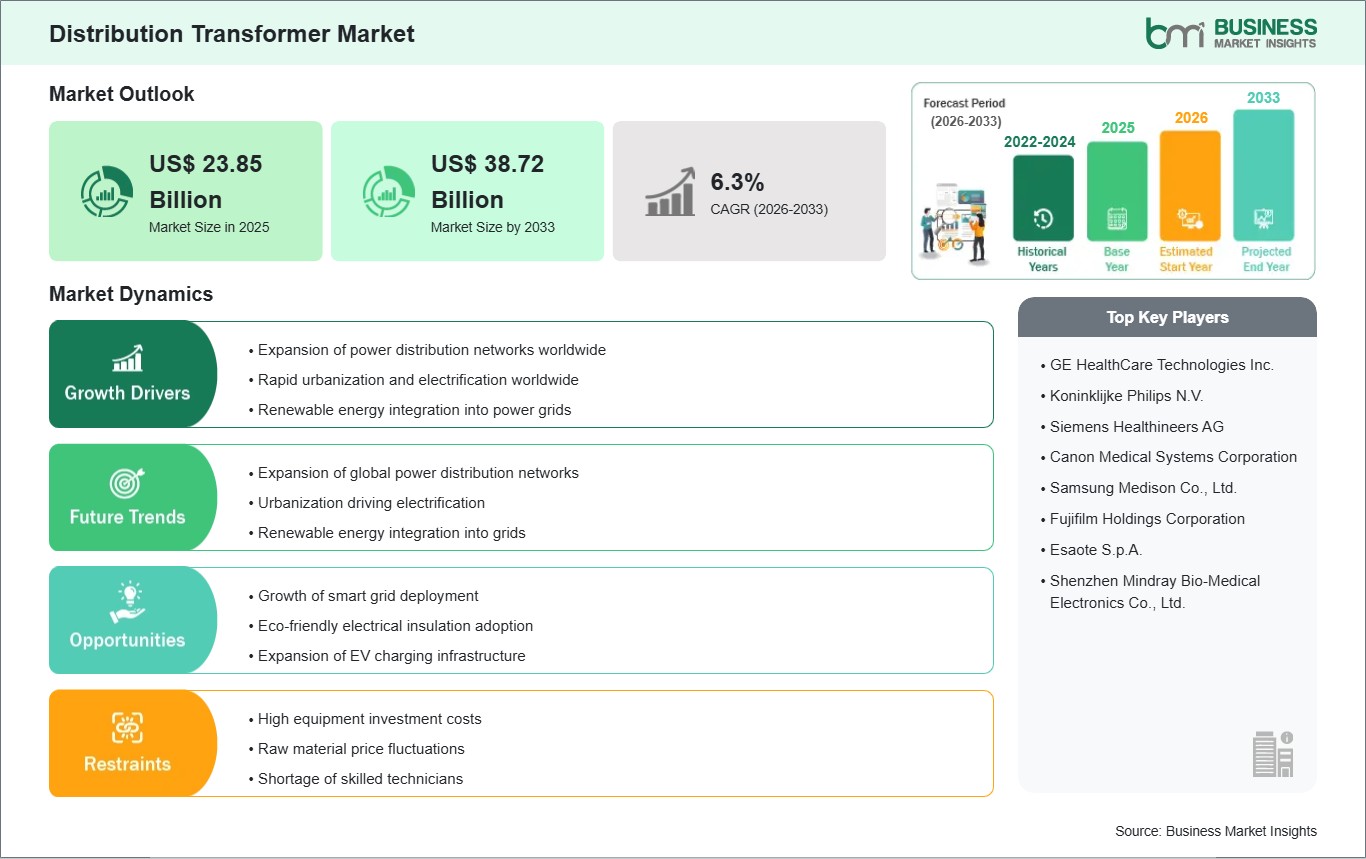

The Distribution Transformer Market size is expected to reach US$ 38.72 Billion by 2033 from US$ 23.85 Billion in 2025. The market is estimated to record a CAGR of 6.24% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global distribution transformer market is a fundamental and enduring component of the electrical power infrastructure, responsible for the final voltage transformation in the power delivery chain—stepping down the voltage from medium-voltage distribution lines (typically 11-33 kV) to the low-voltage levels (400/230 V) used by end consumers. This market is characterized by steady, essential demand driven by the universal need for reliable electricity. Core growth drivers include global urbanization and industrialization, which necessitate the expansion and densification of electrical grids; government-led rural electrification programs in emerging economies; and the ongoing replacement cycle of aging transformer fleets in developed regions. Furthermore, the integration of distributed energy resources (DERs) like rooftop solar and the proliferation of electric vehicle (EV) charging infrastructure are creating new demands and specifications for distribution transformers, requiring enhanced capabilities for bidirectional power flow and voltage regulation.

However, the market contends with significant challenges, including volatile prices of key raw materials like copper, aluminum, and electrical steel; intense competitive pressure leading to margin erosion; and stringent environmental regulations governing the use of insulating oils and mandating higher efficiency standards. Despite these headwinds, substantial opportunities are emerging from the development of smart and amorphous core transformers that offer significantly lower no-load losses, the growing demand for dry-type transformers in indoor and environmentally sensitive applications, and the modernization of grids to support the energy transition toward decarbonization and resilience.

Distribution Transformer Market - Strategic Insights:

Get more information on this report

Distribution Transformer Market Segmentation Analysis:

Key segments that contributed to the derivation of the distribution transformer market analysis are component, waveform, frequency band, and end-user.

By type, the market is segmented into oil-immersed and dry-type transformers. The oil-immersed segment dominated the market in 2025, holding the largest share due to its cost-effectiveness, proven reliability, and superior cooling performance for outdoor utility applications.

By phase, the market is categorized into single-phase and three-phase. Three-phase transformers accounted for the dominant revenue share in 2025, as they form the backbone of commercial, industrial, and utility distribution networks where balanced three-phase power is required.

By power rating, the market is segmented into up to 500 kVA, 501 kVA to 2,500 kVA, and above 2,500 kVA. The up to 500 kVA segment held the largest share in 2025, representing the high-volume segment for pole-mounted and pad-mounted units serving residential neighborhoods, small commercial establishments, and as distribution points in industrial facilities.

By end-user, the market is segmented into utility, industrial, commercial, and residential. The utility sector was the largest end-user in 2025, responsible for the vast majority of procurement to build, maintain, and expand the public electricity distribution network.

Distribution Transformer Market Drivers and Opportunities:

Grid Expansion, Modernization, and Rural Electrification

The most significant drivers for the distribution transformer market are the parallel needs for grid expansion in developing regions and grid modernization in developed ones. Rapid urbanization and industrialization in Asia-Pacific, Africa, and parts of Latin America are driving massive investments in new distribution infrastructure, including thousands of transformers. Concurrently, rural electrification initiatives by governments and international organizations are creating sustained demand for smaller-rated transformers. In mature markets, the aging installed base of transformers—many exceeding their design life—necessitates a steady replacement cycle. Furthermore, modernizing grids to be smarter and more resilient against climate change and cyber threats often involves upgrading to more efficient, condition-monitored transformers, creating a value-added upgrade market.

The Energy Transition and Efficiency Regulations

The global energy transition presents both a challenge and a major opportunity. The integration of distributed energy resources (DERs) and electric vehicle (EV) charging stations can cause voltage fluctuations and reverse power flows, straining conventional transformers. This drives demand for transformers with advanced voltage regulation capabilities (e.g., smart transformers with on-load tap changers). Simultaneously, stringent energy efficiency regulations (such as the EU's Ecodesign Directive or DOE standards in the US) are phasing out lower-efficiency units. This regulatory push is a powerful driver for the adoption of transformers with amorphous metal cores or other advanced designs that minimize core losses, opening a premium market segment for manufacturers with advanced material and design expertise.

Distribution Transformer Market Size and Share Analysis:

By type, oil-immersed transformers maintain cost and performance advantages for most outdoor utility applications, ensuring their continued dominance. However, the dry-type segment's growth is outpacing the market average, driven by safety codes in cities, growth in high-value commercial construction, and the expansion of data centers.

By phase, three-phase transformers command a higher average selling price and are essential for all non-residential power distribution, securing their revenue leadership. Single-phase transformers lead in unit volume, especially in regions with dispersed residential settlements

By power rating, the under-500 kVA segment is the volume workhorse of the grid. The 501-2500 kVA segment is critical for commercial complexes, medium industries, and as substation feeders. Transformers above 2500 kVA are used for heavy industry and primary distribution substations, representing a high-value, lower-volume niche.

By end-user, utilities are the anchor customers, with procurement often tied to long-term grid plans. The industrial sector's demand is closely linked to capital expenditure cycles in manufacturing and mining. The commercial segment is growing steadily with new construction and building retrofits.

Distribution Transformer Market Report Highlights:

Distribution Transformer Market Report Coverage and Deliverables:

The "Distribution Transformer Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Distribution Transformer Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Distribution Transformer Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Distribution Transformer Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the distribution transformer market

Detailed company profiles, including SWOT analysis

Distribution Transformer Market Geographic Insights:

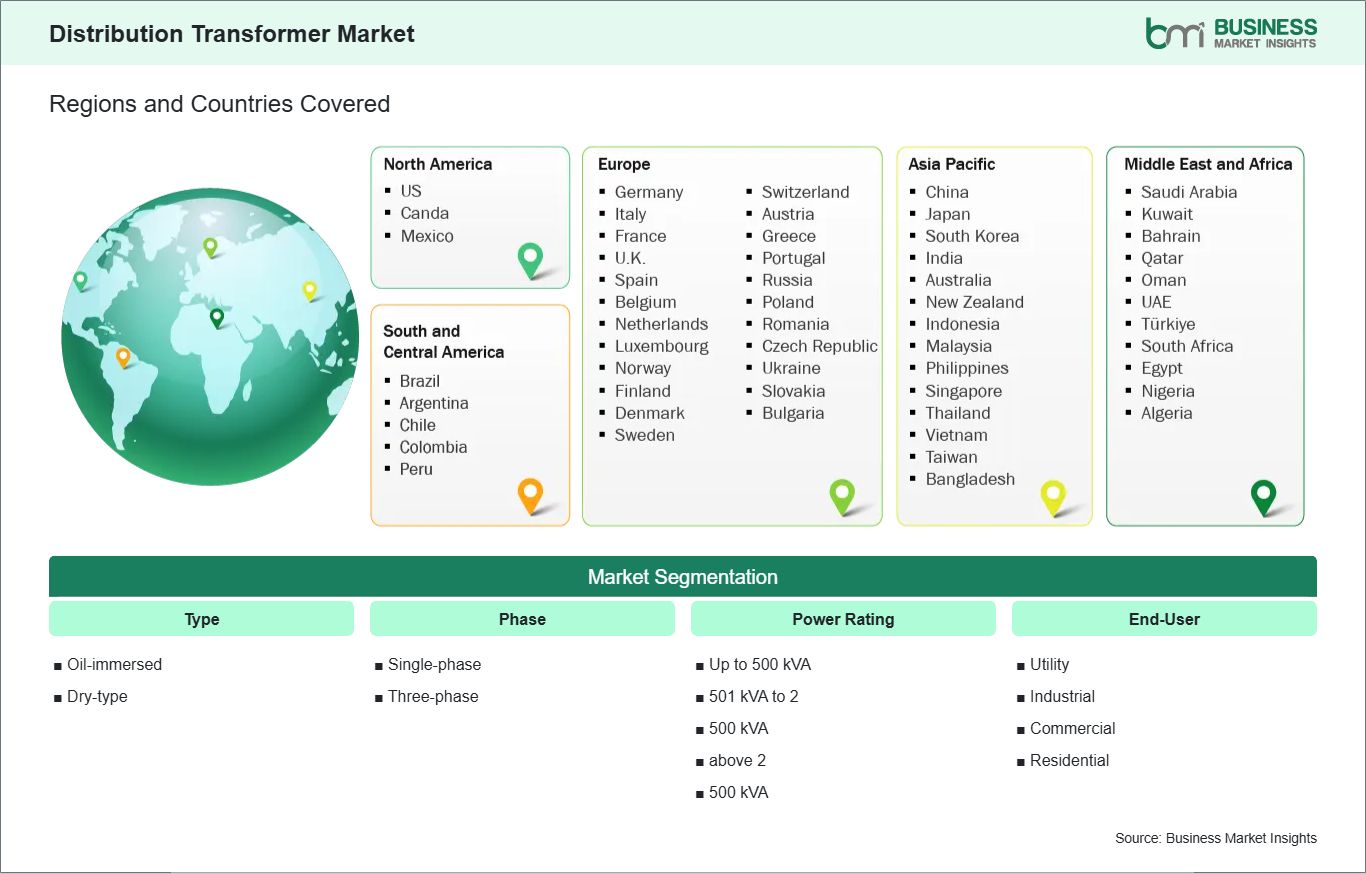

The geographical scope of the distribution transformer market report is divided into five regions: North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America. The Asia Pacific region is both the largest and the fastest-growing market, while North America and Europe are mature markets focused on replacement and efficiency upgrades.

Asia Pacific, led by China, India, Japan, and Southeast Asia, is the undisputed engine of global market growth. This is driven by unprecedented investments in power infrastructure to support economic growth, massive urban development projects, and ambitious government targets for universal electrification and renewable energy integration, all of which require vast quantities of distribution transformers.

North America and Europe are characterized by stable, replacement-driven demand. Growth is fueled by the need to replace aging infrastructure, adopt higher-efficiency units to comply with regulations and sustainability goals, and reinforce grids to accommodate EV charging and renewable generation. The markets are also seeing increased investment in grid resiliency against extreme weather events.

Get more information on this report

Distribution Transformer Market Research Report Guidance:

The report includes qualitative and quantitative data in the distribution transformer market across type, phase, power rating, end-user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the distribution transformer market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the distribution transformer market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the distribution transformer market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover distribution transformer market segments by type, phase, power rating, end-user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the distribution transformer market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Distribution Transformer Market News and Key Development:

The distribution transformer market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the distribution transformer market are:

In September 2025, Siemens Energy is investing approximately €220 million to expand its transformer factory in Nuremberg, Germany, creating 350 new jobs. The foundation stone for the site expansion was laid today in the presence of Bavaria’s Minister President Dr. Markus Söder and Nuremberg’s Mayor Marcus König. With this investment, Siemens Energy is responding to the sharp increase in global demand for large transformers which are crucial for grid expansion.

In April 2024, Hitachi Industrial Equipment Systems Co., Ltd. and Mitsubishi Electric Corporation announced that they have agreed to transfer the distribution transformer business of Mitsubishi Electric's Nagoya Works, which develops and manufactures factory automation (FA) equipment, to Hitachi Industrial Equipment Systems and integrate their businesses.

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Distribution Transformer Market

ABB

Siemens

Schneider Electric

General Electric

Eaton

Hitachi Energy

Mitsubishi Electric

Toshiba Energy Systems

CG Power

BHEL

Frequently Asked Questions

How big is the Distribution Transformer Market?

The Distribution Transformer Market is valued at US$ 23.85 Billion in 2025, it is projected to reach US$ 38.72 Billion by 2033.

What is the CAGR for Distribution Transformer Market by (2026 - 2033)?

As per our report Distribution Transformer Market, the market size is valued at US$ 23.85 Billion in 2025, projecting it to reach US$ 38.72 Billion by 2033. This translates to a CAGR of approximately 6.24% during the forecast period.

What segments are covered in this report?

The Distribution Transformer Market report typically cover these key segments-

Type (Oil-immersed, Dry-type)

Phase (Single-phase, Three-phase)

Power Rating (Up to 500 kVA, 501 kVA to 2,500 kVA, above 2,500 kVA)

What is the historic period, base year, and forecast period taken for Distribution Transformer Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Distribution Transformer Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Distribution Transformer Market?

The Distribution Transformer Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Distribution Transformer Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Distribution Transformer Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Distribution Transformer Market

Get Free Sample For Distribution Transformer Market