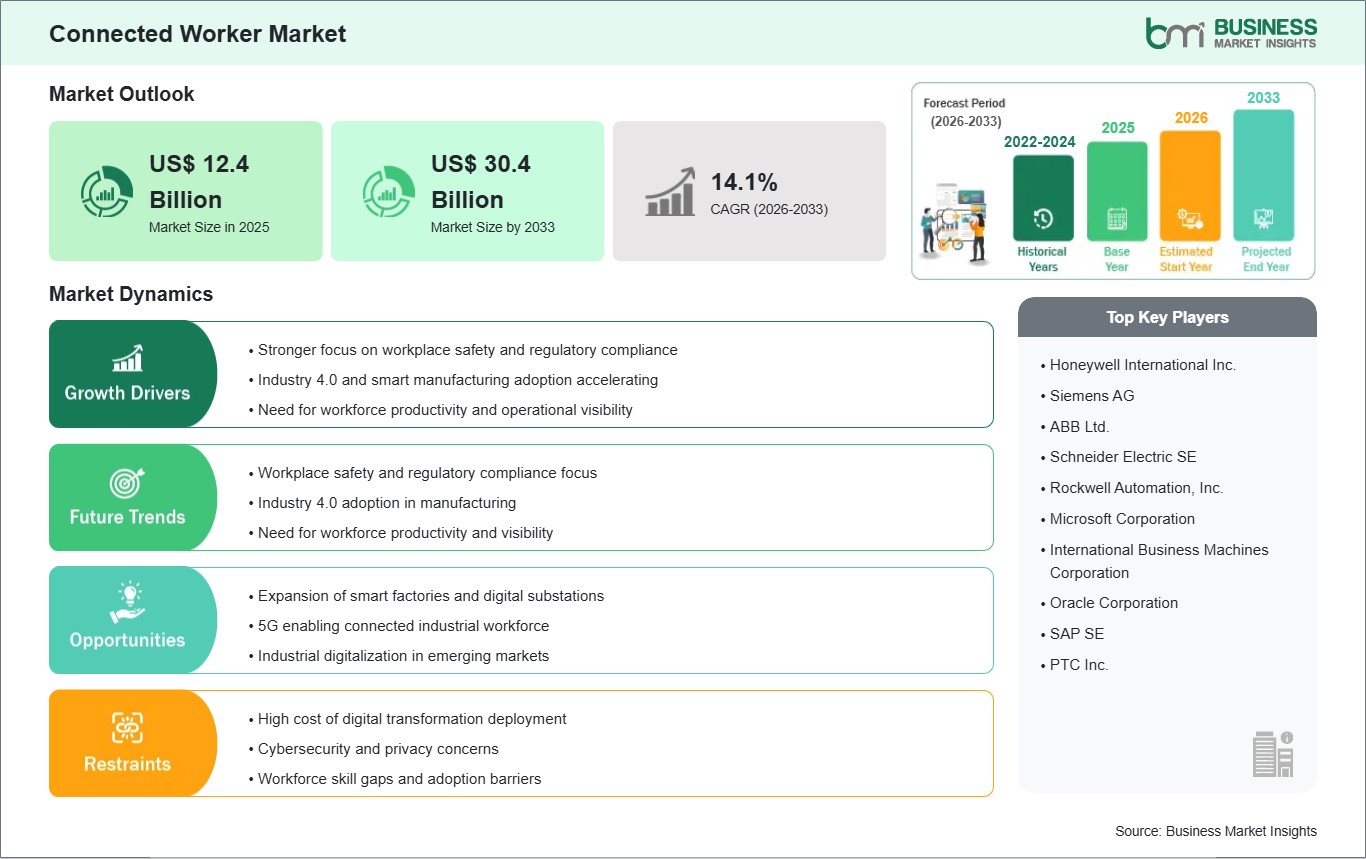

The Connected Worker Market size is expected to reach US$ 30.4 Billion by 2033 from US$ 12.4 Billion in 2025. The market is estimated to record a CAGR of 11.86% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The Connected Worker market represents a critical pillar of digital transformation initiatives across industrial sectors. Connected Worker solutions leverage wearable devices, mobile applications, IoT sensors, augmented reality (AR), artificial intelligence (AI), and cloud-based platforms to enhance workforce productivity, operational visibility, compliance, and safety in frontline environments. These solutions enable real-time communication, remote collaboration, predictive maintenance support, digital workflows, and data-driven decision-making across complex industrial ecosystems. As organizations accelerate Industry 4.0 adoption, Connected Worker technologies are becoming integral to bridging the gap between frontline operations and enterprise systems.

The market is witnessing accelerated adoption due to increasing focus on operational efficiency, workplace safety regulations, labor shortages, and the need to optimize field service operations. The integration of AI-driven analytics, edge computing, and cloud connectivity is further enhancing scalability, system intelligence, and interoperability with ERP and MES systems. Despite strong growth prospects, market expansion faces challenges such as high implementation costs, integration complexities with legacy systems, cybersecurity risks, and workforce resistance to digital transformation. However, continued investment in industrial IoT, 5G connectivity, and enterprise mobility solutions is expected to unlock substantial long-term growth opportunities.

Connected Worker Market - Strategic Insights:

Get more information on this report

Connected Worker Market Segmentation Analysis:

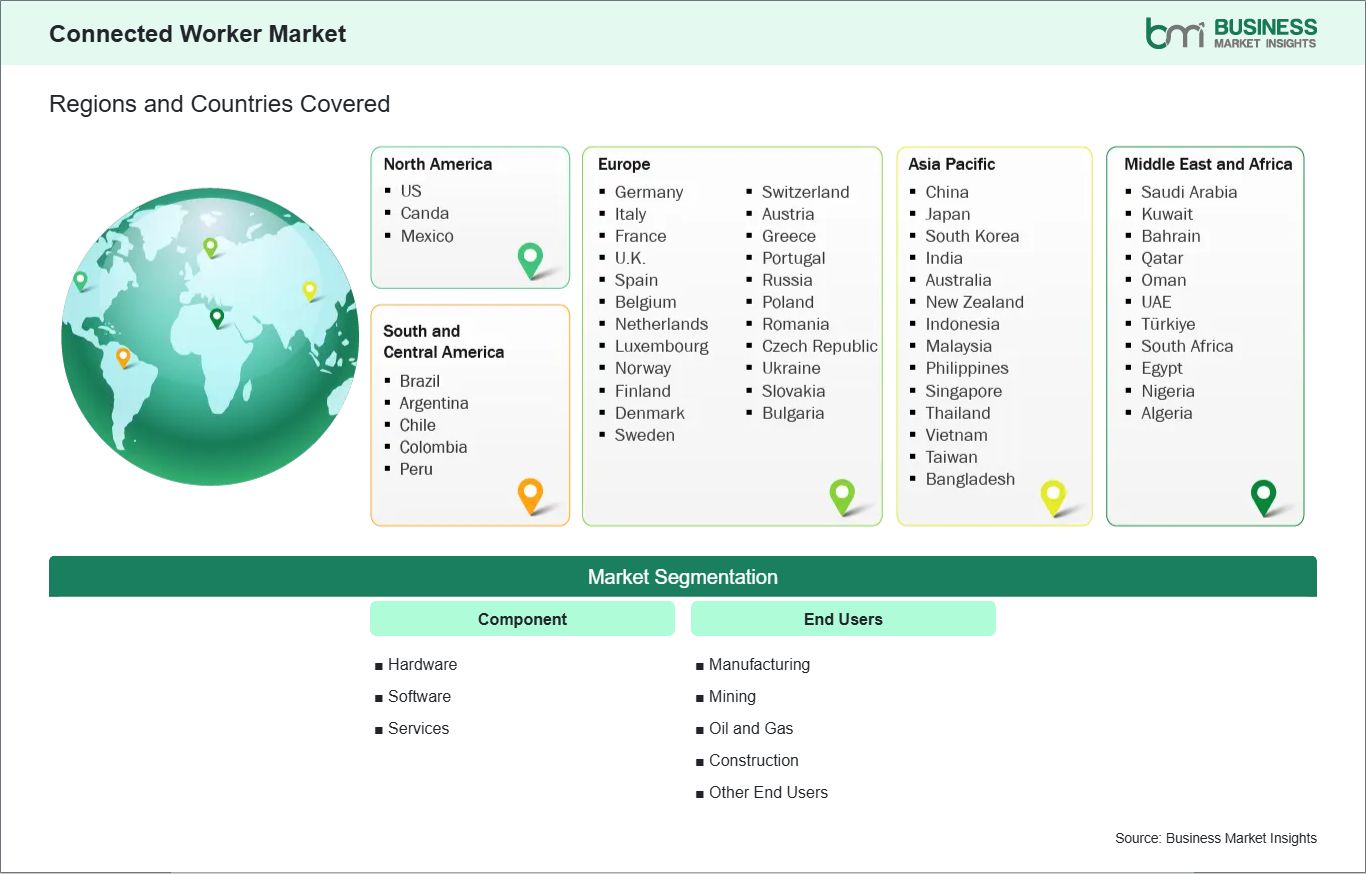

Key segments that contributed to the Connected Worker market analysis are component and end user.

By component, the market is divided into hardware, software, and services. The Hardware segment held the largest market share in 2025.

By end user, the market is divided into Manufacturing, Mining, Oil and Gas, Construction, and Other. The Manufacturing segment held the larger share in 2025.

Connected Worker Market Drivers and Opportunities:

Rising Emphasis on Workplace Safety and Regulatory Compliance

Stringent occupational safety regulations across industrial sectors are driving investments in Connected Worker solutions. Real-time monitoring of worker health metrics, geolocation tracking in hazardous environments, automated incident reporting, and compliance documentation reduce workplace risks and improve adherence to regulatory standards. Industries such as oil & gas, mining, and construction are particularly adopting wearable safety devices and remote monitoring tools to minimize accidents and operational downtime. As regulatory frameworks evolve, digital safety management solutions are becoming essential for risk mitigation and liability reduction.

Additionally, digital incident reporting and compliance documentation streamline audit readiness and regulatory reporting. Connected Worker platforms provide centralized dashboards that record safety inspections, training certifications, and incident histories, thereby reducing administrative burden and improving transparency. Over time, advanced analytics and AI-driven risk modeling enable predictive safety management—identifying patterns and leading indicators that help prevent accidents before they occur.

Acceleration of Industry 4.0 and Smart Manufacturing Initiatives

The global push toward smart manufacturing and industrial automation is significantly accelerating the adoption of Connected Worker platforms. Integration with IoT sensors, machine data, and enterprise systems enables predictive maintenance, digital workflows, and real-time collaboration between field technicians and remote experts. Organizations are leveraging AR-based assistance, AI-powered analytics, and cloud platforms to improve first-time fix rates, reduce downtime, and optimize asset utilization. The convergence of 5G connectivity, edge computing, and industrial IoT ecosystems is expected to create new opportunities for scalable Connected Worker deployments across geographically dispersed facilities.

Furthermore, AI-powered analytics embedded within Connected Worker platforms provide actionable insights into workforce productivity, task completion rates, and asset utilization. Organizations can optimize shift planning, resource allocation, and workflow efficiency using data-driven performance benchmarks. Over time, these insights support continuous improvement initiatives and lean manufacturing strategies.

Connected Worker Market Size and Share Analysis:

By component, the market is divided into hardware, software, and services. The Hardware segment held the largest market share in 2025 due to increased deployment of wearable devices, AR headsets, rugged mobile devices, and smart PPE across industrial facilities.

By end user, the market is divided into Manufacturing, Mining, Oil and Gas, Construction, and Other. The Manufacturing segment held the larger share in 2025, supported by smart factory initiatives and digital workforce enablement programs. Meanwhile, the Oil & Gas and Mining sectors are expected to demonstrate strong growth due to hazardous operational environments and increasing investments in safety-focused digital technologies.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Honeywell International Inc.

Siemens AG

ABB Ltd.

Schneider Electric SE

Rockwell Automation, Inc.

Microsoft Corporation

International Business Machines Corporation

Oracle Corporation

SAP SE

PTC Inc.

Get more information on this report

Connected Worker Market Report Coverage and Deliverables:

The "Connected Worker Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Connected Worker market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Connected Worker market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Connected Worker market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Connected Worker market

Detailed company profiles, including SWOT analysis

Connected Worker Market Geographic Insights:

The Connected Worker market is geographically segmented into North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America, reflecting varied levels of industrial digitization, regulatory maturity, infrastructure readiness, and technology adoption across regions.

Asia Pacific is expected to witness the fastest growth and maintain a dominant position during the forecast period. This growth is driven by rapid industrialization, expanding manufacturing hubs, and increasing investments in Industry 4.0 initiatives across countries such as China, India, Japan, and South Korea. Governments in the region are actively promoting smart factory development, digital workforce enablement, and advanced manufacturing under national transformation programs. The strong presence of electronics, automotive, and heavy industries, combined with rising adoption of IoT, AI, and 5G technologies, is accelerating deployment of Connected Worker platforms to enhance productivity, safety, and operational visibility.

North America and Europe represent mature markets characterized by high adoption of industrial automation, established regulatory frameworks, and early implementation of digital transformation strategies. In these regions, demand is primarily driven by stringent workplace safety regulations, strong emphasis on ESG compliance, and widespread integration of enterprise mobility solutions. Industries such as oil & gas, aerospace, utilities, and advanced manufacturing are leveraging Connected Worker technologies to optimize asset performance, ensure compliance, and improve frontline collaboration.

Middle East & Africa and South & Central America are emerging markets experiencing steady growth, supported by infrastructure modernization, expansion of energy and mining sectors, and increasing investments in industrial digitalization. Governments and private enterprises in these regions are adopting Connected Worker solutions to improve worker safety, streamline field operations, and enhance efficiency in large-scale industrial and construction projects. Growing awareness of digital workforce management and rising adoption of mobile connectivity further contribute to market expansion across these developing regions.

Get more information on this report

Connected Worker Market Research Report Guidance:

The report includes qualitative and quantitative data in the Connected Worker market across component, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Connected Worker market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Connected Worker market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Connected Worker market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover Connected Worker market segments by cable type, testing type, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Connected Worker market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer

Connected Worker Market News and Key Development:

The Connected Worker market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Connected Worker market are:

In October 2025, CDS Visual, part of Dover (NYSE: DOV) and a leading provider of visual-based digital software solutions for manufacturers, announced the launch of CDS Mentor™ 3.0, a new version of its connected workforce platform that aims to unify the shop floor lifecycle through digital work instruction authoring, execution, quality, skills management and real-time insights.

In September 2024, Rockwell Automation, Inc. (NYSE: ROK), the world’s largest company dedicated to industrial automation and digital transformation, announced the launch of its connected worker solution from Plex, by Rockwell Automation. These industry-leading capabilities were developed to help users enhance productivity, quality, and safety on the shop floor.

Key Sources Referred:

International Data Corporation (IDC)Consumer Technology Association (CTA)National Institute of Standards and Technology (NIST)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Connected Worker Market

Honeywell International Inc.

Siemens AG

ABB Ltd.

Schneider Electric SE

Rockwell Automation, Inc.

Microsoft Corporation

IBM Corporation

Oracle Corporation

SAP SE

PTC Inc.

Frequently Asked Questions

How big is the Connected Worker Market?

The Connected Worker Market is valued at US$ 12.4 Billion in 2025, it is projected to reach US$ 30.4 Billion by 2033.

What is the CAGR for Connected Worker Market by (2026 - 2033)?

As per our report Connected Worker Market, the market size is valued at US$ 12.4 Billion in 2025, projecting it to reach US$ 30.4 Billion by 2033. This translates to a CAGR of approximately 11.86% during the forecast period.

What segments are covered in this report?

The Connected Worker Market report typically cover these key segments-

Component (Hardware, Software, Services)

End Users (Manufacturing, Mining, Oil and Gas, Construction, Other End Users)

What is the historic period, base year, and forecast period taken for Connected Worker Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Connected Worker Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Connected Worker Market?

The Connected Worker Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Honeywell International Inc.

Siemens AG

ABB Ltd.

Schneider Electric SE

Rockwell Automation, Inc.

Microsoft Corporation

International Business Machines Corporation

Oracle Corporation

SAP SE

PTC Inc.

Who should buy this report?

The Connected Worker Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Connected Worker Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Connected Worker Market

Get Free Sample For Connected Worker Market