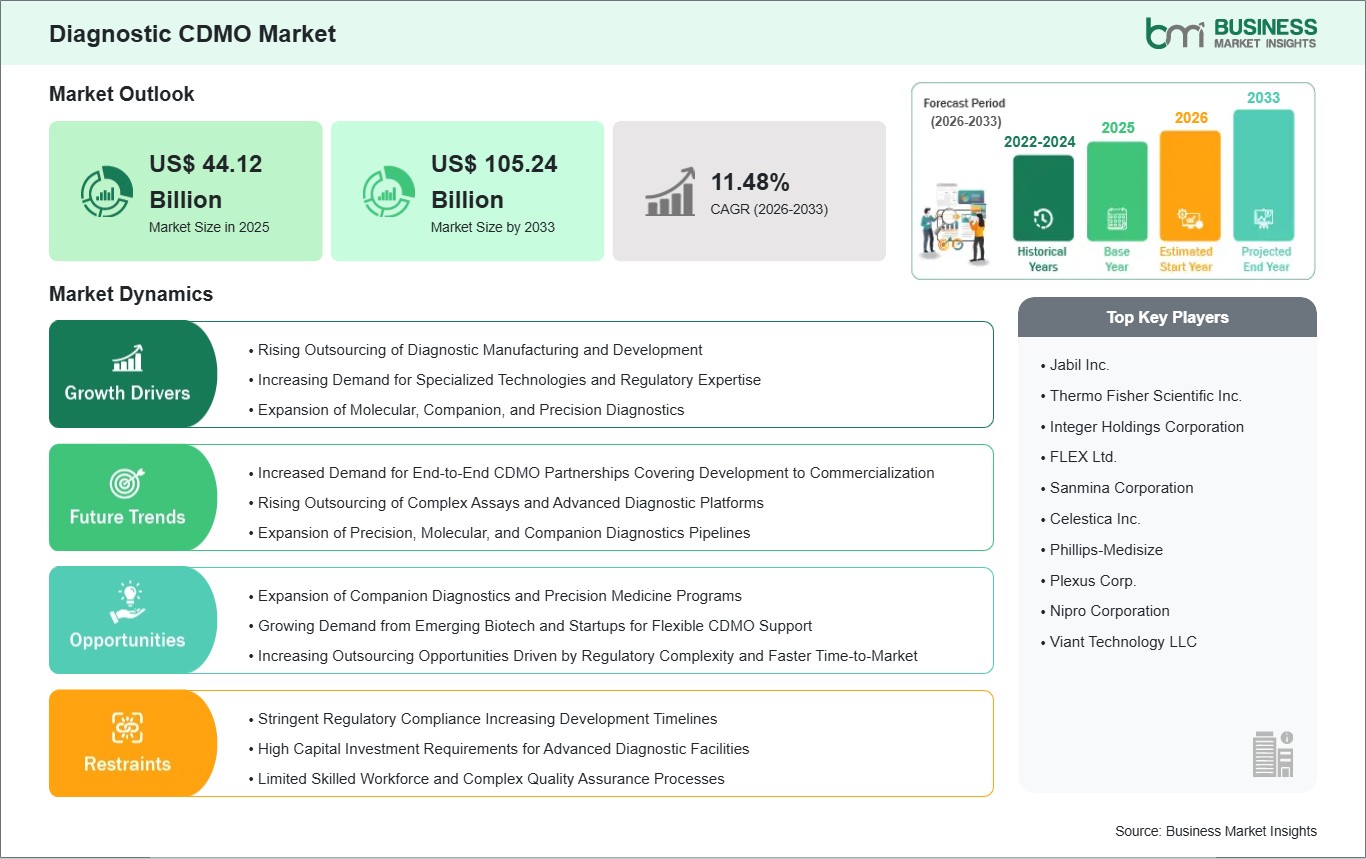

The Diagnostic CDMO Market size is expected to reach US$ 105.24 Billion by 2033 from US$ 44.12 Billion in 2025. The market is estimated to record a CAGR of 11.48% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The Diagnostic Contract Development and Manufacturing Organization (CDMO) market is experiencing a profound transformation as diagnostic companies increasingly pivot toward outsourcing to manage rising R&D costs and complex regulatory environments. Diagnostic CDMOs provide end-to-end services, from initial product design and component manufacturing to final assembly and regulatory filing. This shift is primarily driven by the "decentralization of diagnostics," where there is an urgent demand for rapid, point-of-care (POC) testing and home-based diagnostic kits. By partnering with CDMOs, OEMs can leverage advanced manufacturing technologies like automation, microfluidics, and 3D printing without the heavy capital expenditure of building in-house facilities.

While the market is bolstered by the rising global burden of chronic and infectious diseases, it faces challenges such as stringent and evolving regulatory frameworks (like the EU's IVDR) and the high technical barrier for Class III (high-risk) device manufacturing. However, massive opportunities are emerging in the integration of AI-driven digital diagnostics, the growth of personalized medicine requiring companion diagnostics, and the expansion of manufacturing hubs in the Asia-Pacific region, which offers both cost advantages and skilled technical talent.

Diagnostic CDMO Market - Strategic Insights:

Get more information on this report

Diagnostic CDMO Market Segmentation Analysis:

Key segments that contributed to the derivation of the Diagnostic CDMO market analysis are service, class, application, and end use.

By Service, the market is segmented into Contract Manufacturing, Contract Development, Packaging, Labelling & Sterilization, Regulatory Affairs, and Others. The Contract Manufacturing segment is further divided into Accessories, Assembly, Component, and Device Manufacturing. The Contract Development segment is further categorized into Product Design, Testing & Validation, and Quality Management.

By Class, the market is divided into Class I, Class II, and Class III.

By Application, the market is segmented into Infectious Disease Diagnostics, Oncology Diagnostics, Cardiometabolic Diagnostics, Genetic & Genomic Testing, and Respiratory & Critical Care Diagnostics.

By End Use, the market is categorized into Original Equipment Manufacturers (OEMs), Pharmaceutical & Biopharmaceutical Companies, and Others.

Diagnostic CDMO Market Drivers and Opportunities:

Rising Demand for Point-of-Care and Rapid Testing

The ongoing shift from traditional centralized laboratory testing to rapid, patient-side diagnostics is emerging as a powerful catalyst across the healthcare and diagnostics market. Both consumers and healthcare providers now expect near-instant results for a wide range of health parameters, from routine glucose monitoring and cholesterol checks to the rapid detection of infectious diseases. This demand for speed, convenience, and real-time decision-making is pushing OEMs to redesign complex laboratory assays into compact, user-friendly, point-of-care solutions. As a result, CDMOs with specialized capabilities in miniaturization, microfluidics, assay integration, and portable device engineering are increasingly sought after. These partners play a critical role in enabling OEMs to deliver accurate, reliable diagnostic tools that function seamlessly outside centralized lab environments.

Advancements in Molecular Diagnostics and Precision Medicine

The rapid expansion of genetic and genomic testing has created a significant opportunity for CDMOs that possess deep expertise in molecular biology and advanced analytical technologies. As pharmaceutical companies increasingly develop companion diagnostics to pair with highly targeted therapies, particularly in oncology, they depend on specialized CDMO partners to support the intricate R&D, validation, and precision manufacturing these diagnostics require. These tools must meet rigorous regulatory standards and deliver exceptionally accurate results, making the role of CDMOs crucial. By offering capabilities such as assay design, biomarker validation, and scalable production, CDMOs enable pharma companies to accelerate personalized medicine development.

Diagnostic CDMO Market Size and Share Analysis:

The Diagnostic CDMO market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within service, class, application, and end use, offering insights into their contribution to overall market performance.

Diagnostic CDMO is a highly specialized market where growth is driven due to massive demand for Class II infectious disease kits and the high-value innovation in genetic and oncology diagnostics. Contract Manufacturing currently serves as the market's financial anchor, accounting for nearly half of all revenue, as global OEMs move away from in-house production to optimize their supply chains and reduce capital expenditure. However, a significant shift is occurring toward Contract Development and Class III devices, fueled by the "precision medicine" boom, which requires sophisticated, high-risk diagnostic tools and end-to-end design services. While Hospitals and Labs remain the traditional end users, the convergence of drug and device development is making Pharmaceutical Companies a high-growth vertical for CDMOs, particularly in the creation of companion diagnostics. Ultimately, the market is transitioning from a simple "build-to-print" model to a strategic partnership ecosystem where CDMOs act as critical innovation hubs for the next generation of rapid, molecular, and point-of-care testing.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Jabil Inc.

Thermo Fisher Scientific Inc.

Integer Holdings Corporation

FLEX Ltd.

Sanmina Corporation

Celestica Inc.

Phillips-Medisize

Plexus Corp.

Nipro Corporation

Viant Technology LLC

Get more information on this report

Diagnostic CDMO Market Report Coverage and Deliverables:

The "Diagnostic CDMO Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Diagnostic CDMO market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Diagnostic CDMO market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Diagnostic CDMO market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Diagnostic CDMO market

Detailed company profiles, including SWOT analysis

Diagnostic CDMO Market Geographic Insights:

The geographical scope of the Diagnostic CDMO market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America.

North America is a high-growth market supported by a robust ecosystem of biotech startups and a stringent, yet clear, FDA regulatory pathway. Europe is currently navigating the implementation of the In Vitro Diagnostic Regulation (IVDR), which has increased the demand for CDMOs with high-tier regulatory affairs expertise. Asia Pacific is a rapidly growing region, as global OEMs "resell" or "de-risk" their supply chains by moving manufacturing to hubs in China, India, and Southeast Asia. In the Middle East and Africa, the market is growing through the development of local diagnostic manufacturing to reduce reliance on imports. South and Central America are witnessing growth as clinical laboratory networks modernize and expand.

Get more information on this report

Diagnostic CDMO Market Research Report Guidance:

The report includes qualitative and quantitative data in the Diagnostic CDMO market across service, class, application, end use, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Diagnostic CDMO market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Diagnostic CDMO market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Diagnostic CDMO market scenario in terms of historical market revenues and forecast till the year 2033.

Chapters 7 to 10 cover the Diagnostic CDMO market segments by service, class, application, end use, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market volume, revenue forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Diagnostic CDMO market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Diagnostic CDMO Market News and Key Development:

The Diagnostic CDMO market is evaluated by gathering qualitative and quantitative data post-primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Diagnostic CDMO market are:

In June 2025, Zydus Lifesciences has announced its entry into the global biologics contract development and manufacturing organisation (CDMO) market with a planned acquisition of two manufacturing facilities from US-based Agenus for up to $125 million (around INR 1,070 crore).

In April 2025, Roche announces $50bn US investment in pharma and diagnostics. Once the new and expanded manufacturing capacities are operational, Roche aims to export more medicines from the US than it imports.

In February 2025, Jabil Inc., a global leader in engineering, manufacturing, and supply chain solutions, announced the successful acquisition of Pharmaceutics International, Inc. (Pii), a contract development and manufacturing organization (CDMO) specializing in early-stage, clinical, and commercial volume aseptic filling, lyophilization, and oral solid dose manufacturing.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Diagnostic CDMO Market

Jabil Inc.

Thermo Fisher Scientific Inc.

Integer Holdings Corporation

FLEX Ltd.

Sanmina Corporation

Celestica Inc.

Phillips-Medisize

Plexus Corp.

Nipro Corporation

Viant Technology LLC

Frequently Asked Questions

How big is the Diagnostic CDMO Market?

The Diagnostic CDMO Market is valued at US$ 44.12 Billion in 2025, it is projected to reach US$ 105.24 Billion by 2033.

What is the CAGR for Diagnostic CDMO Market by (2026 - 2033)?

As per our report Diagnostic CDMO Market, the market size is valued at US$ 44.12 Billion in 2025, projecting it to reach US$ 105.24 Billion by 2033. This translates to a CAGR of approximately 11.48% during the forecast period.

What segments are covered in this report?

The Diagnostic CDMO Market report typically cover these key segments-

End Use (Original Equipment Manufacturers (OEMs), Pharmaceutical & Biopharmaceutical Companies, Others)

What is the historic period, base year, and forecast period taken for Diagnostic CDMO Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Diagnostic CDMO Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Diagnostic CDMO Market?

The Diagnostic CDMO Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Jabil Inc.

Thermo Fisher Scientific Inc.

Integer Holdings Corporation

FLEX Ltd.

Sanmina Corporation

Celestica Inc.

Phillips-Medisize

Plexus Corp.

Nipro Corporation

Viant Technology LLC

Who should buy this report?

The Diagnostic CDMO Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Diagnostic CDMO Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Diagnostic CDMO Market

Get Free Sample For Diagnostic CDMO Market