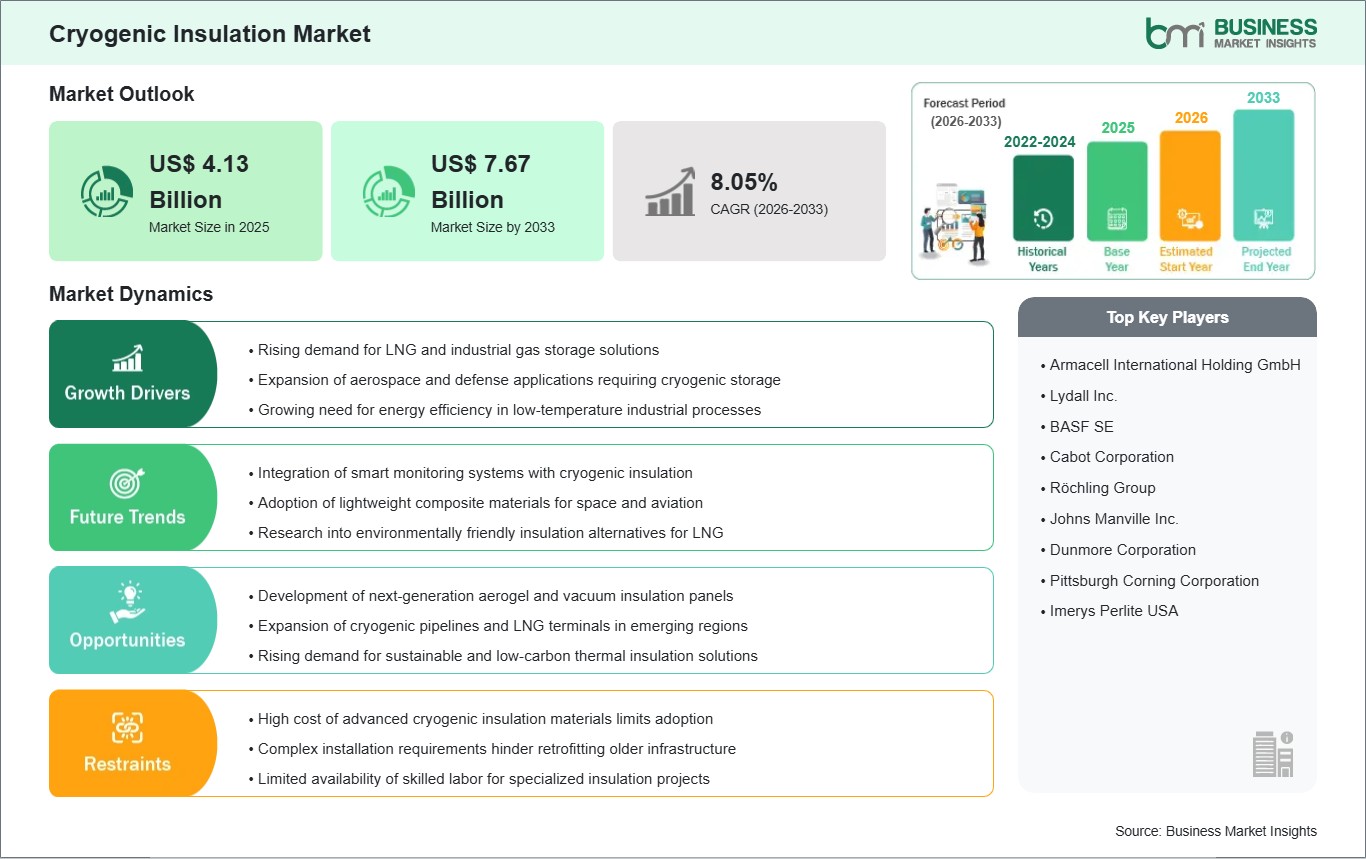

Rising demand for LNG and industrial gas storage solutions

The global cryogenic insulation market is significantly driven by the rising demand for liquefied natural gas (LNG) and industrial gas storage solutions. LNG has emerged as a key transitional fuel and strategic energy resource that meets the energy consumption needs of multiple regions. The world has established new LNG terminals, storage facilities and transportation infrastructure, which now exists throughout various regions. Cryogenic insulation systems enable LNG storage and transportation operations to maintain ultra-low temperature requirements while also reducing boiling gas emissions and gas loss during long-term storage and marine transportation.

Cryogenic insulation proves essential for industrial applications that require liquid oxygen, nitrogen, and argon as medical gases, metallurgical gases and chemical processing gases because it maintains specific temperatures and safe operations throughout various applications. Medical facilities require cryogenically stored oxygen to provide critical care, while the metal fabrication and welding industries depend on liquid nitrogen and argon for their insulation needs, which protects against both shielding and cooling requirements.

European and North American regions require better insulation performance for their ongoing upgrades to gas storage facilities and distribution networks. The increasing industrial gas consumption in the Asia Pacific, together with its fast infrastructure growth, leads to higher adoption rates of cryogenic insulation technology. The rising global demand for advanced thermal solutions demonstrates their vital role in maintaining operational systems while reducing energy losses across both the energy sector and industrial gas industry.

Development of next-generation aerogel and vacuum insulation panels

A key opportunity in the global cryogenic insulation market lies in the development of next‑generation aerogel and vacuum insulation panel (VIP) technologies. Traditional insulation materials such as polyurethane foams and perlite have served well in many applications, but increasingly complex industrial and energy storage requirements are pushing manufacturers and researchers to innovate higher‑performance alternatives. Aerogels, which offer extremely low thermal conductivity, enable improved temperature retention with thinner material thickness, making them attractive for space‑constrained installations and advanced LNG carriers.

Vacuum insulation panels complement this trend by providing excellent thermal resistance through evacuated core structures that significantly reduce convective and conductive heat transfer. These materials are finding greater acceptance in high‑end industrial and aerospace applications, where reliability, energy efficiency, and durability are paramount. For example, space agencies and private aerospace firms incorporate advanced insulation panels in cryogenic rocket fuel tanks and launch systems to preserve propellant at ultra‑low temperatures amid harsh environmental conditions.

In emerging economies, increased interest in these advanced materials reflects a broader push to modernize energy storage infrastructure and reduce overall lifecycle costs. As awareness of energy efficiency and sustainability grows, manufacturers have greater incentive to invest in research and commercialization of aerogel and VIP solutions, positioning these technologies as strategic differentiators in the global cryogenic insulation landscape.