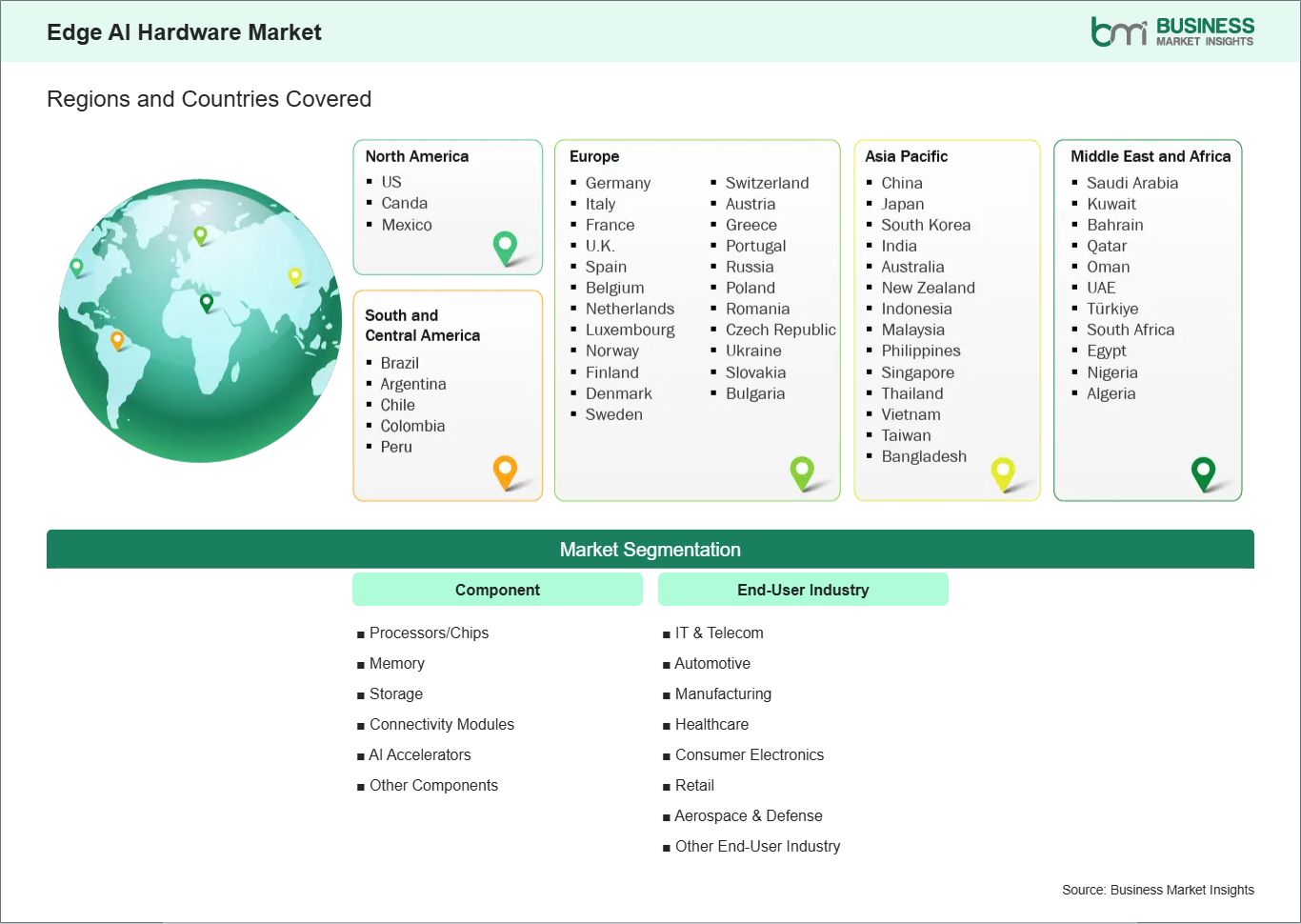

By component, the edge AI hardware market is bifurcated into processors/chips, memory, storage, connectivity modules, AI accelerators, and others. Processors/chips held a significant share in 2025.

By end-user industry, the edge AI hardware market is bifurcated into IT & telecom, automotive, manufacturing, healthcare, consumer electronics, retail, aerospace & defense, and other end-user industries. IT & telecom held a significant share in 2025.

Edge AI Hardware Market Drivers and Opportunities:

Growing Demand for Real-Time AI Processing at the Edge

The increasing need for low-latency, real-time AI computation is a key driver for the edge AI hardware market. Applications such as autonomous vehicles, smart cameras, industrial automation, and IoT devices require processing data locally to reduce reliance on cloud computing and ensure rapid decision-making. Rising adoption of 5G networks, AI-powered surveillance, and intelligent manufacturing systems is accelerating demand for high-performance processors, AI accelerators, and edge-specific hardware solutions. The need to enhance energy efficiency, reduce bandwidth usage, and maintain data privacy further strengthens the market growth for edge AI hardware globally.

Expansion of Edge AI in Industrial and Automotive Applications

The growing deployment of edge AI hardware in industrial automation and automotive sectors presents a significant growth opportunity. Industries are increasingly implementing smart factories, predictive maintenance systems, and robotics that rely on on-device AI processing for faster analytics and decision-making. Similarly, autonomous vehicles and ADAS (Advanced Driver Assistance Systems) require edge AI hardware for real-time perception, navigation, and safety monitoring. With rising investments in AI-enabled industrial IoT and smart mobility, manufacturers of edge AI processors, accelerators, and connectivity modules have substantial opportunities to expand their market presence and develop industry-specific solutions.

Edge AI Hardware Market Size and Share Analysis:

By component, the edge AI hardware market is segmented into processors/chips, memory, storage, connectivity modules, AI accelerators, and others. Processors/chips held a significant share in 2025 due to their widespread deployment across autonomous vehicles, industrial automation systems, smart cameras, and IoT devices, driven by strong demand for real-time AI computation, low-latency processing, and enhanced energy efficiency at the edge.

By end-user industry, the edge AI hardware market is segmented into IT & telecom, automotive, manufacturing, healthcare, consumer electronics, retail, aerospace & defense, and other end-user industries. IT & telecom held a significant share in 2025 due to the increasing deployment of edge AI devices to manage data-intensive applications, optimize network performance, and enable intelligent decision-making across enterprise and consumer networks.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

NVIDIA Corporation

Qualcomm Technologies, Inc.

Intel Corporation

Apple Inc.

Huawei Technologies Co., Ltd.

Samsung Electronics Co., Ltd.

MediaTek Inc.

Advanced Micro Devices, Inc.

IBM Corporation

Google LLC

Get more information on this report

Edge AI Hardware Market Report Coverage and Deliverables:

The "Edge AI hardware market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Edge AI hardware market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Edge AI hardware market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Edge AI hardware market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the edge AI hardware market

Detailed company profiles, including SWOT analysis

Edge AI Hardware Market Geographic Insights:

The geographical scope of the edge AI hardware market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The edge AI hardware market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific edge AI hardware market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The region is witnessing strong growth, driven by rapid industrialization, expansion of smart infrastructure, and increasing investments in AI-enabled devices and IoT systems. Major economies such as China, Japan, and India are leading market growth due to rising demand for edge AI processors, AI accelerators, smart cameras, and industrial automation hardware across IT, automotive, manufacturing, and healthcare sectors.

The region is also experiencing growing adoption of advanced edge AI hardware technologies, including AI chips, connectivity modules, and memory/storage solutions optimized for low-latency processing. Increasing emphasis on real-time data processing, energy-efficient AI computation, and edge intelligence, coupled with government initiatives supporting smart cities and Industry 4.0 adoption, is further boosting market demand. Additionally, rising investments in autonomous vehicles, smart factories, healthcare monitoring systems, and AI-driven consumer electronics are positioning Asia-Pacific as a key growth region in the global edge AI hardware market.

Get more information on this report

Edge AI Hardware Market Research Report Guidance:

The report includes qualitative and quantitative data in the edge AI hardware market across component, end-user industry, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the edge AI hardware market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the edge AI hardware market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the edge AI hardware market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover edge AI hardware market segments by component, end-user industry, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the edge AI hardware market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Edge AI Hardware Market News and Key Development:

The edge AI hardware market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the edge AI hardware market are:

In January 2026, Qualcomm Technologies, Inc. announced its expanded IoT product portfolio, including new Qualcomm Dragonwing Q-series processors. Complemented by new services and developer offerings and fueled by the acquisition of Augentix, Arduino, Edge Impulse, FocusAI, and Foundries.io in the last 18 months, Qualcomm Technologies is now positioned to address the needs of a much wider spectrum of IoT customers ranging from global enterprises to independent local developers, with the vision to become the provider of choice for core edge compute and AI technology across all industrial and embedded verticals.

In January 2026, Ambarella, Inc. (NASDAQ: AMBA), an edge AI semiconductor company, announced during CES the CV7 edge AI vision system-on-chip (SoC), which is optimized for a wide range of AI perception applications. Examples include advanced, AI-based 8K consumer products (e.g., action and 360-degree cameras), multi-imager enterprise security cameras, robotics (e.g. aerial drones), industrial automation and high-performance video conferencing devices. The CV7 is also ideal for multi-stream automotive designs—especially those running CNNs and transformer-based networks at the edge—such as AI vision gateways and hubs in fleet video telematics, 360-degree surround-view and video-recording applications, and passive driver assistance systems (ADAS). These applications can all leverage the CV7 for its simultaneous processing of multiple video streams up to 8Kp60 and exceptional image quality, in combination with high-performance edge AI and low power consumption.

In September 2025, ADLINK Technology Inc., a global leader in edge computing, proudly announces the launch of a comprehensive portfolio of industrial computing solutions built on Intel® Core™ 200S series processors. These new platforms deliver major gains in AI performance, energy efficiency, and I/O flexibility—empowering next-generation applications in industrial automation, infotainment, edge AI systems, and immersive computing.

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Edge AI Hardware Market

About Author— Electronics and Semiconductor Research Team

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the Edge AI Hardware Market?

The Edge AI Hardware Market is valued at US$ 25.43 Billion in 2025, it is projected to reach US$ 92.41 Billion by 2033.

What is the CAGR for Edge AI Hardware Market by (2026 - 2033)?

As per our report Edge AI Hardware Market, the market size is valued at US$ 25.43 Billion in 2025, projecting it to reach US$ 92.41 Billion by 2033. This translates to a CAGR of approximately 17.50% during the forecast period.

What segments are covered in this report?

The Edge AI Hardware Market report typically cover these key segments-

Component (Processors/Chips, Memory, Storage, Connectivity Modules, AI Accelerators, Other Components)

End-User Industry (IT & Telecom, Automotive, Manufacturing, Healthcare, Consumer Electronics, Retail, Aerospace & Defense, Other End-User Industry)

What is the historic period, base year, and forecast period taken for Edge AI Hardware Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Edge AI Hardware Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Edge AI Hardware Market?

The Edge AI Hardware Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

NVIDIA Corporation

Qualcomm Technologies, Inc.

Intel Corporation

Apple Inc.

Huawei Technologies Co., Ltd.

Samsung Electronics Co., Ltd.

MediaTek Inc.

Advanced Micro Devices, Inc.

IBM Corporation

Google LLC

Who should buy this report?

The Edge AI Hardware Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Edge AI Hardware Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Edge AI Hardware Market

Get Free Sample For Edge AI Hardware Market