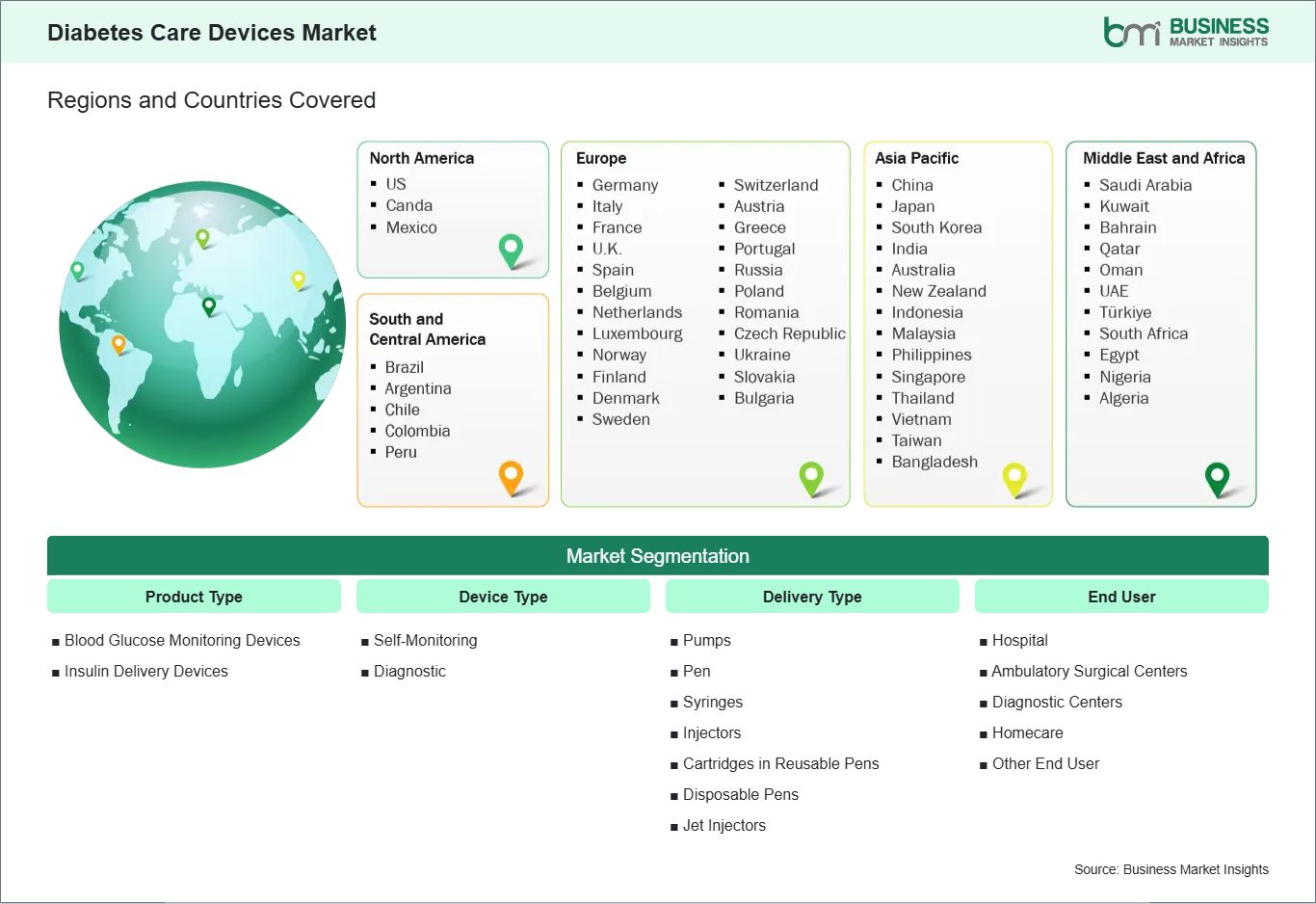

By product type, the diabetes care devices market is categorized into blood glucose monitoring devices, insulin delivery devices. The blood glucose monitoring devices segment held the largest share of the market in 2025. Blood glucose monitoring devices lead the market because they are essential for daily diabetes management and used far more frequently than insulin delivery systems. Devices like self-monitoring meters and continuous glucose monitoring (CGM) systems offer real-time, user-friendly glucose readings, empowering patients to adjust diet and therapy immediately. Their broad accessibility, lower cost, and compatibility with digital health platforms drive higher adoption globally across all patient types.

By device type, the market is bifurcated into self-monitoring, diagnostic. The self-monitoring segment held a larger share of the market in 2025. Self-monitoring devices dominate compared with diagnostic devices because diabetes management requires frequent and ongoing glucose checks by patients themselves. Self-monitoring tools, including SMBG meters and wearable CGMs, provide immediate actionable data that supports daily treatment decisions and reduces clinic visits. This convenience, coupled with technology improvements and mobile connectivity for remote care, makes self-monitoring the primary choice for long-term management of both Type 1 and Type 2 diabetes.

By delivery type, the market is segmented into pumps, pen, syringes, injectors, cartridges in reusable pens, disposable pens, jet injectors. The pen segment held the largest share of the market in 2025. Among delivery modes, pens often lead due to their ease of use, portability, and patient preference over more complex pumps or traditional syringes. Pens simplify dosing (especially disposable and smart pens with dose tracking), making them popular with both insulin-dependent Type 2 and Type 1 populations. Their balance of convenience, affordability, and accuracy drives sustained volume share globally, particularly in self-administered home care settings.

By end user, the diabetes care devices market is segmented into hospital, ambulatory surgical centers, diagnostic centers, homecare, other end user. The hospital segment dominated the market in 2025. Hospitals remain the largest end-user segment as they are the primary point of diagnosis, treatment initiation, and advanced device deployment (like professional CGM systems and pumps). They centralize multidisciplinary diabetes care, handle severe or complex cases, and integrate device use within broader inpatient and outpatient programs. Insurance coverage and institutional purchasing power further anchor hospitals as the leading end-user globally.