01

Market Summery

Executive Summary and Global Market Analysis

Contrast injector is a device that is used only for the purpose of diagnostics. It assists in the visualization of internal organs by injecting the contrast medium (dye) into the patient's blood vessels during, e.g., CT, MRI, angiography, and interventional radiology. Thus, the device is also called a contrast media injector. They often vary in the level of sophistication from being simply non-power injectors to digitally dosed, fully automatic injectors that keep track of the doses, and even integrate with the imaging machines. Such features yield improvements in workflow accuracy, patient safety, and consistency in the amount of contrast delivered.

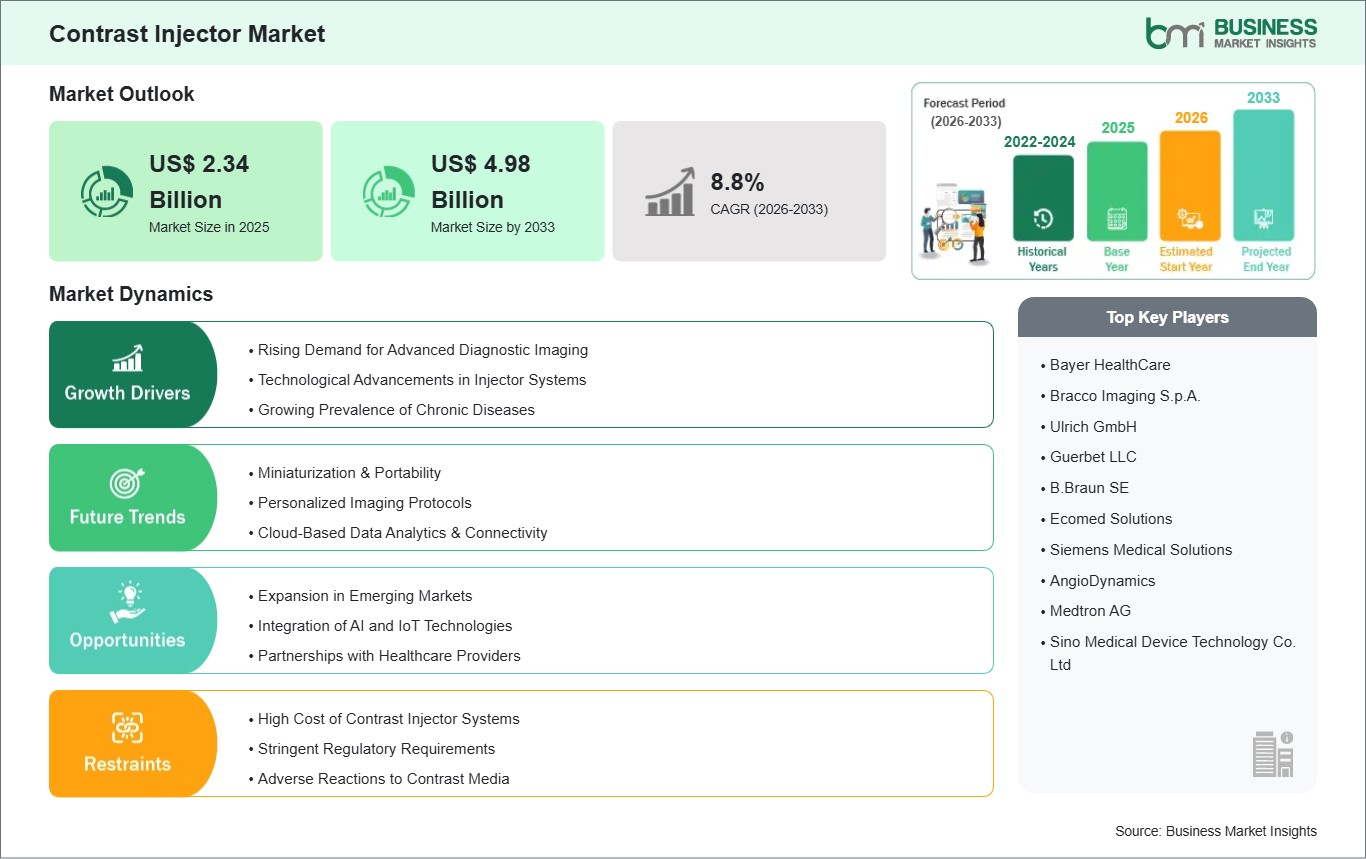

The contrast injector industry has been growing slowly yet steadily across the world. One of the reasons is the increased rate of chronic diseases such as heart disorder, cancer, and brain ailments that necessitate imaging to the highest standards for diagnosis and treatment planning. Besides this, the rising number of minimally invasive diagnostic procedures is expediting the use of contrast injectors in hospitals, diagnostic clinics, and specialty clinics throughout the world. Innovations in technology— like dual-head injectors, syringeless technology, AI-integrated injection protocols, automated contrast dosing, and real-time monitoring— are the main differences that influence product lines and also lead to better clinical results. North America and Europe continue to be the most developed markets due to their advanced healthcare systems and high imaging procedure volumes, whereas Asia-Pacific is the region expected to grow the most rapidly, owing to the investments in healthcare and the increase in access to modern imaging technology. Even though there are still issues like high costs and regulatory matters, long-term market growth is expected to be will supported through continued investments in healthcare infrastructure development, research and development alliances, and the digital imaging workflow integration.

03

Segment Analysis

Contrast Injector Market Segmentation

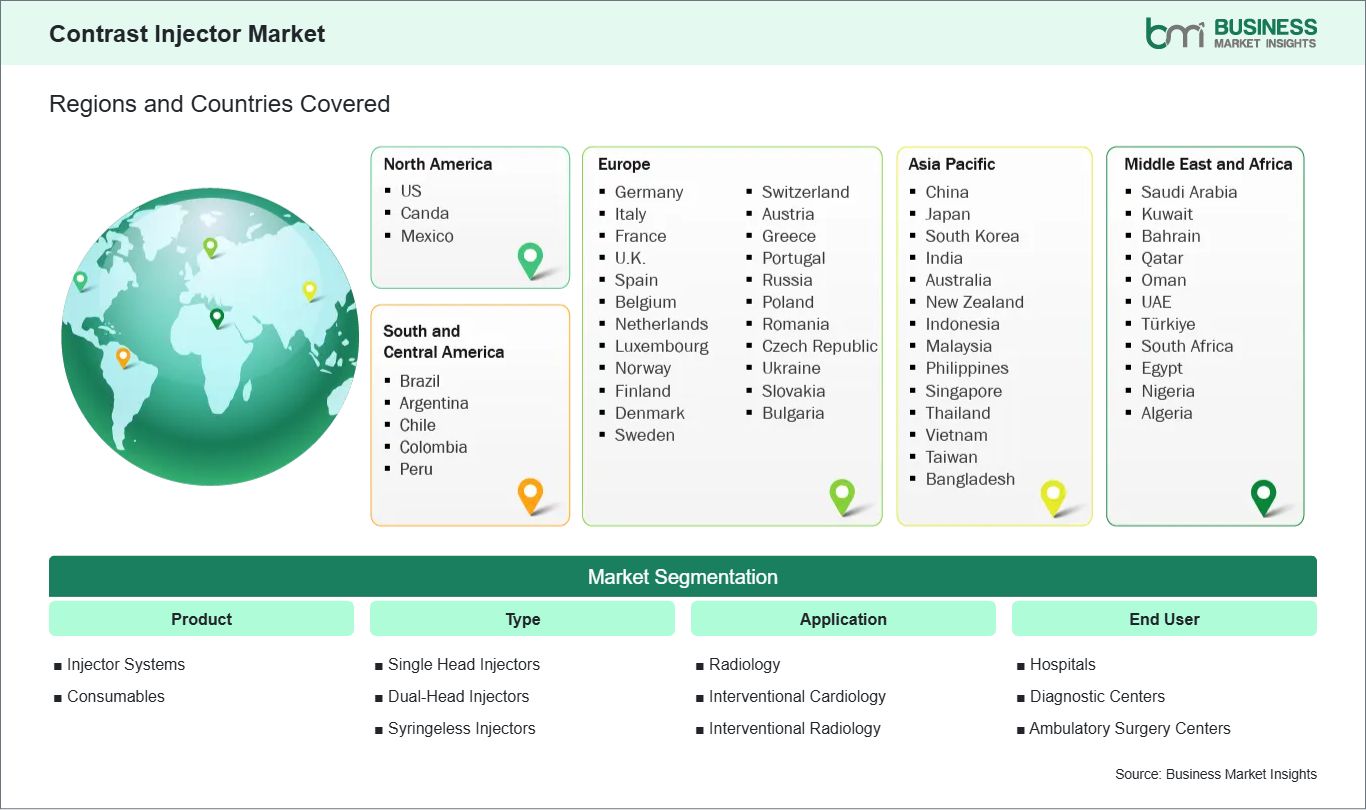

Key segments that contributed to the derivation of the contrast injector market analysis are product, type, application, and end user.

- By product, the contrast injector market is bifurcated into injector systems, consumables. The injector systems segment dominated the market in 2025.

- By type, the market is categorized into single head injectors, dual-head injectors, syringeless injectors. The single head injectors segment held the largest share of the market in 2025.

- By application, the market is segmented into radiology, interventional cardiology, interventional radiology. The radiology segment held the largest share of the market in 2025.

- By end user, the contrast injector market is segmented into hospitals, diagnostic centers, ambulatory surgery centers. The hospitals segment dominated the market in 2025.

04

Market Forces

Contrast Injector Market Drivers and Opportunities

Rising Demand for Advanced Diagnostic Imaging

One of the main factors propelling the contrast injector market is the escalating demand for sophisticated diagnostic imaging procedures, which is mainly a result of the worldwide increase in the number of chronic diseases like cancer, cardiovascular, and neurological disorders. These diseases necessitate the use of imaging techniques that are sharp and done occasionally, like CT, MRI, and angiography, to detect, monitor, and direct treatment. They also require a significant amount of contrast-enhanced imaging and injectors to be used which happens quite often. For instance, hospitals may not be very different in terms of the overall volume of imaging being done as they all are making contrast-enhanced scans a standard part of disease diagnosis and staging, with a larger percentage of CT scans now requiring the use of contrast in order to get the best possible visibility. Moreover, technological advances such as automated flow control and real-time monitoring not only increase the accuracy of the procedure but also enhance the safety thus making the modern injectors more appealing to the healthcare providers who want to improve the quality of diagnosis and efficiency of the process. The fact that both developed and developing health care facilities are continuously using high-precision imaging methods reveals the strong and continuous demand for contrast injector systems and related consumables worldwide.

Technological Advancements and Smart Injector Integration

The most prominent chance in the contrast injector market is the development of new technologies and its integration with existing ones very quickly—AI driven systems, syringeless injectors and imaging IT platforms—which are all becoming part of the changing paradigm of clinical imaging workflows. The most recent licensing of AI-enhanced injectors with real-time dosing optimization and predictive analytics has made it possible to deliver contrast more precisely and more efficiently, thus cutting down on waste and at the same time improving patient safety. In addition, the manufacture of syringeless systems, which are becoming popular in more than 40% of new installations, is a process that not only drastically reduces plastic waste but also coincides with sustainability goals and operational efficiency. Furthermore, the connection with Picture Archiving and Communication Systems (PACS) and Radiology Information Systems (RIS) is making the automatic choice of injection protocol and dose documentation possible, which brings uniformity and reduces the chances of errors by human intervention. All these developments make it possible for the healthcare sector, in particular, for big hospitals, and advanced diagnostic centers to change their value propositions by increasing imaging quality and speeding up radiology workflows making it possible for the market to grow beyond traditional injector sales to software, services, and data-driven offerings.

05

Size and Share Analysis

Contrast Injector Market Size and Share Analysis

By product, the contrast injector market is bifurcated into injector systems, consumables. The injector systems segment dominated the market in 2025. The injector systems segment leads because healthcare providers prioritize automated, precise delivery devices for CT, MRI, and angiography procedures, driving higher investment in the core hardware that improves accuracy, reduces errors, and supports advanced imaging workflows. Injector systems benefit from technological innovation and long replacement cycles, making them strategic purchases for hospitals and imaging centers.

By type, the market is categorized into single head injectors, dual-head injectors, syringeless injectors. The single head injectors segment held the largest share of the market in 2025. It holds the largest share as these systems are cost-effective, simple, and widely compatible with routine diagnostic imaging like CT and MRI. Their lower cost and ease of use make them highly preferred, especially in clinics and general radiology departments where complex multi-head capabilities are not always necessary.

By application, the market is segmented into radiology, interventional cardiology, interventional radiology. The radiology segment held the largest share of the market in 2025. It dominates because diagnostic imaging (CT scans, MRIs, angiography) constitutes the largest volume of contrast-enhanced procedures globally. Routine imaging across chronic disease diagnosis, oncology, and neurological conditions drives sustained demand for contrast injectors in radiology departments.

By end user, the contrast injector market is segmented into hospitals, diagnostic centers, ambulatory surgery centers. The hospitals segment dominated the market in 2025. Hospitals lead as end users due to their high patient throughput, comprehensive imaging departments, and the need for advanced injector systems across multiple modalities and specialties. Hospitals perform far more contrast-enhanced studies than outpatient centers, contributing to greater procurement and recurring consumable use.

07

Report Coverage

Contrast Injector Market Report Coverage and Deliverables

The " Contrast Injector Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Contrast injector market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Contrast injector market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Contrast injector market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the contrast injector market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Contrast Injector Market Geographic Insights

The geographical scope of the contrast injector market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The contrast injector market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific contrast injector market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The Asia-Pacific contrast injector market is experiencing robust growth, due to the expanding healthcare infrastructure and investment in diagnostic imaging. Countries such as China, India, Japan, and South Korea have made it a point to provide their hospitals and imaging centers with the latest in medical technology that requires advanced contrast injectors and thereby are upgrading their facilities with modern CT and MRI systems. Healthcare development in China and government support for better healthcare facilities have turned China into the biggest market in the region, whereas Japan has the high technology adoption in the hospitals thus increasing the adoption of such procedures.

Besides, the high number of chronic diseases like cancer, heart, and vascular diseases along with the large and aging population in the Asia-Pacific region has resulted in increase in imaging exams which subsequently focuses on the adoption of new technologies by the providers in order to make the process safer and more efficient. Moreover, the heightened awareness of early diagnosis and preventive healthcare, together with the increased accessibility of imaging in lower-tier cities and the growth of medical tourism in countries like Thailand and Singapore, is creating a demand for contrast injectors beyond the metropolitan areas, thus speeding up the growth of the Asia-Pacific market.

10

Industry Activity

Recent Developments

The contrast injector market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the contrast injector market are:

- In November 2025, Bracco Diagnostics Inc., the U.S. confederate of Bracco Imaging S.p.A., a medical imaging company, declared that the U.S. FDA had magnified the purpose of Bracco's branded Max 3 Rapid Exchange and Syringeless Injector in magnetic resonance imaging (MRI) procedures. The new indication widens the range of the Max 3 system for single-dose and multi-dose vials, and the recently authorized VUEWAY (gadopiclenol) Injection Imaging Bulk Package (IBP) in both 30 mL and 50 mL sizes, thus facilitating the MRI contrast administration with more freedom and processing.

- In April 2025, Bayer and Siemens Healthineers launched the MEDRAD Centargo project, which is a totally automated contrast injector system geared towards decreasing the time between scanning and minimizing manual work to technologists. This technological development enables the healthcare staff to accord more attention to the patients, thus, facilitating efficiency and improving overall workflow in diagnostic imaging procedures.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Health Organization (WHO)Centers for Disease Control and Prevention (CDC)OECD Health Statistics & HealthInstitute for Health Metrics and EvaluationDHIS2 Health Management DataCompany websitesCompany annual reportsCompany investor presentations