01

Market Summery

Executive Summary and Global Market Analysis

District heating systems distribute thermal energy that is generated centrally through insulated pipelines to homes, businesses, and factories. These systems provide effective space heating and hot water while lowering the need for local combustion. By integrating centralized thermal infrastructure, we can use fuel more efficiently and support long-term energy planning in crowded urban areas.

Urban redevelopment programs and energy transition policies play a significant role in how these systems are deployed in both developed and developing economies. City governments are increasingly choosing centralized thermal distribution to boost energy efficiency and cut down emissions from standalone heating systems. Factories and mixed-use developments are also connecting to district heating systems to help manage energy more effectively over the long term.

The market shows a wide range of segments based on the heat source, plant setup, and application. Natural gas and biomass systems are used extensively due to how well they fit existing infrastructure and their ability to scale operations. Combined heat and power plants are also popular because they produce electricity and thermal energy at the same time, resulting in better fuel efficiency.

New technologies are changing how modern district heating networks operate. Digital monitoring systems, advanced heat exchangers, and large heat pumps are enhancing load balancing and thermal storage. The recovery of waste heat is becoming more common in industrial areas where excess thermal energy can be redirected to municipal heating systems.

Current market conditions depend on infrastructure upgrades, public-private investment models, and long-term utility agreements. Participants are focusing on optimizing networks, integrating renewable heat sources, and improving grid flexibility to enhance performance. The ongoing emphasis on decarbonization and energy resilience is continuing to shape project development priorities in the global district heating industry.

03

Segment Analysis

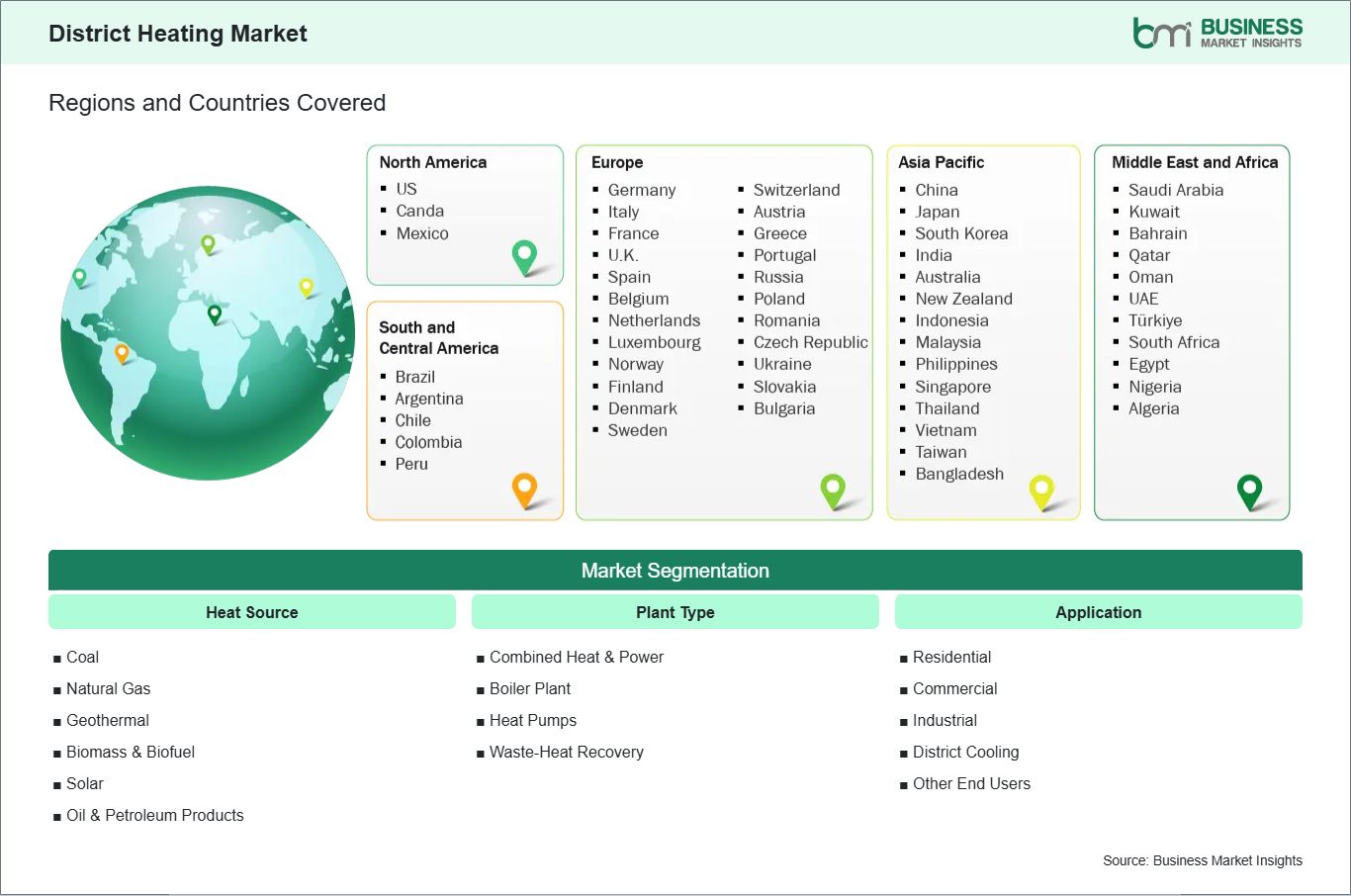

District Heating Market Segmentation

The market is segmented by heat source, plant type, and application across diversified thermal infrastructure networks.

By Heat Source

- Coal – Legacy infrastructure sustains utilization in established industrial heating networks.

- Natural Gas – Flexible combustion characteristics support large-scale urban heating operations.

- Geothermal – Stable baseload thermal output enhances long-term energy reliability.

- Biomass and Biofuel – Renewable feedstocks strengthen low-emission heating initiatives.

- Solar – Seasonal thermal storage improves renewable heat integration efficiency.

- Oil and Petroleum Products – Backup thermal generation supports peak-demand continuity.

By Plant Type

- Combined Heat and Power – Simultaneous electricity and heat generation improves fuel utilization efficiency.

- Boiler Plant – Centralized steam generation supports conventional district heating infrastructure.

- Heat Pumps – Electrified heating systems enhance low-temperature network performance.

- Waste-Heat Recovery – Captured industrial heat reduces primary fuel consumption requirements.

By Application

- Residential – Urban housing developments maintain consistent thermal distribution demand.

- Commercial – Institutional facilities prioritize centralized energy management systems.

- Industrial – Manufacturing complexes require continuous large-scale thermal supply.

- District Cooling – Integrated thermal networks support multi-season energy applications.

- Other End Users – Specialized facilities adopt customized centralized heating solutions.

04

Market Forces

District Heating Market Drivers and Opportunities

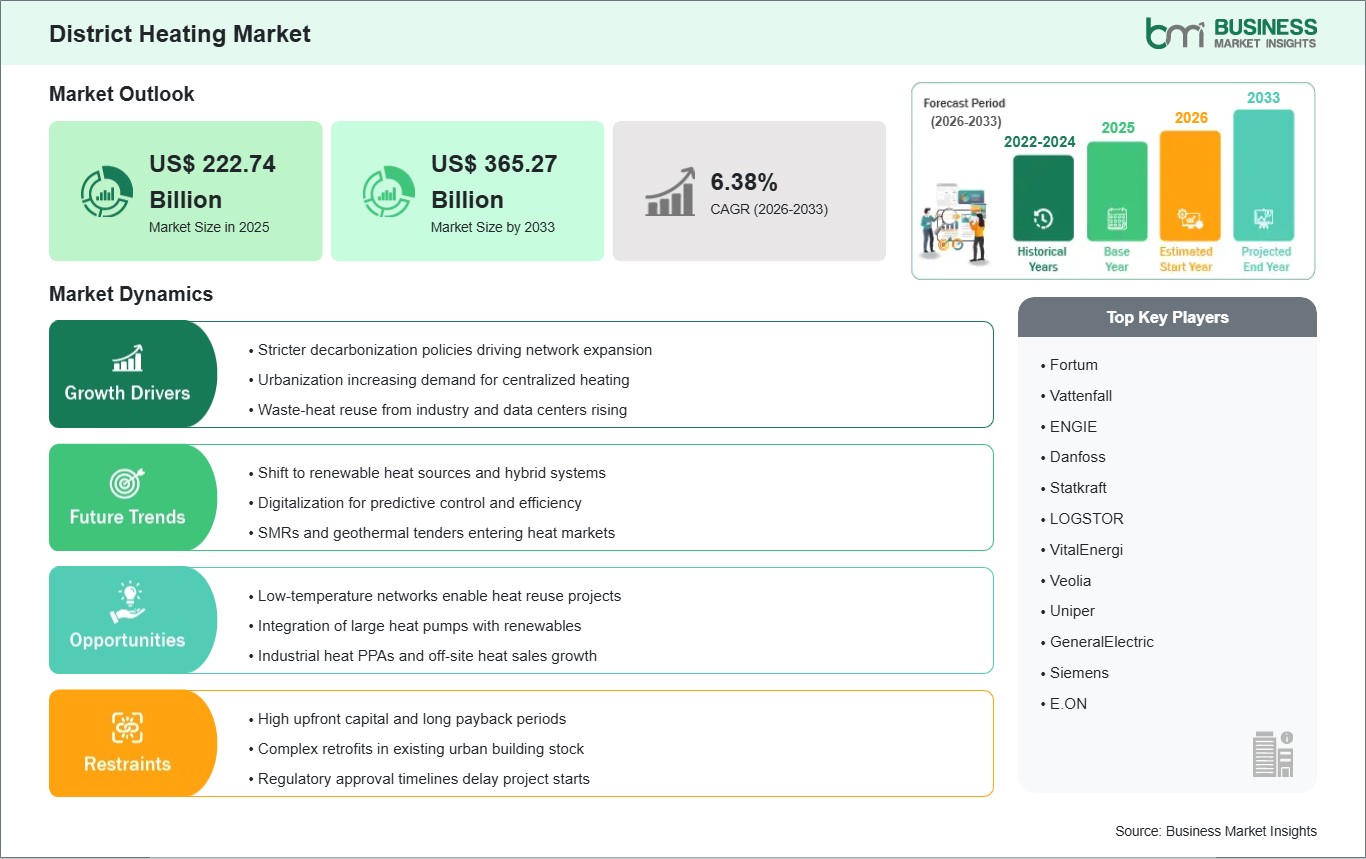

Driver: Expansion of Urban Energy Efficiency Initiatives

Municipal governments are improving energy efficiency systems to update old heating infrastructure and cut down on local emissions. Centralized heating networks tackle inefficiencies linked to scattered boilers while supporting better thermal distribution in high-density urban areas. Investments in public infrastructure and long-term goals for reducing carbon emissions are promoting wider use in residential and commercial developments.

This shift is changing how infrastructure is planned in metropolitan areas, where reliable heating and effective fuel use remain important goals. District heating systems enhance centralized energy management and make it easier to include renewable and recovered heat sources. These systems are becoming more important as city authorities look for scalable heating solutions that support sustainability and energy security.

Opportunity: Integration of Renewable and Recovered Heat Technologies

Thermal network operators are adding renewable heat sources and technologies for recovering industrial waste heat to diversify their energy supplies. Large-scale heat pumps, geothermal facilities, and biomass-based systems are making thermal generation cleaner while improving operational flexibility. These innovations help create low-temperature district heating setups that can boost overall network efficiency.

Future growth opportunities are arising through smart energy districts and combined urban utility systems. Improvements in thermal storage, digital monitoring, and the use of renewable energy in a decentralized way are likely to strengthen the network's ability to adapt over time. Wider use of recovered industrial heat and electric heating technologies may further change operational models across modern district heating systems.

05

Size and Share Analysis

District Heating Market Size and Share Analysis

The District Heating Market is projected to grow from US$ 222.74 Billion in 2025 to US$ 365.27 Billion by 2033 , registering a CAGR of 6.38% from 2026 to 2033.

The District Heating Market was valued at USD 205.5 Billion in 2025 and is projected to reach USD 301.89 Billion by 2033, registering a CAGR of 4.9% during the forecast period.

Market expansion shows ongoing improvements in infrastructure, a growing use of renewable thermal sources, and more widespread adoption of centralized heating systems in urban areas. Natural gas systems remain prominent due to existing pipelines and their flexibility. Combined heat and power plants also continue to thrive since they enhance both thermal and electrical energy production within centralized utility systems. Renewable heat sources, especially biomass and geothermal technologies, are increasingly shaping infrastructure diversity plans.

Residential applications represent a significant share of use in crowded urban settings, where centralized thermal supply ensures better heating consistency and efficiency. The commercial and industrial sectors are also adopting district heating systems to improve energy management practices and bolster long-term sustainability goals in institutional and manufacturing facilities.

07

Report Coverage

District Heating Market Report Coverage and Deliverables

The " District Heating Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

- Market size and forecast at global, regional, and country levels for all market segments covered under the scope

- Market trends, as well as drivers, restraints, and opportunities

- Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the District heating market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

District Heating Market Geographic Insights

The District Heating market displays various regional adoption patterns influenced by infrastructure maturity, energy transition priorities, climate conditions, and long-term urban development plans. Countries with established centralized heating systems are modernizing their existing networks. Meanwhile, emerging economies are looking into district-scale thermal distribution to support growing urban populations and industrial growth areas.

North America shows increasing interest in integrated thermal infrastructure at universities, commercial campuses, and municipal developments. Renewal projects and decarbonization goals are prompting utilities to consider low-emission heating options. Waste-heat use and electrified heating technologies are also gaining attention as municipalities aim for more resilient and adaptable urban energy systems.

Asia Pacific is witnessing strong infrastructure expansion tied to rapid urbanization and industrial growth. Major metropolitan areas are including centralized heating and cooling systems in their smart city initiatives. Governments in the region are promoting cleaner thermal generation technologies to lessen reliance on inefficient local heating systems while enhancing long-term energy efficiency.

Europe has a well-established district heating ecosystem backed by extensive pipeline infrastructure and efforts to integrate renewable energy. Biomass, geothermal, and waste-energy systems play a key role in regional modernization initiatives. Emerging markets in the Middle East, Africa, and South and Central America are gradually looking into district thermal solutions for urban developments, institutional facilities, and industrial clusters that need centralized energy distribution.

10

Industry Activity

Recent Developments

The district heating market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the district heating market are:

- March 2026: Fortum announced expansion initiatives focused on low-carbon district heating and large-scale heat pump integration in Nordic energy networks.

- October 2024: ENGIE advanced multiple urban district energy projects emphasizing renewable thermal sources and waste-heat recovery technologies.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

International Energy Agency International District Energy Association Euroheat and Power United Nations Environment Programme World Bank U.S. Department of Energy European Environment Agency International Renewable Energy Agency