01

Market Summery

Executive Summary and Global Market Analysis

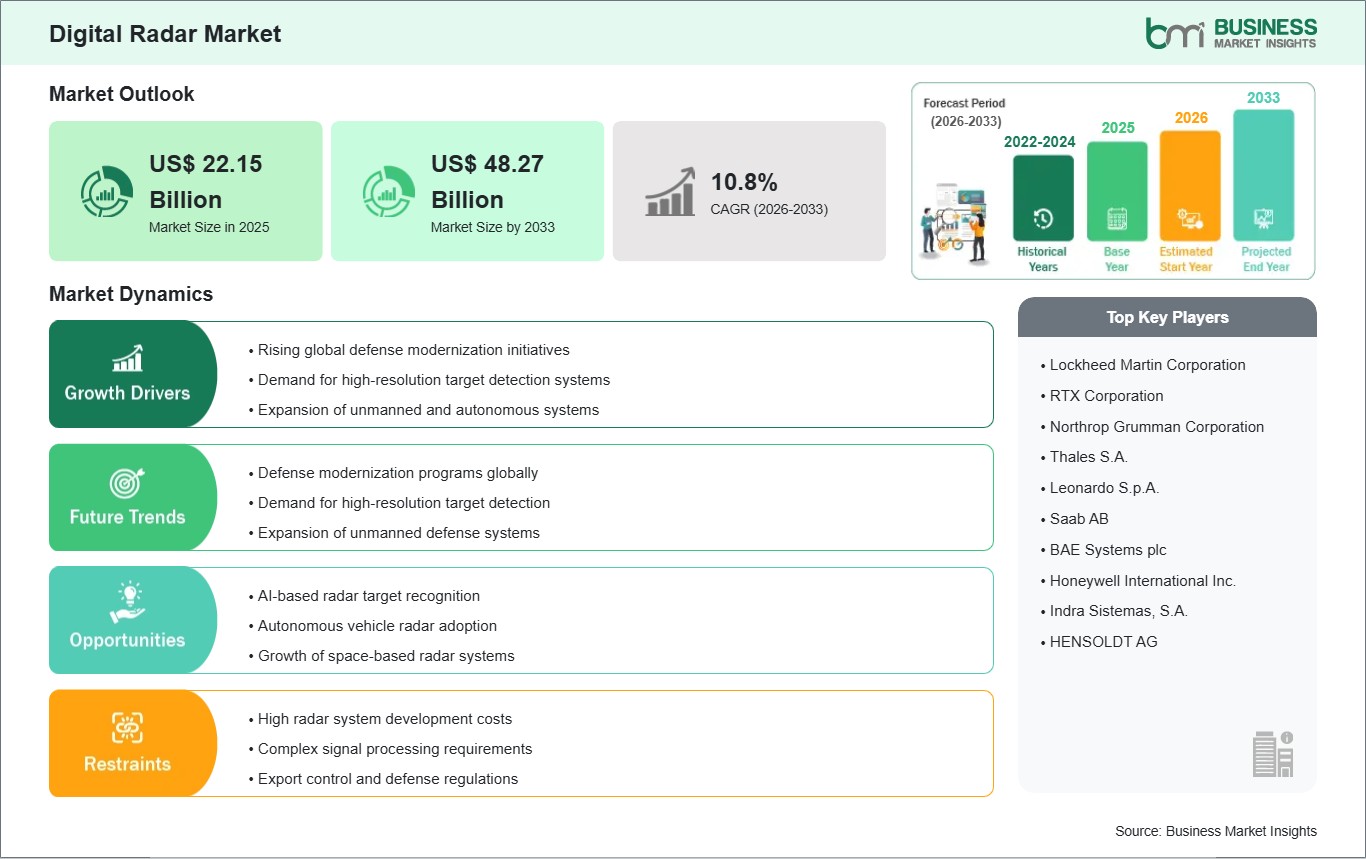

The global digital radar market is at the forefront of a technological revolution in sensing and detection, transitioning from traditional analog systems to fully digital architectures. Digital radar systems leverage direct digital synthesis (DDS), software-defined radio (SDR) principles, and advanced digital signal processing (DSP) to offer unparalleled flexibility, precision, and performance. By digitizing the signal at the earliest possible stage in the receiver chain, these systems enable software-reconfigurable operation, real-time adaptive waveform generation, and superior target discrimination in cluttered environments. The market is experiencing robust growth driven by the modernization of defense and aerospace platforms with active electronically scanned array (AESA) radars, the rapid deployment of advanced driver-assistance systems (ADAS) and autonomous vehicles requiring high-resolution automotive radars, and the expansion of air traffic management and weather monitoring infrastructure.

However, the market faces significant challenges, including the high research, development, and production costs associated with advanced digital components, the complexity of system integration and software development, and the need for specialized technical expertise. Despite these hurdles, substantial opportunities are emerging from the development of cognitive and AI-enabled radars capable of autonomous decision-making, the miniaturization of digital radar components for UAVs and consumer applications, and the increasing demand for multi-mission, multifunctional radar systems in both military and commercial sectors.

03

Segment Analysis

Digital Radar Market Segmentation

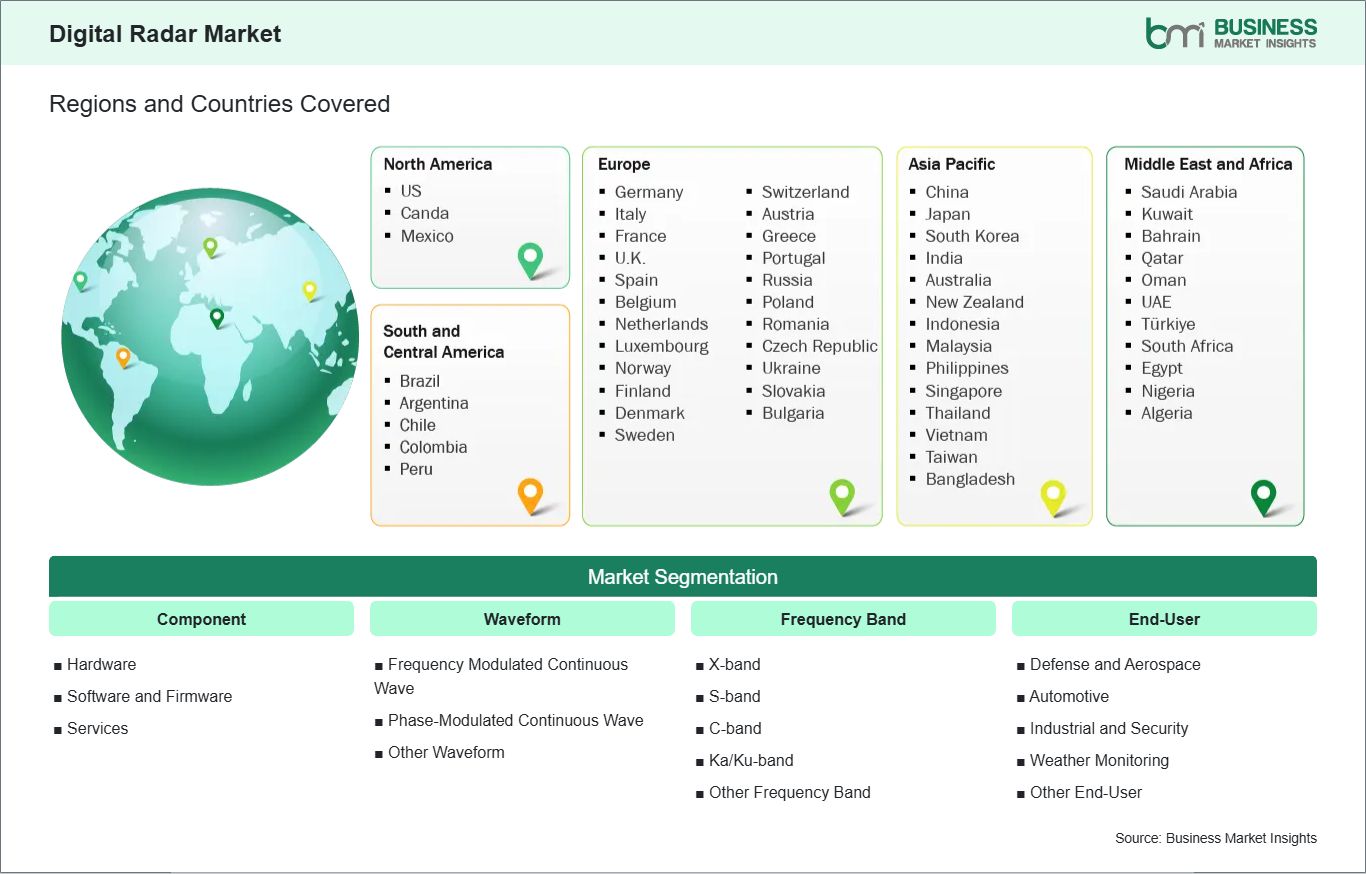

Key segments that contributed to the derivation of the digital radar market analysis are component, waveform, frequency band, and end-user.

- By component, the market is segmented into hardware, software and firmware, and services. The hardware segment, comprising digital transceivers, antennas, processors, and analog-to-digital converters, dominated the market in 2025, representing the foundational technological investment.

- By waveform, the market is categorized into Frequency Modulated Continuous Wave (FMCW), Phase-Modulated Continuous Wave (PMCW), and others. FMCW technology held the largest share in 2025, particularly dominating the automotive radar sector due to its excellent range resolution, low power consumption, and relative simplicity.

- By frequency band, the market is segmented into X-band, S-band, C-band, Ka/Ku-band, and others. The X-band segment accounted for the largest share in 2025, owing to its widespread use in maritime navigation, defense fire control, and weather monitoring, offering a balance between resolution and atmospheric penetration.

- By end-user, the market is segmented into defense and aerospace, automotive, industrial and security, weather monitoring, and others. The defense and aerospace segment held the dominant revenue share in 2025, driven by high-value platform modernization programs globally.

04

Market Forces

Digital Radar Market Drivers and Opportunities

Defense Modernization and the Autonomous Vehicle Revolution

Two parallel megatrends are powering the digital radar market. In the defense sector, nations worldwide are investing in next-generation platforms (fighter jets, naval vessels, ground vehicles) equipped with digital AESA radars. These systems provide multifunction capabilities (simultaneous air-to-air and air-to-ground modes), low probability of intercept (LPI), and enhanced electronic warfare resilience. Simultaneously, the automotive industry's march toward higher levels of autonomy (SAE Levels 3-5) is creating an unprecedented volume demand for high-resolution, cost-effective digital radar sensors. These sensors are critical for functions like adaptive cruise control, automatic emergency braking, and blind-spot detection, requiring digital architectures to handle complex urban environments and object classification.

Software-Defined Flexibility and AI Integration

The transition to software-defined digital radar architectures presents a monumental opportunity. It allows a single hardware platform to be reconfigured via software for multiple missions—from air surveillance to weather sensing—reducing lifecycle costs and increasing operational flexibility. This software-centric approach dovetails with the integration of Artificial Intelligence (AI) and Machine Learning (ML) directly into the radar processing chain. AI can be used for advanced clutter rejection, automatic target recognition (ATR), and predictive maintenance of the radar system itself. This convergence opens new markets for cognitive radar systems that can learn and adapt to their environment in real-time, creating high-value niches in electronic intelligence (ELINT), counter-UAS, and smart infrastructure monitoring.

05

Size and Share Analysis

Digital Radar Market Size and Share Analysis

By component, hardware maintains the largest share, but the value is progressively shifting towards sophisticated software algorithms and AI models that define system capabilities. Services related to system integration, lifecycle support, and software updates are becoming increasingly significant revenue streams, especially in defense contracts.

By waveform, FMCW's dominance in automotive ensures its volume leadership. However, PMCW and other advanced waveforms are capturing share in high-performance defense and next-generation communication-sensing integrated systems, offering higher growth margins.

By frequency band, X-band's versatility secures its leading position. The higher-frequency Ka/Ku-bands are witnessing accelerated growth for applications requiring very high resolution and compact antenna sizes, such as missile seekers, satellite-based radar, and high-resolution mapping.

By end-user, defense and aerospace remain the high-value core, characterized by long development cycles and stringent requirements. The automotive sector is the volume growth engine, with millions of radar units shipped annually. Industrial and security applications (perimeter surveillance, drone detection) represent steady, expanding markets.

07

Report Coverage

Digital Radar Market Report Coverage and Deliverables

The "Digital Radar Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

- Digital Radar Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Digital Radar Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Digital Radar Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the digital radar market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Digital Radar Market Geographic Insights

The geographical scope of the digital radar market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America holds the largest market share, driven by defense spending and automotive R&D, while Asia Pacific is projected to register the highest CAGR during the forecast period.

North America, led by the United States, is the technological and market leader. Massive defense budgets fund advanced radar programs for the U.S. Department of Defense, and the region is home to leading automotive OEMs and Tier-1 suppliers driving ADAS innovation. This combination of defense and commercial excellence sustains its dominant position.

Asia Pacific is the fastest-growing region, fueled by rising defense expenditures in China, India, Japan, and South Korea, coupled with the world's largest automotive production base. Regional governments are heavily investing in indigenous radar technology development and modernizing air defense networks, creating a vibrant demand landscape.

Europe maintains a strong, innovation-driven market, with leading defense contractors (e.g., Thales, Leonardo) and automotive manufacturers (e.g., BMW, Mercedes-Benz) at the forefront of digital radar development for both military and civilian applications, supported by collaborative EU defense initiatives.

10

Industry Activity

Recent Developments

The digital radar market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the digital radar market are:

- In November 2025, Echodyne, the radar platform company, is pleased to announce that its radars have been selected by Digital Force Technologies (DFT) as the primary radars across its Seraphim C-UAS family of systems. DFT combines extensive defense expertise and cutting-edge technology to deliver unparalleled solutions that meet the evolving needs of the warfighter from concept to battlefield application. The Seraphim C-UAS is a modular, expandable family of autonomous solutions for detection, assessment, tracking, deterrence and defeat of UAS threats.

- In February 2025, Raytheon, an RTX business (NYSE: RTX), has successfully completed flight testing on the first-ever AI/ML-powered Radar Warning Receiver (RWR) system for a fourth-generation aircraft.

- In January 2025, Texas Instruments (TI) (Nasdaq: TXN) today introduced new integrated automotive chips to enable safer, more immersive driving experiences at any vehicle price point. TI's AWRL6844 60GHz mmWave radar sensor supports occupancy monitoring for seat belt reminder systems, child presence detection and intrusion detection with a single chip running edge AI algorithms, enabling a safer driving environment. With TI's next-generation audio DSP core, the AM275x-Q1 MCUs and AM62D-Q1 processors make premium audio features more affordable. Paired with TI's latest analog products, including the TAS6754-Q1 Class-D audio amplifier, engineers can take advantage of a complete audio amplifier system offering.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations