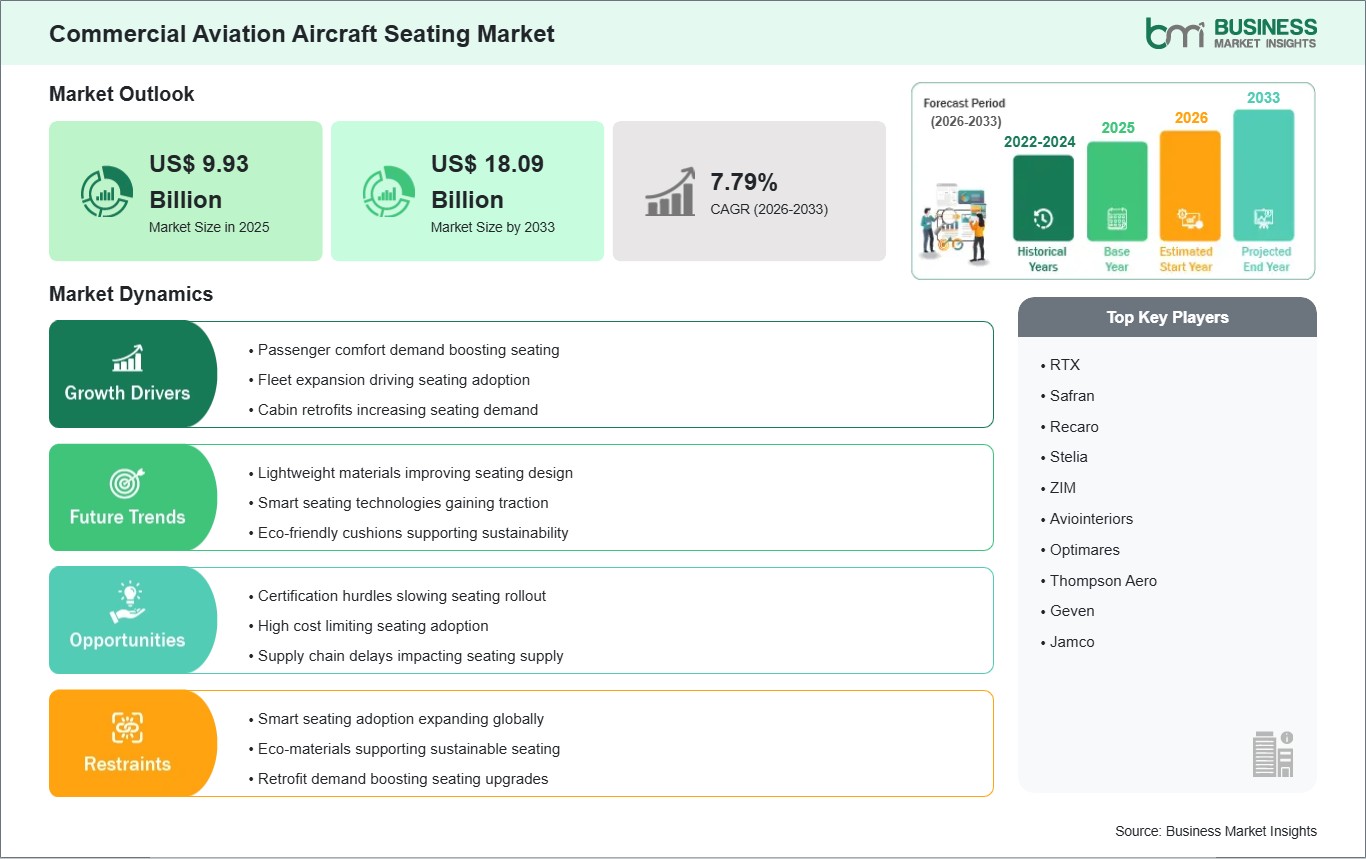

The Commercial Aviation Aircraft Seating Market size is expected to reach US$ 18.09 Billion by 2033 from US$ 9.93 Billion in 2025.The market is estimated to record a CAGR of 7.79% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Commercial aviation aircraft seating refers to the subset of aircraft manufacturers' efforts dedicated to developing and incorporating seats for passengers, pilots, and crew members. Such seats have to offer high levels of ergonomics, lightness, and compliance with all regulatory requirements. This allows for improving the quality of passengers' experience while ensuring better performance from an operational and energy standpoint.

The growth in the sector can be explained by the growing air traffic, as well as the increasing demand for more comfortable traveling conditions. Modern cabin renovation projects are increasingly concerned with ergonomic design and lightweight materials. In addition, the increased competition among airlines leads to higher interest in improving their seating configurations to attract customers and enhance their experience.

The segmentation patterns in terms of volume vary depending on whether we are talking about passenger, pilot, or crew seating. Passenger seats account for a major proportion of this market since there is a large number of commercial flights performed globally. Economy class dominates the market in terms of size, but premium, business, and first-class seating continue to grow.

Technological development within aircraft seating revolves around issues such as minimizing seat weight, implementing a modular design approach, and incorporating features that enhance comfort. Technologies such as advanced foams, electrical mechanisms for seat adjustments, and even actuator systems have helped to enhance the comfort levels and efficiencies associated with seats on aircraft.

Competitive forces will be characterized by innovations in lightweight materials used in seats and ergonomic designs that maximize passenger comfort while at the same time ensuring that the seating complies with aviation safety regulations. Customized seat solutions that incorporate the branding efforts of airlines will emerge as a major trend in this competitive industry.

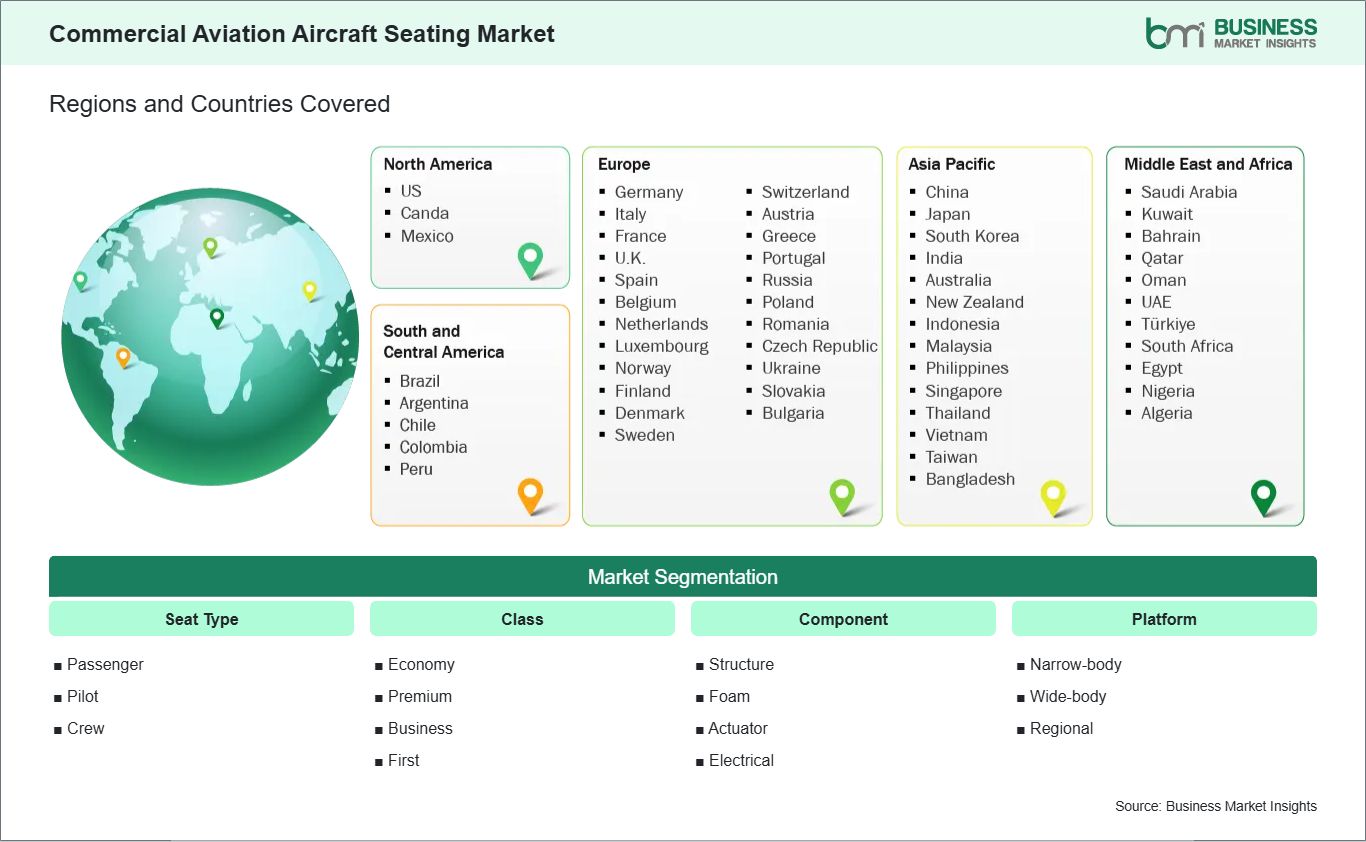

The commercial aviation aircraft seating market is segmented based on seat type, class, component, and platform, reflecting the aviation industry’s focus on cabin optimization, passenger comfort enhancement, and aircraft efficiency across different fleet categories and travel experiences.

By Seat Type

Passenger: High-density seating configurations support commercial airline operations and passenger volume efficiency.

Pilot: Ergonomically designed seats ensure safety, control accessibility, and operational precision.

Crew: Functional seating supports in-flight service efficiency and operational mobility.

By Class

Economy: Standardized seating maximizes capacity and cost efficiency across routes.

Premium: Enhanced comfort features improve passenger experience on mid-tier travel segments.

Business: Spacious configurations support productivity and elevated service standards.

First: Luxury-focused seating integrates advanced comfort and privacy features.

By Component

Structure: Lightweight frameworks improve fuel efficiency and aircraft performance.

Actuator: Adjustable systems enable personalized seating configurations.

Electrical: Integrated controls support smart seat functionality and passenger convenience.

By Platform

Narrow-body: Efficient seating layouts support short to medium-haul operational demand.

Wide-body: High-capacity configurations enable long-haul international travel comfort.

Regional: Compact seating designs optimize space in short-distance aircraft operations.

Commercial Aviation Aircraft Seating Market Drivers and Opportunities:

Passenger comfort demand boosting seating

The expectation by passengers concerning their comfort during flights is fast becoming one of the key factors that are motivating airlines to develop new aircraft seats that will meet these expectations. There is more concern about increasing comfort levels through better design of seats, legroom, comfort, and convenience, among other considerations. Airlines are beginning to recognize that travelers are making decisions about which airline to use depending not just on the cost and schedule but also on the comfort levels available on their airplanes. This has led to greater attention to developing better seats that facilitate comfort without compromising on efficiency.

Increased emphasis on the well-being of the traveler is leading to greater demand for lightweight and technologically advanced seating solutions. There is increased focus from the regulatory body and airlines on meeting certain seating standards that enhance the safety, health, and comfort of passengers. Innovations such as modular seat designs, enhanced seating functionality, and the use of foam technology have all come into play in responding to changes in traveler demands. In particular, premium and business class travel trends are playing a role in promoting innovations in seating functionality.

Smart seating adoption expanding globally

The implementation of smart seating technology is opening up new possibilities in terms of the commercial aviation aircraft seating market. Air carriers are actively investigating connected seating technologies that include automated adjustment features, passenger monitoring tools, entertainment control options, and personalized seating preferences. Besides enhancing the cabin experience and passenger services, smart seating helps air operators manage their operations through increased data accessibility. The introduction of smart seating technology fits well into the general transformation trend towards the creation of connected aircraft and digital-based passenger services offered by the aviation industry. As fleets become more technologically advanced, smart cabin infrastructure will become a standard requirement in future purchases.

In addition, smart seating is expected to positively affect innovation in terms of the interior design of narrow-body and wide-body aircraft in the future. The development of seating technology with sensor-based components that facilitate predictive maintenance, energy-saving measures, and lifecycle improvements is on the rise. Further incorporation of wireless connections and cabin management system software solutions adds additional incentives to implement these systems on board planes. The aviation sector in emerging markets understands the importance of using advanced digital technology in the seats to improve passenger experience.

Commercial Aviation Aircraft Seating Market Size and Share Analysis:

The Commercial Aviation Aircraft Seating Market is projected to grow from US$ 9.93 Billion in 2025 to US$ 18.09 Billion by 2033 , registering a CAGR of 7.79% from 2026 to 2033.

By seat type, passenger seats maintain the leading position because commercial aircraft are designed with a substantially higher number of passenger seats compared to pilot and crew seating. Rising global air travel, increasing aircraft deliveries, and airline investments in passenger comfort, lightweight seating, and cabin modernization continue to drive strong demand for passenger seating systems.

By class, economy dominates due to its large seating capacity and widespread adoption across full-service and low-cost airlines. Airlines prioritize maximizing passenger volume and operational profitability, leading to higher installation and replacement rates for economy seats, particularly in narrow-body aircraft operating high-frequency domestic and regional routes.

By component, structure leads the market as it forms the core framework of aircraft seats, contributing significantly to overall seat weight, durability, and manufacturing cost. Growing emphasis on lightweight materials to improve fuel efficiency and comply with aviation standards continues to increase demand for advanced seat structure components.

By platform, narrow-body holds a significant share due to their large operational fleet and extensive use in short- and medium-haul commercial routes worldwide. High production volumes from major aircraft manufacturers, increasing regional connectivity, and rising passenger traffic significantly boost seating demand and replacement activities within this aircraft category.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

RTX

Safran

Recaro

Stelia

ZIM

Aviointeriors

Optimares

Thompson Aero

Geven

Jamco

Get more information on this report

Commercial Aviation Aircraft Seating Market Report Coverage and Deliverables:

The "Commercial Aviation Aircraft Seating Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

The market size and forecast at global, regional, and country levels for all market segments covered under the scope

The market trends, as well as drivers, restraints, and opportunities

The market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

There is a wide variety of adoption trends for the commercial aviation aircraft seating market based on fleet development, passenger experience requirements, and new investments made in aircraft renovation. Demand differs regionally according to the volume of air traffic, airline competition, and infrastructure developed for the use of commercial aircraft in various regions around the world. This market demonstrates a shift towards lighter and more innovative cabin interior components, including improved aircraft seats.

The North American market plays a key role in this industry owing to high levels of commercial aviation and ongoing cabin renewal programs within the sector. The United States is the dominant country within the region, with large airlines purchasing advanced seating systems for their aircraft. Additionally, Canada is making a contribution to ongoing market growth through investment in aircraft renovation programs.

The Asia-Pacific is an area of fast growth driven by increases in air traffic and huge aircraft procurement plans. The growth in Asia-Pacific is mainly due to China and India, which have growing airlines and airports, while Japan is developing its cabin interiors to provide high levels of comfort. The growth in narrow-body aircraft seats in the region is also influenced by low-cost carriers in Southeast Asia.

Europe shows strong adoption thanks to the robust manufacturing capabilities of aerospace companies and highly developed airline services. Countries such as Germany, France, and the UK concentrate on the development of lightweight aircraft seats and cabin interiors to optimize fuel consumption. Emerging regions such as the Middle East and Latin America will be gradually gaining momentum as airlines in the United Arab Emirates, Saudi Arabia, and Brazil grow and purchase new aircraft.

Get more information on this report

Commercial Aviation Aircraft Seating Market Research Report Guidance:

The report includes qualitative and quantitative data for the Commercial Aviation Aircraft Seating Market across seat type, class, component, platform, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Commercial Aviation Aircraft Seating Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Commercial Aviation Aircraft Seating Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Commercial Aviation Aircraft Seating Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover Commercial Aviation Aircraft Seating Market segments by seat type, class, component, platform, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Commercial Aviation Aircraft Seating Market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Commercial Aviation Aircraft Seating Market News and Key Development:

The commercial aviation aircraft seating market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the commercial aviation aircraft seating market are:

In August 2024, RECARO Aircraft Seating announced that IndiGo had selected its R5 seats for the business-class cabins of A321neo aircraft, marking the airline’s first introduction of business-class seating and covering 45 aircraft shipsets.

In May 2024, RTX (Collins Aerospace) announced the launch of its Helix next-generation main cabin seat for narrowbody aircraft at the 2024 Aircraft Interiors Expo, focusing on lightweight design, improved passenger comfort, and lower fuel consumption for commercial airlines.

Key Sources Referred:

Federal Aviation Administration (FAA)European Union Aviation Safety Agency (EASA)International Civil Aviation Organization (ICAO)International Air Transport Association (IATA)Civil Aviation Administration of China (CAAC)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Commercial Aviation Aircraft Seating Market

Dhananjay is a market research and consulting professional with over 5 years of experience in syndicated reports, consulting assignments, and custom research projects. He holds a Bachelor's degree in Pharmacy and an MBA in Marketing, combining technical domain knowledge with strong business acumen and analytical rigor.

Currently supporting end-to-end research engagements and delivering actionable, data-driven insights across multiple industries, Dhananjay is skilled in market forecasting, market sizing, competitive benchmarking, and trend analysis, with a strong focus on delivering high-quality, decision-ready insights for strategic..

Show More

Frequently Asked Questions

How big is the Commercial Aviation Aircraft Seating Market?

The Commercial Aviation Aircraft Seating Market is valued at US$ 9.93 Billion in 2025, it is projected to reach US$ 18.09 Billion by 2033.

What is the CAGR for Commercial Aviation Aircraft Seating Market by (2026 - 2033)?

As per our report Commercial Aviation Aircraft Seating Market, the market size is valued at US$ 9.93 Billion in 2025, projecting it to reach US$ 18.09 Billion by 2033. This translates to a CAGR of approximately 7.79% during the forecast period.

What segments are covered in this report?

The Commercial Aviation Aircraft Seating Market report typically cover these key segments-

Seat Type (Passenger, Pilot, Crew)

Class (Economy, Premium, Business, First)

Component (Structure, Foam, Actuator, Electrical)

Platform (Narrow-body, Wide-body, Regional)

What is the historic period, base year, and forecast period taken for Commercial Aviation Aircraft Seating Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Commercial Aviation Aircraft Seating Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Commercial Aviation Aircraft Seating Market?

The Commercial Aviation Aircraft Seating Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

RTX

Safran

Recaro

Stelia

ZIM

Aviointeriors

Optimares

Thompson Aero

Geven

Jamco

Who should buy this report?

The Commercial Aviation Aircraft Seating Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Commercial Aviation Aircraft Seating Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Commercial Aviation Aircraft Seating Market

Get Free Sample For Commercial Aviation Aircraft Seating Market