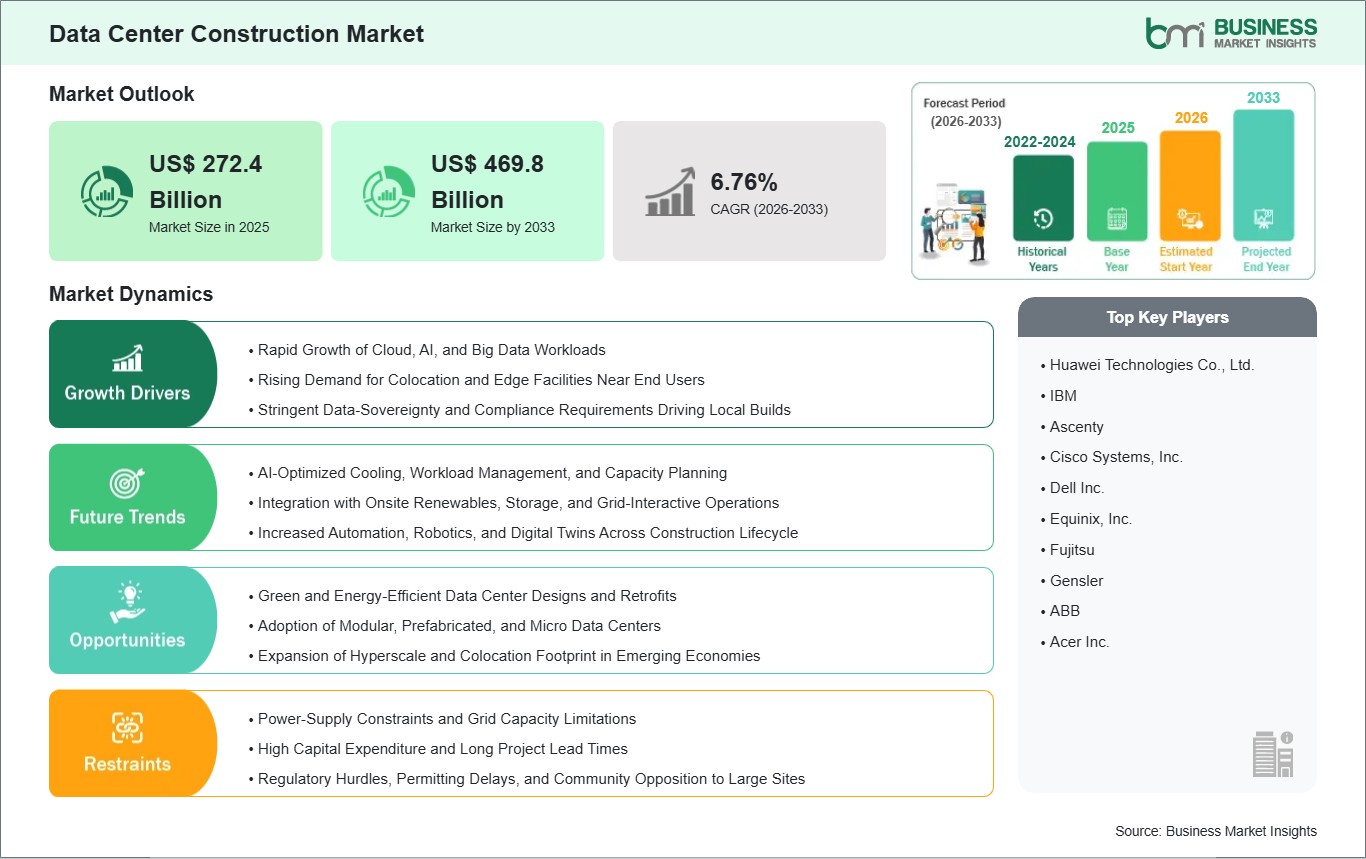

The Data Center Construction Market size is expected to reach US$ 469.8 Billion by 2033 from US$ 272.4 Billion in 2025. The market is estimated to record a CAGR of 7.05% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The data center construction market is the basis of the world's digital infrastructure, which includes physical facilities for cloud platforms, enterprise IT, content delivery, and AI workloads. These places are the integration of IT, power, and cooling systems that provide secure, always on processing capacity for industries, e.g. banking, telecommunications, ecommerce, manufacturing, and government services. Essentially, modern data centers can boast of being very reliable, having scalable compute, and the possibility of placing capacity close to users for low latency applications such as streaming, gaming, and industrial automation.

The market expansion is a result of increasing cloud adoption, rapid data traffic growth, and the rise of hyperscale and colocation providers who are building larger campuses across regions. Edge computing, 5G rollout, and AI training clusters are the reasons why demand for new and upgraded facilities with higher rack densities and advanced cooling is growing so fast.

However, the industry is weighed down by high capital costs, grid power constraints, lack of land in key metros, and stricter environmental and permitting regulations. Despite that, there are still plenty of exciting opportunities in emerging markets, brownfield retrofits, modular and prefabricated builds, and the energy efficient designs, renewable integration, and innovative cooling technologies that lower carbon footprint while enabling capacity to grow.

Data Center Construction Market - Strategic Insights:

Get more information on this report

Data Center Construction Market Segmentation Analysis:

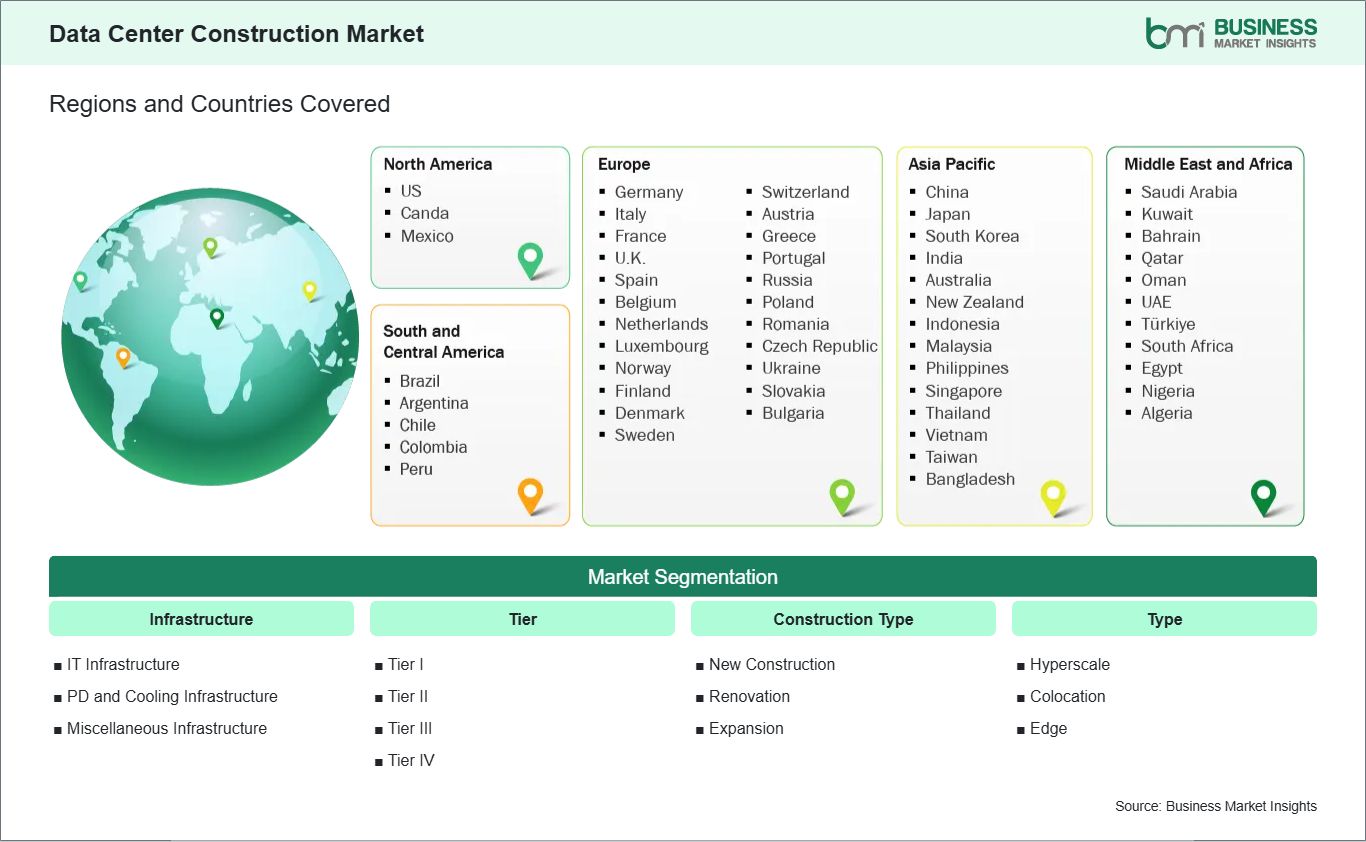

Key segments that contributed to the derivation of the Data Center Construction market analysis are infrastructure, tier, construction type, type, and end user.

By infrastructure, the data center construction market is segmented into IT infrastructure, PD and cooling infrastructure, and miscellaneous infrastructure. The IT infrastructure segment accounted for the largest share of the market in 2024.

By tier, the market is segmented into Tier I, Tier II, Tier III, and Tier IV. The Tier III segment dominated the market in 2024.

By construction type, the market is segmented into new construction, renovation, and expansion. The new construction segment held the largest share of the market in 2024.

By type, the market is segmented into hyperscale, colocation, and edge. The colocation segment held the largest share of the market in 2024.

By end user, the market is segmented into IT and telecommunications, BFSI, and government. The IT and telecommunications segment held the largest share of the market in 2024.

Data Center Construction Market Drivers and Opportunities:

Cloud, AI, and Data Explosion

The data center construction market is largely driven by the global surge in cloud computing, AI, and other data, intense digital services. Hyperscale cloud providers, OTT platforms, and big enterprises are expanding their infrastructures to support video streaming, SaaS, fintech, gaming, and generative AI workloads which require huge amounts of low, latency compute and storage capacity. Worldwide IP traffic and data creation keep increasing at an exponential rate which is forcing operators to build new campuses as well as expand their existing facilities in strategic hubs and emerging regions.

Meanwhile, enterprises are also upgrading their old on, premises infrastructures and adopting hybrid, cloud models which need colocation and edge data centers close to industrial sites and areas with high population densities in order to meet latency and data, sovereignty requirements. The introduction of 5G and the increase in the number of connected devices are, therefore, putting more pressure on networks, thus, creating a need for more edge facilities that can process the data closer to end users.

Data center location decisions are becoming increasingly influenced by government and regulatory incentives for digital economy initiatives, e, governance, and localization rules. The trends combine to form a continued pipeline of greenfield projects, brownfield expansions, and upgrades, thus, firmly positioning data center construction as a key enabler of the digital transformation and AI, driven innovation across the major industries.

Sustainable and Modular Data Centers

A major opportunity in the data center construction market lies in changes made in the design of facilities and new energy, efficient, modular, and sustainable structures that can respond to the rapidly increasing environmental and operational challenges. Data centers still represent one of the largest consumers of electricity and, as such, they are getting a lot of attention from regulators, utilities, and communities, especially in power, constrained metros. Consequently, the demand for high, efficiency cooling (liquid, immersion, free, air), advanced power distribution, real, time energy management, and the installation of on, site renewables and battery storage to lower the PUE as well as the carbon footprint is rising.

Construction firms and technology vendors that are able to deliver low, carbon, water, efficient campuses along with verifiable sustainability metrics are turning out to be the most favored by hyper scalers and colocation providers who have ambitious net, zero commitments. The requirement for prefabricated and modular data centers, which can shorten deployment timelines, standardize quality, and enable incremental capacity additions, is raising this being a perfect solution for emerging markets, remote industrial sites, and latency, sensitive edge locations. In such situations, the modular solutions provide the capability to react quickly to changes.

Data Center Construction Market Size and Share Analysis:

By infrastructure, the data center construction market is divided into IT infrastructure, PD and cooling infrastructure, and miscellaneous infrastructure. The IT infrastructure segment was the largest contributor to the market in 2024. IT infrastructure refers to the core computing hardware of data centers, which includes servers, storage, and networking equipment, and this is what undergoes continuous upgrades to support increased workloads and the virtualization process.

By tier, the market is divided into Tier I, Tier II, Tier III, and Tier IV. The Tier III segment had the largest share of the market in 2024. Tier III data centers provide high availability with several distribution paths and concurrent maintainability at a level lower than Tier IV, thus, most colocation and enterprise facilities choose them.

By construction type, the market is divided into new construction, renovation, and expansion. In 2024, the new construction segment was the major contributor to the market. Greenfield projects give operators the freedom to implement up, to, date, energy, saving designs and facilitate large hyperscale campuses in both new and mature hubs.

By type, the market division includes hyperscale, colocation, and edge. In 2024, the colocation segment accounted for the most significant share of the market. Colocation data centers are the preferred choice of companies implementing hybrid cloud strategies and of cloud providers looking for a local presence without the need to own all the physical assets.

By end user, the market division includes IT and telecommunications, BFSI, and government. The IT and telecommunications segment was the leading contributor to the market in 2024. The segment growth was mainly driven by cloud service providers, internet companies, and carriers, who expanded their capacity to support digital services and the increase of data traffic.

Data Center Construction Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Huawei Technologies Co., Ltd.

IBM

Ascenty

Cisco Systems, Inc.

Dell Inc.

Equinix, Inc.

Fujitsu

Gensler

ABB

Acer Inc.

Get more information on this report

Data Center Construction Market Report Coverage and Deliverables:

The Data Center Construction Market Size and Forecast (2022–2033) report provides a detailed analysis of the market covering below areas:

Data center construction market size and forecast at global, regional, and country levels for all the key market segments covered under the scope.

Data center construction market trends, as well as market dynamics such as drivers, restraints, and key opportunities.

Data center construction market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments.

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Data center construction market.

Detailed company profiles, including SWOT analysis.

Data Center Construction Market Geographic Insights:

The geographical scope of the data center construction market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Data center construction market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific Data center construction market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. China and India are at the top of the list when it comes to the amount of data consumed as more and more devices and applications are connected to the internet. Consequently, solid digital, economy policies, rapid cloud adoption, and expansion by hyperscale and colocation providers are some of the reasons that are leading to the formation of large campus developments and edge facilities in major hubs like Singapore, Mumbai, Sydney, Tokyo, and Seoul. Besides that, governments are investing in fiber backbones, renewable power, and industrial parks. However, data, localization, and cybersecurity regulations in countries like India and China make a favorable environment for local build, outs. The Markets of Southeast Asia, such as Indonesia, Malaysia, Thailand, and Vietnam, have become locations of interest for operators who want.

Get more information on this report

Data Center Construction Market Research Report Guidance:

The report includes qualitative and quantitative data in the Data center construction market across infrastructure, tier, construction type, type, and end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Data center construction market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Data center construction market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Data center construction market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 12 cover Data center construction market segments by infrastructure, tier, construction type, type, and end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 13 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 14 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 15 provides detailed profiles of the major companies operating in the Data center construction market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 16, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Data Center Construction Market News and Key Development:

The Data center construction market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the data center construction market are:

In November 2025, Amazon announced plans to invest at least $3 billion in Warren County, Mississippi, to build a new data center campus to support artificial intelligence (AI) and cloud computing technologies. This investment is estimated to create at least 200 new jobs at the Amazon data center campus, plus support more than 300 additional full-time equivalent positions in the Warren County community overall.

In October 2025, Bechtel Corporation announced plans to modularize the NVIDIA Omniverse blueprint to accelerate how multi-generation, gigawatt‑scale AI infrastructure is designed and built. By turning the NVIDIA Omniverse blueprint designs into a scalable, repeatable format, new AI capacity can be delivered faster across the globe. Bechtel will showcase modularization of AI factory design at NVIDIA GTC 2025 in Washington, D.C.

Key Sources Referred:

International Energy AgencyWorld Bank – Global Trade IndicatorsWorld Trade Organization (WTO)AFCOMData Center CoalitionData Center Construction AllianceInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Data Center Construction Market

Huawei Technologies Co., Ltd.

IBM

Ascenty

Cisco Systems, Inc.

Dell Inc.

Equinix, Inc.

Fujitsu

Gensler

ABB

Acer Inc.

About Author— Electronics and Semiconductor Research Team

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the Data Center Construction Market?

The Data Center Construction Market is valued at US$ 272.4 Billion in 2025, it is projected to reach US$ 469.8 Billion by 2033.

What is the CAGR for Data Center Construction Market by (2026 - 2033)?

As per our report Data Center Construction Market, the market size is valued at US$ 272.4 Billion in 2025, projecting it to reach US$ 469.8 Billion by 2033. This translates to a CAGR of approximately 7.05% during the forecast period.

What segments are covered in this report?

The Data Center Construction Market report typically cover these key segments-

Infrastructure (IT Infrastructure, PD and Cooling Infrastructure, Miscellaneous Infrastructure)

Tier (Tier I, Tier II, Tier III, Tier IV)

Construction Type (New Construction, Renovation, Expansion)

Type (Hyperscale, Colocation, Edge)

What is the historic period, base year, and forecast period taken for Data Center Construction Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Data Center Construction Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Data Center Construction Market?

The Data Center Construction Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Huawei Technologies Co., Ltd.

IBM

Ascenty

Cisco Systems, Inc.

Dell Inc.

Equinix, Inc.

Fujitsu

Gensler

ABB

Acer Inc.

Who should buy this report?

The Data Center Construction Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Data Center Construction Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Data Center Construction Market

Get Free Sample For Data Center Construction Market