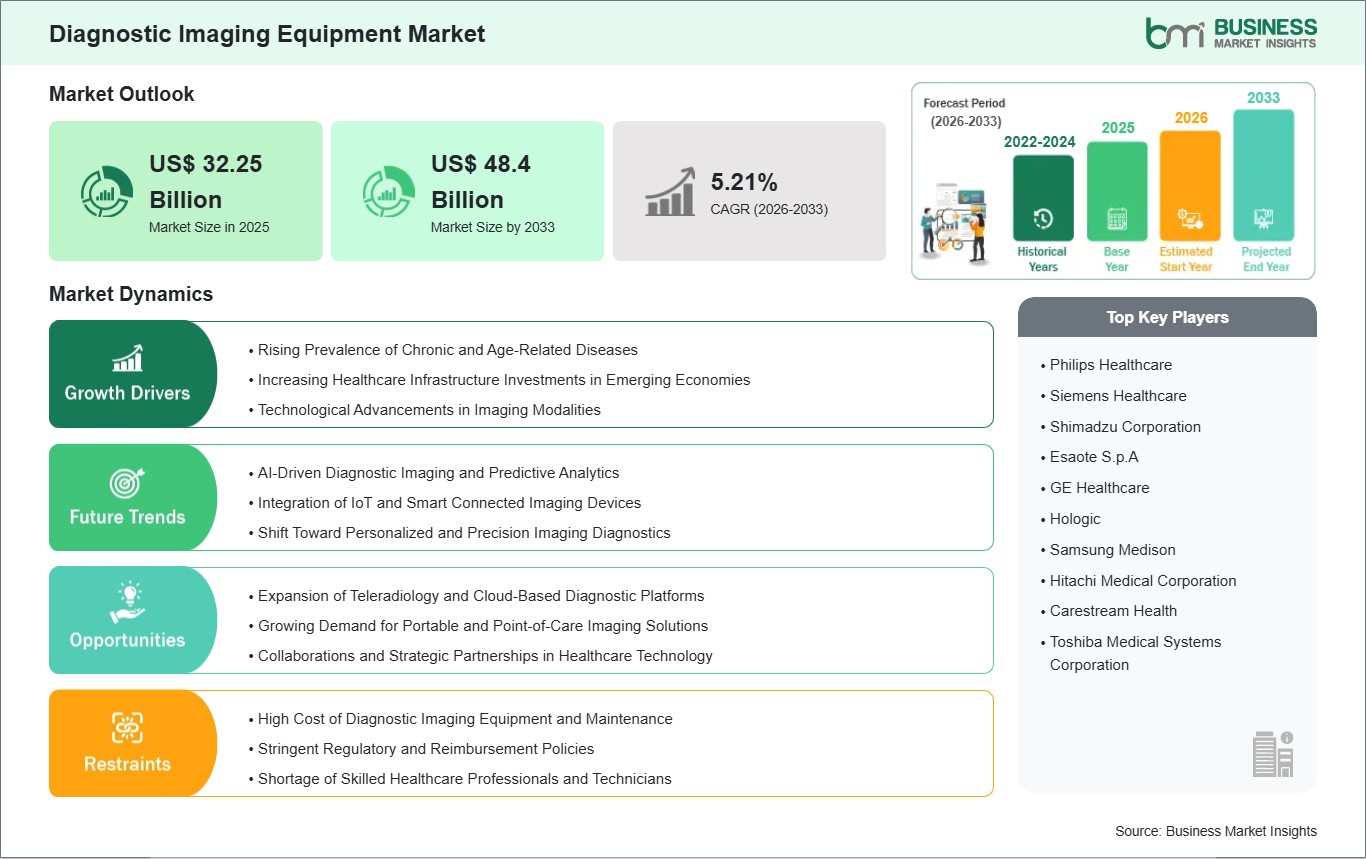

The Diagnostic Imaging Equipment Market size is expected to reach US$ 48.4 Billion by 2033 from US$ 32.25 Billion in 2025. The market is estimated to record a CAGR of 5.21% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Diagnostic imaging equipment describes medical technologies which produce body interior visualizations to help with disease and injury diagnosis and treatment monitoring and medical treatment execution. X-ray systems and computed tomography (CT) and magnetic resonance imaging (MRI) and ultrasound and nuclear imaging and fluoroscopy all belong to this category of medical imaging equipment.

The global diagnostic imaging equipment market experiences steady development through ongoing technological progress and expanded clinical use cases and fresh digital and artificial intelligence-based solutions which become increasingly integrated into medical operations. The demand for medical services exists because more people need treatment for chronic diseases which include cancer and cardiovascular disorders and neurological conditions together with the growing need for correct medical assessments and the increase in older population segments. The healthcare sector throughout the world needs advanced imaging systems which provide better diagnostic accuracy and shorter scan durations and reduced radiation levels and better operational performance. Emerging economies experience fast economic development because their healthcare systems expand and their people gain more access to diagnostic facilities and both public and private sectors invest in modern medical technology. The equipment markets in developed areas concentrate on replacing existing equipment and enhancing software and improving patient outcomes through value-based healthcare solutions. Manufacturers face three major obstacles because they must comply with regulations and manage expensive equipment and deal with unpredictable reimbursement rates which leads them to pursue portable cost-efficient solutions that can expand their operations. The market reflects a transition from standalone imaging devices to integrated, data-driven diagnostic ecosystems that support precision medicine and improved patient outcomes across diverse care settings.

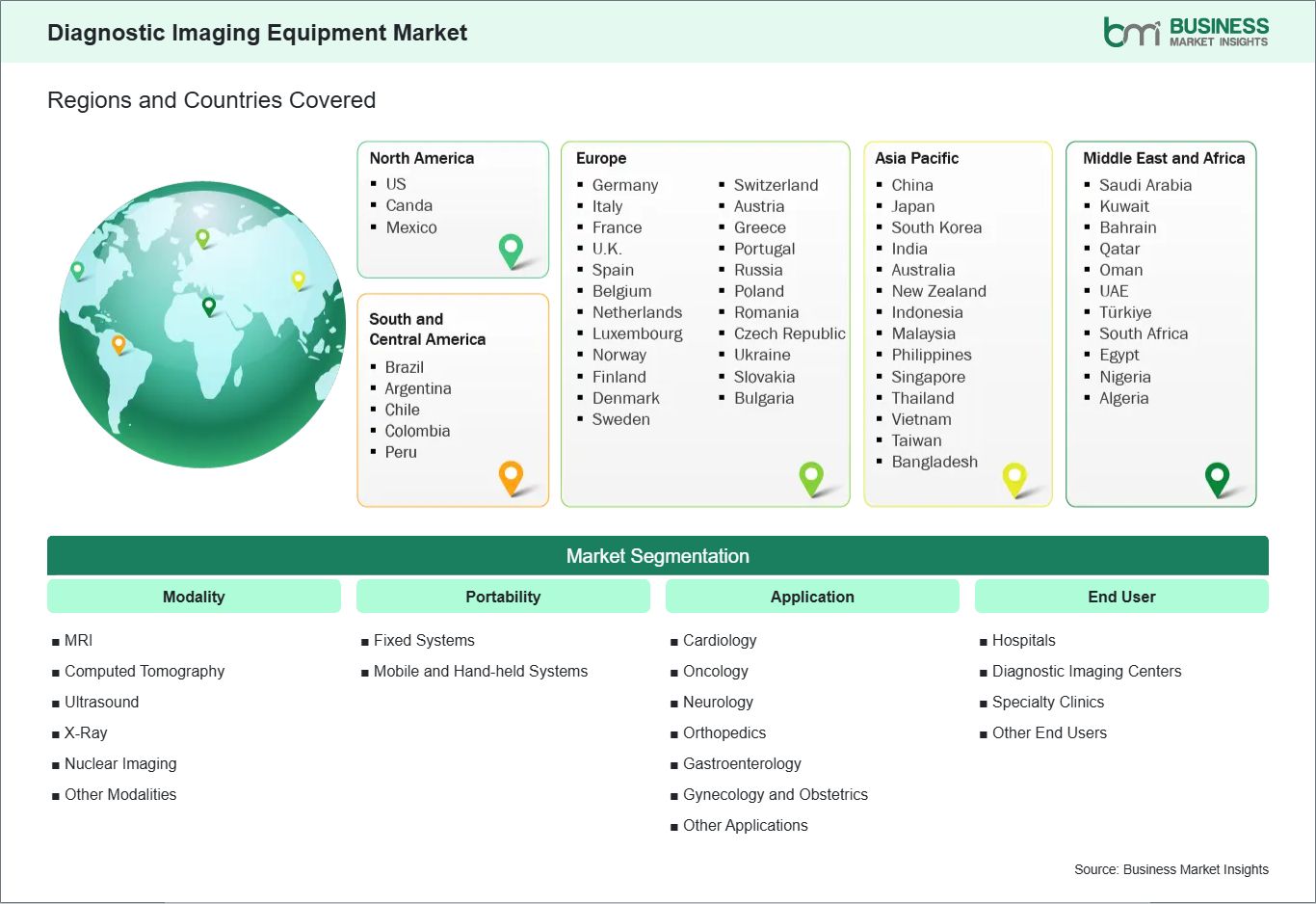

Key segments that contributed to the derivation of the diagnostic imaging equipment market analysis are modality, portability, application, end user.

By modality, the diagnostic imaging equipment market is categorized into MRI, computed tomography, ultrasound, X-ray, nuclear imaging, other modalities. The X-ray segment held the largest share of the market in 2025.

By portability, the market is bifurcated into fixed systems, mobile and hand-held systems. The fixed systems segment held a larger share of the market in 2025.

By application, the market is segmented into cardiology, oncology, neurology, orthopedics, gastroenterology, gynecology and obstetrics, other applications. The oncology segment held the largest share of the market in 2025.

By end user, the diagnostic imaging equipment market is segmented into hospitals, diagnostic imaging centers, specialty clinics, other end users. The hospitals segment dominated the market in 2025.

Diagnostic Imaging Equipment Market Drivers and Opportunities:

Integration of Artificial Intelligence and Advanced Imaging Technologies

The diagnostic imaging equipment market experiences growth because hospitals adopt artificial intelligence technologies together with modern imaging methods which provide better diagnostic results and improved operational processes and medical decision-making assistance. Scanners powered by artificial intelligence technology establish better diagnostic certainty because they process complex visual content through automated systems which can discover hidden details while decreasing diagnostic mistakes. Between 2023 and 2025, the medical imaging industry introduced more than 1500 new imaging systems which featured artificial intelligence and low-radiation imaging and combined different imaging techniques. The healthcare industry adopts advanced medical imaging technology because it enables early disease detection and accurate diagnosis and operational improvements which are essential for high-demand medical specialties such as oncology and cardiology and shows how artificial intelligence technology drives industry growth.

Expansion into Portable and Point-of-Care Imaging

The diagnostic imaging equipment market will experience major growth because portable and point-of-care (POC) imaging solutions of medical facilities which extend their services beyond traditional hospital environments. Mobile CT scanners and compact ultrasound units which belong to the category of portable imaging devices, allow medical professionals to perform quick diagnostic tests at emergency rooms and intensive care units and rural clinics and remote locations, because these devices fulfill diagnostic requirements which permanent diagnostic equipment cannot meet. The introduction of next-generation AI-powered mobile CT systems by Samsung in India enables clinical facilities to implement these systems without needing extensive medical infrastructure because they provide better patient care through advanced diagnostic capabilities. Decentralized healthcare models enable medical facilities to diagnose patients more rapidly while decreasing patient transfer requirements and providing undeserved communities with better access to specialized imaging technology. The current trend provides manufacturers with a chance to create portable imaging solutions which have low expenses and high-performance capabilities that enable medical facilities to expand their diagnostic services while improving their healthcare systems across the globe.

Diagnostic Imaging Equipment Market Size and Share Analysis:

By modality, the diagnostic imaging equipment market is categorized into MRI, computed tomography, ultrasound, X-ray, nuclear imaging, other modalities. The X-ray segment held the largest share of the market in 2025. X-ray systems lead due to their widespread availability, cost-effectiveness, and broad clinical utility across emergency care, orthopedics, pulmonology, and dental imaging. They are often the first-line diagnostic tool because of fast imaging times and relatively low radiation doses in modern digital systems. High installation base, frequent use in routine examinations, and continuous upgrades to digital radiography and AI-assisted image analysis further reinforce X-ray's dominance across both developed and emerging healthcare markets.

By portability, the market is bifurcated into fixed systems, mobile and hand-held systems. The fixed systems segment held a larger share of the market in 2025. Fixed diagnostic imaging systems dominate as they deliver higher imaging power, resolution, and reliability compared to mobile or hand-held alternatives. Modalities such as MRI, CT, and high-end X-ray systems require stable infrastructure, shielding, and advanced cooling systems, making fixed installations essential in hospitals and imaging centers. Their ability to support complex, high-volume diagnostic workflows and advanced clinical applications ensures sustained preference, particularly for critical and specialized diagnostic procedures.

By application, the market is segmented into cardiology, oncology, neurology, orthopedics, gastroenterology, gynecology and obstetrics, other applications. The oncology segment held the largest share of the market in 2025. Oncology leads due to the critical role of imaging in cancer detection, staging, treatment planning, and therapy monitoring. Modalities such as CT, MRI, PET, and hybrid imaging are integral throughout the cancer care continuum. The global rise in cancer incidence, increasing screening programs, and growing demand for precision diagnostics have significantly boosted imaging utilization in oncology, making it the most imaging-intensive and technologically advanced application area.

By end user, the diagnostic imaging equipment market is segmented into hospitals, diagnostic imaging centers, specialty clinics, other end users. The hospitals segment dominated the market in 2025. Hospitals lead the end-user segment as they serve as primary hubs for advanced diagnostics, emergency care, and complex procedures. They house a wide range of imaging modalities under one roof and handle high patient volumes across multiple specialties. Strong capital investment capacity, access to skilled radiology professionals, and the need for integrated diagnostic services support hospital dominance. Additionally, hospitals increasingly adopt advanced imaging systems to enhance clinical outcomes and operational efficiency.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Philips Healthcare

Siemens Healthcare

Shimadzu Corporation

Esaote S.p.A

GE Healthcare

Hologic

Samsung Medison

Hitachi Medical Corporation

Carestream Health

Toshiba Medical Systems Corporation

Get more information on this report

Diagnostic Imaging Equipment Market Report Coverage and Deliverables:

The " Diagnostic Imaging Equipment Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Diagnostic imaging equipment market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Diagnostic imaging equipment market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Diagnostic imaging equipment market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the diagnostic imaging equipment market

Detailed company profiles, including SWOT analysis

The geographical scope of the diagnostic imaging equipment market report is divided into five regions: North America, Asia Pacific, Europe, Middle East and Africa, and South and Central America. The diagnostic imaging equipment market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific diagnostic imaging equipment market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The Asia-Pacific diagnostic imaging equipment market is experiencing robust growth, due to several key factors. The rising number of elderly people in Japan, China, and South Korea brings about an increase in chronic diseases which need imaging studies for both early diagnosis and ongoing treatment. The healthcare system in India, China, and Southeast Asian countries is expanding because rising healthcare costs and growing insurance coverage help more patients obtain advanced diagnostic services, which leads hospitals and clinics to purchase new imaging equipment. High-end medical systems such as MRI and CT scanners are being obtained by healthcare organizations because of China-based hospital modernization initiatives and Australia-based digital health implementation strategies. The entry of private medical facilities and diagnostic networks into the market has increased competition in the area, which has resulted in more imaging facilities being established in both urban and semi-urban regions. The market is expanding because of technological innovations which provide local solutions, such as portable ultrasound devices that Indian rural clinics can use. The growing public understanding of preventive healthcare together with screening initiatives drives people to use diagnostic imaging more frequently, which creates ongoing market expansion.

Get more information on this report

Diagnostic Imaging Equipment Market Research Report Guidance:

The report includes qualitative and quantitative data in the diagnostic imaging equipment market across modality, portability, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the diagnostic imaging equipment market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the diagnostic imaging equipment market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the diagnostic imaging equipment market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 11 cover diagnostic imaging equipment market segments by modality, portability, application, end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue forecast and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the diagnostic imaging equipment market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Diagnostic Imaging Equipment Market News and Key Development:

The diagnostic imaging equipment market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the diagnostic imaging equipment market are:

In January 2025, Siemens Healthineers, a leading medical devices company, showcased a comprehensive range of diagnostic imaging solutions at Asian Oceanian Congress of Radiology (AOCR) 2025 in Chennai. Highlighting the importance of informed clinical decision-making across the entire healthcare continuum, the company introduced its innovative portfolio in MRI, CT, digital X-ray, and ultrasound, reinforcing its commitment to advancing precision medicine.

In January 2025, NVIDIA announced a collaboration with GE HealthCare to advance innovation in autonomous imaging, which aims to create autonomous X-ray technologies and ultrasound applications. Medical imaging systems must possess both environmental understanding and operational capabilities to establish X-ray and ultrasound system autonomy. The system creates an automated process which handles all tasks from patient positioning to image acquisition and quality assessment.

Key Sources Referred:

World Health Organization (WHO)Centers for Disease Control and PreventionInstitute for Health Metrics and EvaluationUNICEF - Health and Nutrition Data -OECD Health StatisticsCompany websitesCompany annual reportsCompany investor presentations

The List of Companies - Diagnostic Imaging Equipment Market

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Frequently Asked Questions

How big is the Diagnostic Imaging Equipment Market?

The Diagnostic Imaging Equipment Market is valued at US$ 32.25 Billion in 2025, it is projected to reach US$ 48.4 Billion by 2033.

What is the CAGR for Diagnostic Imaging Equipment Market by (2026 - 2033)?

As per our report Diagnostic Imaging Equipment Market, the market size is valued at US$ 32.25 Billion in 2025, projecting it to reach US$ 48.4 Billion by 2033. This translates to a CAGR of approximately 5.21% during the forecast period.

What segments are covered in this report?

The Diagnostic Imaging Equipment Market report typically cover these key segments-

Modality (MRI, Computed Tomography, Ultrasound, X-Ray, Nuclear Imaging, Other Modalities)

Portability (Fixed Systems, Mobile and Hand-held Systems)

Application (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology and Obstetrics, Other Applications)

End User (Hospitals, Diagnostic Imaging Centers, Specialty Clinics, Other End Users)

What is the historic period, base year, and forecast period taken for Diagnostic Imaging Equipment Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Diagnostic Imaging Equipment Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Diagnostic Imaging Equipment Market?

The Diagnostic Imaging Equipment Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Philips Healthcare

Siemens Healthcare

Shimadzu Corporation

Esaote S.p.A

GE Healthcare

Hologic

Samsung Medison

Hitachi Medical Corporation

Carestream Health

Toshiba Medical Systems Corporation

Who should buy this report?

The Diagnostic Imaging Equipment Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Diagnostic Imaging Equipment Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Diagnostic Imaging Equipment Market

Get Free Sample For Diagnostic Imaging Equipment Market