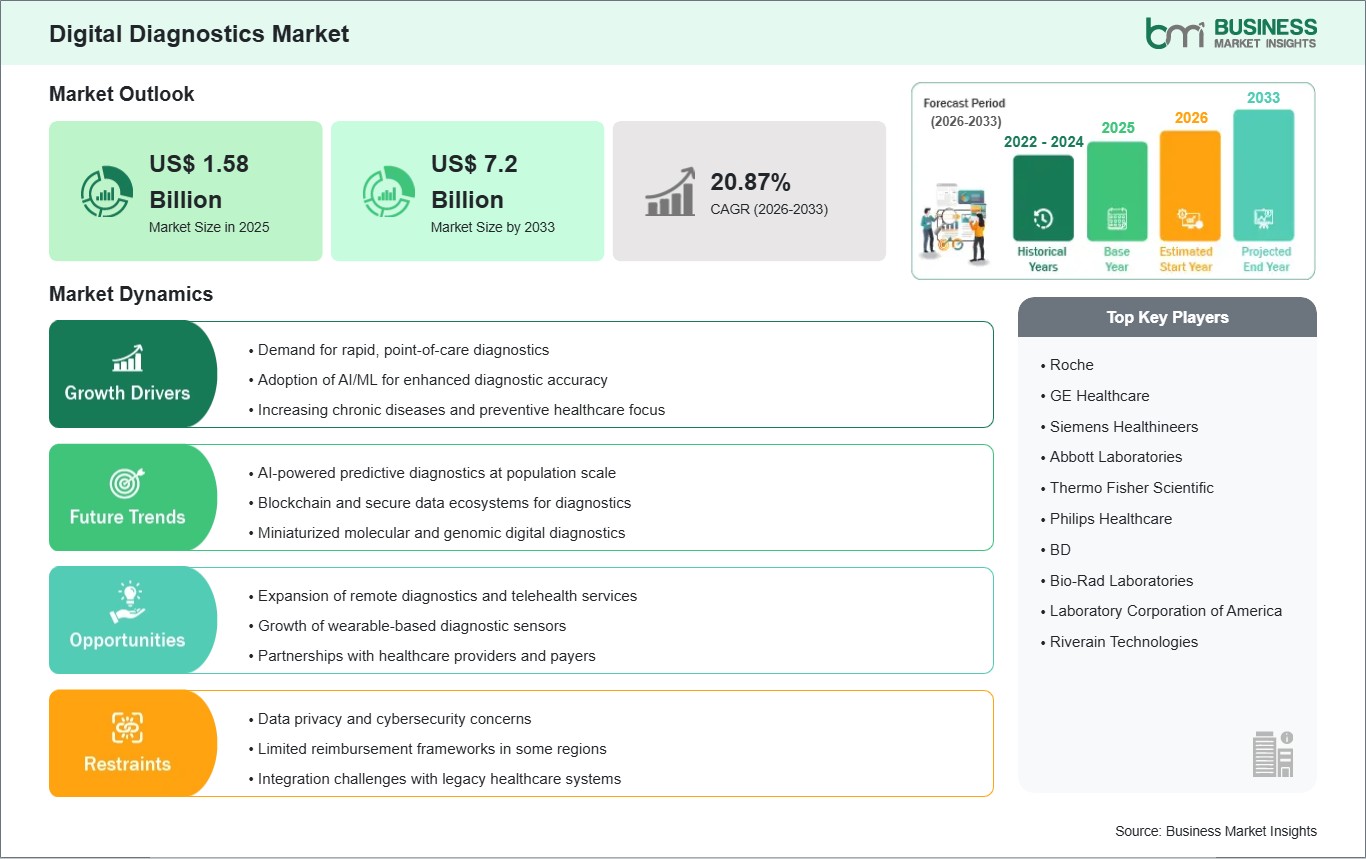

The Digital Diagnostics Market size is expected to reach US$ 7.2 Billion by 2033 from US$ 1.58 Billion in 2025. The market is estimated to record a CAGR of 20.87% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Digital diagnostics is the process by which modern digital technologies are utilized to identify, keep track of, and forecast the state of health conditions in much quicker, more precise, and more efficient ways than traditional ones. In most cases, these solutions are screens which, with the help of electronic health records and telemedicine systems, allow health data to be collected, patients to be monitored, and physicians to be supported in their decisions during consultations to the extent that they become more precise in their diagnosis and can thus intervene even before the disease breaks out throughout various applications in cardiology, oncology, and pathology, as well as in chronic disease management.

At present, the global market for digital diagnostics is expanding at a fast pace, and the main reason for this is the rising number of people suffering from chronic diseases, the growing need for early and correct diagnosis, and the acceptance of digital health solutions. Innovations in technology, especially AI-based imaging, point-of-care devices, and health-monitoring wearables, are changing the diagnostic processes and cutting down the reliance on traditional laboratory infrastructure. The market sees factories burning with investments and product introductions, while partnerships among major players in the sector are a further driving force behind the acceptance. North America is at the forefront presently due to strong healthcare IT infrastructure and early technology adoption, while Asia-Pacific has emerged as the fastest-growing region in the world because of healthcare investments, telemedicine use, and awareness of digital tools. Dangers such as data privacy issues and unusable systems still exist, but innovations in cloud workflow and personalized medicine are anticipated to be the major drivers of long-term growth and healthcare delivery transformation worldwide.

Digital Diagnostics Market - Strategic Insights:

Get more information on this report

Digital Diagnostics Market Segmentation Analysis:

Key segments that contributed to the derivation of the digital diagnostics market analysis are product and services, application, and end-user.

By product and services, the digital diagnostics market is bifurcated into hardware, software and services. The software and services segment dominated the market in 2025.

By application, the market is segmented into cardiology, gynecology, infectious diseases, oncology, diabetes, other applications. The oncology segment held the largest share of the market in 2025.

By end-user, the digital diagnostics market is segmented into hospitals and ASCS, clinical laboratories, academic and research institutes, other end-users. The hospitals and ASCS segment dominated the market in 2025.

Digital Diagnostics Market Drivers and Opportunities:

Rising Adoption of AI-Powered Diagnostic Tools

The quick merger of artificial intelligence (AI) and machine learning (ML) came into the diagnostics workflow as a great force that drove the digital diagnostics market, leading to a very substantial improvement in the accuracy, speed, and efficiency of the whole process. Nowadays, AI-enabled diagnostics are being used in all imaging modalities like X-ray, MRI, and ultrasound, among others, and they are able to spot the presence of anomalies much quicker and with more accuracy than traditional techniques. The influence of AI is seen in innovations like GE HealthCare's Sonic DL AI MRI algorithm, which not only speeds up the scan analysis but also improves the resolution and the platforms that decrease human error and aid real-time data interpretation. AI's ability to reduce the interpretation of high-volume data, lower clinician stress, and promote the use of personalized treatment paths is making it the main reason for investments and the worldwide acceptance of such technology, thereby transforming the diagnostic fields of radiology, pathology, cardiology, and oncology.

Expansion of Telemedicine and Remote Diagnostics

The digital diagnostics market has a remarkable chance to take off due to the gradual increase in integration of telemedicine and remote patient monitoring systems, which are driven by the digitalization of healthcare. As telehealth services become a regular part of the practice—thanks to the demand for remote care and convenience—tools for digital diagnostics are being used on virtual platforms to provide real-time diagnostic results without the need for in-person visits. This integration promotes wider healthcare access, especially in rural and underserved areas where there is limited traditional diagnostic infrastructure. The most recent progress indicates that wearable health devices with new powerful features (e.g., smartwatches performing biomarker analysis for personalized insights) are illustrating how consumer technology can be coupled with clinical diagnostics and thus facilitate market adoption. Moreover, smartphone-based as well as home diagnostic tools are becoming popular, giving patients the advantage of early detection and allowing clinicians to get remote data for faster intervention. The above scenario of telehealth growing and regulatory frameworks adapting to digital care models points to the convergence of digital diagnostics with telemedicine as a transformative opportunity not only to improve care delivery but also to enhance patient outcomes on a global scale.

Digital Diagnostics Market Size and Share Analysis:

By product and services, the digital diagnostics market is bifurcated into hardware, software and services. The software and services segment dominated the market in 2025. The software and services segment lead due to its critical role in interpreting complex diagnostic data, enabling AI-based image analysis, clinical decision support, and integration with healthcare IT systems. Advanced software solutions improve diagnostic accuracy, streamline workflows, and support data analytics across devices, making them indispensable for modern digital diagnostics. This strong value proposition and rising adoption by providers drive its leading position over hardware and services.

By application, the market is segmented into cardiology, gynecology, infectious diseases, oncology, diabetes, other applications. The oncology segment held the largest share of the market in 2025. Within applications, oncology leads as digital diagnostics are heavily applied in cancer detection, where advanced imaging, biomarker analysis, and AI tools enhance early diagnosis and treatment planning. The high global burden of cancer and need for precise, data-driven tools has accelerated adoption in this segment, giving it a larger market share compared to other disease areas.

By end-user, the digital diagnostics market is segmented into hospitals and ASCS, clinical laboratories, academic and research institutes, other end-users. The hospitals and ASCS segment dominated the market in 2025. Hospitals and ambulatory surgical centers (ASCs) dominate because they require comprehensive diagnostic capabilities across specialties, high patient volumes, and substantial healthcare IT infrastructure. Their multi-specialty care environment and investment capacity enable broad deployment of digital diagnostics hardware and software, making them the primary end users.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Roche

GE Healthcare

Siemens Healthineers

Abbott Laboratories

Thermo Fisher Scientific

Philips Healthcare

BD

Bio-Rad Laboratories

Laboratory Corporation of America

Riverain Technologies

Get more information on this report

Digital Diagnostics Market Report Coverage and Deliverables:

The " Digital Diagnostics Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Digital diagnostics market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Digital diagnostics market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Digital diagnostics market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the digital diagnostics market

Detailed company profiles, including SWOT analysis

Digital Diagnostics Market Geographic Insights:

The geographical scope of the digital diagnostics market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The digital diagnostics market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific digital diagnostics market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The Asia-Pacific digital diagnostics market is experiencing robust growth due to several factors that are coming together to change the way healthcare is delivered and technology adoption. The main reason for this change is the increased use of telemedicine and remote patient monitoring, which makes it possible for clinicians to use digital diagnostic tools, such as wearable sensors and mobile health apps, to monitor and diagnose patients outside the hospital, especially in rural areas where access to healthcare is limited. The pandemic of COVID-19 has played a major role in this trend, as it created a new and enduring market for remote consultations and digital care solutions.

The other major reason for this growth is the increase in the number of people suffering from chronic and age-related diseases in countries like China, India, Japan, and South Korea. This situation has made the demand for efficient diagnostic processes that would provide timely detection and management even greater. Governments in the Asia-Pacific region are also investing massively in healthcare digitalization, such as by making the necessary infrastructure, cloud systems, and electronic health systems available to support the integration of AI, machine learning, and other advanced diagnostic technologies. In addition to that, there is a growing consumer awareness of preventive healthcare, rising disposable incomes, and better quality in digital imaging and AI analytics, which are the factors that are collectively encouraging adoption by hospitals, clinics, and patients, leading to sustained growth in the region.

Get more information on this report

Digital Diagnostics Market Research Report Guidance:

The report includes qualitative and quantitative data in the Digital Diagnostics Market across product and services, application, end-user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the digital diagnostics market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the digital diagnostics market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the digital diagnostics market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover Digital Diagnostics Market segments by product and services, application, end-user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the digital diagnostics market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Digital Diagnostics Market News and Key Development:

The digital diagnostics market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the digital diagnostics market are:

In November 2024, Magrabi Health partnered with Digital Diagnostics and Tamer Healthcare to launch LumineticsCore, an AI system for detecting diabetic retinopathy, at its Eye Hospital in Riyadh. LumineticsCore is the first FDA-and SFDA-approved autonomous AI system for diagnosing this leading cause of vision loss. This collaboration aligns with Magrabi Health's rebranding efforts and Saudi Vision 2030's focus on healthcare digitalization.

In November 2025, Hologic, Inc. announced that its Genius Digital Diagnostics System achieved expanded CE marking in the European Union and is now approved to image and review both cell and tissue specimens. With the ability to image the entire slide for review of a broader range of patient sample types, the Genius Digital Diagnostics System will allow European labs to unify digital workflows with one comprehensive solution and support pathologists in their work diagnosing a variety of cancers and other diseases.

Key Sources Referred:

World Health Organization (WHO)Centers for Disease Control and Prevention (CDC)Institute for Health Metrics and EvaluationWorld Bank – Health Data and StatisticsUnited Nations Children’s FundCompany websitesCompany annual reportsCompany investor presentations

The List of Companies - Digital Diagnostics Market

Roche,

GE Healthcare,

Siemens Healthineers,

Abbott Laboratories,

Thermo Fisher Scientific,

Philips Healthcare,

BD,

Bio-Rad Laboratories,

Laboratory Corporation of America,

Riverain Technologies

Frequently Asked Questions

How big is the Digital Diagnostics Market?

The Digital Diagnostics Market is valued at US$ 1.58 Billion in 2025, it is projected to reach US$ 7.2 Billion by 2033.

What is the CAGR for Digital Diagnostics Market by (2026 - 2033)?

As per our report Digital Diagnostics Market, the market size is valued at US$ 1.58 Billion in 2025, projecting it to reach US$ 7.2 Billion by 2033. This translates to a CAGR of approximately 20.87% during the forecast period.

What segments are covered in this report?

The Digital Diagnostics Market report typically cover these key segments-

Product and Services (Hardware, Software and Services)

Application (Cardiology, Gynecology, Infectious Diseases, Oncology, Diabetes, Other Applications)

End-User (Hospitals and ASCs, Clinical Laboratories, Academic and Research Institutes, Other End-Users)

What is the historic period, base year, and forecast period taken for Digital Diagnostics Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Digital Diagnostics Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Digital Diagnostics Market?

The Digital Diagnostics Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Roche,

GE Healthcare,

Siemens Healthineers,

Abbott Laboratories,

Thermo Fisher Scientific,

Philips Healthcare,

BD,

Bio-Rad Laboratories,

Laboratory Corporation of America,

Riverain Technologies

Who should buy this report?

The Digital Diagnostics Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Digital Diagnostics Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Digital Diagnostics Market

Get Free Sample For Digital Diagnostics Market