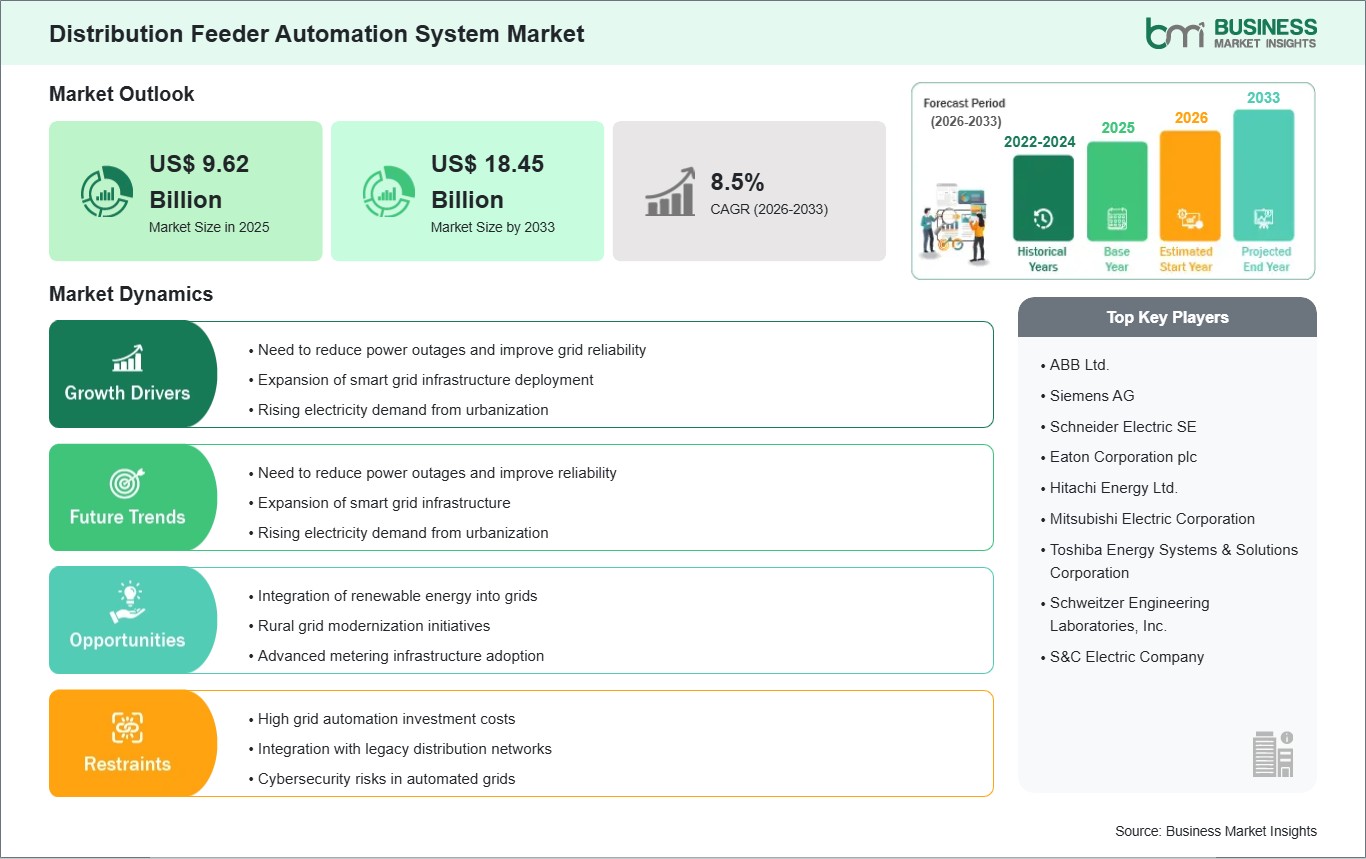

The Distribution Feeder Automation System Market size is expected to reach US$ 18.45 Billion by 2033 from US$ 9.62 Billion in 2025. The market is estimated to record a CAGR of 8.48% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global distribution feeder automation system market is a critical component of the smart grid evolution, focused on enhancing the reliability, efficiency, and resilience of medium-voltage (MV) power distribution networks. These systems integrate intelligent electronic devices (IEDs), sensors, communication networks, and control software to monitor, protect, and automatically control distribution feeders—the backbone lines that deliver electricity from substations to end-users. The market is driven by the urgent need to modernize aging grid infrastructure, reduce System Average Interruption Duration Index (SAIDI) and Frequency Index (SAIFI) metrics, and integrate distributed energy resources (DERs) like solar PV and electric vehicle (EV) charging stations. Utilities worldwide are investing in feeder automation to achieve self-healing grid capabilities, where faults can be automatically detected, isolated, and power restored to unaffected sections within minutes, drastically improving service reliability.

However, the market faces challenges including high capital investment for full-scale deployment, interoperability issues between legacy equipment and new automation technologies, and cybersecurity vulnerabilities in increasingly connected grid networks. Despite these hurdles, significant opportunities are emerging from government mandates and incentives for grid modernization, the growing adoption of IoT and cloud-based analytics for predictive maintenance, and the need to manage bidirectional power flows and voltage stability caused by high penetration of renewable energy sources.

Distribution Feeder Automation System Market - Strategic Insights:

Get more information on this report

Distribution Feeder Automation System Market Segmentation Analysis:

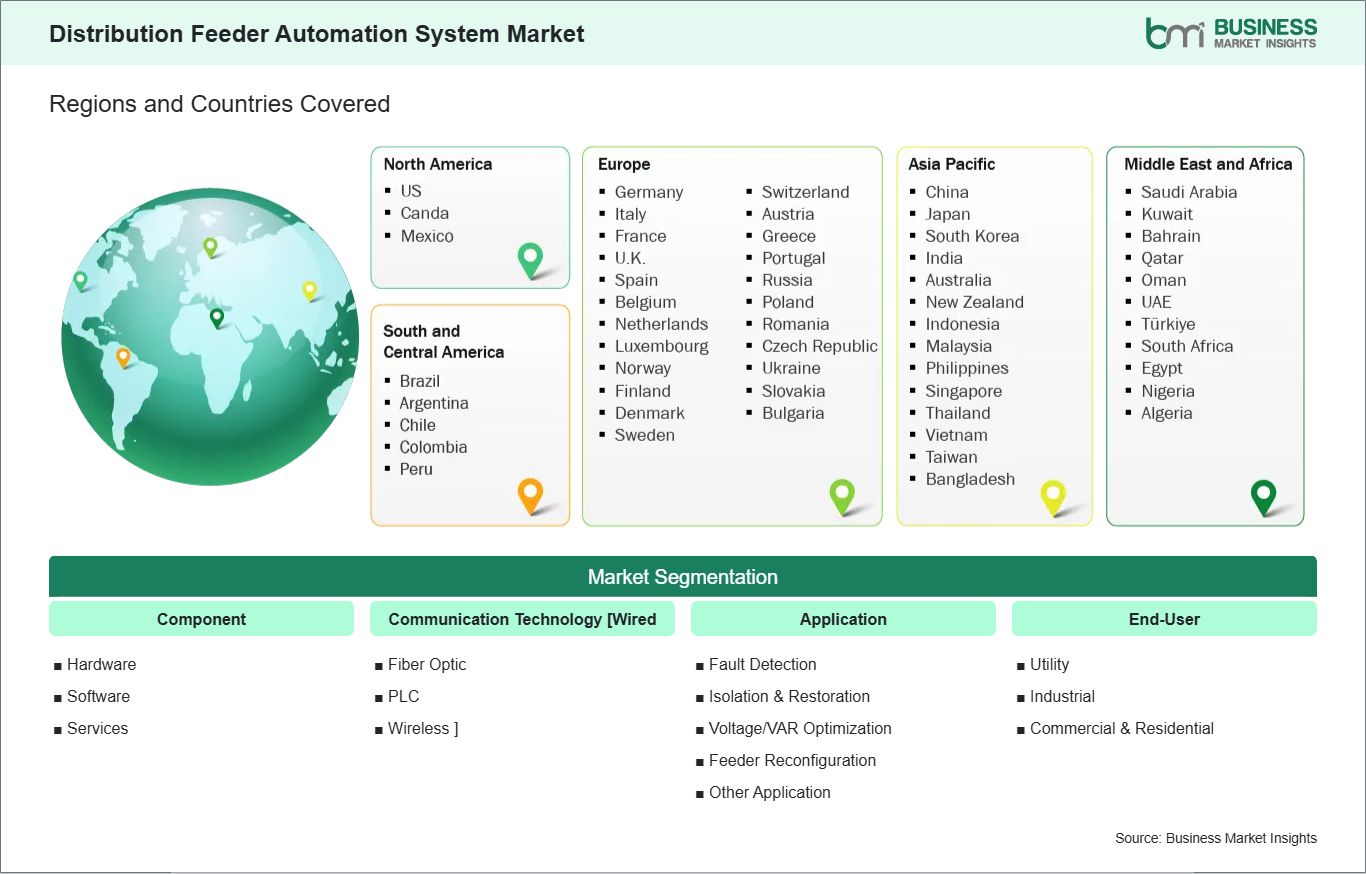

Key segments that contributed to the derivation of the distribution feeder automation system market analysis are component, communication technology, application, and end-user.

By component, the market is segmented into hardware, software and firmware, and services. The hardware segment, comprising reclosers, sectionalizers, fault indicators, capacitor banks, and remote terminal units (RTUs), dominated the market in 2025, as these physical devices form the essential infrastructure for automation.

By communication technology, the market is categorized into wired (fiber optic, power line carrier) and wireless (RF mesh, cellular, others). Wireless communication technologies, particularly RF mesh and cellular (4G/5G), held the largest and fastest-growing share in 2025. They offer lower deployment costs and greater flexibility for retrofitting existing infrastructure compared to trenching for fiber optics, making them ideal for expansive distribution networks.

By application, the market is segmented into Fault Detection, Isolation & Restoration (FDIR), Voltage/VAR Optimization, Feeder Reconfiguration, and others. FDIR accounted for the dominant share in 2025, as it delivers the most immediate and measurable benefit to utilities by minimizing outage times and improving reliability metrics, which are key performance indicators for regulators and customers.

By end-user, the market is segmented into utility, industrial, and commercial & residential. The utility segment held the overwhelming revenue share in 2025, as electric distribution companies are the primary owners and operators of feeder networks.

Distribution Feeder Automation System Market Drivers and Opportunities:

Grid Modernization Mandates and Rising Demand for Reliability

The primary driver for feeder automation is the global push for grid modernization, often backed by regulatory mandates and government funding. Aging infrastructure is prone to failures, leading to costly outages. Regulators are increasingly holding utilities accountable through performance-based rates that reward improved reliability (SAIDI/SAIFI). Feeder automation directly addresses this by enabling a self-healing grid, making it a strategic investment for utilities to meet regulatory expectations, reduce operational costs from truck rolls for manual restoration, and enhance customer satisfaction. The integration of distributed energy resources (DERs) further complicates grid management, creating voltage fluctuations and reverse power flows that automation systems are uniquely positioned to monitor and mitigate.

Integration of Advanced Analytics and DER Management

A major growth opportunity lies in the convergence of feeder automation with Advanced Distribution Management Systems (ADMS) and Distributed Energy Resource Management Systems (DERMS). Modern automation systems are evolving from simple fault management to becoming data-rich platforms. By integrating advanced analytics, machine learning, and weather data, utilities can transition from reactive fault response to predictive maintenance—identifying potential failures (e.g., deteriorating insulation) before they cause outages. Furthermore, as EV penetration and rooftop solar increase, feeder automation systems equipped with DERMS capabilities can actively manage these resources to provide grid services (voltage support, peak shaving), unlocking new value streams and ensuring grid stability.

Distribution Feeder Automation System Market Size and Share Analysis:

By component, hardware remains the largest segment due to the capital-intensive nature of grid equipment. However, the software segment is experiencing higher growth as the intelligence layer becomes more sophisticated, and utilities increasingly adopt cloud-based ADMS platforms. Services related to system integration, consulting, and maintenance are also expanding as deployments become more complex.

By communication technology, wireless solutions are rapidly gaining share due to their scalability and cost-effectiveness. Cellular technology (leveraging public 4G/5G networks) is particularly promising for wide-area coverage, while RF mesh is well-established for dense urban deployments. Fiber optics retains a strong position for high-bandwidth, high-reliability backbone communication in critical utility corridors.

By application, FDIR is the established core application driving initial investments. Voltage/VAR optimization is a high-growth segment as utilities focus on energy efficiency, loss reduction, and integrating renewables. Feeder reconfiguration for load balancing is becoming more important with the uneven load growth from EV clusters.

By end-user, the utility sector is the clear leader. The industrial segment represents a niche but high-value market for microgrids and campus-level automation to ensure process continuity. Commercial and residential influence is indirect, driven by their demand for reliable power and adoption of DERs.

Distribution Feeder Automation System Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

ABB Ltd.

Siemens AG

Schneider Electric SE

Eaton Corporation plc

Hitachi Energy Ltd.

Mitsubishi Electric Corporation

Toshiba Energy Systems & Solutions Corporation

Schweitzer Engineering Laboratories, Inc.

S&C Electric Company

Get more information on this report

Distribution Feeder Automation System Market Report Coverage and Deliverables:

The "Distribution Feeder Automation System Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Distribution Feeder Automation System Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Distribution Feeder Automation System Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Distribution Feeder Automation System Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the distribution feeder automation system market

Detailed company profiles, including SWOT analysis

Distribution Feeder Automation System Market Geographic Insights:

The geographical scope of the distribution feeder automation system market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. Asia Pacific is expected to witness the highest growth during the forecast period, while North America currently holds a significant share due to early adoption and regulatory pushes.

Asia Pacific, led by China, India, Japan, and Southeast Asian nations, is the fastest-growing market. This growth is fueled by massive investments in expanding and modernizing electricity infrastructure to support economic development, ambitious government smart grid initiatives, and the need to improve reliability in rapidly urbanizing areas with increasing power demand.

North America, particularly the United States and Canada, is a mature yet steadily growing market. Strong regulatory frameworks incentivizing grid resilience (e.g., following major weather events), significant utility investment cycles, and high penetration of DERs are key drivers. The U.S. Department of Energy's grid modernization programs provide further impetus.

Europe is a technologically advanced market with a strong focus on renewable integration and energy efficiency. EU directives and funding for smart grid projects, coupled with the need to manage a high share of intermittent renewables, are driving sophisticated feeder automation deployments in countries like Germany, the UK, France, and the Nordic nations.

Get more information on this report

Distribution Feeder Automation System Market Research Report Guidance:

The report includes qualitative and quantitative data in the distribution feeder automation system market across component, communication technology, application, end-user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the distribution feeder automation system market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the distribution feeder automation system market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the distribution feeder automation system market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover distribution feeder automation system market segments by component, communication technology, application, end-user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the distribution feeder automation system market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Distribution Feeder Automation System Market News and Key Development:

The distribution feeder automation system market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the distribution feeder automation system market are:

In January 2026, Hubbell Incorporated is set to introduce its newest advancements in grid automation and intelligent infrastructure at DTECH 2026, booth 3711. The company will highlight its long-established partnerships with utilities and its deep experience developing solutions shaped by real-world operational needs.

In August 2025, Schneider Electric, the leader in the digital transformation of energy management and automation, announces the launch of FeederSeT - a new product range bringing advanced digital connectivity to circuit protection solutions. The FeederSeT range has been designed to support both sustainability and smart system intelligence. It features comprehensive asset health monitoring capabilities, while being adaptable and scalable in line with needs, making it a future-proof choice for any application.

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Distribution Feeder Automation System Market

ABB

Siemens

Schneider Electric

Eaton

GE Grid Solutions

Hitachi Energy

Mitsubishi Electric

Toshiba Energy Systems

Schweitzer Engineering Laboratories

SandC Electric

Frequently Asked Questions

How big is the Distribution Feeder Automation System Market?

The Distribution Feeder Automation System Market is valued at US$ 9.62 Billion in 2025, it is projected to reach US$ 18.45 Billion by 2033.

What is the CAGR for Distribution Feeder Automation System Market by (2026 - 2033)?

As per our report Distribution Feeder Automation System Market, the market size is valued at US$ 9.62 Billion in 2025, projecting it to reach US$ 18.45 Billion by 2033. This translates to a CAGR of approximately 8.48% during the forecast period.

What segments are covered in this report?

The Distribution Feeder Automation System Market report typically cover these key segments-

Component (Hardware, Software, Services)

Communication Technology [Wired (Fiber Optic, PLC), Wireless (RF Mesh, Cellular)]

What is the historic period, base year, and forecast period taken for Distribution Feeder Automation System Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Distribution Feeder Automation System Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Distribution Feeder Automation System Market?

The Distribution Feeder Automation System Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

ABB Ltd.

Siemens AG

Schneider Electric SE

Eaton Corporation plc

Hitachi Energy Ltd.

Mitsubishi Electric Corporation

Toshiba Energy Systems & Solutions Corporation

Schweitzer Engineering Laboratories, Inc.

S&C Electric Company

Who should buy this report?

The Distribution Feeder Automation System Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Distribution Feeder Automation System Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Distribution Feeder Automation System Market

Get Free Sample For Distribution Feeder Automation System Market