01

Market Summery

Executive Summary and Global Market Analysis

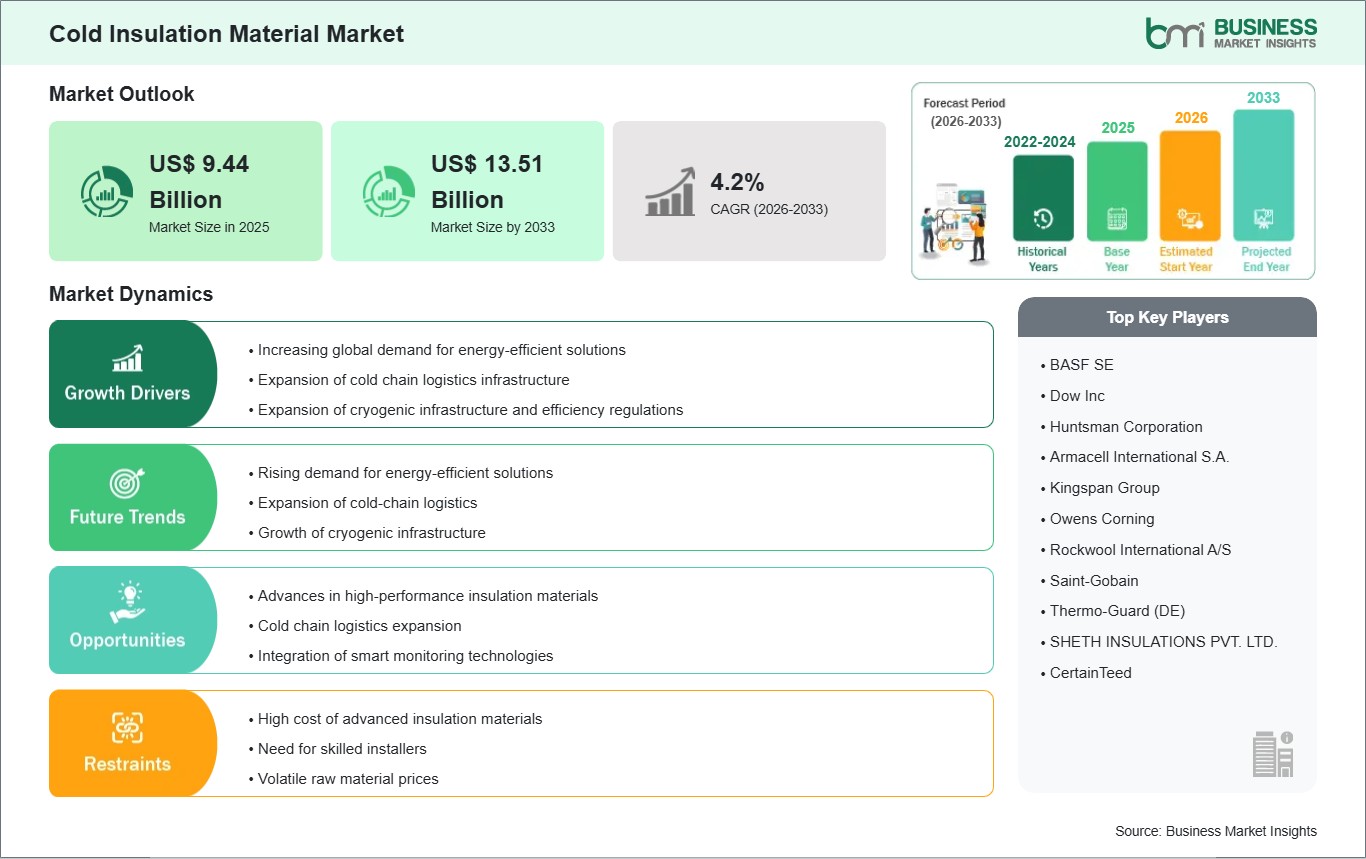

Cold insulation materials are designed to reduce heat transfer and keep temperatures stable in systems that work in low or sub-zero conditions. Common materials include polyurethane foam, polystyrene, elastomeric foam, fiberglass, and perlite. These materials are often used in refrigeration equipment, cold storage warehouses, LNG facilities, and cryogenic applications. Their low thermal conductivity, resistance to moisture, and strong structure are vital for maintaining product quality and boosting efficiency in both industrial and commercial settings.

Market growth relies on the fast expansion of cold chain logistics for food and beverages. There is also a rising demand for temperature-controlled storage of pharmaceuticals and growing investments in LNG production, storage, and transportation. Stricter energy efficiency rules and sustainability goals in various regions are encouraging the use of better insulation solutions that lower energy use and operational losses.

However, the market witnesses challenges, such as fluctuating raw material prices, especially for insulation products made from petrochemicals, and higher initial installation costs compared to traditional options. Despite these challenges, ongoing infrastructure development, growth in logistics that depend on temperature control, and a greater focus on energy savings are expected to drive demand for cold insulation materials steady in the coming years.

03

Segment Analysis

Cold Insulation Material Market Segmentation

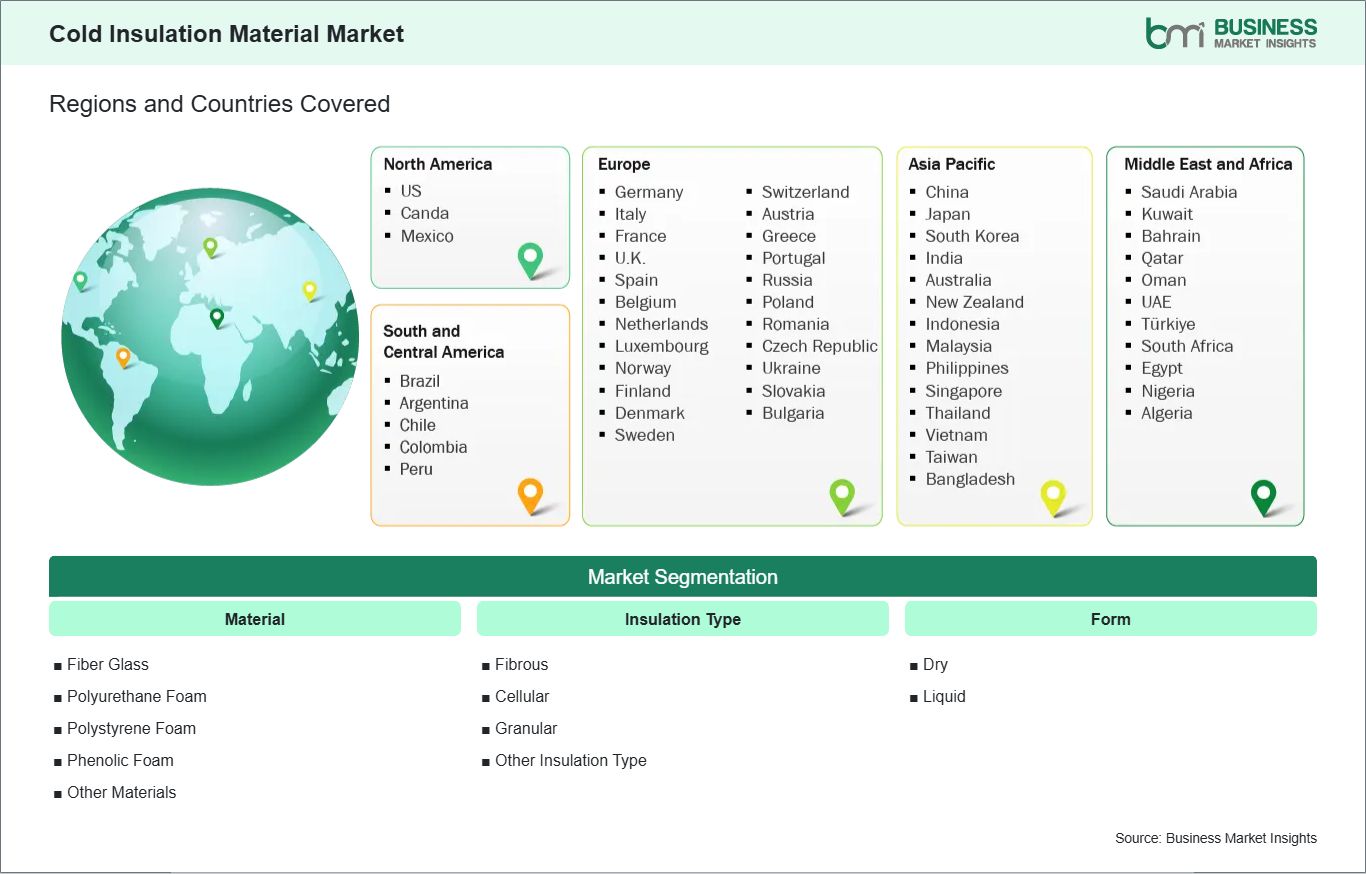

Key segments that contributed to the derivation of the cold insulation material market analysis are material, insulation type, and application.

- By material, the cold insulation material market is segmented into fiberglass, polyurethane foam, polystyrene foam, phenolic foam, and others. Among these, polyurethane foam accounted for the largest market share in 2025.

- By insulation type, the market is classified into fibrous, cellular, granular, and others. The cellular insulation segment dominated the market in 2025.

- By application, the cold insulation material market is segmented into HVAC, chemicals, oil & gas, refrigeration, and others. The refrigeration segment held the largest share in 2025.

04

Market Forces

Cold Insulation Material Market Drivers and Opportunities

Expansion of Cold Chain and LNG Infrastructure

The increased consumption of perishable food, frozen items, and temperature-sensitive medicines has raised the need for reliable cold storage, refrigerated transportation, and distribution centers. Cold insulation materials are vital for keeping stable temperatures, reducing heat loss, and meeting food safety and pharmaceutical quality requirements.

At the same time, growing investments in LNG production, storage terminals, cryogenic tanks, pipelines, and transportation vessels are boosting demand for high-performance insulation that works well at very low temperatures. LNG infrastructure needs materials with low thermal conductivity, high strength, and long-term durability to prevent energy loss and ensure safety. Additionally, government policies that promote cleaner energy sources are encouraging the use of LNG as a transitional fuel, which indirectly supports the need for insulation. The expansion of cold chain logistics and LNG infrastructure is creating steady, large-scale demand for cold insulation materials in industrial, commercial, and energy-related fields.

Development of Sustainable Insulation Materials

The increased focus on energy efficiency and reducing carbon emissions is driving interest in insulation materials that provide better thermal performance while lowering their environmental impact throughout their life cycle. Manufacturers are investing more in materials with lower global warming potential, better recyclability, and fewer emissions during production and installation.

Improvements in material science are leading to insulation products that offer better moisture resistance, longer service life, and greater mechanical stability. These advancements make them suitable for challenging applications like cryogenic storage and industrial refrigeration. Growing awareness of the total cost of ownership is also promoting the use of higher-performance insulation systems that provide long-term energy savings and lower maintenance needs. As industries emphasize sustainability, compliance with regulations, and operational efficiency, the demand for next-generation cold insulation materials is expected to rise, supporting ongoing market growth.

05

Size and Share Analysis

Cold Insulation Material Market Size and Share Analysis

The cold insulation material market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report examines subsegments categorized within material, insulation type, and application, offering insights into their contribution to overall market performance. By material, polyurethane foam holds the largest market share. Its dominance is due to low thermal conductivity, high moisture resistance, and flexibility in low-temperature environments. Polyurethane foam is used extensively in refrigeration systems, cold storage facilities, and industrial process insulation, where steady thermal performance and durability are crucial considerations. Growth in this segment is driven by the expansion of cold chain infrastructure, rising demand for energy-efficient insulation solutions, and increased industrial activity in developed and emerging economies.

07

Report Coverage

Cold Insulation Material Market Report Coverage and Deliverables

The " Cold Insulation Material Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- Cold Insulation material market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Cold Insulation material market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Cold Insulation material market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the cold insulation material market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Cold Insulation Material Market Geographic Insights

The geographical scope of the cold insulation material market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America. Europe holds a significant market share in the cold insulation material market because of its strong industrial base, solid cold chain infrastructure, and focus on energy efficiency. The region has many refrigerated food processing facilities, pharmaceutical manufacturing plants, and cold storage warehouses. These facilities need effective insulation to control temperatures and meet strict quality standards. Europe's extensive LNG import and storage infrastructure, especially in Germany, France, the Netherlands, and Spain, increases the demand for high-performance cold insulation materials in cryogenic tanks and pipelines.

Moreover, strict building energy rules and sustainability initiatives in the European Union encourage the use of better insulation solutions to cut energy use and greenhouse gas emissions. Significant investments in modern HVAC systems and industrial refrigeration also help maintain market leadership. Established insulation material manufacturers, ongoing advancements in material performance, and early adoption of eco-friendly products boost Europe's competitiveness. Together, these factors allow Europe to hold a leading position in the cold insulation material market, supported by steady demand from industrial, commercial, and energy-related sectors.

10

Industry Activity

Recent Developments

The cold insulation material market is evaluated by gathering qualitative and quantitative data post-primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the cold insulation material market are:

- In September 2024, Armacell announced the launch of new aerogel-based insulation technology and expanded its ArmaGel portfolio. This significantly improves thermal performance in cold insulation applications.

- In March 2024, BASF and Shandong Wiskind Architectural Steel Co., Ltd. strengthened their partnership to launch eco-friendly polyurethane (PU) sandwich panels. These panels are designed for cold chain logistics and refrigeration applications, using biomass balance solutions to reduce carbon footprint.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank – Global Trade Indicators World Trade Organization (WTO) International Monetary Fund (IMF) International Trade Administration (ITA) Company Websites Company Annual Reports Company Investor Presentations Global Cold Chain Alliance (GCCA) Thermal Insulation Contractors Association (TICA) Insulation Contractors Association of America (ICAA) European Insulation Manufacturers Association (EURIMA)